Microsoft Boston Consulting Group Matrix

Download Your Competitive Advantage

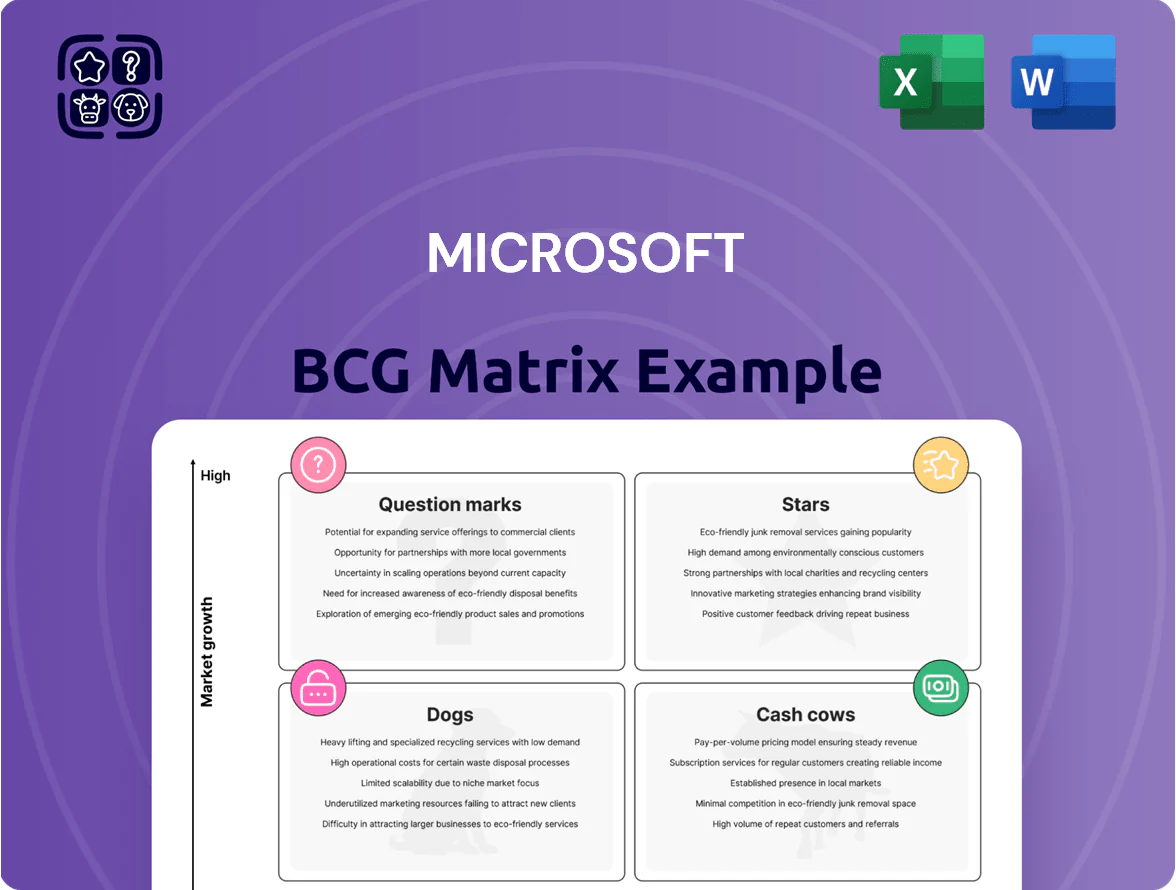

Microsoft’s BCG Matrix snapshot highlights where major product groups—Azure, Office, Windows, LinkedIn, and Gaming—sit in growth and market-share dynamics, revealing which are Stars driving future growth and which are Cash Cows funding investments. This preview teases strategic implications for capital allocation, R&D focus, and portfolio pruning. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Azure Cloud Infrastructure

Azure Cloud Infrastructure is Microsoft’s primary growth engine, capturing nearly 25% of the global cloud market by end-2025 and delivering 34–39% YoY revenue growth in 2025.

Leadership stems from AI-integrated infrastructure; Azure AI services grew about 40% in late 2025, driving enterprise migration of high-value workloads.

Azure demands heavy capital for data-center expansion but generates massive cash inflows, fitting the BCG Star profile.

GitHub Copilot and Developer Tools

GitHub Copilot is a Star: by late 2025 it had over 26 million users, leading the AI-assisted coding market and capturing an estimated 35–40% share of active AI dev-tool users. Its first-mover advantage and deep IDE integrations drove adoption across startups and 70% of Fortune 500 dev teams, lifting subscription revenue to an estimated $420M in FY2025. Continued R&D spend (~$120M annually) is required to fend off rivals, but rapid growth keeps it a high-performing Star.

Dynamics 365 Business Applications

Dynamics 365 outpaced ERP/CRM markets with ~23% revenue growth in 2025 and holds ~25% of the ERP market, driven by AI analytics and tight Microsoft 365 integration that wins midsize and large customers; revenue momentum and Microsoft’s increased R&D spend in FY2025 keep it a high-growth, high-share BCG star, as Microsoft allocated roughly $28B to cloud and AI investments in calendar 2025 to press share gains against SAP and Oracle.

LinkedIn Professional Network

LinkedIn Professional Network (Microsoft) is a Star: 1.2 billion members by end-2025, double-digit annual member growth over four years, and near-monopoly in professional social networking keep rapid user momentum.

Revenue: Marketing Solutions plus Premium subscriptions growing ~10% annually, boosted by AI hiring and sales agents; engagement and ARPU remain above industry average.

Transitioning: strong cash generation positions LinkedIn to become a Cash Cow as regional markets mature but global network effects sustain leadership.

- 1.2B members (2025)

- 4 yrs double-digit growth

- ~10% annual revenue growth (Marketing + Premium)

- High engagement; AI hiring/sales agents driving ARPU

- Star moving toward Cash Cow

Microsoft 365 Commercial Cloud

Microsoft 365 Commercial grows ~15–18% annually, driven by upsells to E5 and Copilot integration; FY2025 Commercial revenue contribution was roughly $70–80B within Microsoft’s Productivity and Business Processes segment.

With ~345 million paid seats as of 2025, it dominates enterprise productivity; net retention stays high, and ARR expansion comes from security, compliance, and AI add-ons.

Though mature, ongoing AI features keep it a Star: high revenue and fast growth but needing heavy investment in GPUs, data centers, and R&D to support Copilot-scale models.

- Growth: 15–18% CAGR

- Paid seats: ~345M (2025)

- Revenue: ~$70–80B (Commercial FY2025 est.)

- Investment: substantial capex for AI infra and R&D

Microsoft Stars: Azure, M365, Copilot, Dynamics & LinkedIn Power Double‑Digit 2025 Growth

Azure, Microsoft 365, GitHub Copilot, Dynamics 365 and LinkedIn are Stars: high market share and 2025 growth—Azure ~25% cloud share, 34–39% YoY; M365 Commercial ~$70–80B, ~345M paid seats, 15–18% CAGR; Copilot ~26M users, ~$420M revenue; Dynamics365 ~25% ERP share, 23% growth; LinkedIn 1.2B members, ~10% revenue growth.

| Product | Share/Users | 2025 Growth | Revenue |

|---|---|---|---|

| Azure | ~25% cloud | 34–39% YoY | — |

| M365 | 345M seats | 15–18% CAGR | $70–80B |

| Copilot | 26M users | — | $420M |

| Dynamics365 | ~25% ERP | 23% | — |

| 1.2B members | ~10% | — |

What is included in the product

BCG Matrix for Microsoft: identifies Stars (Azure, AI), Cash Cows (Windows, Office), Question Marks (Gaming cloud, Surface), Dogs (legacy licenses); strategic investment, hold, or divest guidance tied to market trends.

One-page Microsoft BCG Matrix placing each business unit in a quadrant for instant portfolio clarity.

Cash Cows

Windows OEM and Operating Systems

Windows OEM and desktop OS remain Microsoft’s Cash Cow: Windows held just over 70% global desktop market share in late 2025, anchoring steady OEM licensing revenues that carry gross margins above 70% and contributed roughly $25–30 billion in FY2025 platform licensing revenue to Microsoft’s topline.

Office Consumer and Perpetual Licenses

The consumer Microsoft 365 and perpetual Office licenses are cash cows: 89 million consumer subscribers (Q4 FY2025) with ~8% annual growth in users and low churn, holding dominant share in a saturated productivity market.

They need minimal marketing spend relative to revenue; estimated gross margins above 75% on consumer subscriptions and recurring license renewals provide steady free cash flow to fund cloud and AI investments.

SQL Server and Enterprise On-Premises Software

Microsoft’s on-premises server products like SQL Server and Windows Server still hold roughly 60%–70% market share in enterprise datacenters, supplying steady maintenance and license revenues—Microsoft reported $20.7B in server products and cloud services revenue in FY2024 Q4, much of it recurring—so margins are high and costs low, classifying them as Cash Cows funding Azure growth.

Xbox Content and Services

Xbox Content and Services, driven by Game Pass and first-party titles including Activision Blizzard releases, is a reliable cash cow for Microsoft as hardware sales lag.

Game Pass revenue hit nearly $5.0 billion in 2025, supported by ~30 million subscribers and high retention, while Xbox content sits in a mature market with Microsoft holding a leading share of subscription gaming.

Recurring subscription revenue and strong first-party monetization deliver steady free cash flow and margin stability for Microsoft.

- 2025 Game Pass revenue ~ $5.0B

- ~30M subscribers (2025)

- High retention, recurring cash flow

- First-party IPs boost monetization

Bing Search and News Advertising

Bing Search and News advertising grew ~12% in 2025, boosted by higher revenue per search and AI features in Bing; Microsoft reported search ad revenue of about $14.5B for FY2025, up from $13.0B in FY2024.

As a distant second to Google, Bing remains a stable, high‑margin cash cow within Windows and enterprise deployments, requiring low incremental investment while contributing steady cash flow to Microsoft’s reserves.

- 2025 growth ~12%

- Search ad revenue ≈ $14.5B (FY2025)

- High margins, low incremental capex

- Strong Windows/corporate integration

Microsoft’s 2025 Cash Cows: Windows, M365, Server, Game Pass & Bing Fuel High-Margin Recurring Cash

Windows OEM, Microsoft 365/Office, Server (SQL/Windows Server), Xbox Content/Game Pass, and Bing search are Microsoft cash cows in 2025—generating high-margin, recurring cash: Windows OEM ~$25–30B platform licensing (FY2025), Microsoft 365 consumer 89M subs (Q4 FY2025), Server products recurring revenues (server & cloud ~$20.7B in FY2024 Q4), Game Pass ~$5.0B (2025, ~30M subs), Bing search ~$14.5B (FY2025).

| Business | Key 2025 data | Role |

|---|---|---|

| Windows OEM | ~70% desktop share; $25–30B licensing | High-margin cash |

| Microsoft 365/Office | 89M consumer subs; ~8% YoY growth | Recurring cash |

| Server (SQL/Win) | Server & cloud ~$20.7B (FY2024 Q4) | Maintenance revenue |

| Xbox Content/Game Pass | ~$5.0B revenue; ~30M subs | Subscription cash |

| Bing Search | $14.5B search ads; ~12% growth | High-margin ad cash |

Preview = Final Product

Microsoft BCG Matrix

The file you're previewing on this page is the final BCG Matrix report you'll receive after purchase—no watermarks, no demo content, fully formatted and ready for strategic use. This preview matches the exact downloadable document delivered to your inbox, crafted with market-backed analysis and professional design. Once purchased, the editable, print-ready file is immediately available for presentation, client use, or integration into your planning—no surprises, no revisions required.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

Microsoft’s BCG Matrix snapshot highlights where major product groups—Azure, Office, Windows, LinkedIn, and Gaming—sit in growth and market-share dynamics, revealing which are Stars driving future growth and which are Cash Cows funding investments. This preview teases strategic implications for capital allocation, R&D focus, and portfolio pruning. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Azure Cloud Infrastructure

Azure Cloud Infrastructure is Microsoft’s primary growth engine, capturing nearly 25% of the global cloud market by end-2025 and delivering 34–39% YoY revenue growth in 2025.

Leadership stems from AI-integrated infrastructure; Azure AI services grew about 40% in late 2025, driving enterprise migration of high-value workloads.

Azure demands heavy capital for data-center expansion but generates massive cash inflows, fitting the BCG Star profile.

GitHub Copilot and Developer Tools

GitHub Copilot is a Star: by late 2025 it had over 26 million users, leading the AI-assisted coding market and capturing an estimated 35–40% share of active AI dev-tool users. Its first-mover advantage and deep IDE integrations drove adoption across startups and 70% of Fortune 500 dev teams, lifting subscription revenue to an estimated $420M in FY2025. Continued R&D spend (~$120M annually) is required to fend off rivals, but rapid growth keeps it a high-performing Star.

Dynamics 365 Business Applications

Dynamics 365 outpaced ERP/CRM markets with ~23% revenue growth in 2025 and holds ~25% of the ERP market, driven by AI analytics and tight Microsoft 365 integration that wins midsize and large customers; revenue momentum and Microsoft’s increased R&D spend in FY2025 keep it a high-growth, high-share BCG star, as Microsoft allocated roughly $28B to cloud and AI investments in calendar 2025 to press share gains against SAP and Oracle.

LinkedIn Professional Network

LinkedIn Professional Network (Microsoft) is a Star: 1.2 billion members by end-2025, double-digit annual member growth over four years, and near-monopoly in professional social networking keep rapid user momentum.

Revenue: Marketing Solutions plus Premium subscriptions growing ~10% annually, boosted by AI hiring and sales agents; engagement and ARPU remain above industry average.

Transitioning: strong cash generation positions LinkedIn to become a Cash Cow as regional markets mature but global network effects sustain leadership.

- 1.2B members (2025)

- 4 yrs double-digit growth

- ~10% annual revenue growth (Marketing + Premium)

- High engagement; AI hiring/sales agents driving ARPU

- Star moving toward Cash Cow

Microsoft 365 Commercial Cloud

Microsoft 365 Commercial grows ~15–18% annually, driven by upsells to E5 and Copilot integration; FY2025 Commercial revenue contribution was roughly $70–80B within Microsoft’s Productivity and Business Processes segment.

With ~345 million paid seats as of 2025, it dominates enterprise productivity; net retention stays high, and ARR expansion comes from security, compliance, and AI add-ons.

Though mature, ongoing AI features keep it a Star: high revenue and fast growth but needing heavy investment in GPUs, data centers, and R&D to support Copilot-scale models.

- Growth: 15–18% CAGR

- Paid seats: ~345M (2025)

- Revenue: ~$70–80B (Commercial FY2025 est.)

- Investment: substantial capex for AI infra and R&D

Microsoft Stars: Azure, M365, Copilot, Dynamics & LinkedIn Power Double‑Digit 2025 Growth

Azure, Microsoft 365, GitHub Copilot, Dynamics 365 and LinkedIn are Stars: high market share and 2025 growth—Azure ~25% cloud share, 34–39% YoY; M365 Commercial ~$70–80B, ~345M paid seats, 15–18% CAGR; Copilot ~26M users, ~$420M revenue; Dynamics365 ~25% ERP share, 23% growth; LinkedIn 1.2B members, ~10% revenue growth.

| Product | Share/Users | 2025 Growth | Revenue |

|---|---|---|---|

| Azure | ~25% cloud | 34–39% YoY | — |

| M365 | 345M seats | 15–18% CAGR | $70–80B |

| Copilot | 26M users | — | $420M |

| Dynamics365 | ~25% ERP | 23% | — |

| 1.2B members | ~10% | — |

What is included in the product

BCG Matrix for Microsoft: identifies Stars (Azure, AI), Cash Cows (Windows, Office), Question Marks (Gaming cloud, Surface), Dogs (legacy licenses); strategic investment, hold, or divest guidance tied to market trends.

One-page Microsoft BCG Matrix placing each business unit in a quadrant for instant portfolio clarity.

Cash Cows

Windows OEM and Operating Systems

Windows OEM and desktop OS remain Microsoft’s Cash Cow: Windows held just over 70% global desktop market share in late 2025, anchoring steady OEM licensing revenues that carry gross margins above 70% and contributed roughly $25–30 billion in FY2025 platform licensing revenue to Microsoft’s topline.

Office Consumer and Perpetual Licenses

The consumer Microsoft 365 and perpetual Office licenses are cash cows: 89 million consumer subscribers (Q4 FY2025) with ~8% annual growth in users and low churn, holding dominant share in a saturated productivity market.

They need minimal marketing spend relative to revenue; estimated gross margins above 75% on consumer subscriptions and recurring license renewals provide steady free cash flow to fund cloud and AI investments.

SQL Server and Enterprise On-Premises Software

Microsoft’s on-premises server products like SQL Server and Windows Server still hold roughly 60%–70% market share in enterprise datacenters, supplying steady maintenance and license revenues—Microsoft reported $20.7B in server products and cloud services revenue in FY2024 Q4, much of it recurring—so margins are high and costs low, classifying them as Cash Cows funding Azure growth.

Xbox Content and Services

Xbox Content and Services, driven by Game Pass and first-party titles including Activision Blizzard releases, is a reliable cash cow for Microsoft as hardware sales lag.

Game Pass revenue hit nearly $5.0 billion in 2025, supported by ~30 million subscribers and high retention, while Xbox content sits in a mature market with Microsoft holding a leading share of subscription gaming.

Recurring subscription revenue and strong first-party monetization deliver steady free cash flow and margin stability for Microsoft.

- 2025 Game Pass revenue ~ $5.0B

- ~30M subscribers (2025)

- High retention, recurring cash flow

- First-party IPs boost monetization

Bing Search and News Advertising

Bing Search and News advertising grew ~12% in 2025, boosted by higher revenue per search and AI features in Bing; Microsoft reported search ad revenue of about $14.5B for FY2025, up from $13.0B in FY2024.

As a distant second to Google, Bing remains a stable, high‑margin cash cow within Windows and enterprise deployments, requiring low incremental investment while contributing steady cash flow to Microsoft’s reserves.

- 2025 growth ~12%

- Search ad revenue ≈ $14.5B (FY2025)

- High margins, low incremental capex

- Strong Windows/corporate integration

Microsoft’s 2025 Cash Cows: Windows, M365, Server, Game Pass & Bing Fuel High-Margin Recurring Cash

Windows OEM, Microsoft 365/Office, Server (SQL/Windows Server), Xbox Content/Game Pass, and Bing search are Microsoft cash cows in 2025—generating high-margin, recurring cash: Windows OEM ~$25–30B platform licensing (FY2025), Microsoft 365 consumer 89M subs (Q4 FY2025), Server products recurring revenues (server & cloud ~$20.7B in FY2024 Q4), Game Pass ~$5.0B (2025, ~30M subs), Bing search ~$14.5B (FY2025).

| Business | Key 2025 data | Role |

|---|---|---|

| Windows OEM | ~70% desktop share; $25–30B licensing | High-margin cash |

| Microsoft 365/Office | 89M consumer subs; ~8% YoY growth | Recurring cash |

| Server (SQL/Win) | Server & cloud ~$20.7B (FY2024 Q4) | Maintenance revenue |

| Xbox Content/Game Pass | ~$5.0B revenue; ~30M subs | Subscription cash |

| Bing Search | $14.5B search ads; ~12% growth | High-margin ad cash |

Preview = Final Product

Microsoft BCG Matrix

The file you're previewing on this page is the final BCG Matrix report you'll receive after purchase—no watermarks, no demo content, fully formatted and ready for strategic use. This preview matches the exact downloadable document delivered to your inbox, crafted with market-backed analysis and professional design. Once purchased, the editable, print-ready file is immediately available for presentation, client use, or integration into your planning—no surprises, no revisions required.