Microsoft Porter's Five Forces Analysis

Don't Miss the Bigger Picture

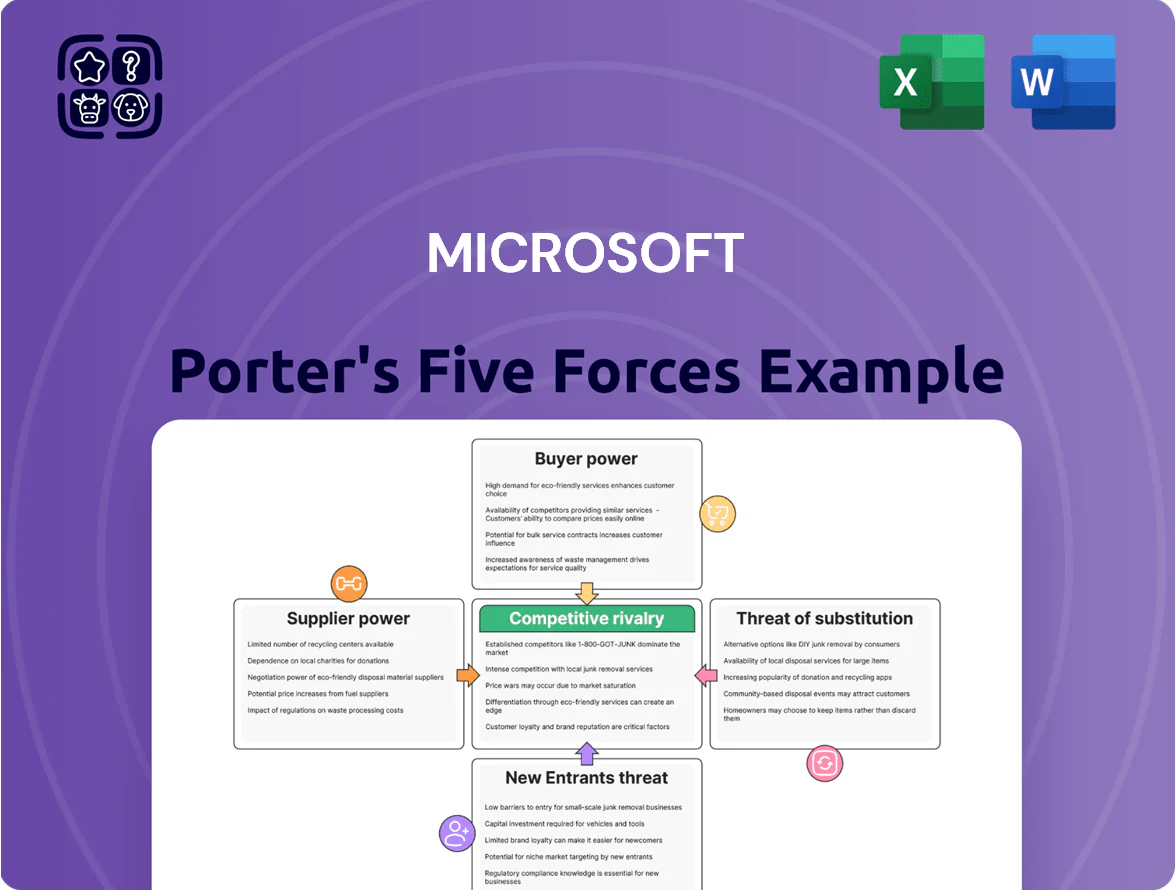

Microsoft operates in a high-stakes tech ecosystem where supplier leverage, buyer power, and platform competition shape strategic choices; its scale and ecosystem advantages mitigate some threats but intensify rivalry and regulatory scrutiny.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Microsoft’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of High-End Semiconductor Manufacturers

The reliance on specialized GPUs for AI and cloud gives a few suppliers—NVIDIA and AMD—major leverage; NVIDIA held ~80% data-center GPU market share in 2024 and set list prices that pushed Azure GPU instance rents up 15–25% YoY.

As Microsoft scales Azure AI, chipmakers control pricing and delivery because global advanced-node foundry capacity was ~90% utilized in 2024, causing multi-quarter lead times.

Microsoft is cutting that supplier power by building custom silicon—Maia and Cobalt—aiming to source >20% of AI inference capacity internally by 2026, reducing vendor dependence.

Global Talent Competition for Specialized Engineering

The global supply of top software engineers, especially in generative AI and cybersecurity, lags demand—LinkedIn reported a 65% year-over-year rise in AI-related talent hires in 2024 while open roles outpaced hires by ~2.5x; this scarcity gives elite engineers leverage as suppliers.

Senior AI researchers and security specialists command total comp packages often exceeding $500k–$1M annually at FAANG and major cloud firms, plus remote and equity flexibility, raising Microsoft’s retention costs.

Microsoft needs sustained investment in pay, stock awards, flexible work, and R&D culture—in 2024 Azure R&D spending rose ~20% to support talent-driven innovation—otherwise attrition risks slowing product leadership.

Energy Providers and Data Center Utilities

The massive data‑center buildout for cloud and AI raises Microsoft’s dependence on local utilities and renewables; as of 2025 Microsoft reported 250+ datacenter regions and expects demand to grow ~30% CAGR through 2028, tightening supplier leverage.

Grid limits and environmental permits constrain site selection and pace; transmission bottlenecks in Texas and Northern Virginia have delayed projects and increased costs by an estimated 10–15% per site in 2023–24.

To reduce supplier power, Microsoft signed 20+ long‑term power purchase agreements totaling ~8.5 GW by end‑2024 and invested in small modular nuclear and fusion R&D partnerships, securing more predictable, low‑carbon supply.

Content Creators and Media Rights Holders

For Xbox and LinkedIn, suppliers are game developers, studios, and content professionals whose work drives engagement; Microsoft paid $68.7B to acquire Activision Blizzard in Oct 2023 to internalize key gaming IP and reduce licensing leverage.

High-quality exclusives give indie studios and IP holders bargaining power—top-tier studios can demand revenue splits, upfront advances, or timed exclusivity, pressuring margins.

Microsoft offsets this by building first-party catalogs (Xbox Game Pass had 30M subscribers in 2023) and long-term licensing deals to secure content pipelines.

- Acquisition reduces supplier leverage

- 30M Game Pass subs strengthen demand

- Exclusives raise negotiation power

- IP ownership cuts licensing costs

Hardware Component Manufacturers for Surface and Xbox

Microsoft depends on a wide network of third-party suppliers for displays, batteries, and sensors; commoditized parts give Microsoft leverage, but bespoke components for high-end Surface models and Xbox (custom SoCs, optical drives) raise supplier power and risk of disruptions.

To mitigate this, Microsoft uses multi-sourcing and logistics partners (by 2024 Microsoft reported >50% of Surface parts multi-sourced) to smooth supply; Xbox production showed a 12% YOY component-cost reduction in 2023 from negotiated volumes.

- Many parts commoditized — lower supplier power

- Specialized components — higher disruption risk

- Multi-sourcing >50% of Surface parts (2024)

- Xbox component costs down 12% YOY (2023)

Microsoft reduces supplier leverage as NVIDIA dominance, foundry strain & AI hiring surge bite

Suppliers wield moderate-to-high power: NVIDIA/AMD dominated data-center GPUs (~80% NVIDIA share in 2024) and constrained foundry capacity (~90% utilization in 2024), while elite AI talent (65% YoY hire rise in 2024) and regional utilities tighten leverage; Microsoft is cutting dependence via Maia/Cobalt (target >20% internal AI inference by 2026), 8.5 GW PPAs (end‑2024), and Activision buy (Oct 2023).

| Metric | Value |

|---|---|

| NVIDIA DC GPU share (2024) | ~80% |

| Foundry utilization (2024) | ~90% |

| AI talent hire rise (LinkedIn 2024) | +65% YoY |

| Internal AI target (2026) | >20% |

| PPAs signed (end‑2024) | 8.5 GW |

What is included in the product

Uncovers the five competitive forces shaping Microsoft's strategy—rivalry, buyer and supplier power, threats from new entrants and substitutes—highlighting key drivers of competition, pricing influence, and entry barriers specific to its cloud, productivity, and platforms businesses.

Condensed Porter's Five Forces for Microsoft—one-sheet clarity to assess competitive threats and strategic levers at a glance.

Customers Bargaining Power

Enterprise Negotiating Power and Volume Discounts

Large corporations and government agencies buying thousands of Microsoft 365 or Azure seats hold strong bargaining power, often securing bespoke pricing and SLAs; in 2024 Microsoft reported over $80B in commercial cloud revenue, reflecting scale that drives volume discounts.

These customers commonly get multi-year enterprise agreements with custom terms and per-user or consumption tiers, and 2023 surveys show 60–70% of large IT buyers negotiate discounts over list prices.

Still, high migration costs—often millions for enterprise-wide migrations plus retraining—limit true exit options, keeping negotiation outcomes favorable to Microsoft.

High Switching Costs and Ecosystem Lock-in

The deep integration of Microsoft’s software suite into business processes creates a strong barrier that lowers customer bargaining power; Microsoft reported 300+ million monthly active Windows 11 devices and 280 million commercial Teams users in 2024, locking workflows into its stack. Once firms build data architecture on Azure—which held about 23% global cloud IaaS market share in 2024—or run communications on Teams, migration and retraining costs often exceed millions and months of downtime. This ecosystem stickiness sustains Microsoft’s pricing power, letting it raise enterprise prices while retaining renewal rates above 90% in many commercial segments.

Individual Consumer Price Sensitivity in Hardware

Individual consumers hold strong bargaining power in Surface and Xbox retail markets because abundant alternatives—Apple and Dell for laptops, Sony and Nintendo for consoles—drive price and feature sensitivity; US consumer surveys in 2024 showed 68% switch for better specs or price.

Microsoft pressures margins to stay competitive, often subsidizing hardware: Xbox Series X/S and Surface margins tightened after 2023 pricing moves; Game Pass and Surface-exclusive features boost loyalty and cut churn risk.

SME Access to Standardized Cloud Solutions

SME access to standardized cloud solutions lets buyers compare Microsoft 365 and Azure against Google Workspace and AWS easily, raising price sensitivity; McKinsey estimated in 2024 that 60% of SMEs shop across 2+ vendors before buying.

Individually SMEs lack volume to force discounts, but collectively churn keeps Microsoft under pressure—IDC found SMB churn in SaaS markets rose to 12% in 2023.

Microsoft counters with tiered pricing and bundles—Microsoft reported in FY2024 that SMB-focused offers grew commercial seats by double digits, showing value delivery for smaller budgets.

- 60% of SMEs compare multiple vendors (McKinsey 2024)

- SMB SaaS churn ~12% (IDC 2023)

- Microsoft FY2024: double-digit SMB seat growth

Subscription Fatigue and Renewal Risks

Microsoft’s cloud dominance: high stickiness, strong enterprise pricing power

Large enterprise deals wield strong bargaining power via bespoke pricing and SLAs, yet high migration/retraining costs and Microsoft’s ecosystem stickiness (Azure ~23% IaaS 2024; commercial cloud $104.4B FY2024; Teams 280M commercial users) limit exits; SMEs compare vendors (60% McKinsey 2024) raising price sensitivity, while ~90% enterprise renewal rates and Copilot tie-ins sustain Microsoft’s pricing power.

| Metric | 2023–2024 |

|---|---|

| Commercial cloud rev | $104.4B FY2024 |

| Azure IaaS share | ~23% 2024 |

| Teams commercial users | 280M 2024 |

| SMEs comparing vendors | 60% (McKinsey 2024) |

| Enterprise renewal rate | ~90% 2024 |

Full Version Awaits

Microsoft Porter's Five Forces Analysis

This preview shows the exact Microsoft Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is the full, professionally formatted file ready for download and use the moment you buy. It contains the complete competitive assessment, supporting insights, and actionable implications for strategy and investment decisions. You’re viewing the actual deliverable you'll get instantly after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Microsoft operates in a high-stakes tech ecosystem where supplier leverage, buyer power, and platform competition shape strategic choices; its scale and ecosystem advantages mitigate some threats but intensify rivalry and regulatory scrutiny.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Microsoft’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of High-End Semiconductor Manufacturers

The reliance on specialized GPUs for AI and cloud gives a few suppliers—NVIDIA and AMD—major leverage; NVIDIA held ~80% data-center GPU market share in 2024 and set list prices that pushed Azure GPU instance rents up 15–25% YoY.

As Microsoft scales Azure AI, chipmakers control pricing and delivery because global advanced-node foundry capacity was ~90% utilized in 2024, causing multi-quarter lead times.

Microsoft is cutting that supplier power by building custom silicon—Maia and Cobalt—aiming to source >20% of AI inference capacity internally by 2026, reducing vendor dependence.

Global Talent Competition for Specialized Engineering

The global supply of top software engineers, especially in generative AI and cybersecurity, lags demand—LinkedIn reported a 65% year-over-year rise in AI-related talent hires in 2024 while open roles outpaced hires by ~2.5x; this scarcity gives elite engineers leverage as suppliers.

Senior AI researchers and security specialists command total comp packages often exceeding $500k–$1M annually at FAANG and major cloud firms, plus remote and equity flexibility, raising Microsoft’s retention costs.

Microsoft needs sustained investment in pay, stock awards, flexible work, and R&D culture—in 2024 Azure R&D spending rose ~20% to support talent-driven innovation—otherwise attrition risks slowing product leadership.

Energy Providers and Data Center Utilities

The massive data‑center buildout for cloud and AI raises Microsoft’s dependence on local utilities and renewables; as of 2025 Microsoft reported 250+ datacenter regions and expects demand to grow ~30% CAGR through 2028, tightening supplier leverage.

Grid limits and environmental permits constrain site selection and pace; transmission bottlenecks in Texas and Northern Virginia have delayed projects and increased costs by an estimated 10–15% per site in 2023–24.

To reduce supplier power, Microsoft signed 20+ long‑term power purchase agreements totaling ~8.5 GW by end‑2024 and invested in small modular nuclear and fusion R&D partnerships, securing more predictable, low‑carbon supply.

Content Creators and Media Rights Holders

For Xbox and LinkedIn, suppliers are game developers, studios, and content professionals whose work drives engagement; Microsoft paid $68.7B to acquire Activision Blizzard in Oct 2023 to internalize key gaming IP and reduce licensing leverage.

High-quality exclusives give indie studios and IP holders bargaining power—top-tier studios can demand revenue splits, upfront advances, or timed exclusivity, pressuring margins.

Microsoft offsets this by building first-party catalogs (Xbox Game Pass had 30M subscribers in 2023) and long-term licensing deals to secure content pipelines.

- Acquisition reduces supplier leverage

- 30M Game Pass subs strengthen demand

- Exclusives raise negotiation power

- IP ownership cuts licensing costs

Hardware Component Manufacturers for Surface and Xbox

Microsoft depends on a wide network of third-party suppliers for displays, batteries, and sensors; commoditized parts give Microsoft leverage, but bespoke components for high-end Surface models and Xbox (custom SoCs, optical drives) raise supplier power and risk of disruptions.

To mitigate this, Microsoft uses multi-sourcing and logistics partners (by 2024 Microsoft reported >50% of Surface parts multi-sourced) to smooth supply; Xbox production showed a 12% YOY component-cost reduction in 2023 from negotiated volumes.

- Many parts commoditized — lower supplier power

- Specialized components — higher disruption risk

- Multi-sourcing >50% of Surface parts (2024)

- Xbox component costs down 12% YOY (2023)

Microsoft reduces supplier leverage as NVIDIA dominance, foundry strain & AI hiring surge bite

Suppliers wield moderate-to-high power: NVIDIA/AMD dominated data-center GPUs (~80% NVIDIA share in 2024) and constrained foundry capacity (~90% utilization in 2024), while elite AI talent (65% YoY hire rise in 2024) and regional utilities tighten leverage; Microsoft is cutting dependence via Maia/Cobalt (target >20% internal AI inference by 2026), 8.5 GW PPAs (end‑2024), and Activision buy (Oct 2023).

| Metric | Value |

|---|---|

| NVIDIA DC GPU share (2024) | ~80% |

| Foundry utilization (2024) | ~90% |

| AI talent hire rise (LinkedIn 2024) | +65% YoY |

| Internal AI target (2026) | >20% |

| PPAs signed (end‑2024) | 8.5 GW |

What is included in the product

Uncovers the five competitive forces shaping Microsoft's strategy—rivalry, buyer and supplier power, threats from new entrants and substitutes—highlighting key drivers of competition, pricing influence, and entry barriers specific to its cloud, productivity, and platforms businesses.

Condensed Porter's Five Forces for Microsoft—one-sheet clarity to assess competitive threats and strategic levers at a glance.

Customers Bargaining Power

Enterprise Negotiating Power and Volume Discounts

Large corporations and government agencies buying thousands of Microsoft 365 or Azure seats hold strong bargaining power, often securing bespoke pricing and SLAs; in 2024 Microsoft reported over $80B in commercial cloud revenue, reflecting scale that drives volume discounts.

These customers commonly get multi-year enterprise agreements with custom terms and per-user or consumption tiers, and 2023 surveys show 60–70% of large IT buyers negotiate discounts over list prices.

Still, high migration costs—often millions for enterprise-wide migrations plus retraining—limit true exit options, keeping negotiation outcomes favorable to Microsoft.

High Switching Costs and Ecosystem Lock-in

The deep integration of Microsoft’s software suite into business processes creates a strong barrier that lowers customer bargaining power; Microsoft reported 300+ million monthly active Windows 11 devices and 280 million commercial Teams users in 2024, locking workflows into its stack. Once firms build data architecture on Azure—which held about 23% global cloud IaaS market share in 2024—or run communications on Teams, migration and retraining costs often exceed millions and months of downtime. This ecosystem stickiness sustains Microsoft’s pricing power, letting it raise enterprise prices while retaining renewal rates above 90% in many commercial segments.

Individual Consumer Price Sensitivity in Hardware

Individual consumers hold strong bargaining power in Surface and Xbox retail markets because abundant alternatives—Apple and Dell for laptops, Sony and Nintendo for consoles—drive price and feature sensitivity; US consumer surveys in 2024 showed 68% switch for better specs or price.

Microsoft pressures margins to stay competitive, often subsidizing hardware: Xbox Series X/S and Surface margins tightened after 2023 pricing moves; Game Pass and Surface-exclusive features boost loyalty and cut churn risk.

SME Access to Standardized Cloud Solutions

SME access to standardized cloud solutions lets buyers compare Microsoft 365 and Azure against Google Workspace and AWS easily, raising price sensitivity; McKinsey estimated in 2024 that 60% of SMEs shop across 2+ vendors before buying.

Individually SMEs lack volume to force discounts, but collectively churn keeps Microsoft under pressure—IDC found SMB churn in SaaS markets rose to 12% in 2023.

Microsoft counters with tiered pricing and bundles—Microsoft reported in FY2024 that SMB-focused offers grew commercial seats by double digits, showing value delivery for smaller budgets.

- 60% of SMEs compare multiple vendors (McKinsey 2024)

- SMB SaaS churn ~12% (IDC 2023)

- Microsoft FY2024: double-digit SMB seat growth

Subscription Fatigue and Renewal Risks

Microsoft’s cloud dominance: high stickiness, strong enterprise pricing power

Large enterprise deals wield strong bargaining power via bespoke pricing and SLAs, yet high migration/retraining costs and Microsoft’s ecosystem stickiness (Azure ~23% IaaS 2024; commercial cloud $104.4B FY2024; Teams 280M commercial users) limit exits; SMEs compare vendors (60% McKinsey 2024) raising price sensitivity, while ~90% enterprise renewal rates and Copilot tie-ins sustain Microsoft’s pricing power.

| Metric | 2023–2024 |

|---|---|

| Commercial cloud rev | $104.4B FY2024 |

| Azure IaaS share | ~23% 2024 |

| Teams commercial users | 280M 2024 |

| SMEs comparing vendors | 60% (McKinsey 2024) |

| Enterprise renewal rate | ~90% 2024 |

Full Version Awaits

Microsoft Porter's Five Forces Analysis

This preview shows the exact Microsoft Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is the full, professionally formatted file ready for download and use the moment you buy. It contains the complete competitive assessment, supporting insights, and actionable implications for strategy and investment decisions. You’re viewing the actual deliverable you'll get instantly after payment.