Midland States Bank PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Gain a competitive edge with our focused PESTLE Analysis of Midland States Bank—uncover how regulatory shifts, economic cycles, and tech adoption will shape its strategic path and risk profile. Ideal for investors, advisors, and strategists, this concise briefing highlights key external drivers and actionable implications. Purchase the full report to access detailed insights, data-driven forecasts, and ready-to-use slides for decision-making.

Political factors

Post-Election Regulatory Shifts

The 2024 federal elections shifted regulatory focus, with Congressional hearings up 18% in 2025 and proposed CFPB/OCC budget adjustments of +6% and +4% respectively for 2026, requiring Midland States Bank to prepare for tighter oversight.

Potential leadership changes at CFPB and OCC could increase exam frequency—regional bank examinations rose 12% in 2025—affecting Midland’s compliance costs and capital planning.

Regulatory shifts also influence deal timelines: bank M&A approvals averaged 210 days in 2025, so Midland must factor longer review periods into acquisition and product-launch schedules.

Midwestern State Fiscal Policies

Operating across Illinois, Indiana, and Missouri exposes Midland States Bank to varied state political environments and tax structures; Illinois's FY2025 budget deficit concerns and Missouri's 2024 corporate tax rate of 4% vs Indiana's 3.23% affect net margins and pricing of loans.

State budget decisions and possible Illinois pension-related fiscal measures influence municipal credit quality and deposit flows—Illinois had $20B in unpaid pension liabilities as of 2024.

Management must track legislative sessions in Springfield and Indianapolis to anticipate shifts in public-sector deposit requirements and lending demand tied to state-funded infrastructure and education spending.

Federal Agricultural Support Programs

Federal farm bill negotiations remain crucial for Midland States Bank given heavy exposure in Iowa and Wisconsin; the 2023 farm bill authorized roughly $114 billion over five years for commodity programs and subsidies, directly underpinning many ag borrowers' cash flows.

USDA crop insurance covered 1.1 million policies in 2024 with $124 billion in liability, offering a credit backstop for the bank's ag loan book.

Political volatility over trade deals or tariffs—soybean exports fell 7% in 2024 vs 2023 after tariff disputes—can quickly erode commodity prices and materially impair credit quality in ag portfolios.

Small Business Administration Policy Changes

Midland States Bank originates SBA loans—over $120m in SBA-backed volume during FY2024—so federal shifts to funding or guarantee rates directly affect its commercial lending capacity and credit risk appetite.

Changes reducing guarantees would likely compress SBA originations; increases tied to Midwestern manufacturing revitalization programs could boost small-scale retail and manufacturing loans in Illinois and adjacent states.

Strategists must monitor Congress and SBA rulemaking, including 2024 proposed budget allocations and the SBA guarantee rate history (generally 75–90%) to align pipeline and capital planning.

- FY2024 SBA volume ~ $120m

- SBA guarantee range historically 75–90%

- Funding/guarantee cuts reduce lending; increases fuel regional lending growth

- Track congressional budgets and SBA rule changes

Infrastructure Spending and Public-Private Partnerships

Rising regulatory scrutiny, longer M&A reviews, and mounting muni & federal credit risks

Political shifts (2024–2026) raise oversight and cost risks: CFPB/OCC budgets +6%/+4% proposed for 2026, regional exams +12% in 2025, bank M&A avg approval 210 days (2025). Illinois pension shortfall $20B (2024) and state capital plans $10–25B (2025–26) affect muni credit and infrastructure lending; FY2024 SBA volume ~$120M; USDA crop-insurance liability $124B (2024).

| Metric | Value |

|---|---|

| CFPB/OCC budget change (proposed) | +6%/+4% (2026) |

| Regional exams | +12% (2025) |

| Bank M&A review | 210 days (2025) |

| Illinois pension gap | $20B (2024) |

| SBA volume FY2024 | $120M |

| USDA insurance liability | $124B (2024) |

What is included in the product

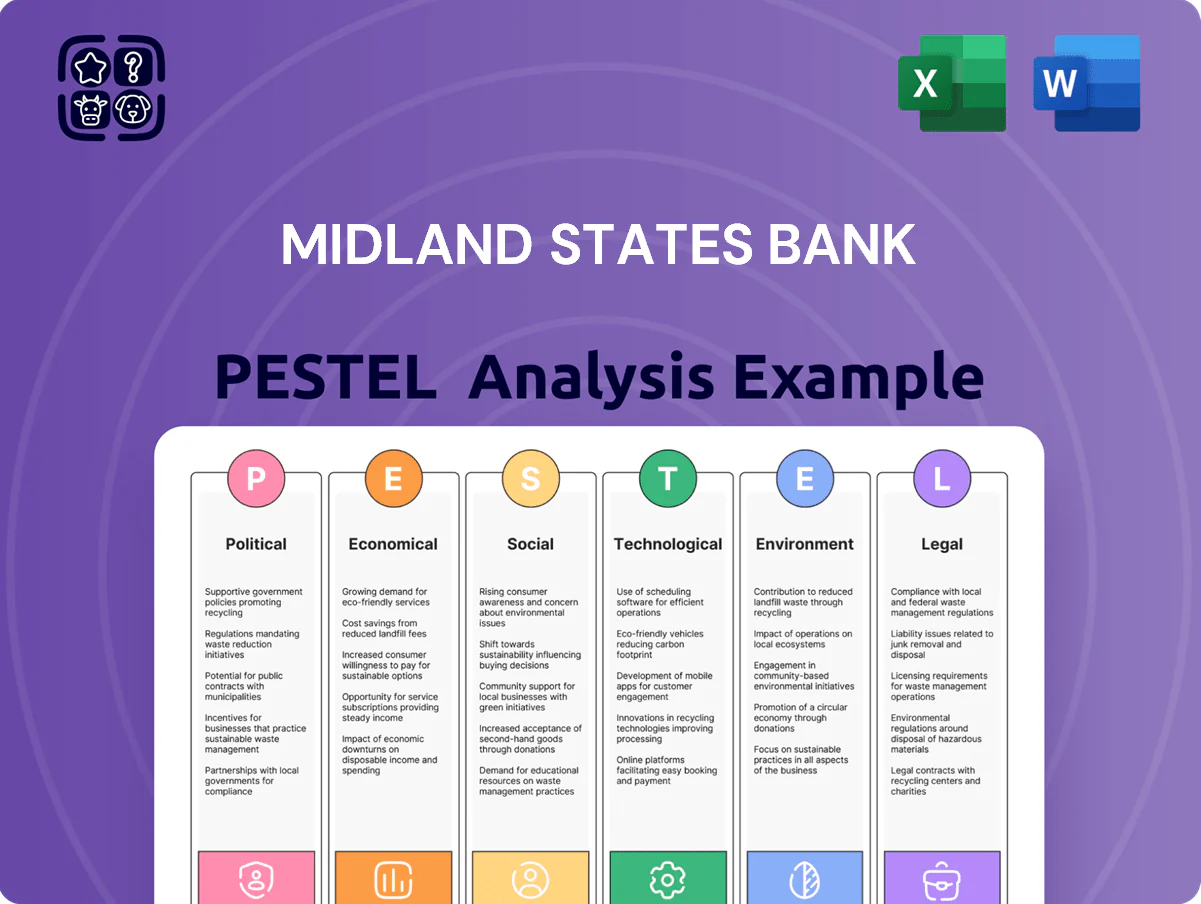

Explores how Political, Economic, Social, Technological, Environmental, and Legal factors uniquely impact Midland States Bank, with each category supported by regional data and current trends to identify risks and opportunities.

A concise, PESTLE-segmented summary of Midland States Bank that simplifies external risk, regulatory and market insights for quick insertion into presentations, team planning, or client reports—editable for local context and easily shared across devices.

Economic factors

Interest Rate Environment Stabilization

As of late 2025, Federal Reserve rate stabilization near 5.25%–5.50% has improved predictability for Midland States Bank's Net Interest Margin management, after the 2022–24 tightening cycle trimmed margins industry-wide.

Midland must balance deposit costs—average consumer deposit betas rose to ~45% in 2024—with loan yields (commercial loan yields in the Midwest averaged ~6.2% in 2025) to preserve profitability.

This backdrop has cooled mortgage demand—national purchase mortgage applications were down ~12% year‑over‑year in 2025—while modestly lifting Midwestern business capital spending intentions, with regional C&I loan demand up ~4% in 2025.

Midwestern Agricultural Commodity Prices

Midland States Bank's footprint is highly sensitive to corn, soybean and livestock prices; corn futures averaged about $5.10/bu and soybeans $13.50/bu in 2025, while feeder cattle hovered near $190/cwt, directly impacting clients' cash flows and debt-service coverage ratios.

Volatility from 2024–25—driven by Black Sea trade shifts, Brazilian crop forecasts and extreme Midwest weather—requires bank economists to monitor global supply chains and NOAA/USDA reports to manage agricultural credit risk.

Commercial Real Estate Market Dynamics

The evolving office/retail mix is pressuring CRE collateral values; U.S. office vacancy averaged 18.8% in Q4 2025 while Chicago and St. Louis metro vacancy rates exceeded 20% and 19% respectively, contributing to regional price discounts of 10–18% year-over-year. Midland States Bank’s Midwest suburban CRE showed steadier fundamentals, but elevated urban vacancies necessitate rigorous stress testing against 30–40% downside scenarios. Proactive portfolio management and higher LTV/coverage thresholds are required to mitigate potential losses from devaluations.

Labor Market and Wage Growth Trends

- Wage growth: +3.8–4.2% (2025)

- Unemployment: ~3.6% (IL/WI, 2025)

- Efficiency ratio: ~63% (FY2024)

- Core deposits growth: ~5.1% (2024)

Equipment Leasing Demand Cycles

Midland States Banks specialized equipment leasing is cyclical, rising with regional manufacturing upswings; U.S. manufacturing output grew 2.1% in 2024, supporting higher lease originations.

During downturns or when borrowing costs rose—benchmark Fed funds peaking at 5.5% in 2024—lease demand contracted, pushing Midland to diversify across construction, medical, and tech sectors.

- Lease originations linked to manufacturing growth (2024 US manufacturing +2.1%)

- Rate sensitivity: Fed funds ~5.5% (2024) reduced demand

- Strategy: diversify into construction, healthcare, tech leases

Stable Fed, Tight Margins: Midwest Banks Face CRE, Ag Price Credit Risks

Stable Fed rates near 5.25–5.50% (late 2025) aid NIM predictability; deposit betas ~45% (2024) vs. commercial loan yields ~6.2% (Midwest, 2025) squeeze margins; ag commodity prices (corn $5.10/bu, soy $13.50/bu, feeder cattle $190/cwt, 2025) and CRE vacancies (US office 18.8%, Chicago >20%, Q4 2025) elevate credit risk; unemployment ~3.6% (IL/WI, 2025) supports deposits and loan performance.

| Metric | Value |

|---|---|

| Fed funds (late 2025) | 5.25–5.50% |

| Deposit beta (2024) | ~45% |

| Midwest C&I yield (2025) | ~6.2% |

| Corn / Soy (2025) | $5.10 / $13.50 per bu |

| Office vacancy (US / Chicago) | 18.8% / >20% |

| Unemployment (IL/WI, 2025) | ~3.6% |

Preview the Actual Deliverable

Midland States Bank PESTLE Analysis

The preview shown here is the exact Midland States Bank PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Gain a competitive edge with our focused PESTLE Analysis of Midland States Bank—uncover how regulatory shifts, economic cycles, and tech adoption will shape its strategic path and risk profile. Ideal for investors, advisors, and strategists, this concise briefing highlights key external drivers and actionable implications. Purchase the full report to access detailed insights, data-driven forecasts, and ready-to-use slides for decision-making.

Political factors

Post-Election Regulatory Shifts

The 2024 federal elections shifted regulatory focus, with Congressional hearings up 18% in 2025 and proposed CFPB/OCC budget adjustments of +6% and +4% respectively for 2026, requiring Midland States Bank to prepare for tighter oversight.

Potential leadership changes at CFPB and OCC could increase exam frequency—regional bank examinations rose 12% in 2025—affecting Midland’s compliance costs and capital planning.

Regulatory shifts also influence deal timelines: bank M&A approvals averaged 210 days in 2025, so Midland must factor longer review periods into acquisition and product-launch schedules.

Midwestern State Fiscal Policies

Operating across Illinois, Indiana, and Missouri exposes Midland States Bank to varied state political environments and tax structures; Illinois's FY2025 budget deficit concerns and Missouri's 2024 corporate tax rate of 4% vs Indiana's 3.23% affect net margins and pricing of loans.

State budget decisions and possible Illinois pension-related fiscal measures influence municipal credit quality and deposit flows—Illinois had $20B in unpaid pension liabilities as of 2024.

Management must track legislative sessions in Springfield and Indianapolis to anticipate shifts in public-sector deposit requirements and lending demand tied to state-funded infrastructure and education spending.

Federal Agricultural Support Programs

Federal farm bill negotiations remain crucial for Midland States Bank given heavy exposure in Iowa and Wisconsin; the 2023 farm bill authorized roughly $114 billion over five years for commodity programs and subsidies, directly underpinning many ag borrowers' cash flows.

USDA crop insurance covered 1.1 million policies in 2024 with $124 billion in liability, offering a credit backstop for the bank's ag loan book.

Political volatility over trade deals or tariffs—soybean exports fell 7% in 2024 vs 2023 after tariff disputes—can quickly erode commodity prices and materially impair credit quality in ag portfolios.

Small Business Administration Policy Changes

Midland States Bank originates SBA loans—over $120m in SBA-backed volume during FY2024—so federal shifts to funding or guarantee rates directly affect its commercial lending capacity and credit risk appetite.

Changes reducing guarantees would likely compress SBA originations; increases tied to Midwestern manufacturing revitalization programs could boost small-scale retail and manufacturing loans in Illinois and adjacent states.

Strategists must monitor Congress and SBA rulemaking, including 2024 proposed budget allocations and the SBA guarantee rate history (generally 75–90%) to align pipeline and capital planning.

- FY2024 SBA volume ~ $120m

- SBA guarantee range historically 75–90%

- Funding/guarantee cuts reduce lending; increases fuel regional lending growth

- Track congressional budgets and SBA rule changes

Infrastructure Spending and Public-Private Partnerships

Rising regulatory scrutiny, longer M&A reviews, and mounting muni & federal credit risks

Political shifts (2024–2026) raise oversight and cost risks: CFPB/OCC budgets +6%/+4% proposed for 2026, regional exams +12% in 2025, bank M&A avg approval 210 days (2025). Illinois pension shortfall $20B (2024) and state capital plans $10–25B (2025–26) affect muni credit and infrastructure lending; FY2024 SBA volume ~$120M; USDA crop-insurance liability $124B (2024).

| Metric | Value |

|---|---|

| CFPB/OCC budget change (proposed) | +6%/+4% (2026) |

| Regional exams | +12% (2025) |

| Bank M&A review | 210 days (2025) |

| Illinois pension gap | $20B (2024) |

| SBA volume FY2024 | $120M |

| USDA insurance liability | $124B (2024) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal factors uniquely impact Midland States Bank, with each category supported by regional data and current trends to identify risks and opportunities.

A concise, PESTLE-segmented summary of Midland States Bank that simplifies external risk, regulatory and market insights for quick insertion into presentations, team planning, or client reports—editable for local context and easily shared across devices.

Economic factors

Interest Rate Environment Stabilization

As of late 2025, Federal Reserve rate stabilization near 5.25%–5.50% has improved predictability for Midland States Bank's Net Interest Margin management, after the 2022–24 tightening cycle trimmed margins industry-wide.

Midland must balance deposit costs—average consumer deposit betas rose to ~45% in 2024—with loan yields (commercial loan yields in the Midwest averaged ~6.2% in 2025) to preserve profitability.

This backdrop has cooled mortgage demand—national purchase mortgage applications were down ~12% year‑over‑year in 2025—while modestly lifting Midwestern business capital spending intentions, with regional C&I loan demand up ~4% in 2025.

Midwestern Agricultural Commodity Prices

Midland States Bank's footprint is highly sensitive to corn, soybean and livestock prices; corn futures averaged about $5.10/bu and soybeans $13.50/bu in 2025, while feeder cattle hovered near $190/cwt, directly impacting clients' cash flows and debt-service coverage ratios.

Volatility from 2024–25—driven by Black Sea trade shifts, Brazilian crop forecasts and extreme Midwest weather—requires bank economists to monitor global supply chains and NOAA/USDA reports to manage agricultural credit risk.

Commercial Real Estate Market Dynamics

The evolving office/retail mix is pressuring CRE collateral values; U.S. office vacancy averaged 18.8% in Q4 2025 while Chicago and St. Louis metro vacancy rates exceeded 20% and 19% respectively, contributing to regional price discounts of 10–18% year-over-year. Midland States Bank’s Midwest suburban CRE showed steadier fundamentals, but elevated urban vacancies necessitate rigorous stress testing against 30–40% downside scenarios. Proactive portfolio management and higher LTV/coverage thresholds are required to mitigate potential losses from devaluations.

Labor Market and Wage Growth Trends

- Wage growth: +3.8–4.2% (2025)

- Unemployment: ~3.6% (IL/WI, 2025)

- Efficiency ratio: ~63% (FY2024)

- Core deposits growth: ~5.1% (2024)

Equipment Leasing Demand Cycles

Midland States Banks specialized equipment leasing is cyclical, rising with regional manufacturing upswings; U.S. manufacturing output grew 2.1% in 2024, supporting higher lease originations.

During downturns or when borrowing costs rose—benchmark Fed funds peaking at 5.5% in 2024—lease demand contracted, pushing Midland to diversify across construction, medical, and tech sectors.

- Lease originations linked to manufacturing growth (2024 US manufacturing +2.1%)

- Rate sensitivity: Fed funds ~5.5% (2024) reduced demand

- Strategy: diversify into construction, healthcare, tech leases

Stable Fed, Tight Margins: Midwest Banks Face CRE, Ag Price Credit Risks

Stable Fed rates near 5.25–5.50% (late 2025) aid NIM predictability; deposit betas ~45% (2024) vs. commercial loan yields ~6.2% (Midwest, 2025) squeeze margins; ag commodity prices (corn $5.10/bu, soy $13.50/bu, feeder cattle $190/cwt, 2025) and CRE vacancies (US office 18.8%, Chicago >20%, Q4 2025) elevate credit risk; unemployment ~3.6% (IL/WI, 2025) supports deposits and loan performance.

| Metric | Value |

|---|---|

| Fed funds (late 2025) | 5.25–5.50% |

| Deposit beta (2024) | ~45% |

| Midwest C&I yield (2025) | ~6.2% |

| Corn / Soy (2025) | $5.10 / $13.50 per bu |

| Office vacancy (US / Chicago) | 18.8% / >20% |

| Unemployment (IL/WI, 2025) | ~3.6% |

Preview the Actual Deliverable

Midland States Bank PESTLE Analysis

The preview shown here is the exact Midland States Bank PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.