Mid Penn Bank Boston Consulting Group Matrix

See the Bigger Picture

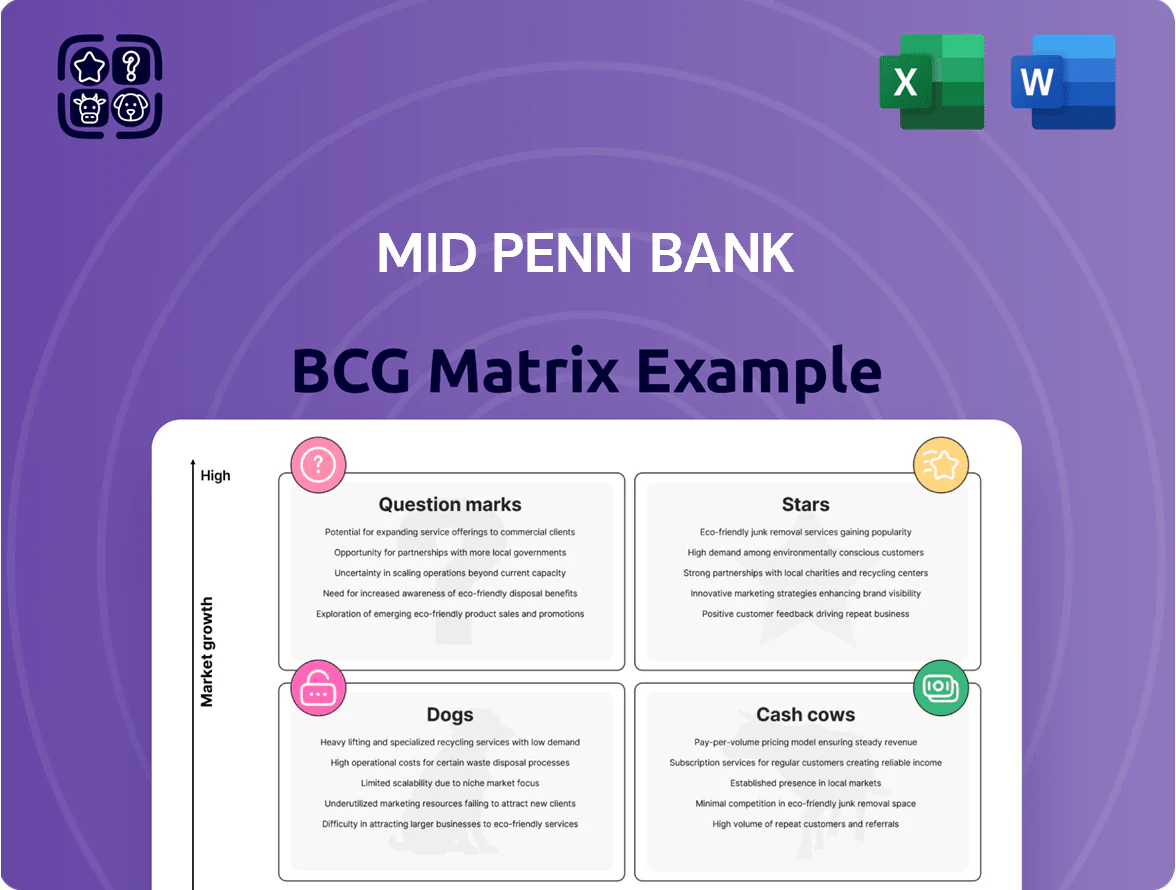

Mid Penn Bank’s BCG Matrix preview highlights where core business lines likely sit—stable Cash Cows from retail deposits, high-potential Stars in digital lending, and possible Question Marks in niche commercial services—offering a snapshot of resource allocation priorities and growth levers. This high-level view teases quadrant placements and strategic implications; purchase the full BCG Matrix for a complete, data-driven breakdown, quadrant-by-quadrant recommendations, and editable Word and Excel deliverables to guide confident investment and strategic decisions.

Stars

Commercial Real Estate and Construction Lending

Mid Penn Bank leads CRE and construction lending, with these loans making up 65% of its total loan portfolio as of 2025 and driving strong interest income.

Late-2025 industry data shows a 40% jump in U.S. commercial mortgage originations, placing this segment in a high-growth quadrant of the BCG matrix.

Local decision-making and CRE expertise let Mid Penn capture share from larger banks, though ongoing capital injections are needed to fund metro expansions.

Greater Philadelphia Market Expansion

Through the 2025 acquisition of William Penn Bancorp, Mid Penn nearly doubled its Greater Philadelphia assets to about $1.8 billion, adding 12 branches and mass‑affluent clients—transforming this region into a BCG Matrix Star. The bank is targeting $5 billion in regional assets, pursuing aggressive deposit and loan growth in a metro area with 2024–25 population growth of ~0.8% annually and strong suburban housing demand. Significant marketing, branch rebranding, employee integration, and IT consolidation spend is underway to capture share in one of the nation’s most competitive banking corridors.

SBA and Specialty Commercial Lending

SBA and specialty commercial lending—notably healthcare and professional services—are Mid Penn Bank’s fastest-growing segments; SBA originations grew 22% in 2024 to $420 million, making Mid Penn the top community-bank SBA lender in Pennsylvania by volume.

For 2025 Mid Penn prioritizes these higher-yielding assets to offset net interest margin compression (NIM fell to 2.45% in 2024); niche focus aids yield diversification despite higher underwriting and marketing cash needs.

Digital Banking and Treasury Services

Digital Banking and Treasury Services is a Star: platform adoption rose 22% Y/Y in 2025, driving new commercial client wins and higher fee income as average treasury revenue per commercial client grew 14% to $8,600 annually.

Real-time payment rails and automated receivables keep Mid Penn competitive; as a regional first-mover, it gained ~2.1 percentage points market share vs. traditional banks in 2024–25.

Ongoing capital required: estimated $6–8m annual spend on cybersecurity and software updates, but anticipated cost-to-serve falls 18% over three years, supporting long-term margins.

- 22% platform adoption increase (2025)

- $8,600 avg treasury revenue per client

- +2.1 ppt market share vs peers (2024–25)

- $6–8m annual tech/cyber spend

- 18% projected cost-to-serve reduction in 3 years

New Jersey Market Penetration

Following the 2024 Brunswick Bancorp acquisition and 2025 integrations, Mid Penn Bank targets Central and Southern New Jersey as a high-growth Stars segment in the BCG matrix, aiming for >15% deposit CAGR and 8–10% loan growth versus 3–4% in legacy markets.

These corridors host a denser base of tech SMEs and affluent households—Mercer, Middlesex, and Burlington counties show median household incomes 20–35% above Mid Penn’s Pennsylvania footprint—so the bank is building de novo centers and local BD teams.

Initial operations are cash-heavy: estimated startup and branding spend of $45–60M through 2026, pressuring near-term margins but targeting ~200–300 bps higher NIMs long term and market-leading share within 5–7 years.

- 2024 acquisition closed; 2025 integrations complete

- Target: >15% deposit CAGR; 8–10% loan growth

- Estimated $45–60M upfront spend to 2026

- Targets +200–300 bps NIM lift; 5–7 year dominance

Mid Penn: CRE-led growth, digital treasury gains, NJ rollout targets >15% deposit CAGR

Mid Penn’s Stars: CRE/construction, digital treasury, and NJ/Philly metros drive high growth and share; CRE = 65% loans (2025), treasury revenue $8,600/client, platform adoption +22% (2025), SBA originations $420M (2024). Capital push: $6–8M/yr tech spend; $45–60M NJ rollout to 2026 targeting >15% deposit CAGR.

| Metric | Value |

|---|---|

| CRE share | 65% |

| Platform adoption | +22% (2025) |

| SBA originations | $420M (2024) |

| Tech spend | $6–8M/yr |

| NJ rollout spend | $45–60M |

What is included in the product

Comprehensive BCG Matrix review of Mid Penn Bank’s units with strategic guidance on Stars, Cash Cows, Question Marks, and Dogs.

One-page BCG matrix placing Mid Penn Bank units into quadrants for quick strategy decisions, export-ready for PowerPoint.

Cash Cows

Core Central Pennsylvania Deposit Base

Mid Penn Bank holds top-three deposit market share in Dauphin, Lancaster, Cumberland, and Schuylkill counties, supplying a stable, low-cost funding base that supported 62% of deposit funding in 2024 and lowered cost of funds to 0.85% that year.

These mature markets need minimal marketing spend, deliver consistent high-margin cash flow—net interest margin of 3.45% in 2024—and let the bank "milk" legacy deposits to finance growth.

The core deposit cash cow primarily funds dividends (2024 payout ratio 48%) and the 2023–2025 acquisition plan, which targets $350m in deal size to expand into adjacent regions.

Traditional Residential Mortgages

As of 2025, Mid Penn Bank’s traditional residential mortgages—holding ~28% share of its loan book—generate steady net interest margin income (~3.1% NIM) and $4.2M in servicing fees annually, offering predictable cash flow but low growth due to Pennsylvania market saturation.

The bank prioritizes processing efficiency (reducing origination time to 12 days) over expansion; cash from this segment is routinely redeployed to higher-growth commercial loans, funding ~18% of new commercial originations in 2025.

Agricultural and Legacy Small Business Loans

Mid Penn Bank’s agricultural and legacy small-business loans dominate central Pennsylvania with roughly 35–45% local market share and >70% repeat-borrower rate, making them a cash cow in a mature, low-growth sector.

These portfolios show low charge-off rates (~0.3%–0.6% in 2024) and stable yields, covering admin costs and funding branch ops; minimal reinvestment lets the bank harvest steady profits.

Consumer Checking and Savings Accounts

Consumer checking and savings across Mid Penn Bank’s 65-branch network are a primary source of low-cost liquidity, funding loans with stable deposits; retail churn fell to 4.2% in 2024, supporting predictable funding.

These accounts sit in a low-growth lifecycle but hold a high local market share and remain cash cows; digital adoption (45% of customers using mobile by YE 2024) cut servicing costs and raised net interest margin accretion.

- 65 branches; 4.2% churn (2024)

- High local share; low-growth stage

- 45% mobile users (YE 2024)

- Primary low-cost liquidity for lending

Home Equity Loans and Lines of Credit

Fixed-rate home equity loans and variable-rate HELOCs form a mature, high-margin segment of Mid Penn Bank’s consumer book, secured by junior liens on primary residences and generating steady interest income amid a stabilized PA housing market.

The bank holds strong share within its retail base—about 18% of regional home-equity originations in 2025—so these products need minimal promotion and deliver low servicing costs.

They act as reliable cash cows, funding liquidity for R&D in fintech; in 2025 net interest margin contribution from home-equity products was roughly 24% of consumer NII.

- High margin, low maintenance

- Secured by junior liens on primary residences

- ~18% regional originations share (2025)

- ~24% of consumer net interest income (2025)

- Funds fintech R&D and liquidity

Mid Penn: Deposit-Funded, Low-Cost NIM Driving Stable Dividends & Acquisition Fuel

Mid Penn’s deposit-led cash cows (62% deposit funding, 0.85% cost of funds in 2024) and mature loan segments (3.45% NIM overall; mortgages ~28% of book; HELOCs ~18% originations share in 2025) generate stable, low-growth cash used for dividends (48% payout 2024) and funding acquisitions (~$350M target 2023–25), with low charge-offs (0.3%–0.6% 2024) and 45% mobile adoption (YE 2024).

| Metric | Value |

|---|---|

| Deposit funding | 62% (2024) |

| Cost of funds | 0.85% (2024) |

| Net interest margin | 3.45% (2024) |

| Mortgage share | ~28% loan book (2025) |

| HELOC originations | ~18% regional (2025) |

| Payout ratio | 48% (2024) |

| Charge-offs | 0.3%–0.6% (2024) |

| Mobile users | 45% (YE 2024) |

Full Transparency, Always

Mid Penn Bank BCG Matrix

The file you're previewing is the exact Mid Penn Bank BCG Matrix report you'll receive after purchase—no watermarks, no placeholder text, just a fully formatted, analysis-ready document crafted for strategic decision-making and presentation.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Mid Penn Bank’s BCG Matrix preview highlights where core business lines likely sit—stable Cash Cows from retail deposits, high-potential Stars in digital lending, and possible Question Marks in niche commercial services—offering a snapshot of resource allocation priorities and growth levers. This high-level view teases quadrant placements and strategic implications; purchase the full BCG Matrix for a complete, data-driven breakdown, quadrant-by-quadrant recommendations, and editable Word and Excel deliverables to guide confident investment and strategic decisions.

Stars

Commercial Real Estate and Construction Lending

Mid Penn Bank leads CRE and construction lending, with these loans making up 65% of its total loan portfolio as of 2025 and driving strong interest income.

Late-2025 industry data shows a 40% jump in U.S. commercial mortgage originations, placing this segment in a high-growth quadrant of the BCG matrix.

Local decision-making and CRE expertise let Mid Penn capture share from larger banks, though ongoing capital injections are needed to fund metro expansions.

Greater Philadelphia Market Expansion

Through the 2025 acquisition of William Penn Bancorp, Mid Penn nearly doubled its Greater Philadelphia assets to about $1.8 billion, adding 12 branches and mass‑affluent clients—transforming this region into a BCG Matrix Star. The bank is targeting $5 billion in regional assets, pursuing aggressive deposit and loan growth in a metro area with 2024–25 population growth of ~0.8% annually and strong suburban housing demand. Significant marketing, branch rebranding, employee integration, and IT consolidation spend is underway to capture share in one of the nation’s most competitive banking corridors.

SBA and Specialty Commercial Lending

SBA and specialty commercial lending—notably healthcare and professional services—are Mid Penn Bank’s fastest-growing segments; SBA originations grew 22% in 2024 to $420 million, making Mid Penn the top community-bank SBA lender in Pennsylvania by volume.

For 2025 Mid Penn prioritizes these higher-yielding assets to offset net interest margin compression (NIM fell to 2.45% in 2024); niche focus aids yield diversification despite higher underwriting and marketing cash needs.

Digital Banking and Treasury Services

Digital Banking and Treasury Services is a Star: platform adoption rose 22% Y/Y in 2025, driving new commercial client wins and higher fee income as average treasury revenue per commercial client grew 14% to $8,600 annually.

Real-time payment rails and automated receivables keep Mid Penn competitive; as a regional first-mover, it gained ~2.1 percentage points market share vs. traditional banks in 2024–25.

Ongoing capital required: estimated $6–8m annual spend on cybersecurity and software updates, but anticipated cost-to-serve falls 18% over three years, supporting long-term margins.

- 22% platform adoption increase (2025)

- $8,600 avg treasury revenue per client

- +2.1 ppt market share vs peers (2024–25)

- $6–8m annual tech/cyber spend

- 18% projected cost-to-serve reduction in 3 years

New Jersey Market Penetration

Following the 2024 Brunswick Bancorp acquisition and 2025 integrations, Mid Penn Bank targets Central and Southern New Jersey as a high-growth Stars segment in the BCG matrix, aiming for >15% deposit CAGR and 8–10% loan growth versus 3–4% in legacy markets.

These corridors host a denser base of tech SMEs and affluent households—Mercer, Middlesex, and Burlington counties show median household incomes 20–35% above Mid Penn’s Pennsylvania footprint—so the bank is building de novo centers and local BD teams.

Initial operations are cash-heavy: estimated startup and branding spend of $45–60M through 2026, pressuring near-term margins but targeting ~200–300 bps higher NIMs long term and market-leading share within 5–7 years.

- 2024 acquisition closed; 2025 integrations complete

- Target: >15% deposit CAGR; 8–10% loan growth

- Estimated $45–60M upfront spend to 2026

- Targets +200–300 bps NIM lift; 5–7 year dominance

Mid Penn: CRE-led growth, digital treasury gains, NJ rollout targets >15% deposit CAGR

Mid Penn’s Stars: CRE/construction, digital treasury, and NJ/Philly metros drive high growth and share; CRE = 65% loans (2025), treasury revenue $8,600/client, platform adoption +22% (2025), SBA originations $420M (2024). Capital push: $6–8M/yr tech spend; $45–60M NJ rollout to 2026 targeting >15% deposit CAGR.

| Metric | Value |

|---|---|

| CRE share | 65% |

| Platform adoption | +22% (2025) |

| SBA originations | $420M (2024) |

| Tech spend | $6–8M/yr |

| NJ rollout spend | $45–60M |

What is included in the product

Comprehensive BCG Matrix review of Mid Penn Bank’s units with strategic guidance on Stars, Cash Cows, Question Marks, and Dogs.

One-page BCG matrix placing Mid Penn Bank units into quadrants for quick strategy decisions, export-ready for PowerPoint.

Cash Cows

Core Central Pennsylvania Deposit Base

Mid Penn Bank holds top-three deposit market share in Dauphin, Lancaster, Cumberland, and Schuylkill counties, supplying a stable, low-cost funding base that supported 62% of deposit funding in 2024 and lowered cost of funds to 0.85% that year.

These mature markets need minimal marketing spend, deliver consistent high-margin cash flow—net interest margin of 3.45% in 2024—and let the bank "milk" legacy deposits to finance growth.

The core deposit cash cow primarily funds dividends (2024 payout ratio 48%) and the 2023–2025 acquisition plan, which targets $350m in deal size to expand into adjacent regions.

Traditional Residential Mortgages

As of 2025, Mid Penn Bank’s traditional residential mortgages—holding ~28% share of its loan book—generate steady net interest margin income (~3.1% NIM) and $4.2M in servicing fees annually, offering predictable cash flow but low growth due to Pennsylvania market saturation.

The bank prioritizes processing efficiency (reducing origination time to 12 days) over expansion; cash from this segment is routinely redeployed to higher-growth commercial loans, funding ~18% of new commercial originations in 2025.

Agricultural and Legacy Small Business Loans

Mid Penn Bank’s agricultural and legacy small-business loans dominate central Pennsylvania with roughly 35–45% local market share and >70% repeat-borrower rate, making them a cash cow in a mature, low-growth sector.

These portfolios show low charge-off rates (~0.3%–0.6% in 2024) and stable yields, covering admin costs and funding branch ops; minimal reinvestment lets the bank harvest steady profits.

Consumer Checking and Savings Accounts

Consumer checking and savings across Mid Penn Bank’s 65-branch network are a primary source of low-cost liquidity, funding loans with stable deposits; retail churn fell to 4.2% in 2024, supporting predictable funding.

These accounts sit in a low-growth lifecycle but hold a high local market share and remain cash cows; digital adoption (45% of customers using mobile by YE 2024) cut servicing costs and raised net interest margin accretion.

- 65 branches; 4.2% churn (2024)

- High local share; low-growth stage

- 45% mobile users (YE 2024)

- Primary low-cost liquidity for lending

Home Equity Loans and Lines of Credit

Fixed-rate home equity loans and variable-rate HELOCs form a mature, high-margin segment of Mid Penn Bank’s consumer book, secured by junior liens on primary residences and generating steady interest income amid a stabilized PA housing market.

The bank holds strong share within its retail base—about 18% of regional home-equity originations in 2025—so these products need minimal promotion and deliver low servicing costs.

They act as reliable cash cows, funding liquidity for R&D in fintech; in 2025 net interest margin contribution from home-equity products was roughly 24% of consumer NII.

- High margin, low maintenance

- Secured by junior liens on primary residences

- ~18% regional originations share (2025)

- ~24% of consumer net interest income (2025)

- Funds fintech R&D and liquidity

Mid Penn: Deposit-Funded, Low-Cost NIM Driving Stable Dividends & Acquisition Fuel

Mid Penn’s deposit-led cash cows (62% deposit funding, 0.85% cost of funds in 2024) and mature loan segments (3.45% NIM overall; mortgages ~28% of book; HELOCs ~18% originations share in 2025) generate stable, low-growth cash used for dividends (48% payout 2024) and funding acquisitions (~$350M target 2023–25), with low charge-offs (0.3%–0.6% 2024) and 45% mobile adoption (YE 2024).

| Metric | Value |

|---|---|

| Deposit funding | 62% (2024) |

| Cost of funds | 0.85% (2024) |

| Net interest margin | 3.45% (2024) |

| Mortgage share | ~28% loan book (2025) |

| HELOC originations | ~18% regional (2025) |

| Payout ratio | 48% (2024) |

| Charge-offs | 0.3%–0.6% (2024) |

| Mobile users | 45% (YE 2024) |

Full Transparency, Always

Mid Penn Bank BCG Matrix

The file you're previewing is the exact Mid Penn Bank BCG Matrix report you'll receive after purchase—no watermarks, no placeholder text, just a fully formatted, analysis-ready document crafted for strategic decision-making and presentation.