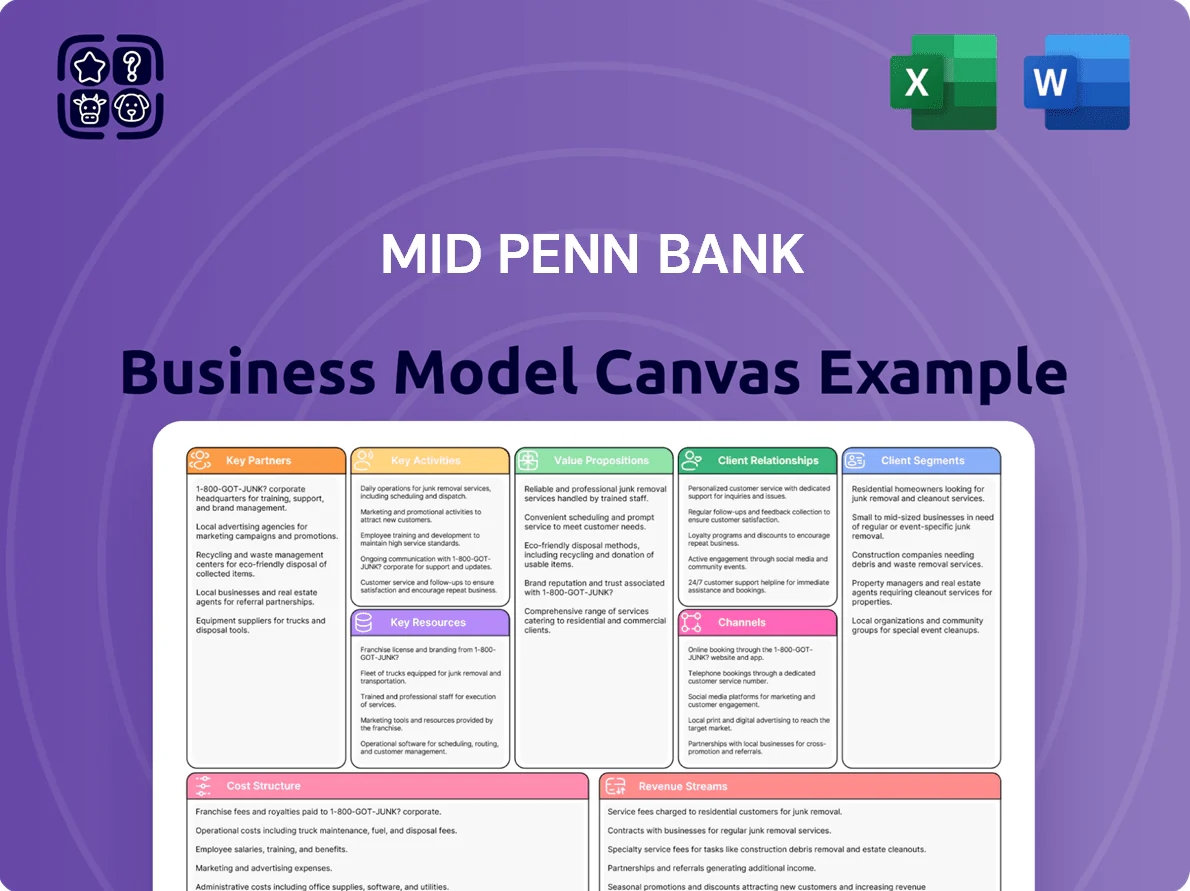

Mid Penn Bank Business Model Canvas

Mid Penn Bank Business Model Canvas: Downloadable, Section-by-Section Strategic Playbook

Unlock Mid Penn Bank’s strategic playbook with our concise Business Model Canvas — a section-by-section breakdown of customer segments, value propositions, revenue streams, and key partnerships that shows exactly how the bank creates and captures value; download the full Word & Excel files for actionable insights, benchmarking, and investor-ready analysis to accelerate your strategy.

Partnerships

Strategic Fintech Integrations

Mid Penn Bank partners with fintechs to add real-time payments and advanced analytics for retail and commercial clients, cutting implementation costs versus building in-house and speeding time-to-market; in 2024 fintech integrations helped banks reduce digital launch costs by ~40% and shorten rollout time by ~6 months (Source: Aite-Novarica 2024).

Correspondent Banking Networks

Mid Penn Bank partners with large correspondent banks to route international payments and high-value wires beyond regional rails, tapping networks that processed over $120 trillion in global payments in 2024; these partners supply access to global liquidity and FX services—reducing FX spreads for corporate clients by up to 15 bps in 2024—and let local businesses transact globally while keeping Mid Penn as their community bank.

Local Community and Non-Profit Organizations

Partnerships with regional chambers and local non-profits keep Mid Penn Bank’s community brand visible and feed mortgage, small-business, and CRA (Community Reinvestment Act) pipelines; in 2024 Mid Penn reported $1.2B in loans to local businesses and households across Pennsylvania, with 18% YoY growth in community lending.

Regulatory and Compliance Agencies

The bank coordinates with the Federal Deposit Insurance Corporation (FDIC) and the Pennsylvania Department of Banking and Securities for regular audits, reporting, and supervisory consultations to meet capital, liquidity, and AML/CFT standards.

In 2025 this alignment supports safety and public trust as regulators focus on resilience—FDIC stress-test frameworks and PA supervisory exams target capital ratios, liquidity coverage, and cyber-resilience metrics.

- Regular FDIC and PA exams

- Quarterly regulatory reporting

- Capital and liquidity ratio monitoring

- AML/CFT and cyber-resilience focus

Third-Party Investment and Insurance Providers

Mid Penn Bank partners with external brokerage and insurance firms to offer diversified investment vehicles and specialized insurance for high-net-worth and corporate clients, generating fee-based income while using partners' product shelves and expertise; in 2025 the regional banking channel reported 18–22% of noninterest income from wealth/insurance alliances.

- Fee income boost: 18–22% of noninterest income (2025 regional avg)

- Client focus: HNW and corporate accounts

- Capability: access to global asset managers and specialty insurers

Mid Penn Bank scales digital payments, FX & community lending — cuts costs, boosts fee income

Mid Penn Bank leverages fintechs, correspondent banks, community partners, regulators, and wealth/insurance firms to expand digital payments, global FX, community lending, compliance, and fee income; 2024–25 metrics: fintech cut launch costs ~40%, global payments network $120T (2024), community loans $1.2B (2024, +18% YoY), wealth/insurance = 18–22% noninterest income (2025).

| Partner | Role | Key 2024–25 Metric |

|---|---|---|

| Fintechs | Payments/analytics | -40% cost, -6 months rollout (2024) |

| Correspondents | Intl payments/FX | $120T network (2024), -15bps FX spread |

| Community Orgs | Origination/brand | $1.2B loans, +18% YoY (2024) |

| Regulators | Supervision | FDIC/PA exams, capital/liquidity focus (2025) |

| Wealth/Insurance | Fee products | 18–22% noninterest income (2025) |

What is included in the product

A concise, ready-made Business Model Canvas for Mid Penn Bank detailing customer segments, value propositions, channels, revenue streams, key activities, resources, partners, cost structure, and risk insights, reflecting real-world operations and strategic plans to support presentations, funding discussions, and decision-making.

High-level view of Mid Penn Bank’s business model with editable cells, condensing community banking strategy into a digestible one-page snapshot to save hours of formatting while enabling quick comparison, collaboration, and boardroom-ready presentations.

Activities

Commercial and Personal Loan Underwriting

Mid Penn Bank rigorously assesses creditworthiness for small businesses, real estate developers, and individuals, combining ratio-based financial analysis with machine-learning credit models; as of 2025 the bank targets a net charge-off rate under 0.40% and maintains an NIM (net interest margin) near 3.6% to balance yield and risk. Efficient loan processing—average commercial approval turnaround ~10–14 days—supports asset quality and drove 2024 loan growth of ~7.2%, sustaining interest income and local capital availability.

Deposit and Liquidity Management

Mid Penn Bank attracts and retains checking, savings and CD deposits to fund loans, with deposits comprising about 82% of liabilities as of 2025 Q3 and core deposit beta kept low to protect net interest margin (reported NIM 2.85% in 2024).

Daily fund-cost management and laddered CD maturities target market-sensitive rates, while liquidity buffers (liquids + Fed balances ≈ 12% of assets) ensure withdrawal coverage and capital utility.

Digital Banking Platform Maintenance

Mid Penn Bank prioritizes ongoing investment in online and mobile banking, allocating about 12% of IT budget to digital channels in 2025 to meet expectations of tech-savvy customers; teams update cybersecurity to NIST 800-53-aligned controls and aim for 99.95% uptime. Technical staff streamline UI for personal and business users, target sub-2-second page loads, and maintain 24/7 access to core services and APIs.

Community Engagement and Business Development

Bank executives and relationship managers attend local events and network weekly to source deals, driving the relationship-based model that captures high-value commercial accounts across Pennsylvania; Mid Penn reported 2024 commercial loan originations of $342M, underscoring the approach’s effectiveness.

These boots-on-the-ground activities reduce customer acquisition cost and increase average commercial deposit balances—Mid Penn’s commercial deposits rose 6.1% YoY in 2024—helping win market share in competitive counties like Dauphin and Lancaster.

- Weekly event outreach by senior staff

- $342M commercial loans originated in 2024

- 6.1% YoY commercial deposit growth in 2024

- Focus on Dauphin, Lancaster counties

Regulatory Compliance and Risk Mitigation

Mid Penn Bank allocates major resources to transaction monitoring for fraud and AML (anti-money laundering), processing 100% of high-risk alerts within 24 hours and reducing fraud losses by 22% in 2024.

Continuous internal audits and staff training—26 hours average per employee in 2024—ensure federal/state compliance, limiting legal exposure and protecting the bank’s market reputation.

- 24h alert resolution for high-risk cases

- 22% reduction in fraud losses (2024)

- 26 training hours per employee (2024)

- Ongoing internal audits across all departments

Mid Penn: Deposit‑funded growth, disciplined lending, digital resilience, -22% fraud

Mid Penn focuses on relationship lending, disciplined credit underwriting (target NCO <0.40%), deposit-funded growth (deposits ≈82% liabilities), digital channels (12% IT to digital, 99.95% uptime goal), strong AML/fraud controls (24h high-risk alerts, fraud losses -22% in 2024), and local origination (2024 commercial originations $342M; commercial deposits +6.1% YoY).

| Metric | 2024/2025 |

|---|---|

| Commercial originations | $342M (2024) |

| Commercial deposit growth | +6.1% YoY (2024) |

| Deposits of liabilities | ≈82% (2025 Q3) |

| NIM | ~3.6% target / 2.85% (2024) |

| Fraud loss change | -22% (2024) |

| IT digital spend | 12% (2025) |

What You See Is What You Get

Business Model Canvas

The Mid Penn Bank Business Model Canvas shown here is the actual deliverable—not a mockup—so when you purchase you’ll receive this same professionally formatted document ready for use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Mid Penn Bank Business Model Canvas: Downloadable, Section-by-Section Strategic Playbook

Unlock Mid Penn Bank’s strategic playbook with our concise Business Model Canvas — a section-by-section breakdown of customer segments, value propositions, revenue streams, and key partnerships that shows exactly how the bank creates and captures value; download the full Word & Excel files for actionable insights, benchmarking, and investor-ready analysis to accelerate your strategy.

Partnerships

Strategic Fintech Integrations

Mid Penn Bank partners with fintechs to add real-time payments and advanced analytics for retail and commercial clients, cutting implementation costs versus building in-house and speeding time-to-market; in 2024 fintech integrations helped banks reduce digital launch costs by ~40% and shorten rollout time by ~6 months (Source: Aite-Novarica 2024).

Correspondent Banking Networks

Mid Penn Bank partners with large correspondent banks to route international payments and high-value wires beyond regional rails, tapping networks that processed over $120 trillion in global payments in 2024; these partners supply access to global liquidity and FX services—reducing FX spreads for corporate clients by up to 15 bps in 2024—and let local businesses transact globally while keeping Mid Penn as their community bank.

Local Community and Non-Profit Organizations

Partnerships with regional chambers and local non-profits keep Mid Penn Bank’s community brand visible and feed mortgage, small-business, and CRA (Community Reinvestment Act) pipelines; in 2024 Mid Penn reported $1.2B in loans to local businesses and households across Pennsylvania, with 18% YoY growth in community lending.

Regulatory and Compliance Agencies

The bank coordinates with the Federal Deposit Insurance Corporation (FDIC) and the Pennsylvania Department of Banking and Securities for regular audits, reporting, and supervisory consultations to meet capital, liquidity, and AML/CFT standards.

In 2025 this alignment supports safety and public trust as regulators focus on resilience—FDIC stress-test frameworks and PA supervisory exams target capital ratios, liquidity coverage, and cyber-resilience metrics.

- Regular FDIC and PA exams

- Quarterly regulatory reporting

- Capital and liquidity ratio monitoring

- AML/CFT and cyber-resilience focus

Third-Party Investment and Insurance Providers

Mid Penn Bank partners with external brokerage and insurance firms to offer diversified investment vehicles and specialized insurance for high-net-worth and corporate clients, generating fee-based income while using partners' product shelves and expertise; in 2025 the regional banking channel reported 18–22% of noninterest income from wealth/insurance alliances.

- Fee income boost: 18–22% of noninterest income (2025 regional avg)

- Client focus: HNW and corporate accounts

- Capability: access to global asset managers and specialty insurers

Mid Penn Bank scales digital payments, FX & community lending — cuts costs, boosts fee income

Mid Penn Bank leverages fintechs, correspondent banks, community partners, regulators, and wealth/insurance firms to expand digital payments, global FX, community lending, compliance, and fee income; 2024–25 metrics: fintech cut launch costs ~40%, global payments network $120T (2024), community loans $1.2B (2024, +18% YoY), wealth/insurance = 18–22% noninterest income (2025).

| Partner | Role | Key 2024–25 Metric |

|---|---|---|

| Fintechs | Payments/analytics | -40% cost, -6 months rollout (2024) |

| Correspondents | Intl payments/FX | $120T network (2024), -15bps FX spread |

| Community Orgs | Origination/brand | $1.2B loans, +18% YoY (2024) |

| Regulators | Supervision | FDIC/PA exams, capital/liquidity focus (2025) |

| Wealth/Insurance | Fee products | 18–22% noninterest income (2025) |

What is included in the product

A concise, ready-made Business Model Canvas for Mid Penn Bank detailing customer segments, value propositions, channels, revenue streams, key activities, resources, partners, cost structure, and risk insights, reflecting real-world operations and strategic plans to support presentations, funding discussions, and decision-making.

High-level view of Mid Penn Bank’s business model with editable cells, condensing community banking strategy into a digestible one-page snapshot to save hours of formatting while enabling quick comparison, collaboration, and boardroom-ready presentations.

Activities

Commercial and Personal Loan Underwriting

Mid Penn Bank rigorously assesses creditworthiness for small businesses, real estate developers, and individuals, combining ratio-based financial analysis with machine-learning credit models; as of 2025 the bank targets a net charge-off rate under 0.40% and maintains an NIM (net interest margin) near 3.6% to balance yield and risk. Efficient loan processing—average commercial approval turnaround ~10–14 days—supports asset quality and drove 2024 loan growth of ~7.2%, sustaining interest income and local capital availability.

Deposit and Liquidity Management

Mid Penn Bank attracts and retains checking, savings and CD deposits to fund loans, with deposits comprising about 82% of liabilities as of 2025 Q3 and core deposit beta kept low to protect net interest margin (reported NIM 2.85% in 2024).

Daily fund-cost management and laddered CD maturities target market-sensitive rates, while liquidity buffers (liquids + Fed balances ≈ 12% of assets) ensure withdrawal coverage and capital utility.

Digital Banking Platform Maintenance

Mid Penn Bank prioritizes ongoing investment in online and mobile banking, allocating about 12% of IT budget to digital channels in 2025 to meet expectations of tech-savvy customers; teams update cybersecurity to NIST 800-53-aligned controls and aim for 99.95% uptime. Technical staff streamline UI for personal and business users, target sub-2-second page loads, and maintain 24/7 access to core services and APIs.

Community Engagement and Business Development

Bank executives and relationship managers attend local events and network weekly to source deals, driving the relationship-based model that captures high-value commercial accounts across Pennsylvania; Mid Penn reported 2024 commercial loan originations of $342M, underscoring the approach’s effectiveness.

These boots-on-the-ground activities reduce customer acquisition cost and increase average commercial deposit balances—Mid Penn’s commercial deposits rose 6.1% YoY in 2024—helping win market share in competitive counties like Dauphin and Lancaster.

- Weekly event outreach by senior staff

- $342M commercial loans originated in 2024

- 6.1% YoY commercial deposit growth in 2024

- Focus on Dauphin, Lancaster counties

Regulatory Compliance and Risk Mitigation

Mid Penn Bank allocates major resources to transaction monitoring for fraud and AML (anti-money laundering), processing 100% of high-risk alerts within 24 hours and reducing fraud losses by 22% in 2024.

Continuous internal audits and staff training—26 hours average per employee in 2024—ensure federal/state compliance, limiting legal exposure and protecting the bank’s market reputation.

- 24h alert resolution for high-risk cases

- 22% reduction in fraud losses (2024)

- 26 training hours per employee (2024)

- Ongoing internal audits across all departments

Mid Penn: Deposit‑funded growth, disciplined lending, digital resilience, -22% fraud

Mid Penn focuses on relationship lending, disciplined credit underwriting (target NCO <0.40%), deposit-funded growth (deposits ≈82% liabilities), digital channels (12% IT to digital, 99.95% uptime goal), strong AML/fraud controls (24h high-risk alerts, fraud losses -22% in 2024), and local origination (2024 commercial originations $342M; commercial deposits +6.1% YoY).

| Metric | 2024/2025 |

|---|---|

| Commercial originations | $342M (2024) |

| Commercial deposit growth | +6.1% YoY (2024) |

| Deposits of liabilities | ≈82% (2025 Q3) |

| NIM | ~3.6% target / 2.85% (2024) |

| Fraud loss change | -22% (2024) |

| IT digital spend | 12% (2025) |

What You See Is What You Get

Business Model Canvas

The Mid Penn Bank Business Model Canvas shown here is the actual deliverable—not a mockup—so when you purchase you’ll receive this same professionally formatted document ready for use.