Mid Penn Bank Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

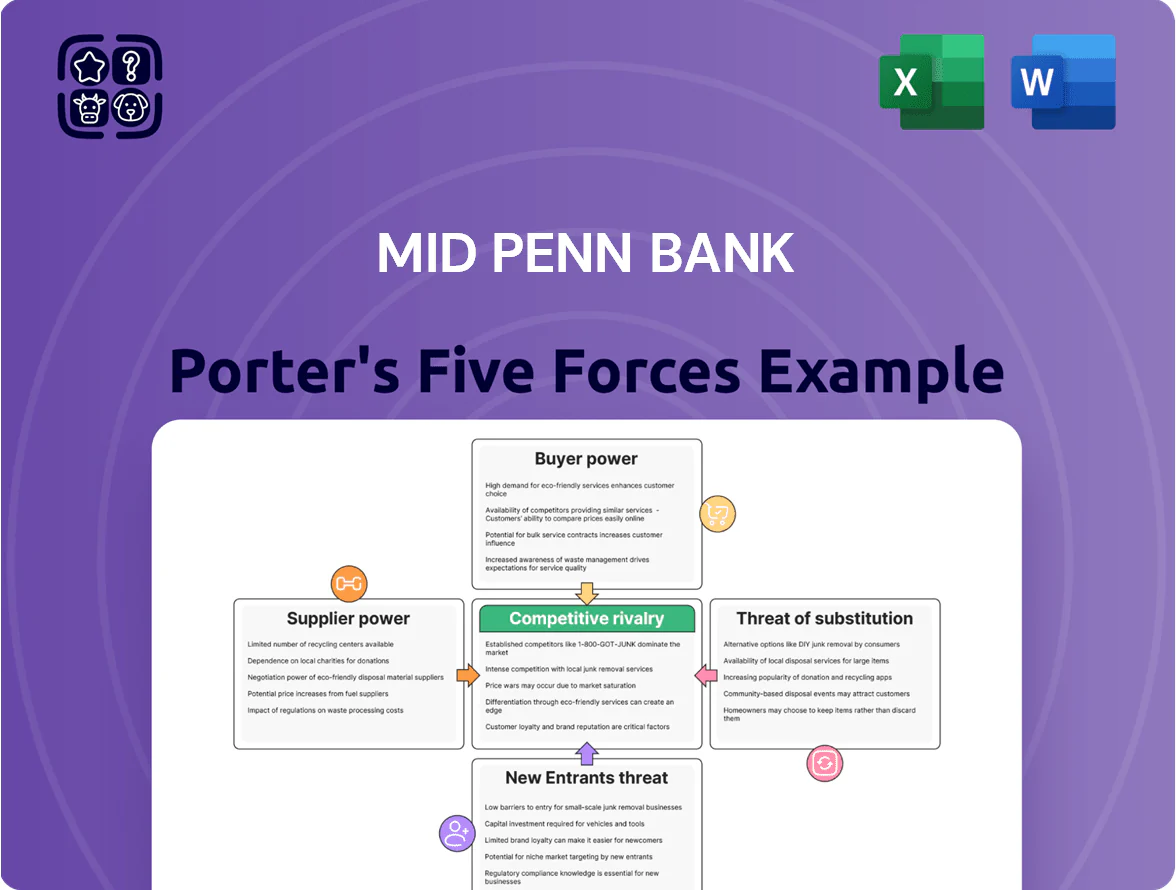

Mid Penn Bank faces moderate competitive pressure: strong local customer loyalty offsets rising fintech threats, while regulatory costs and limited supplier leverage keep margins squeezed; niche community banking strengths coexist with vulnerability to rate shifts and consolidation. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Mid Penn Bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Core Technology Providers

Mid Penn Bank depends on a few core vendors for banking systems, cybersecurity, and payments, giving suppliers high leverage because switching costs often exceed millions and risk service outages; Gartner estimated 70% of regional banks used top-three core providers in 2024.

By end-2025, demand for AI and cloud pushed concentration: top cloud/AI firms controlled >60% market share for banking-specific services, raising vendor bargaining power and pricing pressure on Mid Penn.

Competition for Skilled Financial Talent

The limited pool of experienced commercial lenders, compliance officers and cybersec experts in Pennsylvania gives top talent strong bargaining power; a 2024 Labor Market Analytics report showed vacancy-to-hire ratios for financial specialists at 1.8x in the region. Mid Penn must now compete with fintechs and banks, driving median compensation up ~12% vs 2021 and forcing richer benefits to keep relationship bankers essential to revenue retention.

Cost of Wholesale Funding and Liquidity

When Mid Penn Bank exhausts internal deposits, it taps wholesale funding and the Federal Home Loan Bank (FHLB); these suppliers price loans off macro conditions and Fed policy, leaving limited negotiation room.

By late 2025, benchmark SOFR rose to ~5.1% and FHLB advance spreads widened, pushing wholesale funding costs up ~120–180 bps versus 2023, making external funding notably pricier and more volatile for the bank.

Regulatory Compliance and Legal Oversight

Government and state regulators act as non-market suppliers by controlling licenses and the operating rules Mid Penn Bank must follow, making compliance non-negotiable and costly.

FDIC and Pennsylvania Department of Banking mandates raised capital ratios and reporting: since 2023 banks saw CET1-like targets increase ~150–250 bps industrywide, and 2025 rules demand quarterly enhanced liquidity reporting, boosting compliance budgets by mid-sized banks ~10–15%.

These rules shift strategic choices—slowing dividend/expansion plans and prioritizing capital preservation—so regulators exert high supplier power over Mid Penn’s strategy.

- Regulators supply licenses and rules, non-negotiable

- 2025 tighter capital + reporting raised compliance costs ~10–15%

- Capital targets up ~150–250 basis points since 2023

- Regulatory power constrains dividends, M&A, growth

Influence of Credit Rating Agencies

Credit rating agencies that rate Mid Penn Bank’s debt directly affect its cost of capital and market reputation; a one-notch downgrade typically raises borrowing spreads by ~30–60 bps, per historical regional bank data through 2024.

A downgrade can sharply raise funding costs and deter institutional investors, as seen when similar regional banks saw 15–25% drop in bond demand after downgrades in 2023–24.

Management must keep capital ratios and asset quality strong to satisfy agencies; maintaining CET1 around 10–12% and NPLs below 1% is crucial.

- Agencies set spreads: one-notch ≈ +30–60 bps

- Investor pullback: bond demand down 15–25% post-downgrade

- Targets: CET1 10–12%, NPLs <1%

Suppliers Squeeze Regionals: concentrated vendors, talent gaps, rising costs & caps

Suppliers hold strong power: core banking, cloud/AI, and cybersecurity vendors are concentrated (top-three core vendors used by ~70% of regionals in 2024), talent shortages raised financial-specialist vacancy-to-hire to 1.8x in 2024, wholesale funding costs rose ~120–180 bps by late‑2025 vs 2023, and regulators raised capital targets ~150–250 bps since 2023.

| Supplier | Key metric | 2024–2025 |

|---|---|---|

| Core vendors | Market share (top‑3) | ~70% |

| Cloud/AI | Banking services share | >60% (2025) |

| Talent | Vacancy:hire | 1.8x (2024) |

| Wholesale funding | Cost change | +120–180 bps (2023–late‑2025) |

| Regulators | Capital targets shift | +150–250 bps since 2023 |

What is included in the product

Concise Porter’s Five Forces assessment of Mid Penn Bank, revealing competitive intensity, customer and supplier influence, entry barriers, substitute threats, and strategic levers to protect margin and market share.

A concise Porter's Five Forces one-sheet for Mid Penn Bank—quickly spot competitive pressures and tailor strategy with editable intensity settings for evolving market risks.

Customers Bargaining Power

Low Switching Costs for Retail Depositors

Retail depositors can shift funds quickly thanks to digital banking and apps; 2024 FDIC data showed 45% of consumers used mobile transfers monthly, lowering switching friction for Mid Penn Bank.

Online rate transparency means consumers compare yields instantly; as of Q4 2025 national average 12-month CD rates ranged 0.5–5.0%, so customers chase top yields.

This ease forces Mid Penn Bank to price deposits competitively to avoid outflows—community banks saw net deposit declines of 2.1% in 2024 when rates lagged peers.

Price Sensitivity in Commercial Lending

Small and medium-sized businesses, Mid Penn Bank’s core clients, show high price sensitivity to interest rate margins and loan terms; in 2025 regional SMBs paid average commercial loan spreads near 250 basis points, pushing intense competition. These sophisticated borrowers routinely solicit bids from regional and national banks, with 62% requesting multiple proposals in the past 12 months. To win deals the bank often trims margin or bundles fee-based treasury and advisory services, raising relationship cost by an estimated 15–40% per account.

Demand for Integrated Digital Experiences

Modern customers expect seamless digital interfaces like national banks and fintechs; a 2024 Accenture survey found 68% of US consumers would switch banks for better digital tools, and 55% of SMEs cite digital capability as a top factor (2025 industry reports). If Mid Penn Bank lags, clients can migrate to competitors offering richer UX and automation, making integrated digital experience a baseline for retention in 2025.

Leverage of High Net Worth Clients

- Top 5% depositors ≈ 10% total deposits (2024)

- Servicing premium 30–50 bps

- High churn risks if personalization lag

Information Symmetry and Market Transparency

The democratization of financial data means Mid Penn Bank customers are better informed about rates, fees, and alternatives; 2024 data shows 74% of US bank consumers use online rate comparison tools, shrinking information asymmetry and pressuring margins.

As a result Mid Penn cannot command large premiums on basic deposit and loan products; customers negotiate with market rate benchmarks (e.g., 12-month CD national avg 4.23% as of Dec 2024), improving their bargaining power.

Customers enter loan/service talks armed with data—credit-score portals, fee aggregators, and national APR databases—so conversion depends more on service and niche pricing.

- 74% use online comparison tools (2024)

- 12-month CD national avg 4.23% (Dec 2024)

- Lower price opacity → tighter margins

- Negotiations driven by published benchmarks

Digital switching forces Mid Penn to match market yields—deposits, margins & liquidity at risk

Customers hold strong bargaining power: digital switching and rate transparency push Mid Penn to match market yields (12-month CD avg 4.23% Dec 2024) or lose deposits; top 5% depositors equal ~10% of balances, so small outflows hit liquidity; SMBs demand ~250 bps loan spreads and solicit multiple bids (62%); digital experience and fee pressure force tighter margins and higher servicing costs (30–50 bps for private banking).

| Metric | Value |

|---|---|

| 12‑mo CD avg (Dec 2024) | 4.23% |

| Top 5% depositors share (2024) | ≈10% |

| SMB avg loan spread (2025) | ~250 bps |

| Private banking cost premium | 30–50 bps |

| Consumers using comparison tools (2024) | 74% |

Preview Before You Purchase

Mid Penn Bank Porter's Five Forces Analysis

This preview shows the exact Mid Penn Bank Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted and ready for download the moment you buy, containing the same professional assessment, data-driven insights, and strategic implications you see now. You're looking at the final deliverable—instant access upon payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Mid Penn Bank faces moderate competitive pressure: strong local customer loyalty offsets rising fintech threats, while regulatory costs and limited supplier leverage keep margins squeezed; niche community banking strengths coexist with vulnerability to rate shifts and consolidation. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Mid Penn Bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Core Technology Providers

Mid Penn Bank depends on a few core vendors for banking systems, cybersecurity, and payments, giving suppliers high leverage because switching costs often exceed millions and risk service outages; Gartner estimated 70% of regional banks used top-three core providers in 2024.

By end-2025, demand for AI and cloud pushed concentration: top cloud/AI firms controlled >60% market share for banking-specific services, raising vendor bargaining power and pricing pressure on Mid Penn.

Competition for Skilled Financial Talent

The limited pool of experienced commercial lenders, compliance officers and cybersec experts in Pennsylvania gives top talent strong bargaining power; a 2024 Labor Market Analytics report showed vacancy-to-hire ratios for financial specialists at 1.8x in the region. Mid Penn must now compete with fintechs and banks, driving median compensation up ~12% vs 2021 and forcing richer benefits to keep relationship bankers essential to revenue retention.

Cost of Wholesale Funding and Liquidity

When Mid Penn Bank exhausts internal deposits, it taps wholesale funding and the Federal Home Loan Bank (FHLB); these suppliers price loans off macro conditions and Fed policy, leaving limited negotiation room.

By late 2025, benchmark SOFR rose to ~5.1% and FHLB advance spreads widened, pushing wholesale funding costs up ~120–180 bps versus 2023, making external funding notably pricier and more volatile for the bank.

Regulatory Compliance and Legal Oversight

Government and state regulators act as non-market suppliers by controlling licenses and the operating rules Mid Penn Bank must follow, making compliance non-negotiable and costly.

FDIC and Pennsylvania Department of Banking mandates raised capital ratios and reporting: since 2023 banks saw CET1-like targets increase ~150–250 bps industrywide, and 2025 rules demand quarterly enhanced liquidity reporting, boosting compliance budgets by mid-sized banks ~10–15%.

These rules shift strategic choices—slowing dividend/expansion plans and prioritizing capital preservation—so regulators exert high supplier power over Mid Penn’s strategy.

- Regulators supply licenses and rules, non-negotiable

- 2025 tighter capital + reporting raised compliance costs ~10–15%

- Capital targets up ~150–250 basis points since 2023

- Regulatory power constrains dividends, M&A, growth

Influence of Credit Rating Agencies

Credit rating agencies that rate Mid Penn Bank’s debt directly affect its cost of capital and market reputation; a one-notch downgrade typically raises borrowing spreads by ~30–60 bps, per historical regional bank data through 2024.

A downgrade can sharply raise funding costs and deter institutional investors, as seen when similar regional banks saw 15–25% drop in bond demand after downgrades in 2023–24.

Management must keep capital ratios and asset quality strong to satisfy agencies; maintaining CET1 around 10–12% and NPLs below 1% is crucial.

- Agencies set spreads: one-notch ≈ +30–60 bps

- Investor pullback: bond demand down 15–25% post-downgrade

- Targets: CET1 10–12%, NPLs <1%

Suppliers Squeeze Regionals: concentrated vendors, talent gaps, rising costs & caps

Suppliers hold strong power: core banking, cloud/AI, and cybersecurity vendors are concentrated (top-three core vendors used by ~70% of regionals in 2024), talent shortages raised financial-specialist vacancy-to-hire to 1.8x in 2024, wholesale funding costs rose ~120–180 bps by late‑2025 vs 2023, and regulators raised capital targets ~150–250 bps since 2023.

| Supplier | Key metric | 2024–2025 |

|---|---|---|

| Core vendors | Market share (top‑3) | ~70% |

| Cloud/AI | Banking services share | >60% (2025) |

| Talent | Vacancy:hire | 1.8x (2024) |

| Wholesale funding | Cost change | +120–180 bps (2023–late‑2025) |

| Regulators | Capital targets shift | +150–250 bps since 2023 |

What is included in the product

Concise Porter’s Five Forces assessment of Mid Penn Bank, revealing competitive intensity, customer and supplier influence, entry barriers, substitute threats, and strategic levers to protect margin and market share.

A concise Porter's Five Forces one-sheet for Mid Penn Bank—quickly spot competitive pressures and tailor strategy with editable intensity settings for evolving market risks.

Customers Bargaining Power

Low Switching Costs for Retail Depositors

Retail depositors can shift funds quickly thanks to digital banking and apps; 2024 FDIC data showed 45% of consumers used mobile transfers monthly, lowering switching friction for Mid Penn Bank.

Online rate transparency means consumers compare yields instantly; as of Q4 2025 national average 12-month CD rates ranged 0.5–5.0%, so customers chase top yields.

This ease forces Mid Penn Bank to price deposits competitively to avoid outflows—community banks saw net deposit declines of 2.1% in 2024 when rates lagged peers.

Price Sensitivity in Commercial Lending

Small and medium-sized businesses, Mid Penn Bank’s core clients, show high price sensitivity to interest rate margins and loan terms; in 2025 regional SMBs paid average commercial loan spreads near 250 basis points, pushing intense competition. These sophisticated borrowers routinely solicit bids from regional and national banks, with 62% requesting multiple proposals in the past 12 months. To win deals the bank often trims margin or bundles fee-based treasury and advisory services, raising relationship cost by an estimated 15–40% per account.

Demand for Integrated Digital Experiences

Modern customers expect seamless digital interfaces like national banks and fintechs; a 2024 Accenture survey found 68% of US consumers would switch banks for better digital tools, and 55% of SMEs cite digital capability as a top factor (2025 industry reports). If Mid Penn Bank lags, clients can migrate to competitors offering richer UX and automation, making integrated digital experience a baseline for retention in 2025.

Leverage of High Net Worth Clients

- Top 5% depositors ≈ 10% total deposits (2024)

- Servicing premium 30–50 bps

- High churn risks if personalization lag

Information Symmetry and Market Transparency

The democratization of financial data means Mid Penn Bank customers are better informed about rates, fees, and alternatives; 2024 data shows 74% of US bank consumers use online rate comparison tools, shrinking information asymmetry and pressuring margins.

As a result Mid Penn cannot command large premiums on basic deposit and loan products; customers negotiate with market rate benchmarks (e.g., 12-month CD national avg 4.23% as of Dec 2024), improving their bargaining power.

Customers enter loan/service talks armed with data—credit-score portals, fee aggregators, and national APR databases—so conversion depends more on service and niche pricing.

- 74% use online comparison tools (2024)

- 12-month CD national avg 4.23% (Dec 2024)

- Lower price opacity → tighter margins

- Negotiations driven by published benchmarks

Digital switching forces Mid Penn to match market yields—deposits, margins & liquidity at risk

Customers hold strong bargaining power: digital switching and rate transparency push Mid Penn to match market yields (12-month CD avg 4.23% Dec 2024) or lose deposits; top 5% depositors equal ~10% of balances, so small outflows hit liquidity; SMBs demand ~250 bps loan spreads and solicit multiple bids (62%); digital experience and fee pressure force tighter margins and higher servicing costs (30–50 bps for private banking).

| Metric | Value |

|---|---|

| 12‑mo CD avg (Dec 2024) | 4.23% |

| Top 5% depositors share (2024) | ≈10% |

| SMB avg loan spread (2025) | ~250 bps |

| Private banking cost premium | 30–50 bps |

| Consumers using comparison tools (2024) | 74% |

Preview Before You Purchase

Mid Penn Bank Porter's Five Forces Analysis

This preview shows the exact Mid Penn Bank Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted and ready for download the moment you buy, containing the same professional assessment, data-driven insights, and strategic implications you see now. You're looking at the final deliverable—instant access upon payment.