MidWestOne Bank Business Model Canvas

MidWestOne Bank: Business Model Canvas—Strategy, Customers & Revenue Drivers

Unlock the full strategic blueprint behind MidWestOne Bank with our Business Model Canvas—detailing customer segments, value propositions, key activities, and revenue levers to reveal how the bank wins and scales in regional markets.

Partnerships

Fintech and Technology Providers

The bank partners with core processors like FIS and FinTech developers to power mobile banking, online account opening, and integrated payments, cutting in-house R&D costs; MidWestOne reported 38% of new deposits via digital channels in 2024.

Correspondent Banking Networks

MidWestOne partners with money-center banks to route international payments and offer treasury services, giving clients access to SWIFT global payment rails and liquidity tools; as of 2024 these correspondent links supported roughly $1.2 billion in cross-border flows annually for the bank’s commercial portfolio. These networks let regional firms manage FX and working capital across global supply chains efficiently.

Insurance and Wealth Affiliates

MidWestOne partners with national carriers and investment firms to distribute annuities, life insurance, and mutual funds via its wealth division; in 2024 these non-deposit products generated roughly 12% of fee revenue, helping boost average customer wallet share by an estimated $18,500 per high-net-worth household.

Government-Sponsored Enterprises

Strategic ties with the Small Business Administration and Fannie Mae let MidWestOne Bank originate SBA-guaranteed loans and sell conforming mortgages to the secondary market, cutting credit risk and freeing capital; in 2024 the bank sold roughly $150m+ in mortgage loans and participated in $75m of SBA-backed lending to support community development.

- Reduces credit risk via SBA guarantees

- Provides liquidity: ~$150m mortgage sales (2024)

- Supports community lending: ~$75m SBA volume (2024)

Local Community and Economic Groups

MidWestOne Bank partners with regional chambers and economic development corporations to source local growth deals, inform community reinvestment projects, and target small-business lending; in 2025 these ties helped generate roughly 18% of new commercial relationships and supported $120M in community loans across Iowa and Minnesota in 2024.

- Referral share: ~18% of new commercial clients

- Community loans supported: $120,000,000 (2024)

- Focus regions: Iowa, Minnesota—localized lending pipelines

MidWestOne’s partner-driven model fuels deposits, cross-border flows, wealth & community lending

MidWestOne leverages core processors (FIS) and fintechs to drive digital deposits (38% of new deposits, 2024), correspondent banks for $1.2B cross-border flows (2024), wealth partners for 12% of fee revenue (adds ~$18,500 wallet per HNW), SBA/Fannie ties for ~$150M mortgage sales and $75M SBA lending (2024), and local economic partners generating ~18% new commercial clients and $120M community loans (2024).

| Partnership | Key 2024 Metric |

|---|---|

| Digital providers | 38% new deposits |

| Correspondents | $1.2B cross-border |

| Wealth partners | 12% fee rev, +$18,500 HNW |

| SBA/Fannie | $150M mortgages, $75M SBA |

| Local dev | 18% new clients, $120M loans |

What is included in the product

A concise, pre-written Business Model Canvas for MidWestOne Bank detailing customer segments, channels, value propositions, revenue streams, and key activities across the nine BMC blocks, reflecting real-world banking operations and strategic priorities to support presentations, investor discussions, and strategic decision-making.

High-level, editable Business Model Canvas that condenses MidWestOne Bank’s strategy into a single page, saving hours of structuring while enabling quick comparison, team collaboration, and board-ready presentations.

Activities

Commercial and Retail Lending

MidWestOne Bank underwrites and manages commercial real estate, agricultural, and consumer loans, with $8.4 billion in total loans held for investment as of 2025, using rigorous credit analysis and quarterly portfolio monitoring to maintain asset quality (nonperforming loans 0.45% in Q4 2024). Lending drives balance-sheet growth and interest income, contributing roughly 72% of net interest revenue in 2024.

Deposit and Liquidity Management

MidWestOne Bank attracts and retains core deposits via checking, savings and CDs—$6.4B in deposits as of 12/31/2024—balancing liquidity needs with cost of funds to protect a net interest margin (NIM) that was 3.45% in 2024; efficient deposit gathering funds lending (loans/leases $5.2B) and ensures compliance with liquidity coverage and reserve rules, keeping loan-to-deposit near 81% to meet regulatory and stress-test buffers.

Wealth Management and Trust Services

MidWestOne provides fiduciary services, investment management, and estate planning to HNW individuals and institutions, requiring specialist asset-allocation skills and trust-administration compliance; in 2024 trust-related fees contributed roughly $45M to noninterest income, helping fee revenue make up about 38% of total revenue and boosting client retention rates above 85% for HNW segments.

Digital Banking Operations

Risk Management and Compliance

Ongoing monitoring of federal and Iowa regulatory changes plus quarterly internal audits keep MidWestOne Bank aligned with Bank Secrecy Act and AML rules and inform capital adequacy reviews; as of 2025 the bank reports a CET1 ratio of 11.8% and AML SAR filings rose 9% YoY.

Robust risk management reduces legal fines and reputational loss, lowering expected regulatory cost volatility and supporting stable lending operations.

- Quarterly audits and regulatory scans

- BSA/AML program with SAR increases +9% (2025)

- CET1 ratio 11.8% (2025)

- Capital adequacy stress tests annually

MidWestOne: $8.4B loans, $6.4B deposits, 3.45% NIM, 11.8% CET1, 0.45% NPL

MidWestOne originates and services $8.4B loans (2025) and manages $6.4B deposits (12/31/24), driving ~72% of net interest revenue with NIM 3.45% (2024) while trust fees ~$45M support fee income; CET1 11.8% (2025) and NPL 0.45% (Q4 2024) reflect tight credit and risk controls.

| Metric | Value |

|---|---|

| Total loans (held) | $8.4B (2025) |

| Deposits | $6.4B (12/31/24) |

| NIM | 3.45% (2024) |

| Trust fees | $45M (2024) |

| CET1 | 11.8% (2025) |

| NPL | 0.45% (Q4 2024) |

Full Version Awaits

Business Model Canvas

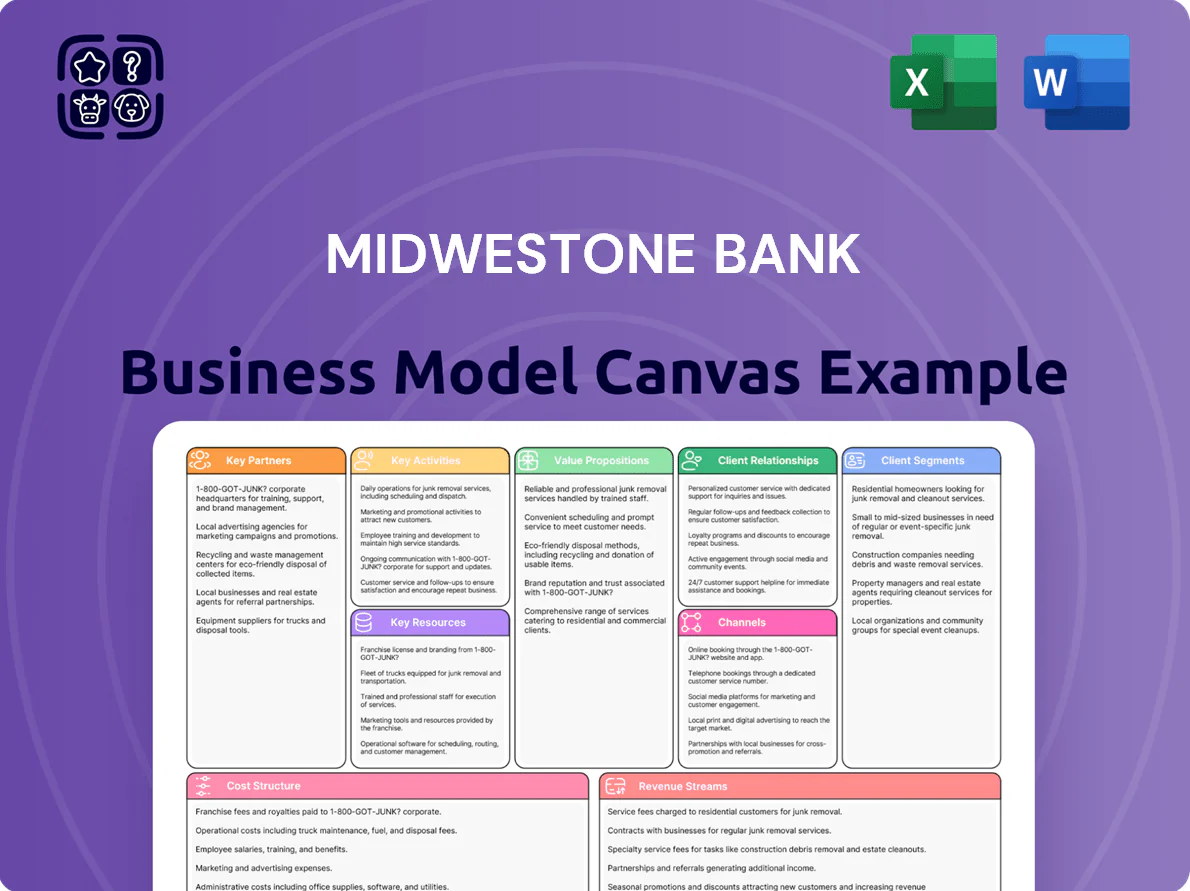

The MidWestOne Bank Business Model Canvas shown here is the actual deliverable, not a mockup—this preview is a direct excerpt from the final file you’ll receive after purchase.

When you complete your order, you’ll instantly get the same professionally formatted document in editable Word and Excel formats, with all sections and content included exactly as shown.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

MidWestOne Bank: Business Model Canvas—Strategy, Customers & Revenue Drivers

Unlock the full strategic blueprint behind MidWestOne Bank with our Business Model Canvas—detailing customer segments, value propositions, key activities, and revenue levers to reveal how the bank wins and scales in regional markets.

Partnerships

Fintech and Technology Providers

The bank partners with core processors like FIS and FinTech developers to power mobile banking, online account opening, and integrated payments, cutting in-house R&D costs; MidWestOne reported 38% of new deposits via digital channels in 2024.

Correspondent Banking Networks

MidWestOne partners with money-center banks to route international payments and offer treasury services, giving clients access to SWIFT global payment rails and liquidity tools; as of 2024 these correspondent links supported roughly $1.2 billion in cross-border flows annually for the bank’s commercial portfolio. These networks let regional firms manage FX and working capital across global supply chains efficiently.

Insurance and Wealth Affiliates

MidWestOne partners with national carriers and investment firms to distribute annuities, life insurance, and mutual funds via its wealth division; in 2024 these non-deposit products generated roughly 12% of fee revenue, helping boost average customer wallet share by an estimated $18,500 per high-net-worth household.

Government-Sponsored Enterprises

Strategic ties with the Small Business Administration and Fannie Mae let MidWestOne Bank originate SBA-guaranteed loans and sell conforming mortgages to the secondary market, cutting credit risk and freeing capital; in 2024 the bank sold roughly $150m+ in mortgage loans and participated in $75m of SBA-backed lending to support community development.

- Reduces credit risk via SBA guarantees

- Provides liquidity: ~$150m mortgage sales (2024)

- Supports community lending: ~$75m SBA volume (2024)

Local Community and Economic Groups

MidWestOne Bank partners with regional chambers and economic development corporations to source local growth deals, inform community reinvestment projects, and target small-business lending; in 2025 these ties helped generate roughly 18% of new commercial relationships and supported $120M in community loans across Iowa and Minnesota in 2024.

- Referral share: ~18% of new commercial clients

- Community loans supported: $120,000,000 (2024)

- Focus regions: Iowa, Minnesota—localized lending pipelines

MidWestOne’s partner-driven model fuels deposits, cross-border flows, wealth & community lending

MidWestOne leverages core processors (FIS) and fintechs to drive digital deposits (38% of new deposits, 2024), correspondent banks for $1.2B cross-border flows (2024), wealth partners for 12% of fee revenue (adds ~$18,500 wallet per HNW), SBA/Fannie ties for ~$150M mortgage sales and $75M SBA lending (2024), and local economic partners generating ~18% new commercial clients and $120M community loans (2024).

| Partnership | Key 2024 Metric |

|---|---|

| Digital providers | 38% new deposits |

| Correspondents | $1.2B cross-border |

| Wealth partners | 12% fee rev, +$18,500 HNW |

| SBA/Fannie | $150M mortgages, $75M SBA |

| Local dev | 18% new clients, $120M loans |

What is included in the product

A concise, pre-written Business Model Canvas for MidWestOne Bank detailing customer segments, channels, value propositions, revenue streams, and key activities across the nine BMC blocks, reflecting real-world banking operations and strategic priorities to support presentations, investor discussions, and strategic decision-making.

High-level, editable Business Model Canvas that condenses MidWestOne Bank’s strategy into a single page, saving hours of structuring while enabling quick comparison, team collaboration, and board-ready presentations.

Activities

Commercial and Retail Lending

MidWestOne Bank underwrites and manages commercial real estate, agricultural, and consumer loans, with $8.4 billion in total loans held for investment as of 2025, using rigorous credit analysis and quarterly portfolio monitoring to maintain asset quality (nonperforming loans 0.45% in Q4 2024). Lending drives balance-sheet growth and interest income, contributing roughly 72% of net interest revenue in 2024.

Deposit and Liquidity Management

MidWestOne Bank attracts and retains core deposits via checking, savings and CDs—$6.4B in deposits as of 12/31/2024—balancing liquidity needs with cost of funds to protect a net interest margin (NIM) that was 3.45% in 2024; efficient deposit gathering funds lending (loans/leases $5.2B) and ensures compliance with liquidity coverage and reserve rules, keeping loan-to-deposit near 81% to meet regulatory and stress-test buffers.

Wealth Management and Trust Services

MidWestOne provides fiduciary services, investment management, and estate planning to HNW individuals and institutions, requiring specialist asset-allocation skills and trust-administration compliance; in 2024 trust-related fees contributed roughly $45M to noninterest income, helping fee revenue make up about 38% of total revenue and boosting client retention rates above 85% for HNW segments.

Digital Banking Operations

Risk Management and Compliance

Ongoing monitoring of federal and Iowa regulatory changes plus quarterly internal audits keep MidWestOne Bank aligned with Bank Secrecy Act and AML rules and inform capital adequacy reviews; as of 2025 the bank reports a CET1 ratio of 11.8% and AML SAR filings rose 9% YoY.

Robust risk management reduces legal fines and reputational loss, lowering expected regulatory cost volatility and supporting stable lending operations.

- Quarterly audits and regulatory scans

- BSA/AML program with SAR increases +9% (2025)

- CET1 ratio 11.8% (2025)

- Capital adequacy stress tests annually

MidWestOne: $8.4B loans, $6.4B deposits, 3.45% NIM, 11.8% CET1, 0.45% NPL

MidWestOne originates and services $8.4B loans (2025) and manages $6.4B deposits (12/31/24), driving ~72% of net interest revenue with NIM 3.45% (2024) while trust fees ~$45M support fee income; CET1 11.8% (2025) and NPL 0.45% (Q4 2024) reflect tight credit and risk controls.

| Metric | Value |

|---|---|

| Total loans (held) | $8.4B (2025) |

| Deposits | $6.4B (12/31/24) |

| NIM | 3.45% (2024) |

| Trust fees | $45M (2024) |

| CET1 | 11.8% (2025) |

| NPL | 0.45% (Q4 2024) |

Full Version Awaits

Business Model Canvas

The MidWestOne Bank Business Model Canvas shown here is the actual deliverable, not a mockup—this preview is a direct excerpt from the final file you’ll receive after purchase.

When you complete your order, you’ll instantly get the same professionally formatted document in editable Word and Excel formats, with all sections and content included exactly as shown.