M/I Homes Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

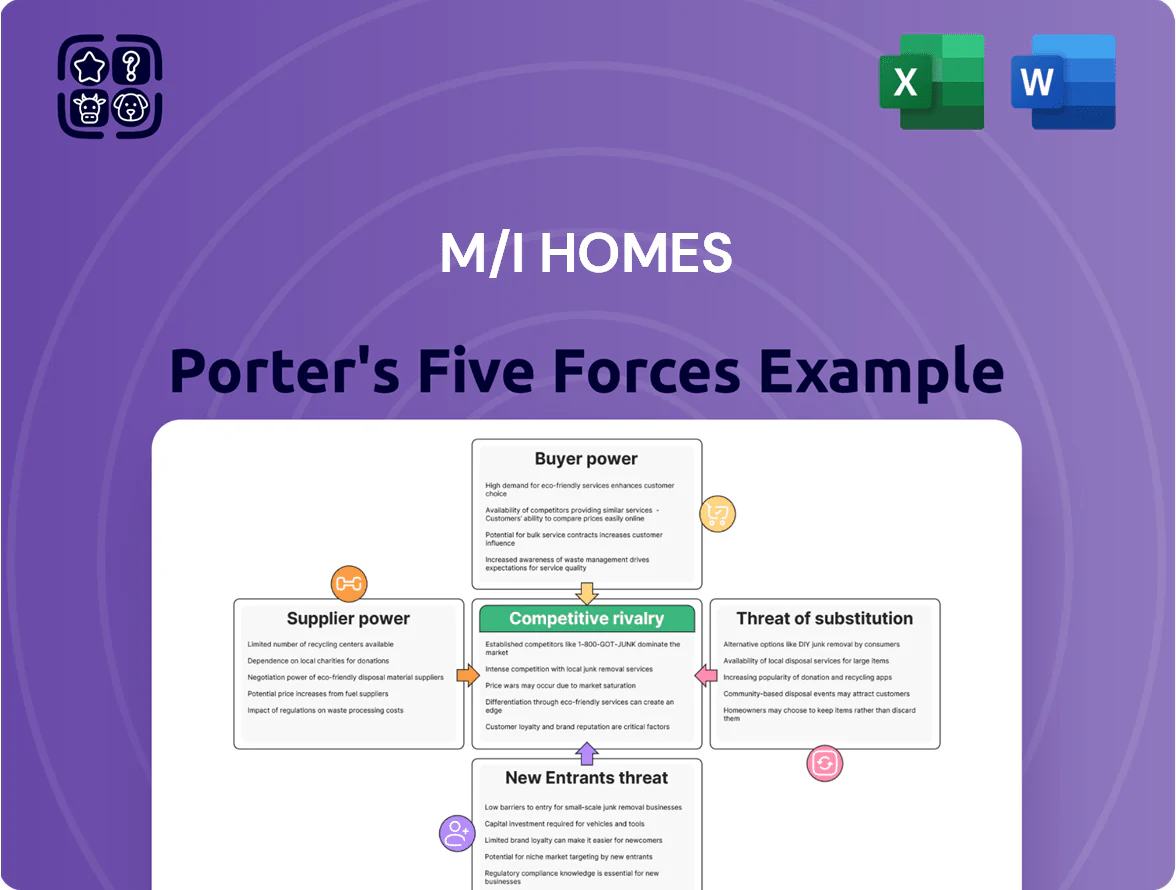

M/I Homes faces intense rivalry from regional and national builders, moderate supplier leverage for land and materials, growing buyer sophistication, and manageable threat from substitutes but rising risk from modular/offsite construction.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore M/I Homes’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Skilled Labor Shortages

The US construction sector faced a shortage of about 400,000 skilled trades workers (electricians, plumbers, carpenters) in Q3 2025, giving subcontractors pricing power to push wage rates up roughly 6–9% year-over-year; this raises M/I Homes’ input costs and compresses margins.

To keep production steady and protect quality, M/I Homes must secure long-term contracts, offer premium pay or retention bonuses, and invest in preferred-vendor pipelines to avoid schedule slippage.

Raw Material Price Volatility

Suppliers of lumber, concrete, and steel exert moderate-high power for M/I Homes; lumber futures rose 28% in 2020–21 and global steel prices climbed ~50% in 2021–22, creating lasting volatility.

M/I Homes gets volume discounts but is mostly a price taker—21% of 2024 COGS linked to commodity inflation—so international tariffs and trade shifts matter.

Sudden material cost spikes hit gross margin directly; a $3,000 increase per home (example) cuts gross margin by ~200–300 bps unless costs are passed to buyers.

Land Availability and Development Costs

Landowners in high-growth metros hold leverage as shovel-ready lots shrink; national lot inventories fell ~17% year-over-year in 2024, tightening supply for M/I Homes.

M/I Homes competes with other homebuilders plus industrial/commercial developers for urban fringe sites, pushing bids higher and speeding land acquisition cycles.

Rising land costs—U.S. median lot price up ~12% in 2024—and local impact fees (often $10k–$50k per home in many Sun Belt markets) let sellers keep firm pricing in desirable submarkets.

Concentration of National Vendors

Concentration among national appliance, HVAC and flooring manufacturers—often 3–5 dominant firms per category—gives suppliers pricing power; when demand exceeds capacity, lead times and premiums rise, as seen in 2024 where appliance backlogs extended 8–12 weeks industry-wide.

M/I Homes depends on these suppliers to meet modern-amenity expectations for first-time and move-up buyers, so supplier constraints can directly raise build costs and delay closings.

- Top-3 supplier share: ~60–80% per category

- Typical 2024 appliance backlog: 8–12 weeks

- Supplier-driven cost pressure: adds 1–3% to build cost

Limited Vertical Integration

Unlike some larger builders that self-perform trades, M/I Homes relies heavily on third-party suppliers for construction, increasing supplier bargaining power in local markets; in 2024 subcontracted costs represented an estimated 38–45% of cost of homes sold per industry data.

Localized suppliers control specialized labor and equipment, so shortages or price hikes (e.g., lumber +12% in 2024) can squeeze margins; management offsets this via strategic procurement and multiyear contracts signed with key trades.

- High subcontracting: ~40% of build costs

- Local supplier concentration raises price risk

- Multiyear contracts reduce volatility

- Strategic procurement needed to protect margins

Supplier squeeze: trades shortage, rising lot costs and commodity-linked build inflation

Suppliers hold moderate‑high power: skilled trades short by ~400,000 (Q3 2025) and subcontracting ~40% of build costs; commodity-linked COGS ~21% (2024), appliance backlogs 8–12 weeks, lot inventories down 17% (2024) and median lot price +12% (2024), all adding 1–3% to build cost unless passed to buyers.

| Metric | Value |

|---|---|

| Skilled trades gap | ~400,000 (Q3 2025) |

| Subcontracting share | ~40% of build costs |

| Commodity COGS link | 21% (2024) |

| Lot inventory change | -17% YoY (2024) |

| Median lot price | +12% (2024) |

What is included in the product

Concise Porter's Five Forces overview for M/I Homes examining rivalry, buyer and supplier power, threat of new entrants, and substitutes to reveal competitive pressures, pricing leverage, and strategic vulnerabilities in the U.S. homebuilding market.

A concise Porter's Five Forces one-sheet for M/I Homes—quickly spot competitive pressures and prioritize strategic moves.

Customers Bargaining Power

Mortgage Rate Sensitivity

Information Transparency and Digital Comparison

Modern homebuyers use online platforms to compare floor plans, pricing, and amenities across builders instantly, and Zillow and Redfin report 93% of buyers research online before contact; this transparency cuts information asymmetry that once favored builders. As customers can shop micro-market pricing, M/I Homes must match local median new-home prices (US median new-home price was $414,900 in 2024) or risk losing leads. Real-time comparison tools also compress sales cycles, so competitive incentives and clear value propositions are critical to convert digitally sourced leads.

Expectation of Incentives

Buyers now expect incentives like $5k–$15k in closing help or upgraded finishes, pushing negotiation leverage up; the NAHB reported 2024 incentives rose 18% year-over-year.

M/I Homes uses these incentives to sustain sales velocity—inventory turnover slipped to 5.2 months in Q3 2025 without incentives, so promotions cut hold times and limit carrying costs.

Low Switching Costs

Until a purchase agreement and deposit are in place, buyers face virtually zero switching costs from M/I Homes to rivals; industry surveys in 2024 showed 62% of new-home shoppers considered at least three builders before contracting.

The large supply in new-construction and resale markets—US housing starts at 1.48M in 2024—lets buyers walk away if price or specs mismatch, pressuring M/I to win commitments early.

So M/I emphasizes service, upgrades, and loyalty programs to convert tours into signed contracts; closings lag if conversion rates drop below 25%.

- Zero pre-deposit switching costs

- 62% shop 3+ builders (2024)

- US starts 1.48M (2024) increase choice

- Focus: service, upgrades, loyalty to raise conversion

Demographic Shifts and Buyer Preferences

- 45% of buyers: Millennial/Gen Z (NAR 2024)

- 3–5% resale boost from modern/sustainable features

- ~15% lower utilities with high-efficiency systems

- 62% conduct extensive online home research (Zillow 2024)

Buyers Hold Leverage: Rate Shock Costs ~8%—Builders Must Offer Buy‑Downs, Upgrades, Fast Conversions

| Metric | Value |

|---|---|

| Rate swing impact | ~8% buying power loss |

| Shoppers/ builders | 62% (2024) |

| Incentives growth | +18% (2024) |

Full Version Awaits

M/I Homes Porter's Five Forces Analysis

This preview shows the exact M/I Homes Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups—fully formatted, professionally written, and ready for download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

M/I Homes faces intense rivalry from regional and national builders, moderate supplier leverage for land and materials, growing buyer sophistication, and manageable threat from substitutes but rising risk from modular/offsite construction.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore M/I Homes’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Skilled Labor Shortages

The US construction sector faced a shortage of about 400,000 skilled trades workers (electricians, plumbers, carpenters) in Q3 2025, giving subcontractors pricing power to push wage rates up roughly 6–9% year-over-year; this raises M/I Homes’ input costs and compresses margins.

To keep production steady and protect quality, M/I Homes must secure long-term contracts, offer premium pay or retention bonuses, and invest in preferred-vendor pipelines to avoid schedule slippage.

Raw Material Price Volatility

Suppliers of lumber, concrete, and steel exert moderate-high power for M/I Homes; lumber futures rose 28% in 2020–21 and global steel prices climbed ~50% in 2021–22, creating lasting volatility.

M/I Homes gets volume discounts but is mostly a price taker—21% of 2024 COGS linked to commodity inflation—so international tariffs and trade shifts matter.

Sudden material cost spikes hit gross margin directly; a $3,000 increase per home (example) cuts gross margin by ~200–300 bps unless costs are passed to buyers.

Land Availability and Development Costs

Landowners in high-growth metros hold leverage as shovel-ready lots shrink; national lot inventories fell ~17% year-over-year in 2024, tightening supply for M/I Homes.

M/I Homes competes with other homebuilders plus industrial/commercial developers for urban fringe sites, pushing bids higher and speeding land acquisition cycles.

Rising land costs—U.S. median lot price up ~12% in 2024—and local impact fees (often $10k–$50k per home in many Sun Belt markets) let sellers keep firm pricing in desirable submarkets.

Concentration of National Vendors

Concentration among national appliance, HVAC and flooring manufacturers—often 3–5 dominant firms per category—gives suppliers pricing power; when demand exceeds capacity, lead times and premiums rise, as seen in 2024 where appliance backlogs extended 8–12 weeks industry-wide.

M/I Homes depends on these suppliers to meet modern-amenity expectations for first-time and move-up buyers, so supplier constraints can directly raise build costs and delay closings.

- Top-3 supplier share: ~60–80% per category

- Typical 2024 appliance backlog: 8–12 weeks

- Supplier-driven cost pressure: adds 1–3% to build cost

Limited Vertical Integration

Unlike some larger builders that self-perform trades, M/I Homes relies heavily on third-party suppliers for construction, increasing supplier bargaining power in local markets; in 2024 subcontracted costs represented an estimated 38–45% of cost of homes sold per industry data.

Localized suppliers control specialized labor and equipment, so shortages or price hikes (e.g., lumber +12% in 2024) can squeeze margins; management offsets this via strategic procurement and multiyear contracts signed with key trades.

- High subcontracting: ~40% of build costs

- Local supplier concentration raises price risk

- Multiyear contracts reduce volatility

- Strategic procurement needed to protect margins

Supplier squeeze: trades shortage, rising lot costs and commodity-linked build inflation

Suppliers hold moderate‑high power: skilled trades short by ~400,000 (Q3 2025) and subcontracting ~40% of build costs; commodity-linked COGS ~21% (2024), appliance backlogs 8–12 weeks, lot inventories down 17% (2024) and median lot price +12% (2024), all adding 1–3% to build cost unless passed to buyers.

| Metric | Value |

|---|---|

| Skilled trades gap | ~400,000 (Q3 2025) |

| Subcontracting share | ~40% of build costs |

| Commodity COGS link | 21% (2024) |

| Lot inventory change | -17% YoY (2024) |

| Median lot price | +12% (2024) |

What is included in the product

Concise Porter's Five Forces overview for M/I Homes examining rivalry, buyer and supplier power, threat of new entrants, and substitutes to reveal competitive pressures, pricing leverage, and strategic vulnerabilities in the U.S. homebuilding market.

A concise Porter's Five Forces one-sheet for M/I Homes—quickly spot competitive pressures and prioritize strategic moves.

Customers Bargaining Power

Mortgage Rate Sensitivity

Information Transparency and Digital Comparison

Modern homebuyers use online platforms to compare floor plans, pricing, and amenities across builders instantly, and Zillow and Redfin report 93% of buyers research online before contact; this transparency cuts information asymmetry that once favored builders. As customers can shop micro-market pricing, M/I Homes must match local median new-home prices (US median new-home price was $414,900 in 2024) or risk losing leads. Real-time comparison tools also compress sales cycles, so competitive incentives and clear value propositions are critical to convert digitally sourced leads.

Expectation of Incentives

Buyers now expect incentives like $5k–$15k in closing help or upgraded finishes, pushing negotiation leverage up; the NAHB reported 2024 incentives rose 18% year-over-year.

M/I Homes uses these incentives to sustain sales velocity—inventory turnover slipped to 5.2 months in Q3 2025 without incentives, so promotions cut hold times and limit carrying costs.

Low Switching Costs

Until a purchase agreement and deposit are in place, buyers face virtually zero switching costs from M/I Homes to rivals; industry surveys in 2024 showed 62% of new-home shoppers considered at least three builders before contracting.

The large supply in new-construction and resale markets—US housing starts at 1.48M in 2024—lets buyers walk away if price or specs mismatch, pressuring M/I to win commitments early.

So M/I emphasizes service, upgrades, and loyalty programs to convert tours into signed contracts; closings lag if conversion rates drop below 25%.

- Zero pre-deposit switching costs

- 62% shop 3+ builders (2024)

- US starts 1.48M (2024) increase choice

- Focus: service, upgrades, loyalty to raise conversion

Demographic Shifts and Buyer Preferences

- 45% of buyers: Millennial/Gen Z (NAR 2024)

- 3–5% resale boost from modern/sustainable features

- ~15% lower utilities with high-efficiency systems

- 62% conduct extensive online home research (Zillow 2024)

Buyers Hold Leverage: Rate Shock Costs ~8%—Builders Must Offer Buy‑Downs, Upgrades, Fast Conversions

| Metric | Value |

|---|---|

| Rate swing impact | ~8% buying power loss |

| Shoppers/ builders | 62% (2024) |

| Incentives growth | +18% (2024) |

Full Version Awaits

M/I Homes Porter's Five Forces Analysis

This preview shows the exact M/I Homes Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups—fully formatted, professionally written, and ready for download and use the moment you buy.