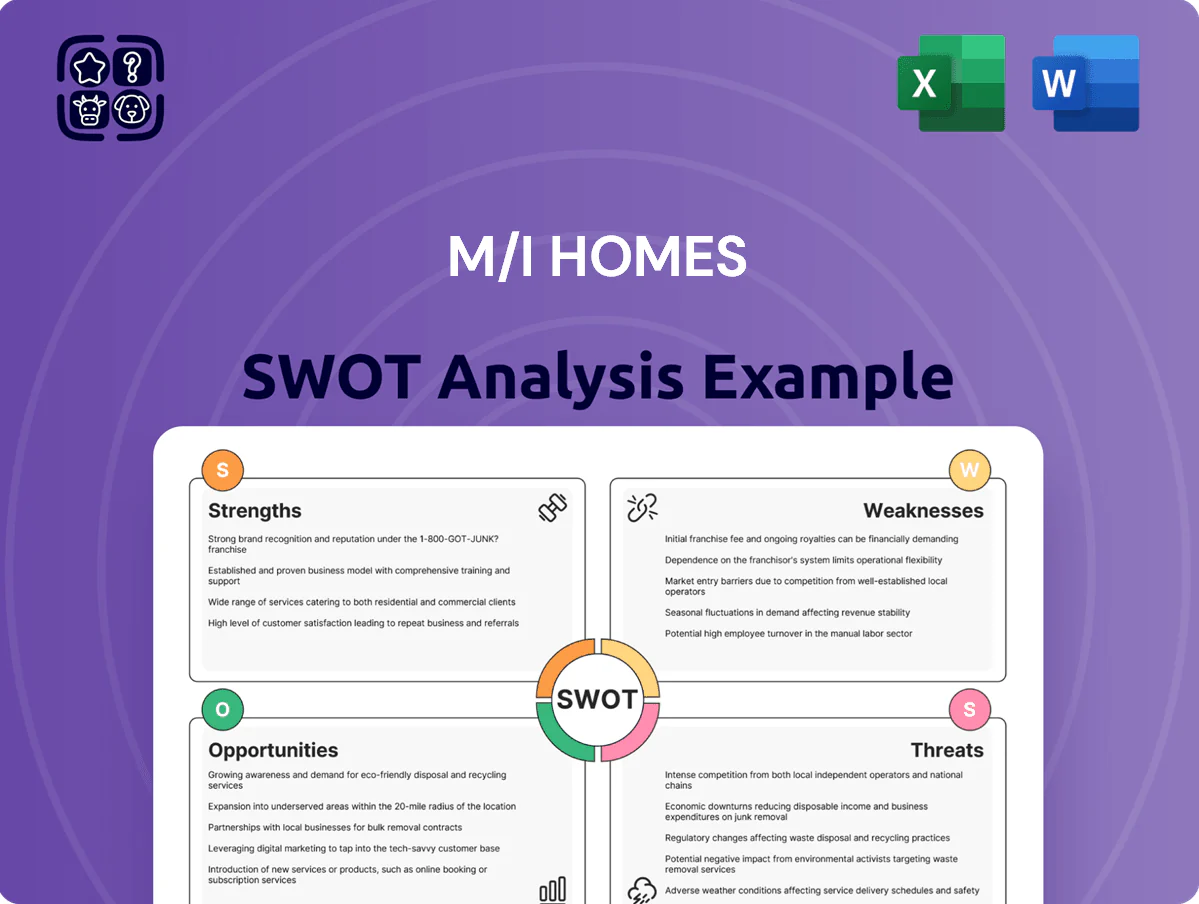

M/I Homes SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

M/I Homes shows solid regional brand strength, disciplined land acquisition, and steady margins, but faces supply-chain risks, labor constraints, and exposure to housing-cycle swings; strategic diversification and margin management will be key. Discover the full SWOT analysis for a research-backed, investor-ready report with Word and Excel deliverables to support planning, pitches, and investment decisions.

Strengths

Diversified Product Portfolio

M/I Homes offers a broad portfolio from the entry-level Smart Series to luxury move-up homes, letting it target first-time buyers and higher-income buyers alike. In 2024 M/I delivered 4,145 homes, spreading mix risk across segments and supporting a 2024 gross margin of ~18.2%. This balanced inventory helps absorb demand shifts—if entry-level sales slow, move-up demand can stabilize revenue. The strategy reduced segment concentration risk during 2023–24 market swings.

Integrated Financial Services

Through M/I Financial, M/I Homes offers in-house mortgage and title services that speed closings and improve satisfaction; in 2024 M/I Financial funded roughly $1.1 billion in loans, adding material fee income and lowering third-party delays.

Strategic Market Positioning

Operational Efficiency

M/I Homes keeps gross margins near 20% (FY 2024 GAAP gross margin 19.8%) by disciplined cost control and tight cycle management, trimming build times via standardized processes and long-term vendor contracts.

This efficiency enables competitive pricing for buyers and delivered ROE of ~16% in 2024, supporting shareholder returns even through volatile input costs.

- FY24 gross margin 19.8%

- FY24 return on equity ~16%

- Standardized builds cut cycle time and waste

- Long-term vendor deals lower input volatility

Strong Financial Position

- Net debt/EBITDA ~1.0x

- Cash ≈ $420M

- 2025 land commitments > $300M

- Equity ≈ $1.8B

M/I Homes: 4,145 builds, $2.9B revenue, ~20% gross margin, strong balance sheet

M/I Homes mixes entry-to-luxury products, delivered 4,145 homes in 2024, GAAP gross margin 19.8% and ROE ~16% (FY24); M/I Financial funded ~$1.1B in 2024, aiding closings; operations focused in growth metros drove $2.9B 2024 revenue; net debt/EBITDA ~1.0x, cash ~$420M, 2025 land commitments >$300M.

| Metric | Value |

|---|---|

| Homes delivered (2024) | 4,145 |

| Revenue (2024) | $2.9B |

| GAAP gross margin (FY24) | 19.8% |

| ROE (FY24) | ~16% |

| M/I Financial loans (2024) | $1.1B |

| Net debt/EBITDA | ~1.0x |

| Cash | $420M |

| 2025 land commitments | >$300M |

What is included in the product

Provides a concise SWOT overview of M/I Homes, highlighting internal strengths and weaknesses alongside external opportunities and threats to assess the company’s strategic positioning and growth prospects.

Delivers a concise SWOT matrix for M/I Homes that speeds strategic alignment and stakeholder briefings with clean, editable formatting for quick updates and integration into reports.

Weaknesses

Geographic Concentration

M/I Homes still gets roughly 60% of revenue from Ohio, Michigan, Indiana, and Florida, so regional recessions or hurricanes hit results hard; in 2024 metro-level weakness drove a 22% drop in closings in two core markets.

Dependence on External Labor

Like peers, M/I Homes depends on third-party subcontractors for construction; subcontracted labor accounted for an estimated 60–70% of onsite costs in 2024, per industry split, raising exposure to shortages.

Skilled-trades shortages pushed wage rates up ~8–12% nationally in 2023–24, so M/I Faces higher direct labor inflation and margin pressure if costs aren’t passed to buyers.

Any contractor disruptions can delay closings; in 2024 average community build delay rose to ~21 days, increasing overhead and carrying costs for M/I.

Interest Rate Sensitivity

Supply Chain Vulnerabilities

- Material costs rose ~12% YoY (Q4 2024)

- Inventory days: company-reported build materials not publicly disaggregated

- Exposure: lumber, steel, concrete price volatility

Limited Scale vs Industry Leaders

Compared with the largest national builders (D.R. Horton, Lennar), M/I Homes held about 1.2% US market share in 2024 versus D.R. Horton’s ~13% (2024 U.S. starts), which weakens its supplier leverage and increases per-unit input costs.

This scale gap limits influence on prime land deals and can compress margins—M/I’s 2024 gross margin was 20.8% vs. industry leaders near 24–26%—so it must target niche segments or stronger product differentiation.

- ~1.2% US share (M/I Homes, 2024)

- D.R. Horton ~13% (2024)

- M/I gross margin 20.8% (2024)

- Industry leader margins 24–26% (2024)

- Strategy: niche focus or product premium

Regionally concentrated builder faces margin squeeze from subcontractor costs & delays

Concentrated geography (60% revenue in OH/MI/IN/FL) raises regional risk; 2024 saw a 22% closings drop in two core metros. Heavy subcontractor reliance (≈60–70% onsite cost) plus 8–12% trade wage inflation pushed delays (~21 days) and margin pressure. Scale gap (≈1.2% US share) limits supplier and land leverage; 2024 gross margin 20.8% vs leaders 24–26%.

| Metric | 2024 |

|---|---|

| Geographic concentration | 60% revenue |

| Closings drop | 22% (two metros) |

| Subcontractor share | 60–70% |

| Wage inflation | 8–12% |

| Build delays | ~21 days |

| US market share | ~1.2% |

| Gross margin | 20.8% |

| Leader margins | 24–26% |

Preview Before You Purchase

M/I Homes SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality; the preview below is taken directly from the full report and reflects the editable, structured file unlocked after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete SWOT Report

M/I Homes shows solid regional brand strength, disciplined land acquisition, and steady margins, but faces supply-chain risks, labor constraints, and exposure to housing-cycle swings; strategic diversification and margin management will be key. Discover the full SWOT analysis for a research-backed, investor-ready report with Word and Excel deliverables to support planning, pitches, and investment decisions.

Strengths

Diversified Product Portfolio

M/I Homes offers a broad portfolio from the entry-level Smart Series to luxury move-up homes, letting it target first-time buyers and higher-income buyers alike. In 2024 M/I delivered 4,145 homes, spreading mix risk across segments and supporting a 2024 gross margin of ~18.2%. This balanced inventory helps absorb demand shifts—if entry-level sales slow, move-up demand can stabilize revenue. The strategy reduced segment concentration risk during 2023–24 market swings.

Integrated Financial Services

Through M/I Financial, M/I Homes offers in-house mortgage and title services that speed closings and improve satisfaction; in 2024 M/I Financial funded roughly $1.1 billion in loans, adding material fee income and lowering third-party delays.

Strategic Market Positioning

Operational Efficiency

M/I Homes keeps gross margins near 20% (FY 2024 GAAP gross margin 19.8%) by disciplined cost control and tight cycle management, trimming build times via standardized processes and long-term vendor contracts.

This efficiency enables competitive pricing for buyers and delivered ROE of ~16% in 2024, supporting shareholder returns even through volatile input costs.

- FY24 gross margin 19.8%

- FY24 return on equity ~16%

- Standardized builds cut cycle time and waste

- Long-term vendor deals lower input volatility

Strong Financial Position

- Net debt/EBITDA ~1.0x

- Cash ≈ $420M

- 2025 land commitments > $300M

- Equity ≈ $1.8B

M/I Homes: 4,145 builds, $2.9B revenue, ~20% gross margin, strong balance sheet

M/I Homes mixes entry-to-luxury products, delivered 4,145 homes in 2024, GAAP gross margin 19.8% and ROE ~16% (FY24); M/I Financial funded ~$1.1B in 2024, aiding closings; operations focused in growth metros drove $2.9B 2024 revenue; net debt/EBITDA ~1.0x, cash ~$420M, 2025 land commitments >$300M.

| Metric | Value |

|---|---|

| Homes delivered (2024) | 4,145 |

| Revenue (2024) | $2.9B |

| GAAP gross margin (FY24) | 19.8% |

| ROE (FY24) | ~16% |

| M/I Financial loans (2024) | $1.1B |

| Net debt/EBITDA | ~1.0x |

| Cash | $420M |

| 2025 land commitments | >$300M |

What is included in the product

Provides a concise SWOT overview of M/I Homes, highlighting internal strengths and weaknesses alongside external opportunities and threats to assess the company’s strategic positioning and growth prospects.

Delivers a concise SWOT matrix for M/I Homes that speeds strategic alignment and stakeholder briefings with clean, editable formatting for quick updates and integration into reports.

Weaknesses

Geographic Concentration

M/I Homes still gets roughly 60% of revenue from Ohio, Michigan, Indiana, and Florida, so regional recessions or hurricanes hit results hard; in 2024 metro-level weakness drove a 22% drop in closings in two core markets.

Dependence on External Labor

Like peers, M/I Homes depends on third-party subcontractors for construction; subcontracted labor accounted for an estimated 60–70% of onsite costs in 2024, per industry split, raising exposure to shortages.

Skilled-trades shortages pushed wage rates up ~8–12% nationally in 2023–24, so M/I Faces higher direct labor inflation and margin pressure if costs aren’t passed to buyers.

Any contractor disruptions can delay closings; in 2024 average community build delay rose to ~21 days, increasing overhead and carrying costs for M/I.

Interest Rate Sensitivity

Supply Chain Vulnerabilities

- Material costs rose ~12% YoY (Q4 2024)

- Inventory days: company-reported build materials not publicly disaggregated

- Exposure: lumber, steel, concrete price volatility

Limited Scale vs Industry Leaders

Compared with the largest national builders (D.R. Horton, Lennar), M/I Homes held about 1.2% US market share in 2024 versus D.R. Horton’s ~13% (2024 U.S. starts), which weakens its supplier leverage and increases per-unit input costs.

This scale gap limits influence on prime land deals and can compress margins—M/I’s 2024 gross margin was 20.8% vs. industry leaders near 24–26%—so it must target niche segments or stronger product differentiation.

- ~1.2% US share (M/I Homes, 2024)

- D.R. Horton ~13% (2024)

- M/I gross margin 20.8% (2024)

- Industry leader margins 24–26% (2024)

- Strategy: niche focus or product premium

Regionally concentrated builder faces margin squeeze from subcontractor costs & delays

Concentrated geography (60% revenue in OH/MI/IN/FL) raises regional risk; 2024 saw a 22% closings drop in two core metros. Heavy subcontractor reliance (≈60–70% onsite cost) plus 8–12% trade wage inflation pushed delays (~21 days) and margin pressure. Scale gap (≈1.2% US share) limits supplier and land leverage; 2024 gross margin 20.8% vs leaders 24–26%.

| Metric | 2024 |

|---|---|

| Geographic concentration | 60% revenue |

| Closings drop | 22% (two metros) |

| Subcontractor share | 60–70% |

| Wage inflation | 8–12% |

| Build delays | ~21 days |

| US market share | ~1.2% |

| Gross margin | 20.8% |

| Leader margins | 24–26% |

Preview Before You Purchase

M/I Homes SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality; the preview below is taken directly from the full report and reflects the editable, structured file unlocked after payment.