Banco Comercial Portugues Porter's Five Forces Analysis

Don't Miss the Bigger Picture

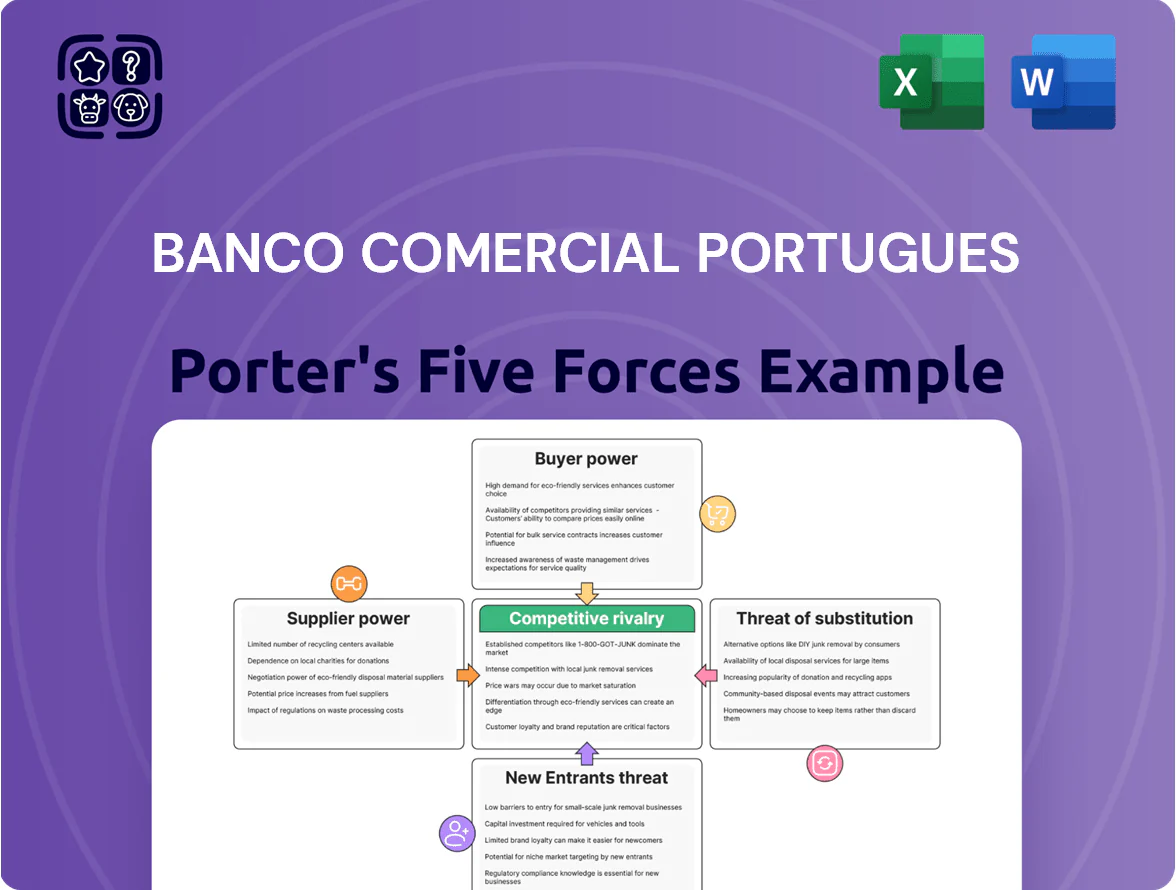

Banco Comercial Português faces moderate competitive rivalry with strong regional banks and fintech challengers, while regulatory barriers and branch network scale limit new entrants; supplier power is low but digitization raises substitute threats. This snapshot highlights strategic pressures on margins and growth potential. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Banco Comercial Portugues’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Central Bank and Regulatory Liquidity

As of late 2025 the European Central Bank (ECB) supplies primary liquidity and sets key rates; its deposit facility rate at 3.25% and targeted longer‑term refinancing operations shape Millennium BCP’s cost of funds and margins.

Millennium BCP’s funding mix—EUR 22.4bn customer deposits and EUR 6.8bn market funding at 9M2025—makes it highly sensitive to ECB policy shifts that alter capital costs.

Regulatory liquidity rules (LCR 142% at 3Q2025) and capital buffers (CET1 12.1% YE2024) constrain balance‑sheet responses, limiting rapid funding reallocation.

Technology and Fintech Infrastructure Providers

Banco Comercial Português depends on specialized global vendors for core banking, cloud, and cybersecurity; in 2024 about 62% of Portuguese banks reported using third‑party cloud services, raising dependency risks.

High technical complexity and integration mean switching costs are large—estimates show migration can cost 5–15% of annual IT budgets—giving suppliers strong bargaining power.

Need for continuous innovation to match digital challengers (neobanks grew ~28% users in Portugal 2023–24) further strengthens vendors’ leverage.

Human Capital and Specialized Labor

Intense competition for data scientists, risk managers and digital-banking specialists in Portugal tightens supplier power; a 2024 Cedefop report showed STEM vacancy rates rose 18% year-on-year, and Glassdoor data indicates median tech salaries in Lisbon climbed 12% in 2024.

BCP faces a small talent pool, so recruitment firms and employees command higher pay and benefits; Korn Ferry estimated Portugal had a 22% shortage in advanced IT skills in 2024.

To stop IP and staff flowing to London and Amsterdam fintech hubs, BCP must boost retention: expect multi-year spend increases—BCP reported HR costs up 9% in 2023—on training, equity, and remote work to remain competitive.

Debt Capital Markets and Institutional Investors

BCP funds long-term needs via covered bonds and subordinated debt to institutional investors; in 2024 it issued covered bonds totaling €1.2bn and €500m of Tier 2 notes, tying pricing to its Ba2/BB credit outlook.

Investor bargaining power rises if BCPs credit rating falls or Eurozone stress increases; in Q3 2025 a 100bp widening in Portuguese bank spreads would raise annual interest costs by ~€12m on €1.2bn.

Shifts in sentiment quickly change availability and yields—during 2022-23 stress, issuance windows narrowed and spreads jumped 150–250bps, showing supplier leverage.

- 2024 covered bonds €1.2bn; Tier 2 €500m

- Credit rating (Ba2/BB) drives pricing

- 100bp spread rise ≈ €12m annual cost on €1.2bn

- 2022–23 stress widened spreads 150–250bps

Deposit Base Granularity

Retail depositors are the primary suppliers of capital for Banco Comercial Português (BCP), but power is low because deposits are highly fragmented across ~6.5 million Portuguese retail accounts as of Dec 2024; no single depositor can exert leverage.

Collective flows respond to Iberian rate spreads; BCP lost ~€1.2bn in deposits to competitors during Q1–Q3 2024 when its savings rates trailed peers by ~40 bps.

By 2025 digital savings platforms increased liquidity mobility; 28% of retail deposits moved at least once yearly in 2024, raising price sensitivity and raising the cost of retaining marginal deposits.

- Fragmented base (~6.5M accounts) → low individual supplier power

- Rate competitiveness drove €1.2bn outflows in early 2024

- 28% of deposits mobile in 2024 → higher price sensitivity in 2025

Suppliers wield high leverage—IT costs, talent gap and mobile deposits squeeze funding

Suppliers (tech vendors, skilled staff, wholesale investors) hold moderate‑high bargaining power: large switching costs (IT migration 5–15% of IT spend), tight talent market (22% advanced IT skill gap 2024), and €1.7bn market funding (2024) tie pricing to BCP’s Ba2/BB rating; retail deposits remain low power but mobile (28% moved 2024), raising marginal funding costs.

| Metric | Value |

|---|---|

| IT migration cost | 5–15% annual IT budget |

| IT skill gap (Portugal) | 22% (2024) |

| Market funding | €6.8bn (9M2025) |

| Deposit mobility | 28% (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Banco Comercial Português, uncovering competitive drivers, buyer/supplier power, entry barriers, substitutes, and disruptive threats to its market position, with strategic insights for investors and planners.

Clear, one-sheet Porter's Five Forces for Banco Comercial Português—perfect for quick strategic decisions and boardroom slides.

Customers Bargaining Power

Low Switching Costs in Retail Banking

PSD3-driven open banking cut retail switching friction; EU data from 2025 shows 28% of Portuguese customers used account portability services, boosting bargaining power for borrowers.

Real-time aggregators let consumers compare rates instantly; average advertised mortgage spreads at Millennium BCP tightened to 1.35% in 2025 vs 1.60% in 2022.

This ease of movement forces Millennium BCP to offer more competitive mortgage and consumer loan terms or risk higher attrition—retail deposit churn rose to 6.8% in 2025.

High Price Sensitivity in Mortgage Lending

With Portugal's housing market driving 2025 growth, borrowers are highly price-sensitive: average mortgage spreads fell to 1.15 percentage points in Q4 2024, so clients shop aggressively for lower rates; large corporates and retail mortgage seekers treat basic loans as commodities, forcing Banco Comercial Português to match competitive offers; pricing transparency—comparison sites and ECB-refinancing rates—lets customers extract better fees and trims, compressing BCP's net interest margin (NIM) which was 1.7% in 2024.

Corporate Client Negotiation Leverage

Large enterprise and multinational clients generate roughly 45% of Banco Comercial Português’s (BCP) corporate revenue in 2024, but they wield strong negotiation leverage for bespoke credit facilities and pricing.

These clients often bank with multiple lenders, using competitive bids to lower transaction fees and secure larger credit lines; BCP reported a 6% margin compression in large-client segments in 2023–24.

Sophisticated treasury teams push for cash‑pooling, FX optimization, and tiered pricing, forcing BCP to offer tailored products or risk losing accounts that represent material fee income.

Rise of Digital Wealth Management Demand

The rise of international brokerages and robo platforms, which captured ~12% of European digital wealth flows in 2023, weakens branch-based pricing power; BCP must show measurable value—custom tax planning, portfolio stress tests, and family-office services—to justify fees.

- Robo fees 0.25%–0.50% AUM (Europe, 2024)

- Digital wealth captured ~12% of flows (2023)

- BCP must add tax, stress tests, family-office services

Consumer Advocacy and Regulatory Protection

Stronger consumer protection laws in Portugal and the EU—notably Portugal’s 2019 consumer credit reforms and the EU’s 2019 Payment Services Directive 2—limit hidden fees and force clearer disclosures, reducing Banco Comercial Português’s (BCP) room to change fees unilaterally.

These rules let customers dispute fees and terms; in 2024 Portugal’s Autoridade de Supervisão de Seguros e Fundos de Pensões and Banco de Portugal handled ~12,000 consumer complaints, signaling effective enforcement and reputational risk for BCP.

- EU PSD2 and consumer credit rules enforce transparency

- ~12,000 regulatory complaints in Portugal (2024)

- Limits BCP’s unilateral fee/term changes

- Increases legal and reputational costs for noncompliance

Customers wield power: high churn, tight spreads, and fee pressure squeeze margins

Customers have high bargaining power: 28% used account portability (2025), retail deposit churn 6.8% (2025), mortgage spreads tightened to 1.15–1.35pp (2024–25), NIM 1.7% (2024); large corporates = 45% corporate revenue (2024) and forced 6% margin compression (2023–24); robo fees 0.25–0.50% AUM; ~12,000 consumer complaints handled in Portugal (2024).

| Metric | Value |

|---|---|

| Account portability (2025) | 28% |

| Retail deposit churn (2025) | 6.8% |

| Mortgage spreads (2024–25) | 1.15–1.35 pp |

| NIM (2024) | 1.7% |

| Corp revenue from large clients (2024) | 45% |

| Margin compression (large clients, 2023–24) | 6% |

| Robo fees (Europe, 2024) | 0.25–0.50% AUM |

| Regulatory complaints (Portugal, 2024) | ~12,000 |

Same Document Delivered

Banco Comercial Portugues Porter's Five Forces Analysis

This preview shows the exact Banco Comercial Português Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full version you’ll get—fully formatted and ready for download and use the moment you buy.

No mockups or samples: you’re previewing the final, professional analysis file that will be available to you instantly after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Banco Comercial Português faces moderate competitive rivalry with strong regional banks and fintech challengers, while regulatory barriers and branch network scale limit new entrants; supplier power is low but digitization raises substitute threats. This snapshot highlights strategic pressures on margins and growth potential. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Banco Comercial Portugues’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Central Bank and Regulatory Liquidity

As of late 2025 the European Central Bank (ECB) supplies primary liquidity and sets key rates; its deposit facility rate at 3.25% and targeted longer‑term refinancing operations shape Millennium BCP’s cost of funds and margins.

Millennium BCP’s funding mix—EUR 22.4bn customer deposits and EUR 6.8bn market funding at 9M2025—makes it highly sensitive to ECB policy shifts that alter capital costs.

Regulatory liquidity rules (LCR 142% at 3Q2025) and capital buffers (CET1 12.1% YE2024) constrain balance‑sheet responses, limiting rapid funding reallocation.

Technology and Fintech Infrastructure Providers

Banco Comercial Português depends on specialized global vendors for core banking, cloud, and cybersecurity; in 2024 about 62% of Portuguese banks reported using third‑party cloud services, raising dependency risks.

High technical complexity and integration mean switching costs are large—estimates show migration can cost 5–15% of annual IT budgets—giving suppliers strong bargaining power.

Need for continuous innovation to match digital challengers (neobanks grew ~28% users in Portugal 2023–24) further strengthens vendors’ leverage.

Human Capital and Specialized Labor

Intense competition for data scientists, risk managers and digital-banking specialists in Portugal tightens supplier power; a 2024 Cedefop report showed STEM vacancy rates rose 18% year-on-year, and Glassdoor data indicates median tech salaries in Lisbon climbed 12% in 2024.

BCP faces a small talent pool, so recruitment firms and employees command higher pay and benefits; Korn Ferry estimated Portugal had a 22% shortage in advanced IT skills in 2024.

To stop IP and staff flowing to London and Amsterdam fintech hubs, BCP must boost retention: expect multi-year spend increases—BCP reported HR costs up 9% in 2023—on training, equity, and remote work to remain competitive.

Debt Capital Markets and Institutional Investors

BCP funds long-term needs via covered bonds and subordinated debt to institutional investors; in 2024 it issued covered bonds totaling €1.2bn and €500m of Tier 2 notes, tying pricing to its Ba2/BB credit outlook.

Investor bargaining power rises if BCPs credit rating falls or Eurozone stress increases; in Q3 2025 a 100bp widening in Portuguese bank spreads would raise annual interest costs by ~€12m on €1.2bn.

Shifts in sentiment quickly change availability and yields—during 2022-23 stress, issuance windows narrowed and spreads jumped 150–250bps, showing supplier leverage.

- 2024 covered bonds €1.2bn; Tier 2 €500m

- Credit rating (Ba2/BB) drives pricing

- 100bp spread rise ≈ €12m annual cost on €1.2bn

- 2022–23 stress widened spreads 150–250bps

Deposit Base Granularity

Retail depositors are the primary suppliers of capital for Banco Comercial Português (BCP), but power is low because deposits are highly fragmented across ~6.5 million Portuguese retail accounts as of Dec 2024; no single depositor can exert leverage.

Collective flows respond to Iberian rate spreads; BCP lost ~€1.2bn in deposits to competitors during Q1–Q3 2024 when its savings rates trailed peers by ~40 bps.

By 2025 digital savings platforms increased liquidity mobility; 28% of retail deposits moved at least once yearly in 2024, raising price sensitivity and raising the cost of retaining marginal deposits.

- Fragmented base (~6.5M accounts) → low individual supplier power

- Rate competitiveness drove €1.2bn outflows in early 2024

- 28% of deposits mobile in 2024 → higher price sensitivity in 2025

Suppliers wield high leverage—IT costs, talent gap and mobile deposits squeeze funding

Suppliers (tech vendors, skilled staff, wholesale investors) hold moderate‑high bargaining power: large switching costs (IT migration 5–15% of IT spend), tight talent market (22% advanced IT skill gap 2024), and €1.7bn market funding (2024) tie pricing to BCP’s Ba2/BB rating; retail deposits remain low power but mobile (28% moved 2024), raising marginal funding costs.

| Metric | Value |

|---|---|

| IT migration cost | 5–15% annual IT budget |

| IT skill gap (Portugal) | 22% (2024) |

| Market funding | €6.8bn (9M2025) |

| Deposit mobility | 28% (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Banco Comercial Português, uncovering competitive drivers, buyer/supplier power, entry barriers, substitutes, and disruptive threats to its market position, with strategic insights for investors and planners.

Clear, one-sheet Porter's Five Forces for Banco Comercial Português—perfect for quick strategic decisions and boardroom slides.

Customers Bargaining Power

Low Switching Costs in Retail Banking

PSD3-driven open banking cut retail switching friction; EU data from 2025 shows 28% of Portuguese customers used account portability services, boosting bargaining power for borrowers.

Real-time aggregators let consumers compare rates instantly; average advertised mortgage spreads at Millennium BCP tightened to 1.35% in 2025 vs 1.60% in 2022.

This ease of movement forces Millennium BCP to offer more competitive mortgage and consumer loan terms or risk higher attrition—retail deposit churn rose to 6.8% in 2025.

High Price Sensitivity in Mortgage Lending

With Portugal's housing market driving 2025 growth, borrowers are highly price-sensitive: average mortgage spreads fell to 1.15 percentage points in Q4 2024, so clients shop aggressively for lower rates; large corporates and retail mortgage seekers treat basic loans as commodities, forcing Banco Comercial Português to match competitive offers; pricing transparency—comparison sites and ECB-refinancing rates—lets customers extract better fees and trims, compressing BCP's net interest margin (NIM) which was 1.7% in 2024.

Corporate Client Negotiation Leverage

Large enterprise and multinational clients generate roughly 45% of Banco Comercial Português’s (BCP) corporate revenue in 2024, but they wield strong negotiation leverage for bespoke credit facilities and pricing.

These clients often bank with multiple lenders, using competitive bids to lower transaction fees and secure larger credit lines; BCP reported a 6% margin compression in large-client segments in 2023–24.

Sophisticated treasury teams push for cash‑pooling, FX optimization, and tiered pricing, forcing BCP to offer tailored products or risk losing accounts that represent material fee income.

Rise of Digital Wealth Management Demand

The rise of international brokerages and robo platforms, which captured ~12% of European digital wealth flows in 2023, weakens branch-based pricing power; BCP must show measurable value—custom tax planning, portfolio stress tests, and family-office services—to justify fees.

- Robo fees 0.25%–0.50% AUM (Europe, 2024)

- Digital wealth captured ~12% of flows (2023)

- BCP must add tax, stress tests, family-office services

Consumer Advocacy and Regulatory Protection

Stronger consumer protection laws in Portugal and the EU—notably Portugal’s 2019 consumer credit reforms and the EU’s 2019 Payment Services Directive 2—limit hidden fees and force clearer disclosures, reducing Banco Comercial Português’s (BCP) room to change fees unilaterally.

These rules let customers dispute fees and terms; in 2024 Portugal’s Autoridade de Supervisão de Seguros e Fundos de Pensões and Banco de Portugal handled ~12,000 consumer complaints, signaling effective enforcement and reputational risk for BCP.

- EU PSD2 and consumer credit rules enforce transparency

- ~12,000 regulatory complaints in Portugal (2024)

- Limits BCP’s unilateral fee/term changes

- Increases legal and reputational costs for noncompliance

Customers wield power: high churn, tight spreads, and fee pressure squeeze margins

Customers have high bargaining power: 28% used account portability (2025), retail deposit churn 6.8% (2025), mortgage spreads tightened to 1.15–1.35pp (2024–25), NIM 1.7% (2024); large corporates = 45% corporate revenue (2024) and forced 6% margin compression (2023–24); robo fees 0.25–0.50% AUM; ~12,000 consumer complaints handled in Portugal (2024).

| Metric | Value |

|---|---|

| Account portability (2025) | 28% |

| Retail deposit churn (2025) | 6.8% |

| Mortgage spreads (2024–25) | 1.15–1.35 pp |

| NIM (2024) | 1.7% |

| Corp revenue from large clients (2024) | 45% |

| Margin compression (large clients, 2023–24) | 6% |

| Robo fees (Europe, 2024) | 0.25–0.50% AUM |

| Regulatory complaints (Portugal, 2024) | ~12,000 |

Same Document Delivered

Banco Comercial Portugues Porter's Five Forces Analysis

This preview shows the exact Banco Comercial Português Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full version you’ll get—fully formatted and ready for download and use the moment you buy.

No mockups or samples: you’re previewing the final, professional analysis file that will be available to you instantly after payment.