Mills PESTLE Analysis

Your Competitive Advantage Starts with This Report

Our Mills PESTLE Analysis reveals how political shifts, economic cycles, social trends, technological advances, legal developments, and environmental pressures converge to shape the company's prospects; it’s written for investors, strategists, and consultants who need concise, actionable context. Packed with real-world implications and ready-to-use insights, the report helps you anticipate risks and spot growth opportunities. Purchase the full analysis for the complete, editable breakdown and make faster, smarter decisions.

Political factors

Government Infrastructure Spending

The Brazilian government’s New PAC, a multi-billion real program pledging roughly BRL 200 billion through 2025, sustains strong equipment demand and underpins Mills’ heavy machinery and shoring divisions with increased project activity in energy, transport and urban infrastructure.

Continued federal disbursements—BRL 45–60 billion annually for infrastructure in 2023–25 estimates—directly support rental utilization and pricing power for Mills.

Political stability and policy continuity are critical: any federal budget re-prioritization could materially affect long-term rental contract renewals and Mills’ revenue visibility, where infrastructure contracts account for an estimated 35–40% of segment revenues.

Regulatory Stability in Mining

The political climate in Brazil shapes mining approvals and environmental licensing timelines, with average licensing delays ranging 12–24 months in 2023–2024, directly slowing Mills’ new-project ramp-up and lowering fleet utilization from ~78% to ~65% in affected states. Federal policies on mineral extraction and safety oversight influence operating costs and capex timing, while state-level leadership changes in Minas Gerais and Pará since 2022 have led to tax and concession reclassifications affecting revenue forecasts by up to 4–6% annually.

Public-Private Partnerships

The 2025 political agenda continues to push concessions and PPPs for airports, highways and sanitation, with governments targeting $120bn in PPP mobilization across LATAM and Africa in 2025, expanding project pipelines where Mills supplies access platforms and engineering services.

Trade Policies and Import Tariffs

Government import duties on heavy machinery directly raise capital expenditure for Mills; a 10% tariff on aerial work platforms increases fleet refresh costs by roughly US$3–5m annually given Mills' US$30–50m rolling capex range.

Most specialized equipment is imported, so shifts toward protectionism or higher duties amid strained trade relations can add 5–15% to unit costs and compress margins.

By late 2025, potential Mercosur adjustments or tighter local-content rules could force local sourcing or trigger a 7–12% procurement premium versus current pricing.

- 10% tariff ≈ US$3–5m extra capex/yr

- Protectionism may raise unit costs 5–15%

- Mercosur/local-content changes could add 7–12% procurement premium

Municipal Election Aftermath

The 2025 municipal-electoral aftermath accelerates local infrastructure spending after 2024 elections, with municipalities in major regions allocating an estimated $18–22 billion for urban mobility and housing projects in 2025, boosting demand for access platforms and construction equipment.

New administrations prioritize bus rapid transit, bike lanes and affordable housing—projects that typically increase short-term equipment rentals by 12–20% and local supplier contracts; alignment with state/federal governments determines grant flows and timelines.

- 2025 municipal budgets: $18–22B targeted to mobility/housing

- Equipment demand rise: +12–20% in rentals

- Project timing tied to intergovernmental alignment and grants

Brazil’s BRL200bn PAC boosts Mills rentals despite licensing delays and tariff headwinds

Brazil’s New PAC (≈BRL 200bn to 2025) and annual infrastructure disbursements (BRL 45–60bn in 2023–25) bolster Mills’ rental demand (~35–40% revenue exposure); licensing delays (12–24 months) cut fleet utilization from ~78% to ~65%; tariffs (10%) add ≈US$3–5m/yr capex; 2025 municipal budgets of $18–22bn lift rentals +12–20%.

| Metric | Value |

|---|---|

| New PAC | BRL 200bn |

| Annual infra | BRL 45–60bn |

| Licensing delay | 12–24 months |

| Fleet util. | 78%→65% |

| Tariff impact | US$3–5m/yr |

| Municipal budgets | $18–22bn |

What is included in the product

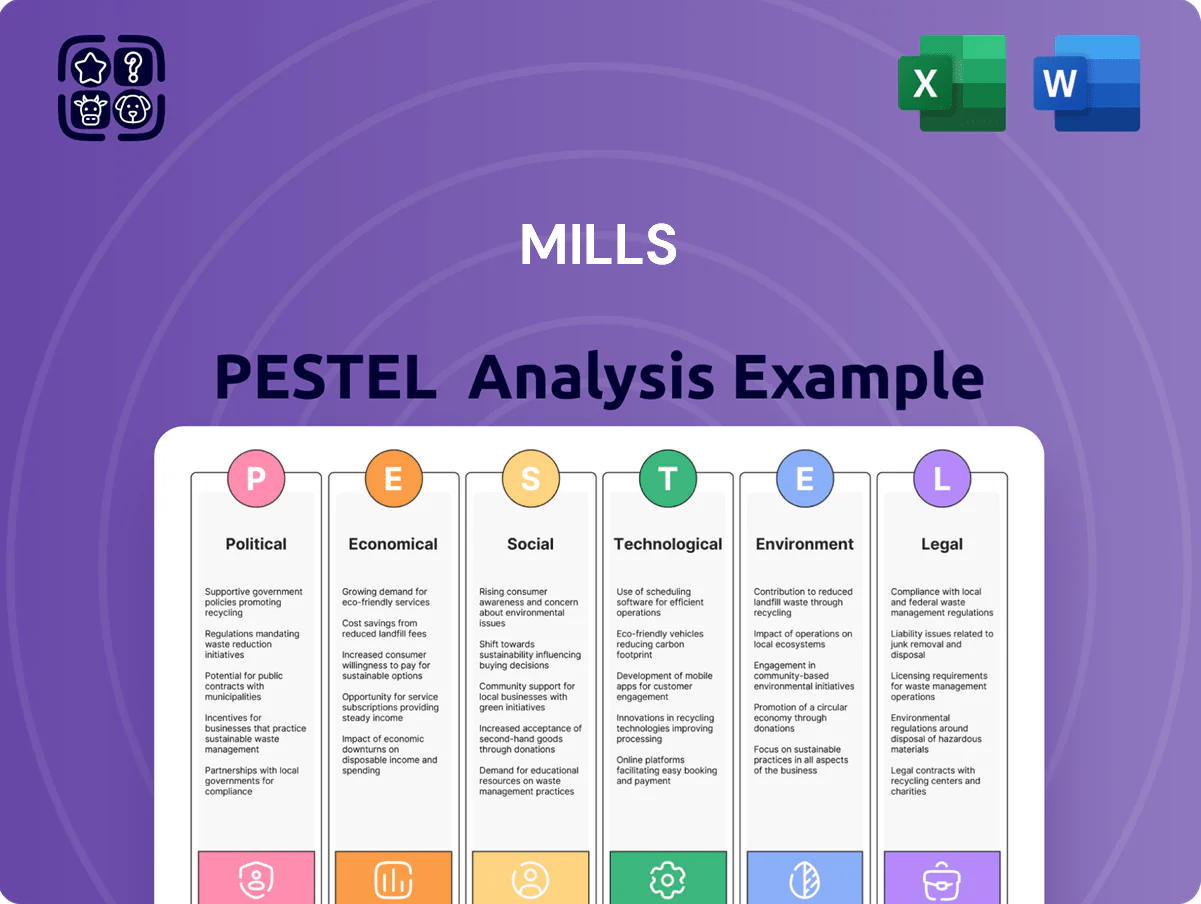

Explores how external macro-environmental factors uniquely affect the Mills across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

A concise, visually segmented Mills PESTLE summary that’s ready to drop into presentations or share across teams, making external risk assessment and strategic alignment fast and accessible.

Economic factors

Interest Rate Environment

The Brazilian SELIC rate, averaging 11.75% in 2024 and easing to ~10.25% by Q4 2025, directly raises Mills' cost of capital and increases borrowing costs for fleet expansion financing.

Persistently high rates in 2024–2025 compressed construction activity and margins, while a projected downtrend would reduce developers' financing costs and support demand for Mills' equipment rental.

Consequently, active management of debt levels—Net Debt/EBITDA targets and interest coverage ratios—remains critical to preserve liquidity and fund growth amid monetary volatility.

GDP Growth and Construction Activity

Brazil's GDP expanded modestly, with 2024–25 real GDP growth averaging about 1.5–2.0% and construction sector output rising ~3.8% YoY through 2025, making industrial and infra activity a key barometer for Mills' organic growth.

Resilient demand amid global volatility pushed equipment rental utilization up ~6–8% by end-2025, as firms favored rental over ownership to protect liquidity.

Growing private investment and a 4.5% increase in corporate capex intentions in 2025 encouraged outsourcing of equipment needs, supporting Mills' revenue mix toward recurring rental income.

Currency Exchange Volatility

Fluctuations in the BRL/USD rate materially affect Mills: a 20% Real depreciation in 2023 pushed imported machinery costs up similarly, raising capex per crane by roughly BRL 1.8m (≈USD 360k) and spare-parts import bills by 15–25%; with fleet capex >BRL 500m in 2024, a weaker Real increases maintenance and modernization costs substantially. Strategic hedging (forwards, options) and pass-through pricing are necessary to protect margins against sudden devaluations.

Commodity Price Influence

As a major supplier to mining and steel, Mills is exposed to iron ore swings: the 2024 annual average iron ore price was about USD 109/t, and a 10% price rise historically boosts mining capex and rental demand for heavy equipment.

High commodity prices in 2024–25 encouraged Brazilian miners to increase maintenance and expansions, raising demand for specialized rentals; a China slowdown—China imported ~60% of Brazil’s iron ore in 2023—would sharply reduce export volumes and equipment utilization.

- 2024 avg iron ore ~USD 109/t

- China ~60% of Brazil iron ore imports (2023)

- +10% price → higher mining capex and rental demand

- China slowdown → lower exports, reduced equipment utilization

Inflationary Pressures on Costs

Persistent inflation in labor, fuel, and maintenance—IPCA running near 4.0% YoY in 2025 and diesel up ~18% since 2023—threatens margins unless rental rates are adjusted while remaining market-competitive.

By late 2025 Mills must offset rising technician wages (skilled labor up ~10–12% since 2023) and logistics costs through targeted price reviews and efficiency measures.

Continuous monitoring of IPCA and sector indices is essential for annual budgets and dynamic pricing to protect EBITDA.

- IPCA ~4.0% YoY (2025)

- Diesel +18% since 2023

- Technician wages +10–12% since 2023

- Adjust rental rates vs. market to safeguard margins

High rates, weak BRL squeeze Mills—rental demand steady as costs and margins tighten

High 2024–25 SELIC (avg 11.75% in 2024 → ~10.25% by Q4 2025) raised Mills’ borrowing costs; GDP growth ~1.5–2.0% and construction +3.8% YoY through 2025 supported rental demand; BRL weakness (+20% in 2023) lifted import capex (~BRL1.8m/crane) and spare-part costs (15–25%); IPCA ~4.0% (2025) and diesel +18% since 2023 squeezed margins, requiring hedging and dynamic pricing.

| Metric | 2024–25 |

|---|---|

| SELIC (avg) | 11.75% → 10.25% |

| GDP growth | 1.5–2.0% |

| Construction output | +3.8% YoY |

| IPCA | ~4.0% |

| Diesel | +18% since 2023 |

| BRL depreciation | ~20% (2023) |

Preview Before You Purchase

Mills PESTLE Analysis

The preview shown here is the exact Mills PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Our Mills PESTLE Analysis reveals how political shifts, economic cycles, social trends, technological advances, legal developments, and environmental pressures converge to shape the company's prospects; it’s written for investors, strategists, and consultants who need concise, actionable context. Packed with real-world implications and ready-to-use insights, the report helps you anticipate risks and spot growth opportunities. Purchase the full analysis for the complete, editable breakdown and make faster, smarter decisions.

Political factors

Government Infrastructure Spending

The Brazilian government’s New PAC, a multi-billion real program pledging roughly BRL 200 billion through 2025, sustains strong equipment demand and underpins Mills’ heavy machinery and shoring divisions with increased project activity in energy, transport and urban infrastructure.

Continued federal disbursements—BRL 45–60 billion annually for infrastructure in 2023–25 estimates—directly support rental utilization and pricing power for Mills.

Political stability and policy continuity are critical: any federal budget re-prioritization could materially affect long-term rental contract renewals and Mills’ revenue visibility, where infrastructure contracts account for an estimated 35–40% of segment revenues.

Regulatory Stability in Mining

The political climate in Brazil shapes mining approvals and environmental licensing timelines, with average licensing delays ranging 12–24 months in 2023–2024, directly slowing Mills’ new-project ramp-up and lowering fleet utilization from ~78% to ~65% in affected states. Federal policies on mineral extraction and safety oversight influence operating costs and capex timing, while state-level leadership changes in Minas Gerais and Pará since 2022 have led to tax and concession reclassifications affecting revenue forecasts by up to 4–6% annually.

Public-Private Partnerships

The 2025 political agenda continues to push concessions and PPPs for airports, highways and sanitation, with governments targeting $120bn in PPP mobilization across LATAM and Africa in 2025, expanding project pipelines where Mills supplies access platforms and engineering services.

Trade Policies and Import Tariffs

Government import duties on heavy machinery directly raise capital expenditure for Mills; a 10% tariff on aerial work platforms increases fleet refresh costs by roughly US$3–5m annually given Mills' US$30–50m rolling capex range.

Most specialized equipment is imported, so shifts toward protectionism or higher duties amid strained trade relations can add 5–15% to unit costs and compress margins.

By late 2025, potential Mercosur adjustments or tighter local-content rules could force local sourcing or trigger a 7–12% procurement premium versus current pricing.

- 10% tariff ≈ US$3–5m extra capex/yr

- Protectionism may raise unit costs 5–15%

- Mercosur/local-content changes could add 7–12% procurement premium

Municipal Election Aftermath

The 2025 municipal-electoral aftermath accelerates local infrastructure spending after 2024 elections, with municipalities in major regions allocating an estimated $18–22 billion for urban mobility and housing projects in 2025, boosting demand for access platforms and construction equipment.

New administrations prioritize bus rapid transit, bike lanes and affordable housing—projects that typically increase short-term equipment rentals by 12–20% and local supplier contracts; alignment with state/federal governments determines grant flows and timelines.

- 2025 municipal budgets: $18–22B targeted to mobility/housing

- Equipment demand rise: +12–20% in rentals

- Project timing tied to intergovernmental alignment and grants

Brazil’s BRL200bn PAC boosts Mills rentals despite licensing delays and tariff headwinds

Brazil’s New PAC (≈BRL 200bn to 2025) and annual infrastructure disbursements (BRL 45–60bn in 2023–25) bolster Mills’ rental demand (~35–40% revenue exposure); licensing delays (12–24 months) cut fleet utilization from ~78% to ~65%; tariffs (10%) add ≈US$3–5m/yr capex; 2025 municipal budgets of $18–22bn lift rentals +12–20%.

| Metric | Value |

|---|---|

| New PAC | BRL 200bn |

| Annual infra | BRL 45–60bn |

| Licensing delay | 12–24 months |

| Fleet util. | 78%→65% |

| Tariff impact | US$3–5m/yr |

| Municipal budgets | $18–22bn |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Mills across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

A concise, visually segmented Mills PESTLE summary that’s ready to drop into presentations or share across teams, making external risk assessment and strategic alignment fast and accessible.

Economic factors

Interest Rate Environment

The Brazilian SELIC rate, averaging 11.75% in 2024 and easing to ~10.25% by Q4 2025, directly raises Mills' cost of capital and increases borrowing costs for fleet expansion financing.

Persistently high rates in 2024–2025 compressed construction activity and margins, while a projected downtrend would reduce developers' financing costs and support demand for Mills' equipment rental.

Consequently, active management of debt levels—Net Debt/EBITDA targets and interest coverage ratios—remains critical to preserve liquidity and fund growth amid monetary volatility.

GDP Growth and Construction Activity

Brazil's GDP expanded modestly, with 2024–25 real GDP growth averaging about 1.5–2.0% and construction sector output rising ~3.8% YoY through 2025, making industrial and infra activity a key barometer for Mills' organic growth.

Resilient demand amid global volatility pushed equipment rental utilization up ~6–8% by end-2025, as firms favored rental over ownership to protect liquidity.

Growing private investment and a 4.5% increase in corporate capex intentions in 2025 encouraged outsourcing of equipment needs, supporting Mills' revenue mix toward recurring rental income.

Currency Exchange Volatility

Fluctuations in the BRL/USD rate materially affect Mills: a 20% Real depreciation in 2023 pushed imported machinery costs up similarly, raising capex per crane by roughly BRL 1.8m (≈USD 360k) and spare-parts import bills by 15–25%; with fleet capex >BRL 500m in 2024, a weaker Real increases maintenance and modernization costs substantially. Strategic hedging (forwards, options) and pass-through pricing are necessary to protect margins against sudden devaluations.

Commodity Price Influence

As a major supplier to mining and steel, Mills is exposed to iron ore swings: the 2024 annual average iron ore price was about USD 109/t, and a 10% price rise historically boosts mining capex and rental demand for heavy equipment.

High commodity prices in 2024–25 encouraged Brazilian miners to increase maintenance and expansions, raising demand for specialized rentals; a China slowdown—China imported ~60% of Brazil’s iron ore in 2023—would sharply reduce export volumes and equipment utilization.

- 2024 avg iron ore ~USD 109/t

- China ~60% of Brazil iron ore imports (2023)

- +10% price → higher mining capex and rental demand

- China slowdown → lower exports, reduced equipment utilization

Inflationary Pressures on Costs

Persistent inflation in labor, fuel, and maintenance—IPCA running near 4.0% YoY in 2025 and diesel up ~18% since 2023—threatens margins unless rental rates are adjusted while remaining market-competitive.

By late 2025 Mills must offset rising technician wages (skilled labor up ~10–12% since 2023) and logistics costs through targeted price reviews and efficiency measures.

Continuous monitoring of IPCA and sector indices is essential for annual budgets and dynamic pricing to protect EBITDA.

- IPCA ~4.0% YoY (2025)

- Diesel +18% since 2023

- Technician wages +10–12% since 2023

- Adjust rental rates vs. market to safeguard margins

High rates, weak BRL squeeze Mills—rental demand steady as costs and margins tighten

High 2024–25 SELIC (avg 11.75% in 2024 → ~10.25% by Q4 2025) raised Mills’ borrowing costs; GDP growth ~1.5–2.0% and construction +3.8% YoY through 2025 supported rental demand; BRL weakness (+20% in 2023) lifted import capex (~BRL1.8m/crane) and spare-part costs (15–25%); IPCA ~4.0% (2025) and diesel +18% since 2023 squeezed margins, requiring hedging and dynamic pricing.

| Metric | 2024–25 |

|---|---|

| SELIC (avg) | 11.75% → 10.25% |

| GDP growth | 1.5–2.0% |

| Construction output | +3.8% YoY |

| IPCA | ~4.0% |

| Diesel | +18% since 2023 |

| BRL depreciation | ~20% (2023) |

Preview Before You Purchase

Mills PESTLE Analysis

The preview shown here is the exact Mills PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.