Mincon Porter's Five Forces Analysis

Don't Miss the Bigger Picture

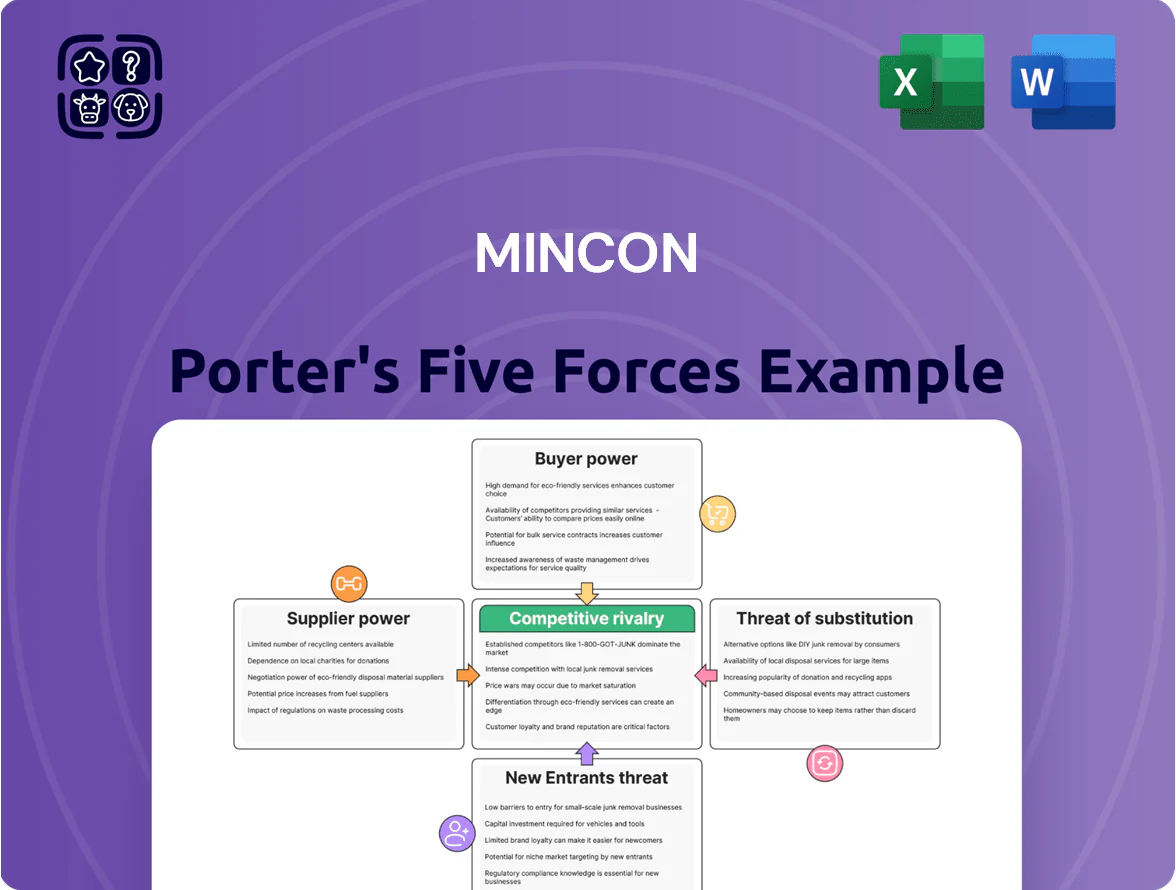

Mincon faces a mixed competitive landscape: supplier concentration and specialized tooling raise costs, while niche differentiation and service depth strengthen customer loyalty and reduce substitution risk.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Mincon’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Volatility

High-grade steel and tungsten carbide are core inputs for Mincon drilling tools, and suppliers have moderate bargaining power because metallurgical precision and ISO 9001:2015 standards limit substitutes. Global steel and tungsten prices rose 14% and 22% in 2024 respectively, pushing Mincon’s COGS sensitivity—a 10% tungsten jump raises tool unit cost ~3.5% (here’s the quick math: tungsten ~35% of consumable cost).

Energy and Utility Costs

Energy-intensive drilling-equipment manufacture makes Mincon exposed to regional electricity price shocks; EU industrial power prices rose 34% in 2022-2023 and averaged €150/MWh in parts of 2024, squeezing margins.

Local utility providers often act as oligopolies, limiting Mincon’s bargaining power and forcing pass-through or margin pressure on inputs.

Investing in energy efficiency and on-site generation (solar + batteries) can cut energy spend by 15–30% and reduce supplier risk.

Specialized Component Dependencies

Mincon depends on niche high-tech hydraulic and pneumatic components, where roughly 70% of parts come from fewer than five global suppliers able to meet ISO 9001 and NORSOK standards for extreme drilling; this supplier concentration lets vendors hold steady pricing, contributing to supplier-side margin pressure of about 120–150 basis points on manufacturing costs in 2024.

Logistics and Shipping Partners

Mincon relies on international freight to serve remote mines, and consolidation among shipping conglomerates (top 5 carriers control ~80% of container capacity by 2024) raises supplier bargaining power, letting carriers push higher rates and tighter schedules.

Supply-chain disruptions through late 2025—Suez/Red Sea route tensions and 2023–25 port congestion—kept spot rates ~2–3x pre‑pandemic levels, further empowering logistics partners and increasing Mincon’s freight cost volatility.

- Top 5 carriers ≈80% capacity (2024)

- Spot rates 2–3x pre‑pandemic (2023–25)

- Route disruptions: Suez/Red Sea tensions (2023–25)

- High bargaining power → higher costs, schedule risk

Labor Market Constraints

Skilled engineers and precision machinists remain scarce: OECD data shows manufacturing tech vacancies rose 18% in 2024, pushing wage premia for specialist machinists up 9% year-over-year, giving labor suppliers clear leverage in Mincon’s hubs.

Specialized labor functions as human-capital suppliers with bargaining power, raising hiring costs and project margins; Mincon must invest in retention and training—typical upskilling programs cost 3–5% of payroll annually.

Supplier squeeze lifts input costs, freight and energy surge; capex cuts risk 15–30%

Suppliers wield moderate-to-high power: concentrated tungsten/steel vendors, 5 key hydraulic suppliers, and top-5 carriers (~80% capacity in 2024) pushed input cost pressure ~120–150 bps and freight spot rates 2–3x pre‑pandemic; energy and skilled-labor cost rises (EU power ~€150/MWh parts of 2024; machining wage premium +9% YoY) add volatility—capex in energy/vertical integration can cut risk ~15–30%.

| Item | 2024–25 Metric |

|---|---|

| Tungsten price change | +22% (2024) |

| Steel price change | +14% (2024) |

| Freight capacity concentration | Top‑5 carriers ≈80% (2024) |

| Freight spot rate vs pre‑pandemic | 2–3x (2023–25) |

| Energy price example | €150/MWh (parts of EU, 2024) |

| Labor vacancy / wage | Vacancies +18%, wage premium +9% (2024) |

| Supplier‑driven margin hit | 120–150 bps (2024) |

What is included in the product

Customized Porter's Five Forces analysis for Mincon that uncovers competitive drivers, supplier and buyer power, entry barriers, substitute threats, and strategic vulnerabilities—delivered with industry context and actionable insights.

A concise Porter's Five Forces one-sheet for Mincon—quickly spot supplier, buyer, and competitive pressures to guide strategic moves.

Customers Bargaining Power

Large-Scale Mining Consolidation

Major miners like BHP Group, Rio Tinto, and Vale accounted for over 35% of global mining capex in 2024, concentrating demand for high-performance drilling tools and raising buyer power.

These firms secure volume discounts of 10–25% and extended 60–120 day payment terms through scale-driven procurement contracts, squeezing supplier margins.

High supplier substitutability and fleet-level tenders enable easy switching, pressuring prices and driving suppliers to compete on total cost of ownership and service.

Price Sensitivity in Construction

Customers in construction and water well sectors typically have margins 3–7 percentage points lower than mining, so price sensitivity is high; a 2024 USGS/IBISWorld review showed average contractor gross margins of ~12% vs mining at ~19%. Mincon must prove lower total cost of ownership—longer bit life, 20–40% lower downtime, and lower maintenance—to justify any premium up to 15% over commodity drills.

Availability of Technical Information

Modern buyers access detailed performance datasets and peer reviews showing drill bit life and penetration rates; 2024 trade tests report Epiroc and Sandvik achieving 10–18% longer bit life in some rock types, so customers benchmark Mincon (market cap ~€270m in 2025) against those metrics.

This transparency raises buyer bargaining power: procurement teams demand equal or better life-per-hour and lower total cost-per-meter, and 36% of mining OEM contracts in 2024 included performance SLAs tied to measured efficiency.

Low Switching Costs for Consumables

Low switching costs for consumables mean customers can buy drill bits and parts from third parties; in 2024 aftermarket drill-bit sales grew ~6% globally, pressuring OEM margins.

Clients can trial alternative consumables without replacing hammers or rigs, so Mincon must keep consumable quality high and prices competitive to protect recurring revenue (consumables often >30% of service revenue).

- Aftermarket growth ~6% (2024)

- Consumables >30% of service revenue

- Third-party parts readily trialable

- Requires tight quality + pricing

Demand for Integrated Solutions

Clients now demand integrated packages—maintenance, remote monitoring, and uptime guarantees—pushing Mincon into service-led sales; in 2024 global aftermarket mining services grew ~7.8% to $42.3B, so buyers expect bundled contracts and SLAs.

This preference raises customer bargaining power: procurement teams insist on lifecycle pricing, KPI-linked payments, and retrofit options, reducing pure-equipment margins and shifting revenue to recurring services.

- Buyers want maintenance + monitoring

- 2024 aftermarket mining services ≈ $42.3B (+7.8%)

- Shift lowers product margins, boosts recurring revenue

- Customers demand SLAs, performance-based pay

Top miners seize capex power—service growth forces Mincon to prove 20–40% downtime edge

Large miners (BHP, Rio Tinto, Vale) drove >35% of 2024 mining capex, securing 10–25% discounts and 60–120 day terms, raising buyer power; aftermarket sales grew ~6% (2024) and services to $42.3B (+7.8%), shifting buyers to demand SLAs and lifecycle pricing, forcing Mincon to compete on 20–40% lower downtime and TCO to justify ≤15% premium.

| Metric | 2024/2025 |

|---|---|

| Top miners share of capex | >35% |

| Procurement discounts | 10–25% |

| Payment terms | 60–120 days |

| Aftermarket growth | ~6% |

| Aftermarket services | $42.3B (+7.8%) |

| Required performance edge | 20–40% lower downtime |

| Acceptable premium | ≤15% |

Preview Before You Purchase

Mincon Porter's Five Forces Analysis

This preview shows the exact Mincon Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders, no abridgments.

The document displayed here is the same professionally written, fully formatted file you'll be able to download the moment you complete payment.

No mockups or samples: this is the final, ready-to-use analysis, delivered instantly with your purchase.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Mincon faces a mixed competitive landscape: supplier concentration and specialized tooling raise costs, while niche differentiation and service depth strengthen customer loyalty and reduce substitution risk.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Mincon’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Volatility

High-grade steel and tungsten carbide are core inputs for Mincon drilling tools, and suppliers have moderate bargaining power because metallurgical precision and ISO 9001:2015 standards limit substitutes. Global steel and tungsten prices rose 14% and 22% in 2024 respectively, pushing Mincon’s COGS sensitivity—a 10% tungsten jump raises tool unit cost ~3.5% (here’s the quick math: tungsten ~35% of consumable cost).

Energy and Utility Costs

Energy-intensive drilling-equipment manufacture makes Mincon exposed to regional electricity price shocks; EU industrial power prices rose 34% in 2022-2023 and averaged €150/MWh in parts of 2024, squeezing margins.

Local utility providers often act as oligopolies, limiting Mincon’s bargaining power and forcing pass-through or margin pressure on inputs.

Investing in energy efficiency and on-site generation (solar + batteries) can cut energy spend by 15–30% and reduce supplier risk.

Specialized Component Dependencies

Mincon depends on niche high-tech hydraulic and pneumatic components, where roughly 70% of parts come from fewer than five global suppliers able to meet ISO 9001 and NORSOK standards for extreme drilling; this supplier concentration lets vendors hold steady pricing, contributing to supplier-side margin pressure of about 120–150 basis points on manufacturing costs in 2024.

Logistics and Shipping Partners

Mincon relies on international freight to serve remote mines, and consolidation among shipping conglomerates (top 5 carriers control ~80% of container capacity by 2024) raises supplier bargaining power, letting carriers push higher rates and tighter schedules.

Supply-chain disruptions through late 2025—Suez/Red Sea route tensions and 2023–25 port congestion—kept spot rates ~2–3x pre‑pandemic levels, further empowering logistics partners and increasing Mincon’s freight cost volatility.

- Top 5 carriers ≈80% capacity (2024)

- Spot rates 2–3x pre‑pandemic (2023–25)

- Route disruptions: Suez/Red Sea tensions (2023–25)

- High bargaining power → higher costs, schedule risk

Labor Market Constraints

Skilled engineers and precision machinists remain scarce: OECD data shows manufacturing tech vacancies rose 18% in 2024, pushing wage premia for specialist machinists up 9% year-over-year, giving labor suppliers clear leverage in Mincon’s hubs.

Specialized labor functions as human-capital suppliers with bargaining power, raising hiring costs and project margins; Mincon must invest in retention and training—typical upskilling programs cost 3–5% of payroll annually.

Supplier squeeze lifts input costs, freight and energy surge; capex cuts risk 15–30%

Suppliers wield moderate-to-high power: concentrated tungsten/steel vendors, 5 key hydraulic suppliers, and top-5 carriers (~80% capacity in 2024) pushed input cost pressure ~120–150 bps and freight spot rates 2–3x pre‑pandemic; energy and skilled-labor cost rises (EU power ~€150/MWh parts of 2024; machining wage premium +9% YoY) add volatility—capex in energy/vertical integration can cut risk ~15–30%.

| Item | 2024–25 Metric |

|---|---|

| Tungsten price change | +22% (2024) |

| Steel price change | +14% (2024) |

| Freight capacity concentration | Top‑5 carriers ≈80% (2024) |

| Freight spot rate vs pre‑pandemic | 2–3x (2023–25) |

| Energy price example | €150/MWh (parts of EU, 2024) |

| Labor vacancy / wage | Vacancies +18%, wage premium +9% (2024) |

| Supplier‑driven margin hit | 120–150 bps (2024) |

What is included in the product

Customized Porter's Five Forces analysis for Mincon that uncovers competitive drivers, supplier and buyer power, entry barriers, substitute threats, and strategic vulnerabilities—delivered with industry context and actionable insights.

A concise Porter's Five Forces one-sheet for Mincon—quickly spot supplier, buyer, and competitive pressures to guide strategic moves.

Customers Bargaining Power

Large-Scale Mining Consolidation

Major miners like BHP Group, Rio Tinto, and Vale accounted for over 35% of global mining capex in 2024, concentrating demand for high-performance drilling tools and raising buyer power.

These firms secure volume discounts of 10–25% and extended 60–120 day payment terms through scale-driven procurement contracts, squeezing supplier margins.

High supplier substitutability and fleet-level tenders enable easy switching, pressuring prices and driving suppliers to compete on total cost of ownership and service.

Price Sensitivity in Construction

Customers in construction and water well sectors typically have margins 3–7 percentage points lower than mining, so price sensitivity is high; a 2024 USGS/IBISWorld review showed average contractor gross margins of ~12% vs mining at ~19%. Mincon must prove lower total cost of ownership—longer bit life, 20–40% lower downtime, and lower maintenance—to justify any premium up to 15% over commodity drills.

Availability of Technical Information

Modern buyers access detailed performance datasets and peer reviews showing drill bit life and penetration rates; 2024 trade tests report Epiroc and Sandvik achieving 10–18% longer bit life in some rock types, so customers benchmark Mincon (market cap ~€270m in 2025) against those metrics.

This transparency raises buyer bargaining power: procurement teams demand equal or better life-per-hour and lower total cost-per-meter, and 36% of mining OEM contracts in 2024 included performance SLAs tied to measured efficiency.

Low Switching Costs for Consumables

Low switching costs for consumables mean customers can buy drill bits and parts from third parties; in 2024 aftermarket drill-bit sales grew ~6% globally, pressuring OEM margins.

Clients can trial alternative consumables without replacing hammers or rigs, so Mincon must keep consumable quality high and prices competitive to protect recurring revenue (consumables often >30% of service revenue).

- Aftermarket growth ~6% (2024)

- Consumables >30% of service revenue

- Third-party parts readily trialable

- Requires tight quality + pricing

Demand for Integrated Solutions

Clients now demand integrated packages—maintenance, remote monitoring, and uptime guarantees—pushing Mincon into service-led sales; in 2024 global aftermarket mining services grew ~7.8% to $42.3B, so buyers expect bundled contracts and SLAs.

This preference raises customer bargaining power: procurement teams insist on lifecycle pricing, KPI-linked payments, and retrofit options, reducing pure-equipment margins and shifting revenue to recurring services.

- Buyers want maintenance + monitoring

- 2024 aftermarket mining services ≈ $42.3B (+7.8%)

- Shift lowers product margins, boosts recurring revenue

- Customers demand SLAs, performance-based pay

Top miners seize capex power—service growth forces Mincon to prove 20–40% downtime edge

Large miners (BHP, Rio Tinto, Vale) drove >35% of 2024 mining capex, securing 10–25% discounts and 60–120 day terms, raising buyer power; aftermarket sales grew ~6% (2024) and services to $42.3B (+7.8%), shifting buyers to demand SLAs and lifecycle pricing, forcing Mincon to compete on 20–40% lower downtime and TCO to justify ≤15% premium.

| Metric | 2024/2025 |

|---|---|

| Top miners share of capex | >35% |

| Procurement discounts | 10–25% |

| Payment terms | 60–120 days |

| Aftermarket growth | ~6% |

| Aftermarket services | $42.3B (+7.8%) |

| Required performance edge | 20–40% lower downtime |

| Acceptable premium | ≤15% |

Preview Before You Purchase

Mincon Porter's Five Forces Analysis

This preview shows the exact Mincon Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders, no abridgments.

The document displayed here is the same professionally written, fully formatted file you'll be able to download the moment you complete payment.

No mockups or samples: this is the final, ready-to-use analysis, delivered instantly with your purchase.