Mineral Resources PESTLE Analysis

Your Shortcut to Market Insight Starts Here

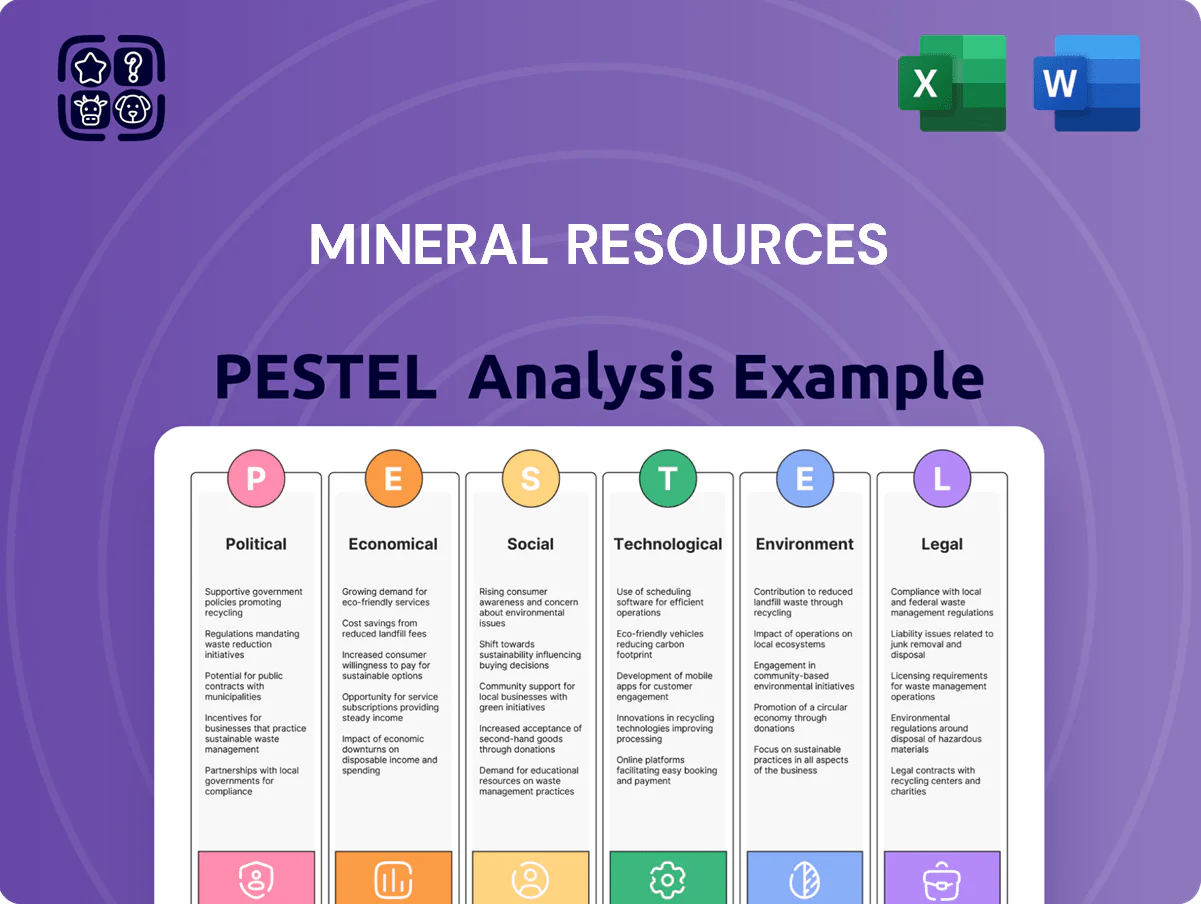

Gain a competitive edge with our PESTLE Analysis of Mineral Resources—concise, action-focused and tailored for investors and strategists; uncover how political, economic, social, technological, legal and environmental forces shape the company’s outlook. Buy the full report to access deep-dive insights, ready-to-use slides and data you can apply immediately to investment cases or strategic planning.

Political factors

Australian Critical Minerals Policy

The Australian Critical Minerals Policy aims to make Australia a top-three global supplier of battery minerals by 2025, with A$2.5 billion in pledged funding and tax incentives; Mineral Resources Limited has secured federal grants and access to fast-track approvals, cutting project lead times by months and reducing reliance on Asian processing hubs. These measures prioritize domestic lithium and rare earth supply chains to support forecasted battery demand growth of ~30% CAGR through 2025.

Geopolitical Trade Relations

Ongoing trade tensions and diplomatic shifts between Australia and major Asian markets—notably China, which bought ~65% of Australia’s iron ore exports in 2023—affect Mineral Resources Limited’s iron ore and lithium export landscape; 2024 tariffs/quota risks rose after several bilateral disputes cut shipments by up to 10% in targeted sectors. Navigating fluctuating tariffs and export quotas tied to alliances and regional security pacts is critical, and maintaining a diversified buyer portfolio reduces single-country reliance risk—Mineral Resources reported ~30% of sales outside China in FY2024.

State Government Royalty Structures

The Western Australian government reviews royalty rates regularly, having raised the iron ore royalty in 2023-24 by 0.25 percentage points, and signals potential adjustments tied to commodity price cycles to meet a A$7.5bn revenue target in 2024–25; such changes can cut project NPV by 5–15% and alter IRR thresholds, directly affecting Mineral Resources Limited’s capital allocation and mine development timing as it lobbies for rates comparable to WA peers and global jurisdictions.

Foreign Investment Review Board Oversight

Stricter FIRB scrutiny of foreign ownership in strategic resource assets limits how Mineral Resources Limited structures joint ventures, increasing approval timelines; FIRB reviewed 2,600 foreign investment applications and blocked or modified 12 significant resource deals in 2024–25.

This regulatory stance protects national interests while allowing capital for large-scale projects; approvals are critical for MRL to secure funding for its A$2.1bn planned energy and lithium investments.

- FIRB reviews increase deal timelines and conditions

- 2,600 applications reviewed; 12 major resource deals altered in 2024–25

- MRL requires approvals for A$2.1bn energy/lithium projects

- Successful navigation is essential for foreign partnerships

Energy Security and Domestic Gas Policy

- WA domestic gas reservation ~35–40% (2025)

- Estimated AU$15–25/tonne energy cost saving for mining (2024–25)

- Limits on export volumes reduce revenue but improve operational stability

Policy boosts cut lead times but China reliance, royalties and FIRB pose major risks

Political support (A$2.5bn) and fast-track approvals cut project lead times; trade tensions with China (65% of iron ore exports in 2023) raise tariff/quota risks; WA royalty hike +0.25ppt reduced project NPV 5–15%; FIRB reviewed 2,600 apps and altered 12 deals (2024–25); WA gas reservation 35–40% (2025) saves AU$15–25/tonne energy.

| Metric | Value |

|---|---|

| Federal funding | A$2.5bn |

| China share iron ore (2023) | 65% |

| FIRB reviews (2024–25) | 2,600 / 12 altered |

| WA gas reservation (2025) | 35–40% |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact Mineral Resources, with data-backed trends and region-focused insights to identify threats and opportunities.

Provides a clean, PESTLE-segmented summary of mineral resources risks and opportunities, easily dropped into presentations or shared across teams for fast alignment and decision-making.

Economic factors

Commodity Price Volatility

Global iron ore and lithium prices remained cyclical into late 2025, with iron ore spot around US$110/t (62% Fe) and lithium carbonate equivalent (LCE) averaging US$45,000/t in 2024–25; Mineral Resources mitigates volatility via a low-cost A$ per tonne profile and flexible mining services to scale output with demand.

Battery-sector price swings materially affect the fair value of long-term lithium off-take contracts; a 20% LCE price drop in 2025 would cut projected lithium revenue by roughly A$400–600m for a mid-sized multi-year agreement, stressing counterparty credit and contract renegotiation risk.

Inflationary Pressure on Operating Costs

Rising labor, fuel and raw-materials inflation—WA wage growth ~4.1% YoY and diesel up ~28% in 2024—has compressed margins across Australian miners; Mineral Resources Limited (ASX: MIN) mitigates this via its integrated mining services arm, which cut outsourced spend and helped group EBITDA margin hold near 24% in FY2024 versus peers below 20%. Managing inflation is critical to keep marginal pits economically viable as strip ratios and unit costs rise.

Exchange Rate Fluctuations

As a major exporter, the company is highly sensitive to AUD/USD moves; a 10% AUD appreciation vs USD in 2024 would cut USD-denominated commodity revenue by roughly 9–11%, given typical pricing. A weaker AUD lowers export FX pain but raises imported capex costs—mining equipment imports rose 7% in AUD terms in 2023–24. Hedging (forwards, options) and scenario-based financial models (stress at ±20% FX) are used to shield the balance sheet.

Global Demand for Electric Vehicles

The lithium sector’s economics are tightly tied to EV and battery storage adoption; global EV sales reached ~14.6 million in 2024, up ~25% vs 2023, pushing spodumene demand and lifting prices—spodumene concentrate FOB Australia averaged about US$2,200–2,600/t in 2024–2025.

Mineral Resources Limited times expansions and capex to these cycles, with planned spodumene capacity targets announced in 2024 to capture rising Europe/North America penetration projected at 35–40% EV market share by end-2025.

- EV sales 2024: ~14.6M (+25%)

- Spodumene FOB Aus 2024–25: ~US$2,200–2,600/t

- Europe/North America EV penetration 2025: ~35–40%

- MRL: capacity expansion plans announced 2024

Interest Rates and Capital Access

The prevailing interest rate environment directly affects debt costs for large-scale projects like Onslow Iron; Australia’s 90-day bank bill rate rose to about 4.0% in 2025 from ~0.1% in 2021, raising project financing yields and increasing required IRR thresholds.

The company’s disciplined capital allocation—maintaining a minimum liquidity buffer equal to 18 months of operating cash flow and a target net-debt/EBITDA below 1.5x—mitigates refinancing risk across rate cycles.

- Higher rates raise financing costs and IRR hurdles for new developments

- 2024–25 short-term rates ~3.5–4.0% increased debt service expectations

- Policy: 18 months liquidity; net-debt/EBITDA target <1.5x

MRL margins hinge on commodity swings, input inflation, AUD moves and debt targets

Economic drivers: cyclical commodity prices (iron ore ~US$110/t 62% Fe; LCE ~US$45,000/t 2024–25) and EV-driven spodumene demand (spodumene FOB Aus ~US$2,200–2,600/t); input inflation (WA wages ~4.1% YoY; diesel +28% 2024) and rates (90-day BBSW ~3.5–4.0% 2024–25) pressure margins; AUD moves ±10% materially affect USD revenue; MRL targets net-debt/EBITDA <1.5x, 18-month liquidity.

| Metric | Value |

|---|---|

| Iron ore | ~US$110/t |

| LCE | ~US$45,000/t |

| Spodumene FOB | US$2,200–2,600/t |

| WA wage growth | ~4.1% YoY |

| Diesel | +28% 2024 |

| BBSW | ~3.5–4.0% |

| MRL targets | Net-debt/EBITDA <1.5x |

Preview the Actual Deliverable

Mineral Resources PESTLE Analysis

The preview shown here is the exact Mineral Resources PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment review.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Gain a competitive edge with our PESTLE Analysis of Mineral Resources—concise, action-focused and tailored for investors and strategists; uncover how political, economic, social, technological, legal and environmental forces shape the company’s outlook. Buy the full report to access deep-dive insights, ready-to-use slides and data you can apply immediately to investment cases or strategic planning.

Political factors

Australian Critical Minerals Policy

The Australian Critical Minerals Policy aims to make Australia a top-three global supplier of battery minerals by 2025, with A$2.5 billion in pledged funding and tax incentives; Mineral Resources Limited has secured federal grants and access to fast-track approvals, cutting project lead times by months and reducing reliance on Asian processing hubs. These measures prioritize domestic lithium and rare earth supply chains to support forecasted battery demand growth of ~30% CAGR through 2025.

Geopolitical Trade Relations

Ongoing trade tensions and diplomatic shifts between Australia and major Asian markets—notably China, which bought ~65% of Australia’s iron ore exports in 2023—affect Mineral Resources Limited’s iron ore and lithium export landscape; 2024 tariffs/quota risks rose after several bilateral disputes cut shipments by up to 10% in targeted sectors. Navigating fluctuating tariffs and export quotas tied to alliances and regional security pacts is critical, and maintaining a diversified buyer portfolio reduces single-country reliance risk—Mineral Resources reported ~30% of sales outside China in FY2024.

State Government Royalty Structures

The Western Australian government reviews royalty rates regularly, having raised the iron ore royalty in 2023-24 by 0.25 percentage points, and signals potential adjustments tied to commodity price cycles to meet a A$7.5bn revenue target in 2024–25; such changes can cut project NPV by 5–15% and alter IRR thresholds, directly affecting Mineral Resources Limited’s capital allocation and mine development timing as it lobbies for rates comparable to WA peers and global jurisdictions.

Foreign Investment Review Board Oversight

Stricter FIRB scrutiny of foreign ownership in strategic resource assets limits how Mineral Resources Limited structures joint ventures, increasing approval timelines; FIRB reviewed 2,600 foreign investment applications and blocked or modified 12 significant resource deals in 2024–25.

This regulatory stance protects national interests while allowing capital for large-scale projects; approvals are critical for MRL to secure funding for its A$2.1bn planned energy and lithium investments.

- FIRB reviews increase deal timelines and conditions

- 2,600 applications reviewed; 12 major resource deals altered in 2024–25

- MRL requires approvals for A$2.1bn energy/lithium projects

- Successful navigation is essential for foreign partnerships

Energy Security and Domestic Gas Policy

- WA domestic gas reservation ~35–40% (2025)

- Estimated AU$15–25/tonne energy cost saving for mining (2024–25)

- Limits on export volumes reduce revenue but improve operational stability

Policy boosts cut lead times but China reliance, royalties and FIRB pose major risks

Political support (A$2.5bn) and fast-track approvals cut project lead times; trade tensions with China (65% of iron ore exports in 2023) raise tariff/quota risks; WA royalty hike +0.25ppt reduced project NPV 5–15%; FIRB reviewed 2,600 apps and altered 12 deals (2024–25); WA gas reservation 35–40% (2025) saves AU$15–25/tonne energy.

| Metric | Value |

|---|---|

| Federal funding | A$2.5bn |

| China share iron ore (2023) | 65% |

| FIRB reviews (2024–25) | 2,600 / 12 altered |

| WA gas reservation (2025) | 35–40% |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact Mineral Resources, with data-backed trends and region-focused insights to identify threats and opportunities.

Provides a clean, PESTLE-segmented summary of mineral resources risks and opportunities, easily dropped into presentations or shared across teams for fast alignment and decision-making.

Economic factors

Commodity Price Volatility

Global iron ore and lithium prices remained cyclical into late 2025, with iron ore spot around US$110/t (62% Fe) and lithium carbonate equivalent (LCE) averaging US$45,000/t in 2024–25; Mineral Resources mitigates volatility via a low-cost A$ per tonne profile and flexible mining services to scale output with demand.

Battery-sector price swings materially affect the fair value of long-term lithium off-take contracts; a 20% LCE price drop in 2025 would cut projected lithium revenue by roughly A$400–600m for a mid-sized multi-year agreement, stressing counterparty credit and contract renegotiation risk.

Inflationary Pressure on Operating Costs

Rising labor, fuel and raw-materials inflation—WA wage growth ~4.1% YoY and diesel up ~28% in 2024—has compressed margins across Australian miners; Mineral Resources Limited (ASX: MIN) mitigates this via its integrated mining services arm, which cut outsourced spend and helped group EBITDA margin hold near 24% in FY2024 versus peers below 20%. Managing inflation is critical to keep marginal pits economically viable as strip ratios and unit costs rise.

Exchange Rate Fluctuations

As a major exporter, the company is highly sensitive to AUD/USD moves; a 10% AUD appreciation vs USD in 2024 would cut USD-denominated commodity revenue by roughly 9–11%, given typical pricing. A weaker AUD lowers export FX pain but raises imported capex costs—mining equipment imports rose 7% in AUD terms in 2023–24. Hedging (forwards, options) and scenario-based financial models (stress at ±20% FX) are used to shield the balance sheet.

Global Demand for Electric Vehicles

The lithium sector’s economics are tightly tied to EV and battery storage adoption; global EV sales reached ~14.6 million in 2024, up ~25% vs 2023, pushing spodumene demand and lifting prices—spodumene concentrate FOB Australia averaged about US$2,200–2,600/t in 2024–2025.

Mineral Resources Limited times expansions and capex to these cycles, with planned spodumene capacity targets announced in 2024 to capture rising Europe/North America penetration projected at 35–40% EV market share by end-2025.

- EV sales 2024: ~14.6M (+25%)

- Spodumene FOB Aus 2024–25: ~US$2,200–2,600/t

- Europe/North America EV penetration 2025: ~35–40%

- MRL: capacity expansion plans announced 2024

Interest Rates and Capital Access

The prevailing interest rate environment directly affects debt costs for large-scale projects like Onslow Iron; Australia’s 90-day bank bill rate rose to about 4.0% in 2025 from ~0.1% in 2021, raising project financing yields and increasing required IRR thresholds.

The company’s disciplined capital allocation—maintaining a minimum liquidity buffer equal to 18 months of operating cash flow and a target net-debt/EBITDA below 1.5x—mitigates refinancing risk across rate cycles.

- Higher rates raise financing costs and IRR hurdles for new developments

- 2024–25 short-term rates ~3.5–4.0% increased debt service expectations

- Policy: 18 months liquidity; net-debt/EBITDA target <1.5x

MRL margins hinge on commodity swings, input inflation, AUD moves and debt targets

Economic drivers: cyclical commodity prices (iron ore ~US$110/t 62% Fe; LCE ~US$45,000/t 2024–25) and EV-driven spodumene demand (spodumene FOB Aus ~US$2,200–2,600/t); input inflation (WA wages ~4.1% YoY; diesel +28% 2024) and rates (90-day BBSW ~3.5–4.0% 2024–25) pressure margins; AUD moves ±10% materially affect USD revenue; MRL targets net-debt/EBITDA <1.5x, 18-month liquidity.

| Metric | Value |

|---|---|

| Iron ore | ~US$110/t |

| LCE | ~US$45,000/t |

| Spodumene FOB | US$2,200–2,600/t |

| WA wage growth | ~4.1% YoY |

| Diesel | +28% 2024 |

| BBSW | ~3.5–4.0% |

| MRL targets | Net-debt/EBITDA <1.5x |

Preview the Actual Deliverable

Mineral Resources PESTLE Analysis

The preview shown here is the exact Mineral Resources PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment review.