Mister Spex Porter's Five Forces Analysis

From Overview to Strategy Blueprint

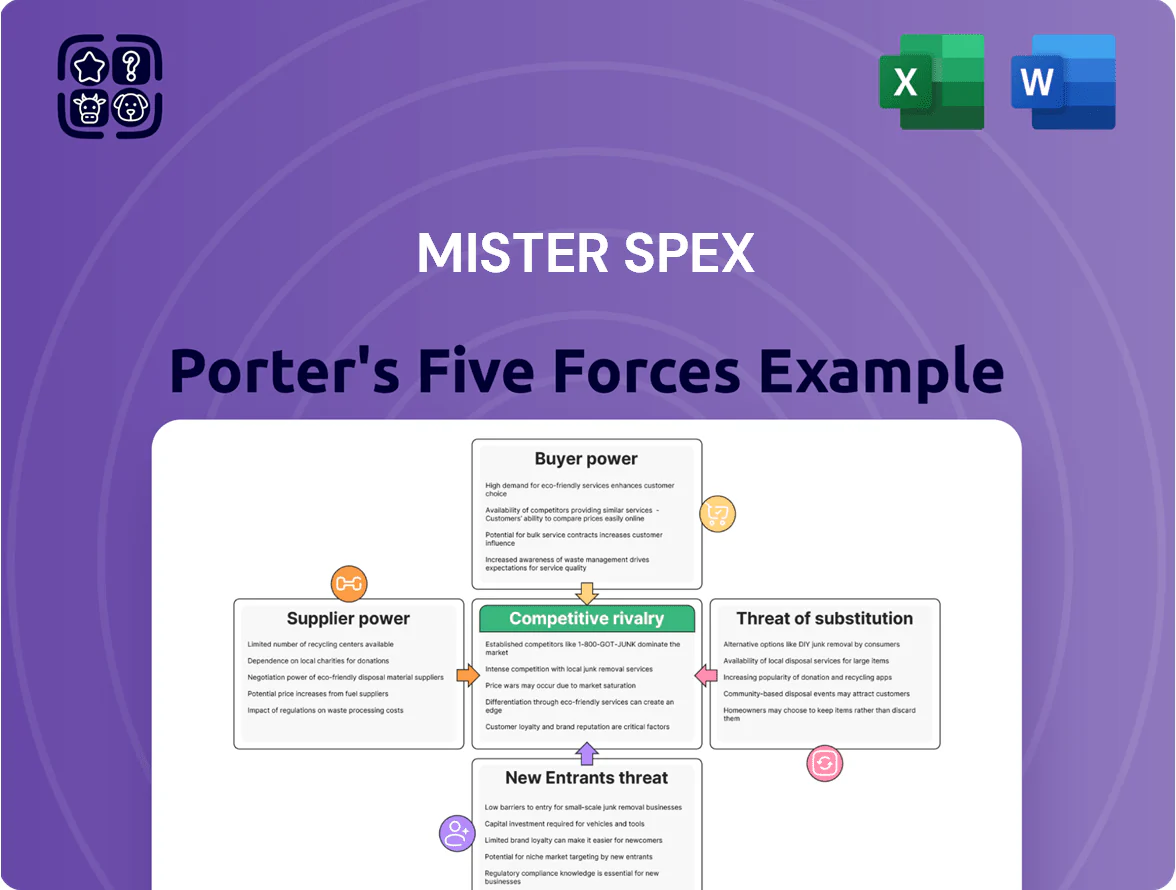

Mister Spex faces moderate buyer power, fierce online rivalry, and evolving substitute threats from omni-channel opticians; supplier leverage is limited but tech/platform risks raise entry barriers.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Mister Spex’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dominance of global eyewear conglomerates

The supply side is highly concentrated: EssilorLuxottica alone held about 28% global eyewear market share and reported €24.8bn revenue in 2023, owning premium brands and key lens patents, which raises supplier power over Mister Spex.

This limits Mister Spex’s ability to push for much lower wholesale prices on high-demand luxury frames, squeezing gross margins on premium assortments.

So Mister Spex must keep close partnerships and timely merchandising agreements to secure new collections that drive traffic and repeat sales.

Technical dependency on specialized lens manufacturers

Mister Spex runs in-house glazing but relies on specialized lens-blank and coating suppliers whose proprietary tech and scale limit replication; global lens-blank market consolidation left top three suppliers controlling ~60% of volumes in 2024. Suppliers can raise prices or prioritize larger OEMs, and a 5% input-cost rise for premium blanks would cut Mister Spex’s 2024 gross margin (reported 34.2%) by roughly 1.7 percentage points—directly squeezing profitability.

Infrastructure and logistics provider reliance

Mister Spex depends on third-party logistics and cloud providers to deliver 24–48 hour shipping and run its e-commerce stack; in 2024, logistics costs rose ~6–8% across Europe while cloud services saw enterprise price increases of 10–15% for key vendors. These suppliers can impose localized but strong power: a 5–10% rate shock or a 24–72 hour outage would hit order fulfillment and revenue recognition. Given 2024 gross margin ~34%, such cost or service shocks would compress margins materially.

Mitigation through private label expansion

Mister Spex expanded private-label frames to 28% of unit sales by FY 2024, cutting purchase dependence on major conglomerates and external designers.

Controlling design and sourcing lifted gross margins on private-label SKUs by ~9 percentage points vs branded frames in 2024, improving bargaining leverage.

This internal supply chain reduced supplier concentration risk—top-5 external suppliers fell from 62% to 41% of procurement value between 2021–2024.

- Private-label = 28% of units (FY 2024)

- Gross margin premium ≈ +9 pp vs branded (2024)

- Top-5 supplier share down 62% → 41% (2021–2024)

Fragmentation of independent boutique brands

The niche independent eyewear market is highly fragmented, giving Mister Spex greater bargaining leverage; over 70% of listed designer SKUs on Mister Spex in 2024 came from independent or boutique labels, reducing supplier concentration.

Because Mister Spex reached ~12 million European users in 2024, smaller brands accept tighter margins and platform fees for scale access, letting Mister Spex negotiate more favorable terms. This supplier diversity offsets power of major eyewear conglomerates.

- 70%+ boutique SKU share (2024)

- ~12 million European users (2024)

- Lower supplier concentration => higher platform leverage

Mister Spex shrinks supplier sway: private-label boost, top-5 share down 62%→41%

Supplier power is mixed: conglomerates like EssilorLuxottica (≈28% market share; €24.8bn revenue 2023) and top-3 lens-blank suppliers (~60% volumes 2024) raise input and premium-frame risk, but Mister Spex reduced dependence via private-label (28% units, +9pp gross margin vs branded 2024) and platform scale (~12m users 2024), cutting top-5 supplier share 62%→41% (2021–2024).

| Metric | Value |

|---|---|

| EssilorLuxottica share | ≈28% |

| EssilorLuxottica revenue | €24.8bn (2023) |

| Private-label share | 28% units (FY2024) |

| Private-label margin lift | +9 pp (2024) |

| Top-3 lens suppliers | ~60% volumes (2024) |

| Top-5 supplier share | 62% → 41% (2021–2024) |

| Platform users | ~12m Europe (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Mister Spex that uncovers competitive intensity, buyer and supplier power, threats from substitutes and new entrants, and highlights disruptive forces and strategic levers to protect market share.

A concise, one-sheet Porter’s Five Forces for Mister Spex—instantly highlights competitive pressures and strategic levers for quick, board-ready decisions.

Customers Bargaining Power

Low switching costs in a digital environment

Customers can switch between online opticians and traditional retailers with a click and no financial penalty, and industry data shows European online eyewear conversion rates fell 6% YoY in 2024 as shoppers shop around more. This low switching cost forces Mister Spex to update UX, virtual try-on tech, and loyalty offers—Mister Spex reported 2024 revenue of €193m, so retention underpins growth. The lack of exit barriers keeps pressure to deliver continuous value; churn sensitivity rises if onboarding or delivery slips beyond 7–10 days.

High price transparency and comparison tools

The digital model lets buyers use comparison engines and tools to find the cheapest Mister Spex frames or contact lenses, with German price-comparison site checks showing average online price spreads of 15–25% in 2024. This visibility lets customers push for lower prices and regular promotions, and Mister Spex ran >20% of sales on discounts in 2024 to stay competitive. As a result, Mister Spex must tune pricing to keep conversions without sparking a race-to-the-bottom on margin.

Rising expectations for omnichannel flexibility

Modern eyewear buyers expect seamless online browsing, home try-ons, and in-store adjustments; 2024 surveys show 62% of EU eyewear shoppers prefer brands offering hybrid services. If Mister Spex fails here, churn rises—benchmarks show omnichannel leaders cut churn by ~18%. This customer demand forces capital allocation to logistics, AR fitting tech, and retail partnerships, giving buyers clear leverage over Mister Spex’s operational spend.

Influence of social proof and online reviews

Trust drives eyewear buys; 72% of EU shoppers read reviews before purchase and 58% cite peer opinion as decisive, so social proof heavily shapes conversion for Mister Spex.

Negative threads on delivery or quality spread fast—platform data show a 1-point drop in average rating can cut conversion by ~10% and raise return rates 6–12%.

That gives customers collective leverage over Mister Spex’s reputation and pricing power; rapid review management and logistics fixes are critical to stem churn.

- 72% EU shoppers read reviews

- 1-point rating drop → ~10% lower conversion

- Rating issues raise returns 6–12%

- Reviews shape pricing and market position

Demand for value-added services at no cost

Mister Spex: Customer leverage, review sensitivity, and costly hybrid service model

High switching ease and price transparency give customers strong leverage over Mister Spex; 2024 figures: revenue €193m, online price spreads 15–25%, >20% sales on discounts, 62% prefer hybrid service, 72% read reviews. Free returns (~€4–8/order) and free eye tests (~€10–20/visit) raise CAC ~15%, while a 1‑point rating drop cuts conversion ~10% and raises returns 6–12%.

| Metric | 2024 Value |

|---|---|

| Revenue (Mister Spex) | €193m |

| Online price spread | 15–25% |

| Sales on discounts | >20% |

| Prefer hybrid service | 62% |

| Read reviews | 72% |

| Free returns cost | €4–8/order |

| Free eye test cost | €10–20/visit |

| CAC uplift | ~15% |

| 1‑pt rating → conversion | −~10% |

| Rating issues → returns | +6–12% |

Preview Before You Purchase

Mister Spex Porter's Five Forces Analysis

This preview shows the exact Mister Spex Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples, fully formatted and ready for use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Mister Spex faces moderate buyer power, fierce online rivalry, and evolving substitute threats from omni-channel opticians; supplier leverage is limited but tech/platform risks raise entry barriers.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Mister Spex’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dominance of global eyewear conglomerates

The supply side is highly concentrated: EssilorLuxottica alone held about 28% global eyewear market share and reported €24.8bn revenue in 2023, owning premium brands and key lens patents, which raises supplier power over Mister Spex.

This limits Mister Spex’s ability to push for much lower wholesale prices on high-demand luxury frames, squeezing gross margins on premium assortments.

So Mister Spex must keep close partnerships and timely merchandising agreements to secure new collections that drive traffic and repeat sales.

Technical dependency on specialized lens manufacturers

Mister Spex runs in-house glazing but relies on specialized lens-blank and coating suppliers whose proprietary tech and scale limit replication; global lens-blank market consolidation left top three suppliers controlling ~60% of volumes in 2024. Suppliers can raise prices or prioritize larger OEMs, and a 5% input-cost rise for premium blanks would cut Mister Spex’s 2024 gross margin (reported 34.2%) by roughly 1.7 percentage points—directly squeezing profitability.

Infrastructure and logistics provider reliance

Mister Spex depends on third-party logistics and cloud providers to deliver 24–48 hour shipping and run its e-commerce stack; in 2024, logistics costs rose ~6–8% across Europe while cloud services saw enterprise price increases of 10–15% for key vendors. These suppliers can impose localized but strong power: a 5–10% rate shock or a 24–72 hour outage would hit order fulfillment and revenue recognition. Given 2024 gross margin ~34%, such cost or service shocks would compress margins materially.

Mitigation through private label expansion

Mister Spex expanded private-label frames to 28% of unit sales by FY 2024, cutting purchase dependence on major conglomerates and external designers.

Controlling design and sourcing lifted gross margins on private-label SKUs by ~9 percentage points vs branded frames in 2024, improving bargaining leverage.

This internal supply chain reduced supplier concentration risk—top-5 external suppliers fell from 62% to 41% of procurement value between 2021–2024.

- Private-label = 28% of units (FY 2024)

- Gross margin premium ≈ +9 pp vs branded (2024)

- Top-5 supplier share down 62% → 41% (2021–2024)

Fragmentation of independent boutique brands

The niche independent eyewear market is highly fragmented, giving Mister Spex greater bargaining leverage; over 70% of listed designer SKUs on Mister Spex in 2024 came from independent or boutique labels, reducing supplier concentration.

Because Mister Spex reached ~12 million European users in 2024, smaller brands accept tighter margins and platform fees for scale access, letting Mister Spex negotiate more favorable terms. This supplier diversity offsets power of major eyewear conglomerates.

- 70%+ boutique SKU share (2024)

- ~12 million European users (2024)

- Lower supplier concentration => higher platform leverage

Mister Spex shrinks supplier sway: private-label boost, top-5 share down 62%→41%

Supplier power is mixed: conglomerates like EssilorLuxottica (≈28% market share; €24.8bn revenue 2023) and top-3 lens-blank suppliers (~60% volumes 2024) raise input and premium-frame risk, but Mister Spex reduced dependence via private-label (28% units, +9pp gross margin vs branded 2024) and platform scale (~12m users 2024), cutting top-5 supplier share 62%→41% (2021–2024).

| Metric | Value |

|---|---|

| EssilorLuxottica share | ≈28% |

| EssilorLuxottica revenue | €24.8bn (2023) |

| Private-label share | 28% units (FY2024) |

| Private-label margin lift | +9 pp (2024) |

| Top-3 lens suppliers | ~60% volumes (2024) |

| Top-5 supplier share | 62% → 41% (2021–2024) |

| Platform users | ~12m Europe (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Mister Spex that uncovers competitive intensity, buyer and supplier power, threats from substitutes and new entrants, and highlights disruptive forces and strategic levers to protect market share.

A concise, one-sheet Porter’s Five Forces for Mister Spex—instantly highlights competitive pressures and strategic levers for quick, board-ready decisions.

Customers Bargaining Power

Low switching costs in a digital environment

Customers can switch between online opticians and traditional retailers with a click and no financial penalty, and industry data shows European online eyewear conversion rates fell 6% YoY in 2024 as shoppers shop around more. This low switching cost forces Mister Spex to update UX, virtual try-on tech, and loyalty offers—Mister Spex reported 2024 revenue of €193m, so retention underpins growth. The lack of exit barriers keeps pressure to deliver continuous value; churn sensitivity rises if onboarding or delivery slips beyond 7–10 days.

High price transparency and comparison tools

The digital model lets buyers use comparison engines and tools to find the cheapest Mister Spex frames or contact lenses, with German price-comparison site checks showing average online price spreads of 15–25% in 2024. This visibility lets customers push for lower prices and regular promotions, and Mister Spex ran >20% of sales on discounts in 2024 to stay competitive. As a result, Mister Spex must tune pricing to keep conversions without sparking a race-to-the-bottom on margin.

Rising expectations for omnichannel flexibility

Modern eyewear buyers expect seamless online browsing, home try-ons, and in-store adjustments; 2024 surveys show 62% of EU eyewear shoppers prefer brands offering hybrid services. If Mister Spex fails here, churn rises—benchmarks show omnichannel leaders cut churn by ~18%. This customer demand forces capital allocation to logistics, AR fitting tech, and retail partnerships, giving buyers clear leverage over Mister Spex’s operational spend.

Influence of social proof and online reviews

Trust drives eyewear buys; 72% of EU shoppers read reviews before purchase and 58% cite peer opinion as decisive, so social proof heavily shapes conversion for Mister Spex.

Negative threads on delivery or quality spread fast—platform data show a 1-point drop in average rating can cut conversion by ~10% and raise return rates 6–12%.

That gives customers collective leverage over Mister Spex’s reputation and pricing power; rapid review management and logistics fixes are critical to stem churn.

- 72% EU shoppers read reviews

- 1-point rating drop → ~10% lower conversion

- Rating issues raise returns 6–12%

- Reviews shape pricing and market position

Demand for value-added services at no cost

Mister Spex: Customer leverage, review sensitivity, and costly hybrid service model

High switching ease and price transparency give customers strong leverage over Mister Spex; 2024 figures: revenue €193m, online price spreads 15–25%, >20% sales on discounts, 62% prefer hybrid service, 72% read reviews. Free returns (~€4–8/order) and free eye tests (~€10–20/visit) raise CAC ~15%, while a 1‑point rating drop cuts conversion ~10% and raises returns 6–12%.

| Metric | 2024 Value |

|---|---|

| Revenue (Mister Spex) | €193m |

| Online price spread | 15–25% |

| Sales on discounts | >20% |

| Prefer hybrid service | 62% |

| Read reviews | 72% |

| Free returns cost | €4–8/order |

| Free eye test cost | €10–20/visit |

| CAC uplift | ~15% |

| 1‑pt rating → conversion | −~10% |

| Rating issues → returns | +6–12% |

Preview Before You Purchase

Mister Spex Porter's Five Forces Analysis

This preview shows the exact Mister Spex Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples, fully formatted and ready for use.