Mitsui Chemicals Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

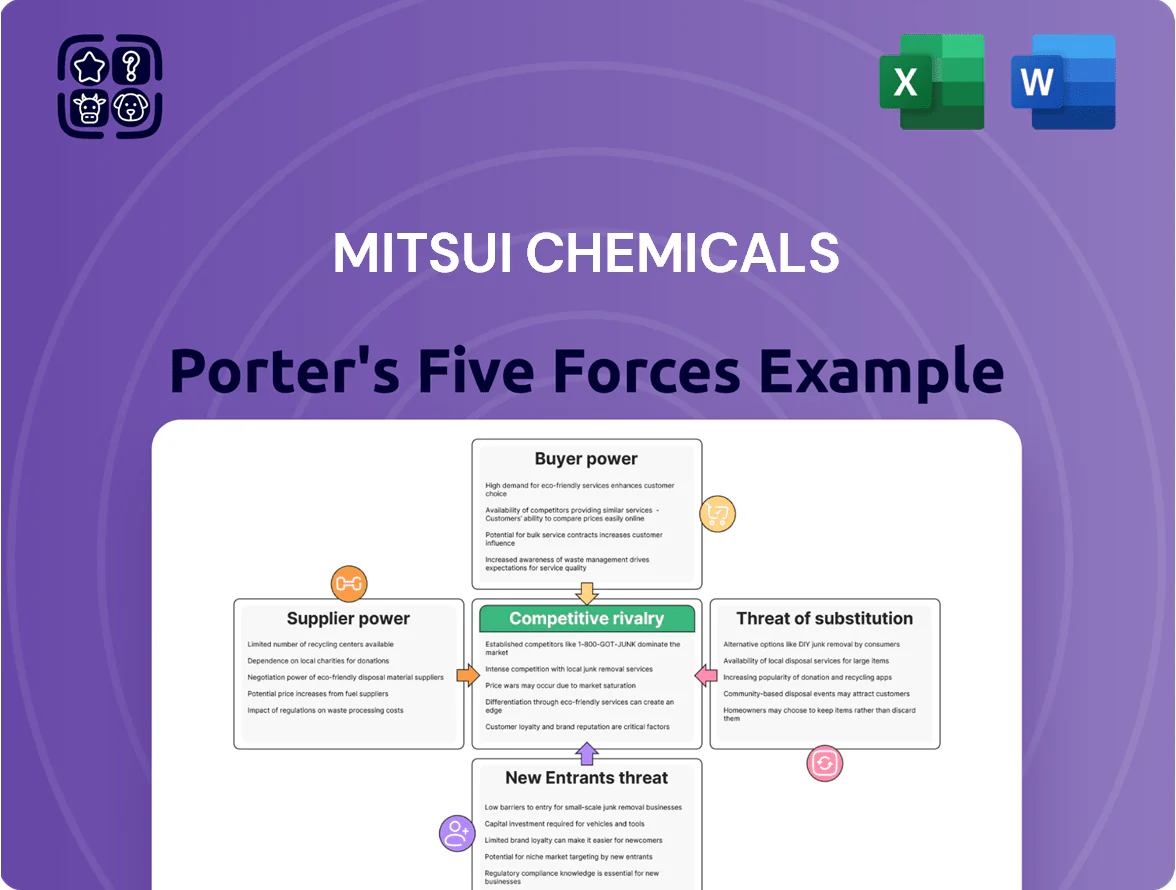

Mitsui Chemicals faces moderate supplier power and high rivalry as it navigates raw material volatility, regulatory pressures, and shifting end-market demand, while barriers to entry and substitutes exert mixed influence on margins and innovation incentives. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Mitsui Chemicals’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility of Naphtha and Crude Oil Feedstock

The primary feedstock for Mitsui Chemicals is naphtha, a crude-oil derivative whose price swung 38% between 2020–2024, driving feedstock cost volatility and squeezing margins.

Procurement depends on a few global oil producers and refineries, so Middle East and Russia-Ukraine disruptions in 2022–2023 raised spot premiums and pushed input costs up.

By end-2025 Mitsui aims to diversify suppliers and increase petrochemical feedstock flexibility to cut exposure to OPEC+ pricing power and reduce procurement risk.

Dependency on Specialized Chemical Intermediates

For functional chemicals and performance polymers, Mitsui Chemicals depends on a few specialized suppliers for catalysts and intermediates, concentrating supply and giving vendors pricing and delivery leverage; in 2024 about 60% of such inputs came from top-five suppliers.

The supplier concentration raised procurement costs volatility—input-price spikes of up to 15% hit margins in FY2023—so Mitsui Chemicals offsets risk via long-term strategic contracts and selective backward integration, including its 2022 joint investment in upstream intermediates capacity in Chiba.

Rising Costs of Renewable and Bio-based Inputs

As Mitsui Chemicals accelerates toward carbon neutrality by 2050, demand for bio-based feedstocks rose ~35% year-over-year by Q3 2025, tightening supply; fewer than 10 large-scale biofeedstock suppliers in Japan and South Korea currently supply industrial grades, letting sellers command 15–30% price premiums for certified green inputs. This transition gives bio-suppliers temporary high bargaining power until recycling and bio-material capacity (projected to double by 2030) matures.

Energy Provider Leverage in Regional Hubs

Energy costs in Japan and Europe drive Mitsui Chemicals’ margins: electricity and natural gas account for roughly 15–25% of variable costs in petrochemical and performance-materials plants, so regional utility rate hikes cut EBITDA directly (example: Japan industrial electricity rose ~7% in 2024 vs 2021).

Regional utilities and state-owned suppliers act like local monopolies, limiting quick fuel switching; Mitsui’s sunk assets and high energy intensity mean suppliers hold steady bargaining power, raising input-cost risk.

- Energy share of variable cost: 15–25%

- Japan industrial electricity +7% (2024 vs 2021)

- Low quick-switch ability due to asset specificity

- Regional utility/state dominance = sustained supplier leverage

Logistics and Maritime Shipping Constraints

- Asia-Europe 40ft avg $2,400 (Q4 2025)

- Blank sailings cut capacity ~6–8% (2024–25)

- Top 10 carriers ≈85% capacity share (2025)

- Higher landed cost and lead-time volatility

Supplier power spikes: feedstock, energy and freight squeeze margins

Suppliers hold medium-high power: naphtha price swings (±38% 2020–24) and concentrated oil/refinery sources raise cost exposure; top-five vendors supplied ~60% of specialized inputs in 2024, and biofeedstock premiums ran 15–30% by Q3 2025, while energy costs (15–25% of variable cost) and freight (Asia‑Europe $2,400/40ft Q4 2025) add leverage.

| Metric | Value |

|---|---|

| Naphtha price swing 2020–24 | 38% |

| Top‑5 supplier share (specialized inputs, 2024) | ~60% |

| Biofeedstock premium (Q3 2025) | 15–30% |

| Energy share of variable cost | 15–25% |

| Asia‑Europe 40ft (Q4 2025) | $2,400 |

What is included in the product

Tailored Porter's Five Forces analysis for Mitsui Chemicals, uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging disruptive threats to its market position.

A concise Porter's Five Forces one-sheet for Mitsui Chemicals—quickly highlights supplier/customer power, rivalry, substitutes, and entrant risks so executives can make fast, informed strategy calls.

Customers Bargaining Power

High Concentration in the Automotive Industry

Price Sensitivity in the Commodity Chemicals Segment

In basic chemicals and petrochemicals, undifferentiated products make price the main buying criterion; global spot ethylene/propylene spreads fell 18% in 2024, intensifying price focus. Buyers in packaging and construction switch easily—Mitsui Chemicals faces churn if its pricing lags market rates where transparency is high. Low loyalty raises pressure on margins; in 2024 commodity sales saw ~12% EBITDA margin vs 18% in specialties, highlighting sensitivity to price shifts.

Stringent Requirements from the Healthcare Sector

Customers in healthcare and ophthalmic lenses require stringent certifications (ISO 13485, FDA 510(k)) and defect rates often below 50 ppm, which limits rapid switching and gave Mitsui Chemicals roughly 12–15% stable revenue from medical polymers in FY2024; however clients push for multi-year price freezes and co-funded R&D, shifting margin pressure back to Mitsui and creating a balanced bargaining power where technical dependence equals pricing demands.

Sustainability and Circular Economy Demands

By end-2025, downstream buyers push Mitsui Chemicals for low-carbon and recyclable polymers, citing scope 3 targets; 68% of global CPG firms require supplier emissions data, per 2024 CDP trends, forcing Mitsui to supply LCA reports and certified recyclates.

Large consumer goods firms can refuse contracts without green certification—roughly 40% of RFPs in 2024 demanded third-party eco-labels—so environmental compliance is now a tangible bargaining chip affecting pricing and contract terms.

- 68% of CPGs require supplier emissions data

- ~40% of 2024 RFPs demanded eco-certification

- Green-certified inputs often command price premia of 5–12%

Availability of Low-Cost Regional Alternatives

Buyers in Asia can choose from many low-cost chemical makers in China and Southeast Asia, raising Mitsui Chemicals' customer bargaining power; Asian chemical exports from China grew 6.8% in 2024, expanding options for purchasers.

Customers leverage supplier competition to demand better prices and terms, pressuring margins; spot-price sensitivity rose after 2022 raw-material swings.

Mitsui fights back by shifting sales to high-value functional materials—these products accounted for about 38% of Mitsui Chemicals’ FY2024 revenue—harder for low-cost regional firms to copy.

- China/SEA producers expand choices; China exports +6.8% in 2024

- Buyer pressure lowers prices; spot volatility increased post-2022

- Mitsui’s high-value segment = ~38% of FY2024 revenue

Auto demand crushes specialty margins; green certification drives 5–12% price premia

Buyers hold high leverage: auto customers take ~35% of FY2024 performance-polymers sales, forcing 0.5–3% annual price cuts and JIT terms; commodity petrochemicals drove an EBITDA margin gap (~12% vs 18% specialties in 2024). Medical polymers gave 12–15% stable revenue but shift R&D costs to Mitsui. Green demands rose—68% CPGs want emissions data; ~40% of 2024 RFPs required eco-certification, with 5–12% price premia.

| Metric | Value |

|---|---|

| Auto share (perf. polymers) | ~35% FY2024 |

| EBITDA: commodities | ~12% 2024 |

| EBITDA: specialties | ~18% 2024 |

| Medical polymers revenue | 12–15% FY2024 |

| CPGs needing emissions data | 68% (2024) |

| RFPs needing eco-cert | ~40% (2024) |

| Green premia | 5–12% |

Preview Before You Purchase

Mitsui Chemicals Porter's Five Forces Analysis

This preview shows the exact Mitsui Chemicals Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples, fully formatted and ready for use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Mitsui Chemicals faces moderate supplier power and high rivalry as it navigates raw material volatility, regulatory pressures, and shifting end-market demand, while barriers to entry and substitutes exert mixed influence on margins and innovation incentives. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Mitsui Chemicals’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility of Naphtha and Crude Oil Feedstock

The primary feedstock for Mitsui Chemicals is naphtha, a crude-oil derivative whose price swung 38% between 2020–2024, driving feedstock cost volatility and squeezing margins.

Procurement depends on a few global oil producers and refineries, so Middle East and Russia-Ukraine disruptions in 2022–2023 raised spot premiums and pushed input costs up.

By end-2025 Mitsui aims to diversify suppliers and increase petrochemical feedstock flexibility to cut exposure to OPEC+ pricing power and reduce procurement risk.

Dependency on Specialized Chemical Intermediates

For functional chemicals and performance polymers, Mitsui Chemicals depends on a few specialized suppliers for catalysts and intermediates, concentrating supply and giving vendors pricing and delivery leverage; in 2024 about 60% of such inputs came from top-five suppliers.

The supplier concentration raised procurement costs volatility—input-price spikes of up to 15% hit margins in FY2023—so Mitsui Chemicals offsets risk via long-term strategic contracts and selective backward integration, including its 2022 joint investment in upstream intermediates capacity in Chiba.

Rising Costs of Renewable and Bio-based Inputs

As Mitsui Chemicals accelerates toward carbon neutrality by 2050, demand for bio-based feedstocks rose ~35% year-over-year by Q3 2025, tightening supply; fewer than 10 large-scale biofeedstock suppliers in Japan and South Korea currently supply industrial grades, letting sellers command 15–30% price premiums for certified green inputs. This transition gives bio-suppliers temporary high bargaining power until recycling and bio-material capacity (projected to double by 2030) matures.

Energy Provider Leverage in Regional Hubs

Energy costs in Japan and Europe drive Mitsui Chemicals’ margins: electricity and natural gas account for roughly 15–25% of variable costs in petrochemical and performance-materials plants, so regional utility rate hikes cut EBITDA directly (example: Japan industrial electricity rose ~7% in 2024 vs 2021).

Regional utilities and state-owned suppliers act like local monopolies, limiting quick fuel switching; Mitsui’s sunk assets and high energy intensity mean suppliers hold steady bargaining power, raising input-cost risk.

- Energy share of variable cost: 15–25%

- Japan industrial electricity +7% (2024 vs 2021)

- Low quick-switch ability due to asset specificity

- Regional utility/state dominance = sustained supplier leverage

Logistics and Maritime Shipping Constraints

- Asia-Europe 40ft avg $2,400 (Q4 2025)

- Blank sailings cut capacity ~6–8% (2024–25)

- Top 10 carriers ≈85% capacity share (2025)

- Higher landed cost and lead-time volatility

Supplier power spikes: feedstock, energy and freight squeeze margins

Suppliers hold medium-high power: naphtha price swings (±38% 2020–24) and concentrated oil/refinery sources raise cost exposure; top-five vendors supplied ~60% of specialized inputs in 2024, and biofeedstock premiums ran 15–30% by Q3 2025, while energy costs (15–25% of variable cost) and freight (Asia‑Europe $2,400/40ft Q4 2025) add leverage.

| Metric | Value |

|---|---|

| Naphtha price swing 2020–24 | 38% |

| Top‑5 supplier share (specialized inputs, 2024) | ~60% |

| Biofeedstock premium (Q3 2025) | 15–30% |

| Energy share of variable cost | 15–25% |

| Asia‑Europe 40ft (Q4 2025) | $2,400 |

What is included in the product

Tailored Porter's Five Forces analysis for Mitsui Chemicals, uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging disruptive threats to its market position.

A concise Porter's Five Forces one-sheet for Mitsui Chemicals—quickly highlights supplier/customer power, rivalry, substitutes, and entrant risks so executives can make fast, informed strategy calls.

Customers Bargaining Power

High Concentration in the Automotive Industry

Price Sensitivity in the Commodity Chemicals Segment

In basic chemicals and petrochemicals, undifferentiated products make price the main buying criterion; global spot ethylene/propylene spreads fell 18% in 2024, intensifying price focus. Buyers in packaging and construction switch easily—Mitsui Chemicals faces churn if its pricing lags market rates where transparency is high. Low loyalty raises pressure on margins; in 2024 commodity sales saw ~12% EBITDA margin vs 18% in specialties, highlighting sensitivity to price shifts.

Stringent Requirements from the Healthcare Sector

Customers in healthcare and ophthalmic lenses require stringent certifications (ISO 13485, FDA 510(k)) and defect rates often below 50 ppm, which limits rapid switching and gave Mitsui Chemicals roughly 12–15% stable revenue from medical polymers in FY2024; however clients push for multi-year price freezes and co-funded R&D, shifting margin pressure back to Mitsui and creating a balanced bargaining power where technical dependence equals pricing demands.

Sustainability and Circular Economy Demands

By end-2025, downstream buyers push Mitsui Chemicals for low-carbon and recyclable polymers, citing scope 3 targets; 68% of global CPG firms require supplier emissions data, per 2024 CDP trends, forcing Mitsui to supply LCA reports and certified recyclates.

Large consumer goods firms can refuse contracts without green certification—roughly 40% of RFPs in 2024 demanded third-party eco-labels—so environmental compliance is now a tangible bargaining chip affecting pricing and contract terms.

- 68% of CPGs require supplier emissions data

- ~40% of 2024 RFPs demanded eco-certification

- Green-certified inputs often command price premia of 5–12%

Availability of Low-Cost Regional Alternatives

Buyers in Asia can choose from many low-cost chemical makers in China and Southeast Asia, raising Mitsui Chemicals' customer bargaining power; Asian chemical exports from China grew 6.8% in 2024, expanding options for purchasers.

Customers leverage supplier competition to demand better prices and terms, pressuring margins; spot-price sensitivity rose after 2022 raw-material swings.

Mitsui fights back by shifting sales to high-value functional materials—these products accounted for about 38% of Mitsui Chemicals’ FY2024 revenue—harder for low-cost regional firms to copy.

- China/SEA producers expand choices; China exports +6.8% in 2024

- Buyer pressure lowers prices; spot volatility increased post-2022

- Mitsui’s high-value segment = ~38% of FY2024 revenue

Auto demand crushes specialty margins; green certification drives 5–12% price premia

Buyers hold high leverage: auto customers take ~35% of FY2024 performance-polymers sales, forcing 0.5–3% annual price cuts and JIT terms; commodity petrochemicals drove an EBITDA margin gap (~12% vs 18% specialties in 2024). Medical polymers gave 12–15% stable revenue but shift R&D costs to Mitsui. Green demands rose—68% CPGs want emissions data; ~40% of 2024 RFPs required eco-certification, with 5–12% price premia.

| Metric | Value |

|---|---|

| Auto share (perf. polymers) | ~35% FY2024 |

| EBITDA: commodities | ~12% 2024 |

| EBITDA: specialties | ~18% 2024 |

| Medical polymers revenue | 12–15% FY2024 |

| CPGs needing emissions data | 68% (2024) |

| RFPs needing eco-cert | ~40% (2024) |

| Green premia | 5–12% |

Preview Before You Purchase

Mitsui Chemicals Porter's Five Forces Analysis

This preview shows the exact Mitsui Chemicals Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples, fully formatted and ready for use.