Mitsui Fudosan Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

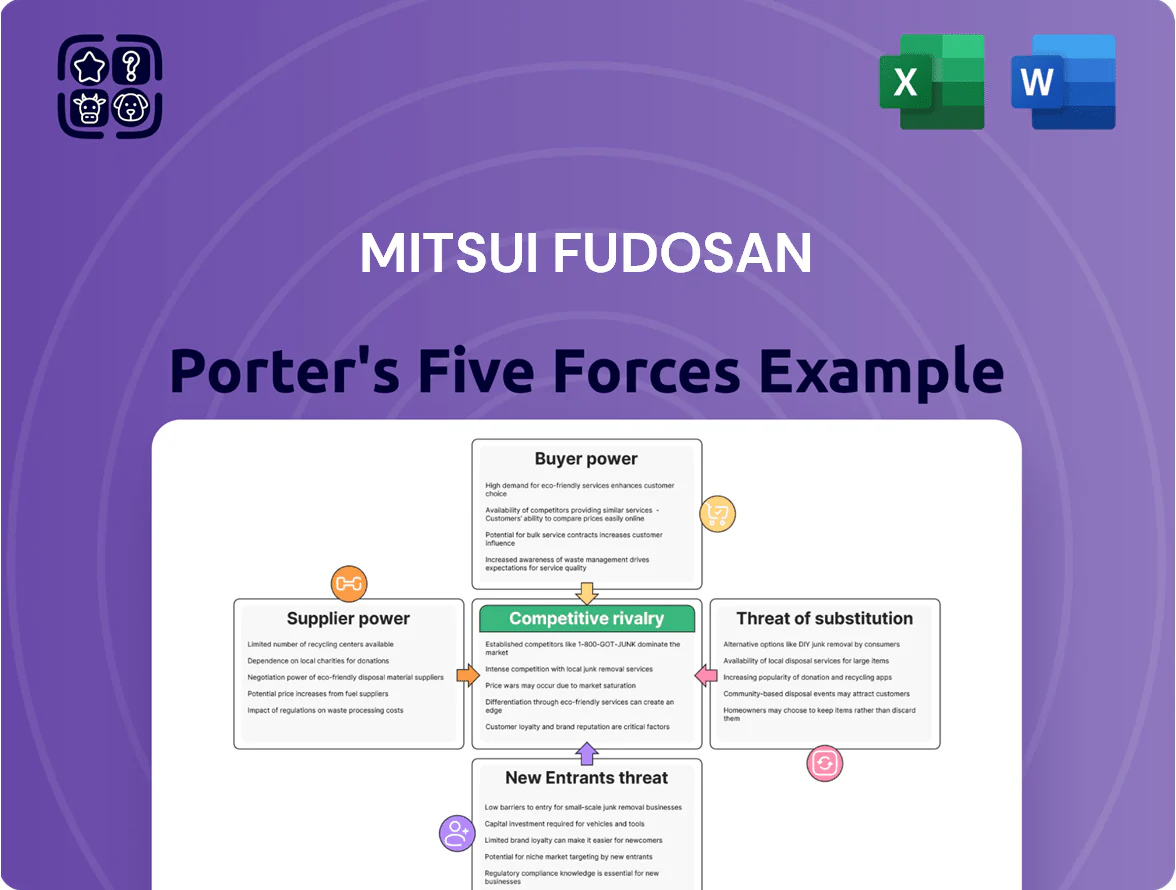

Mitsui Fudosan faces moderate rivalry and high barriers from scale and land control, while buyer power is tempered by differentiated mixed-use developments and long-term leases; supplier influence varies by construction cycles and regulatory constraints, and threat of substitutes is limited but rising via remote work and retail shifts. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Mitsui Fudosan’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of major construction contractors

The Japanese construction market is concentrated: top 5 contractors (Kajima, Taisei, Obayashi, Shimizu, Takenaka) held about 35% of construction revenue in 2024, giving Mitsui Fudosan dependence on their capacity for mega-redevelopments.

These Super Zenikon firms provide unique technical expertise and can mobilize >50,000 workers and heavy equipment for Tokyo projects, so they command price and schedule leverage.

With Tokyo redevelopment investment above ¥3.2 trillion in 2024, contractor bargaining power rises, pressuring Mitsui Fudosan margins and procurement terms.

Limited availability of prime urban land

Landowners in Tokyo and other major Japanese CBDs hold strong leverage because developable urban land is finite; Tokyo’s 23 wards saw built-up area rise to 622 km² by 2023, tightening supply. Mitsui Fudosan must either outbid rivals—2024 land transaction prices in central Tokyo averaged about ¥1.2 million/m²—or form joint ventures with owners to secure sites. This scarcity keeps suppliers in a high bargaining position during acquisitions.

Persistent shortages in skilled construction labor

Japan’s working-age population fell 2.9% from 2015–2020 and shrank to 74.1m in 2024, creating a skilled construction labor shortfall that boosts bargaining power of subcontractors.

Specialized trades have seen wage growth ~4.5% YoY in 2023–24, letting labor providers demand higher pay and stricter terms.

For Mitsui Fudosan this raises project construction costs—estimates suggest 3–6% margin squeeze—and increases risk of schedule delays on large developments.

Fluctuations in global raw material prices

Suppliers of steel, cement and energy face global commodity swings and geopolitical risks; steel prices rose ~12% in 2024 and LNG spot prices jumped 40% in late 2023, so Mitsui Fudosan is exposed to input-cost shock passed through by contractors.

Long projects make margins vulnerable; Mitsui Fudosan must hedge, fix contracts, or index clauses to protect margins—construction cost inflation averaged 6–8% annually in Japan 2022–24.

- Steel +12% (2024)

- LNG spot +40% (late 2023)

- Construction inflation 6–8% (2022–24)

- Mitigations: hedges, fixed-price contracts, index clauses

Dependence on specialized technology providers

The shift to smart buildings and sustainable urban development raises Mitsui Fudosan’s dependence on tech firms supplying IoT and energy-management systems; Gartner estimated global smart building spending at $31.7B in 2024, up 12% YoY.

These suppliers deliver proprietary hardware and software that embed into asset value—upgrades can cost 1–3% of project value, tying Mitsui to niche vendors for compatibility and support.

A concentration of high-tech vendors creates supplier power, risking higher prices, slower innovation access, and integration lock‑in for future-proofing assets.

- Smart-building spend $31.7B (2024)

- Upgrade cost ~1–3% of asset value

- Proprietary systems cause vendor lock‑in

Suppliers’ leverage tightens Mitsui Fudosan margins as land, labor and inputs surge

Suppliers—large contractors, landowners, skilled labor, commodity and smart‑tech vendors—hold strong bargaining power versus Mitsui Fudosan, driven by contractor concentration (top 5 ≈35% market share, 2024), Tokyo land scarcity (central Tokyo ¥1.2M/m² avg, 2024), labor shortfall (74.1m working‑age, 2024) and input shocks (steel +12% 2024; LNG +40% late‑2023), squeezing margins ~3–6%.

| Metric | Value |

|---|---|

| Top5 contractors share | ≈35% (2024) |

| Tokyo land price | ¥1.2M/m² (2024) |

| Working‑age pop | 74.1M (2024) |

| Steel | +12% (2024) |

| LNG | +40% (late‑2023) |

What is included in the product

Tailored exclusively for Mitsui Fudosan, this Porter's Five Forces overview uncovers key drivers of competition, customer and supplier influence, market entry barriers, and disruptive substitutes that shape its pricing power and strategic positioning.

A concise, one-sheet Porter's Five Forces summary for Mitsui Fudosan—instantly highlights competitive pressures and real estate-specific risks for quick strategic decisions.

Customers Bargaining Power

Corporate demand for flexible office solutions

Large corporate tenants now demand flexible leases and high-spec offices for hybrid work; in Japan 2024 demand for flexible space grew 18% year-over-year, giving these clients strong bargaining power.

They push for amenities and green building certification (e.g., ZEB, CASBEE), and often secure rent premiums or fit-out contributions; Mitsui Fudosan faces higher capital and operating costs to meet these demands.

To retain high-value occupants who can choose among developers, Mitsui Fudosan must upgrade assets—its FY2024 capital expenditure rose 12% to ¥198.6bn, reflecting this pressure.

Price sensitivity in the residential market

Individual homebuyers in Japan show high price sensitivity: mortgage rates rose from 0.20% in 2021 to ~0.55% in 2024, cutting buying power and lowering demand for ¥50–¥100M condominiums by an estimated 8–12% year-over-year.

Multiple developers (Mitsui Fudosan, Mitsubishi Estate, Sumitomo Realty) supply luxury condos, enabling buyers to compare units online and offline; listing price transparency has increased, with 65% of buyers using multi-site comparison in 2023.

That dynamic forces Mitsui Fudosan to justify premiums—often 5–15% above peers—through stronger branding, prime Tokyo and Osaka locations, and enhanced post-purchase services such as extended warranties and resident concierge programs.

Negotiating strength of major retail brands

Anchor tenants like international fashion houses and department stores wield strong bargaining power, often securing rent discounts of 10–30% and multi-year guarantees to anchor Mitsui Fudosan’s malls; in 2024 anchor-driven malls reported 18–25% higher footfall than non-anchored centers. Their presence lifts smaller-tenant occupancy rates—Mitsui’s retail portfolio hit 96% occupancy in FY2024—so Mitsui offers customized layouts and lease flex to retain them.

Institutional investor focus on ESG performance

Low switching costs for hotel and resort guests

Individual travelers face low switching costs and can change hotels quickly; global online travel agency bookings rose to 59% of room nights in 2024, increasing price transparency and comparison shopping.

Review sites and OTAs make alternatives visible: 82% of travelers used reviews to choose hotels in 2024, pressuring margins.

Mitsui Fudosan needs heavy spend on loyalty and differentiated experiences—expect loyalty investment to be 2–4% of revenue to defend share.

- Low switching costs—high choice

- 59% OTA share (2024)

- 82% use reviews (2024)

- Recommend loyalty spend 2–4% rev

Japan RE: Flexible-space surge, anchor discounts and ESG-driven net‑zero push

Large corporate tenants and anchor retailers hold strong bargaining power—flexible-space demand rose 18% in Japan (2024) and anchor tenants secure 10–30% rent discounts; Mitsui Fudosan’s FY2024 capex rose 12% to ¥198.6bn to meet specs. Individual condo buyers face higher mortgage rates (~0.55% in 2024), cutting demand ~8–12%, while 65% use multi-site comparison; ESG-focused investors (40%+ AUM, 2024) force net-zero targets across 1,300+ assets.

| Metric | 2024 Value |

|---|---|

| Flexible-space demand Japan | +18% YoY |

| Mitsui Fudosan FY2024 capex | ¥198.6bn (+12%) |

| Mortgage rate (Japan) | ~0.55% |

| Condo demand change | -8–12% YoY |

| Buyers using multi-site comparison | 65% |

| Anchor rent discounts | 10–30% |

| Retail occupancy (Mitsui FY2024) | 96% |

| Global real estate AUM using ESG | 40%+ |

| Assets under net-zero target | 1,300+ |

Preview Before You Purchase

Mitsui Fudosan Porter's Five Forces Analysis

This preview shows the exact Mitsui Fudosan Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or mockups.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Mitsui Fudosan faces moderate rivalry and high barriers from scale and land control, while buyer power is tempered by differentiated mixed-use developments and long-term leases; supplier influence varies by construction cycles and regulatory constraints, and threat of substitutes is limited but rising via remote work and retail shifts. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Mitsui Fudosan’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of major construction contractors

The Japanese construction market is concentrated: top 5 contractors (Kajima, Taisei, Obayashi, Shimizu, Takenaka) held about 35% of construction revenue in 2024, giving Mitsui Fudosan dependence on their capacity for mega-redevelopments.

These Super Zenikon firms provide unique technical expertise and can mobilize >50,000 workers and heavy equipment for Tokyo projects, so they command price and schedule leverage.

With Tokyo redevelopment investment above ¥3.2 trillion in 2024, contractor bargaining power rises, pressuring Mitsui Fudosan margins and procurement terms.

Limited availability of prime urban land

Landowners in Tokyo and other major Japanese CBDs hold strong leverage because developable urban land is finite; Tokyo’s 23 wards saw built-up area rise to 622 km² by 2023, tightening supply. Mitsui Fudosan must either outbid rivals—2024 land transaction prices in central Tokyo averaged about ¥1.2 million/m²—or form joint ventures with owners to secure sites. This scarcity keeps suppliers in a high bargaining position during acquisitions.

Persistent shortages in skilled construction labor

Japan’s working-age population fell 2.9% from 2015–2020 and shrank to 74.1m in 2024, creating a skilled construction labor shortfall that boosts bargaining power of subcontractors.

Specialized trades have seen wage growth ~4.5% YoY in 2023–24, letting labor providers demand higher pay and stricter terms.

For Mitsui Fudosan this raises project construction costs—estimates suggest 3–6% margin squeeze—and increases risk of schedule delays on large developments.

Fluctuations in global raw material prices

Suppliers of steel, cement and energy face global commodity swings and geopolitical risks; steel prices rose ~12% in 2024 and LNG spot prices jumped 40% in late 2023, so Mitsui Fudosan is exposed to input-cost shock passed through by contractors.

Long projects make margins vulnerable; Mitsui Fudosan must hedge, fix contracts, or index clauses to protect margins—construction cost inflation averaged 6–8% annually in Japan 2022–24.

- Steel +12% (2024)

- LNG spot +40% (late 2023)

- Construction inflation 6–8% (2022–24)

- Mitigations: hedges, fixed-price contracts, index clauses

Dependence on specialized technology providers

The shift to smart buildings and sustainable urban development raises Mitsui Fudosan’s dependence on tech firms supplying IoT and energy-management systems; Gartner estimated global smart building spending at $31.7B in 2024, up 12% YoY.

These suppliers deliver proprietary hardware and software that embed into asset value—upgrades can cost 1–3% of project value, tying Mitsui to niche vendors for compatibility and support.

A concentration of high-tech vendors creates supplier power, risking higher prices, slower innovation access, and integration lock‑in for future-proofing assets.

- Smart-building spend $31.7B (2024)

- Upgrade cost ~1–3% of asset value

- Proprietary systems cause vendor lock‑in

Suppliers’ leverage tightens Mitsui Fudosan margins as land, labor and inputs surge

Suppliers—large contractors, landowners, skilled labor, commodity and smart‑tech vendors—hold strong bargaining power versus Mitsui Fudosan, driven by contractor concentration (top 5 ≈35% market share, 2024), Tokyo land scarcity (central Tokyo ¥1.2M/m² avg, 2024), labor shortfall (74.1m working‑age, 2024) and input shocks (steel +12% 2024; LNG +40% late‑2023), squeezing margins ~3–6%.

| Metric | Value |

|---|---|

| Top5 contractors share | ≈35% (2024) |

| Tokyo land price | ¥1.2M/m² (2024) |

| Working‑age pop | 74.1M (2024) |

| Steel | +12% (2024) |

| LNG | +40% (late‑2023) |

What is included in the product

Tailored exclusively for Mitsui Fudosan, this Porter's Five Forces overview uncovers key drivers of competition, customer and supplier influence, market entry barriers, and disruptive substitutes that shape its pricing power and strategic positioning.

A concise, one-sheet Porter's Five Forces summary for Mitsui Fudosan—instantly highlights competitive pressures and real estate-specific risks for quick strategic decisions.

Customers Bargaining Power

Corporate demand for flexible office solutions

Large corporate tenants now demand flexible leases and high-spec offices for hybrid work; in Japan 2024 demand for flexible space grew 18% year-over-year, giving these clients strong bargaining power.

They push for amenities and green building certification (e.g., ZEB, CASBEE), and often secure rent premiums or fit-out contributions; Mitsui Fudosan faces higher capital and operating costs to meet these demands.

To retain high-value occupants who can choose among developers, Mitsui Fudosan must upgrade assets—its FY2024 capital expenditure rose 12% to ¥198.6bn, reflecting this pressure.

Price sensitivity in the residential market

Individual homebuyers in Japan show high price sensitivity: mortgage rates rose from 0.20% in 2021 to ~0.55% in 2024, cutting buying power and lowering demand for ¥50–¥100M condominiums by an estimated 8–12% year-over-year.

Multiple developers (Mitsui Fudosan, Mitsubishi Estate, Sumitomo Realty) supply luxury condos, enabling buyers to compare units online and offline; listing price transparency has increased, with 65% of buyers using multi-site comparison in 2023.

That dynamic forces Mitsui Fudosan to justify premiums—often 5–15% above peers—through stronger branding, prime Tokyo and Osaka locations, and enhanced post-purchase services such as extended warranties and resident concierge programs.

Negotiating strength of major retail brands

Anchor tenants like international fashion houses and department stores wield strong bargaining power, often securing rent discounts of 10–30% and multi-year guarantees to anchor Mitsui Fudosan’s malls; in 2024 anchor-driven malls reported 18–25% higher footfall than non-anchored centers. Their presence lifts smaller-tenant occupancy rates—Mitsui’s retail portfolio hit 96% occupancy in FY2024—so Mitsui offers customized layouts and lease flex to retain them.

Institutional investor focus on ESG performance

Low switching costs for hotel and resort guests

Individual travelers face low switching costs and can change hotels quickly; global online travel agency bookings rose to 59% of room nights in 2024, increasing price transparency and comparison shopping.

Review sites and OTAs make alternatives visible: 82% of travelers used reviews to choose hotels in 2024, pressuring margins.

Mitsui Fudosan needs heavy spend on loyalty and differentiated experiences—expect loyalty investment to be 2–4% of revenue to defend share.

- Low switching costs—high choice

- 59% OTA share (2024)

- 82% use reviews (2024)

- Recommend loyalty spend 2–4% rev

Japan RE: Flexible-space surge, anchor discounts and ESG-driven net‑zero push

Large corporate tenants and anchor retailers hold strong bargaining power—flexible-space demand rose 18% in Japan (2024) and anchor tenants secure 10–30% rent discounts; Mitsui Fudosan’s FY2024 capex rose 12% to ¥198.6bn to meet specs. Individual condo buyers face higher mortgage rates (~0.55% in 2024), cutting demand ~8–12%, while 65% use multi-site comparison; ESG-focused investors (40%+ AUM, 2024) force net-zero targets across 1,300+ assets.

| Metric | 2024 Value |

|---|---|

| Flexible-space demand Japan | +18% YoY |

| Mitsui Fudosan FY2024 capex | ¥198.6bn (+12%) |

| Mortgage rate (Japan) | ~0.55% |

| Condo demand change | -8–12% YoY |

| Buyers using multi-site comparison | 65% |

| Anchor rent discounts | 10–30% |

| Retail occupancy (Mitsui FY2024) | 96% |

| Global real estate AUM using ESG | 40%+ |

| Assets under net-zero target | 1,300+ |

Preview Before You Purchase

Mitsui Fudosan Porter's Five Forces Analysis

This preview shows the exact Mitsui Fudosan Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or mockups.