MMG Porter's Five Forces Analysis

Don't Miss the Bigger Picture

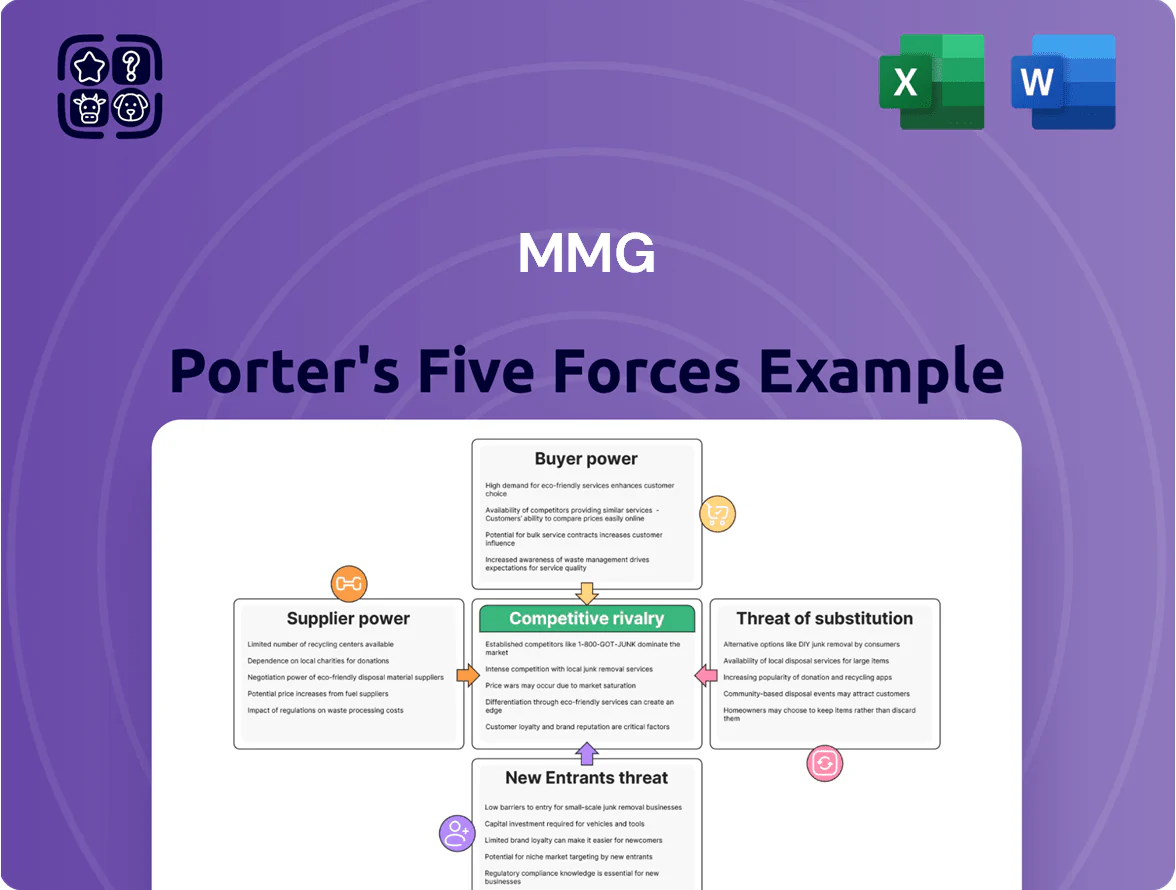

MMG faces a mix of concentrated supplier power, moderate buyer leverage, and elevated competitive rivalry driven by commodity price swings and global mining rivals; barriers to entry are high but substitute materials and ESG pressures create ongoing risk. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore MMG’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Energy and Fuel Dependency

Mining operations need huge diesel and electricity to run haul trucks and mills; MMG used ~1.2 million litres diesel/month at Rosebery in 2024 and 950 GWh/year electricity group-wide in 2024.

By end-2025, integrating renewables pushed MMG to contract with a few specialised green-energy providers; ~40% of new capacity came from third-party PPAs, concentrating supplier power.

Global energy price swings drive OPEX: a 30% diesel price rise in 2022-23 increased fuel spend by ~12% for MMG, showing suppliers—traditional and renewable—wield strong leverage.

Specialized Mining Equipment and Technology

The market for high-capacity mining trucks and automated extraction tech is concentrated among a few global firms—Caterpillar and Komatsu hold roughly 60–70% of large haul truck market share as of 2024—giving suppliers strong bargaining power.

Equipment’s specialization and required long-term maintenance contracts (often 5–10 years) raise MMG’s switching costs and dependence on vendor tech support and spare parts.

Labor Union Influence and Skilled Talent

The global shortage of skilled geologists, engineers and heavy-equipment operators in extractive industries tightened further in 2025, with ILO data showing vacancy rates for mining specialists up ~18% versus 2019, raising recruitment costs by roughly 12–20% for firms like MMG.

Strong unions in South America and Australia—where MMG operates—secured average wage uplifts of 6–10% in 2024–25, and collective actions raised operating disruption risk, increasing labour-related project contingencies by ~3–5%.

Scarcity gives workers and unions leverage to demand higher pay, safer conditions and training investments; for MMG this can translate into 5–15% higher unit labour costs and widened project capex forecasts.

Logistical and Infrastructure Providers

MMG depends on third-party rail, shipping and port operators to move bulk concentrates from remote mines to markets; in 2024 about 70–85% of MMG's shipments used external logistics in key jurisdictions.

These providers often act as regional monopolies or oligopolies, giving them high bargaining power and limited alternatives for MMG; rerouting costs can exceed 15–25% of logistics spend.

The suppliers' power is raised by the lack of substitute routes and by logistics being essential to revenue realization—delays can cut quarterly throughput by double digits.

- 70–85% external logistics dependency (2024)

- Regional monopoly/oligopoly providers

- Rerouting costs +15–25% of logistics spend

- Delays can drop quarterly throughput by 10%+

Consumables and Chemical Reagents

Consumables like flotation reagents, grinding media and explosives are critical for MMG’s copper and zinc mills; global supplier count is ample, but late-2025 local disruptions raised premium on secure contracts and lead-time guarantees.

Suppliers with strong logistics charged 5–12% price premiums in 2025; MMG’s risk from a 7–14 day supply outage can cut throughput 3–6% monthly, so long-term vendor ties trade cost for continuity.

- Multiple global suppliers, but 2025 local disruptions increased reliance on contracts

- Logistics-robust suppliers commanded 5–12% premiums in 2025

- 7–14 day outages can reduce mill throughput 3–6% per month

- MMG prioritizes supply security over spot-price savings

High supplier power: oligopolies, fuel & logistics drive rising costs and operational risk

Suppliers hold strong power: concentrated heavy-equipment makers (60–70% share), energy and logistics oligopolies (70–85% external reliance), skilled-labour scarcity (vacancies +18% vs 2019) and critical consumables with 5–12% premium in 2025 raise MMG’s costs and switching barriers, making supplier bargaining power high and operational risk material.

| Metric | 2024–25 |

|---|---|

| Diesel use (Rosebery) | 1.2M L/mo |

| Electricity | 950 GWh/yr |

| External logistics | 70–85% |

| Equipment market | 60–70% top two |

| Consumable premium | 5–12% |

What is included in the product

Tailored Porter's Five Forces analysis for MMG that uncovers competitive drivers, supplier and buyer power, entry barriers, substitute threats, and strategic levers to defend market share and profitability.

A concise, one-sheet MMG Porter's Five Forces summary that translates complex competitive dynamics into clear strategic actions for faster, board-ready decisions.

Customers Bargaining Power

Concentration of Smelting and Refining Capacity

A large share of MMG’s copper and zinc concentrate—around 60–70% in 2024—was sold to a handful of Chinese smelters, concentrating processing power and raising customer bargaining power.

These smelters set treatment and refining charges (TC/RCs); in 2024 average TC/RCs rose about 5–10% versus 2023, cutting MMG’s gross metal revenues materially.

Because smelters control the main route to market, they can demand lower payable rates and timing terms, directly reducing MMG’s net cash receipts.

Commodity Price Taker Status

As a producer of standardized base metals, MMG is a price taker tied to benchmarks like the London Metal Exchange (LME), where copper averaged 8,270 USD/t and zinc 2,900 USD/t in 2025 YTD; MMG must accept these market prices. Buyers have strong leverage because they can readily source equivalent 99.9% grade copper or 96% zinc from global suppliers, pressuring MMG on premiums and contract terms. Low product differentiation means MMG cannot materially influence LME prices, making revenue sensitive to shifts in global buyer sentiment and inventory cycles.

Strategic Influence of Chinese Offtake Agreements

MMG’s long-term offtake deals with China Minmetals and related state-linked buyers guarantee ~60–70% of annual zinc and copper volumes, giving MMG revenue visibility (2024 pro forma sales ~US$3.2bn) but concentrating customer bargaining power.

These buyers can push for price concessions, rigid delivery windows, and quality specs, trimming MMG’s margin upside—realized EBITDA margin fell to ~18% in 2024 versus 22% in 2022.

Contracts also align shipments with Chinese industrial demand and strategic stockpiling, seen in China’s 2023–24 copper imports rising 12% YoY, which forces MMG to prioritize state-linked schedules over spot-market opportunities.

Industrial Demand from the Green Transition

- EV/renewables drove >30% copper, >40% lithium demand growth by 2025

Availability of Alternative Supply Sources

Global buyers can source copper, zinc and lead from dozens of miners; in 2024 the top 10 miners supplied ~55% of refined copper, so buyers freely switch suppliers based on price and risk.

Choice grows with diverse jurisdictions; buyers reprice for geopolitical risk, shipping fees (ocean freight rose ~18% in 2021–24 for bulk metals) and ESG scores, increasing their leverage.

MMG must prove steady output and audited ethical sourcing—missed delivery or poor ESG ratings can cost contracts and move volumes to rivals.

- Top 10 miners ≈55% copper supply (2024)

- Ocean freight up ~18% (2021–24)

- Buyers shift on ESG and stability

- Operational reliability key to retain contracts

Chinese smelter dominance erodes MMG margins—buyers dictate tougher TC/RCs

Customers hold high bargaining power: ~60–70% of MMG’s 2024 copper/zinc sales flowed to a few Chinese smelters/offtakers, letting them raise TC/RCs ~5–10% in 2024 and cut MMG gross revenues; MMG is price-taker to LME (2025 YTD copper ~8,270 USD/t, zinc ~2,900 USD/t) and lost margin (EBITDA ~18% in 2024). Major buyers (state-linked + OEMs) can switch suppliers; top 10 miners supplied ~55% of copper in 2024, raising buyer leverage.

| Metric | Value |

|---|---|

| Share to Chinese smelters (2024) | 60–70% |

| TC/RC change (2024 vs 2023) | +5–10% |

| LME copper (2025 YTD) | 8,270 USD/t |

| LME zinc (2025 YTD) | 2,900 USD/t |

| MMG EBITDA (2024) | ~18% |

| Top10 miners share (2024) | ~55% |

Same Document Delivered

MMG Porter's Five Forces Analysis

This preview shows the exact MMG Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups; it's the final, professionally formatted document ready for download and use the moment you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

MMG faces a mix of concentrated supplier power, moderate buyer leverage, and elevated competitive rivalry driven by commodity price swings and global mining rivals; barriers to entry are high but substitute materials and ESG pressures create ongoing risk. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore MMG’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Energy and Fuel Dependency

Mining operations need huge diesel and electricity to run haul trucks and mills; MMG used ~1.2 million litres diesel/month at Rosebery in 2024 and 950 GWh/year electricity group-wide in 2024.

By end-2025, integrating renewables pushed MMG to contract with a few specialised green-energy providers; ~40% of new capacity came from third-party PPAs, concentrating supplier power.

Global energy price swings drive OPEX: a 30% diesel price rise in 2022-23 increased fuel spend by ~12% for MMG, showing suppliers—traditional and renewable—wield strong leverage.

Specialized Mining Equipment and Technology

The market for high-capacity mining trucks and automated extraction tech is concentrated among a few global firms—Caterpillar and Komatsu hold roughly 60–70% of large haul truck market share as of 2024—giving suppliers strong bargaining power.

Equipment’s specialization and required long-term maintenance contracts (often 5–10 years) raise MMG’s switching costs and dependence on vendor tech support and spare parts.

Labor Union Influence and Skilled Talent

The global shortage of skilled geologists, engineers and heavy-equipment operators in extractive industries tightened further in 2025, with ILO data showing vacancy rates for mining specialists up ~18% versus 2019, raising recruitment costs by roughly 12–20% for firms like MMG.

Strong unions in South America and Australia—where MMG operates—secured average wage uplifts of 6–10% in 2024–25, and collective actions raised operating disruption risk, increasing labour-related project contingencies by ~3–5%.

Scarcity gives workers and unions leverage to demand higher pay, safer conditions and training investments; for MMG this can translate into 5–15% higher unit labour costs and widened project capex forecasts.

Logistical and Infrastructure Providers

MMG depends on third-party rail, shipping and port operators to move bulk concentrates from remote mines to markets; in 2024 about 70–85% of MMG's shipments used external logistics in key jurisdictions.

These providers often act as regional monopolies or oligopolies, giving them high bargaining power and limited alternatives for MMG; rerouting costs can exceed 15–25% of logistics spend.

The suppliers' power is raised by the lack of substitute routes and by logistics being essential to revenue realization—delays can cut quarterly throughput by double digits.

- 70–85% external logistics dependency (2024)

- Regional monopoly/oligopoly providers

- Rerouting costs +15–25% of logistics spend

- Delays can drop quarterly throughput by 10%+

Consumables and Chemical Reagents

Consumables like flotation reagents, grinding media and explosives are critical for MMG’s copper and zinc mills; global supplier count is ample, but late-2025 local disruptions raised premium on secure contracts and lead-time guarantees.

Suppliers with strong logistics charged 5–12% price premiums in 2025; MMG’s risk from a 7–14 day supply outage can cut throughput 3–6% monthly, so long-term vendor ties trade cost for continuity.

- Multiple global suppliers, but 2025 local disruptions increased reliance on contracts

- Logistics-robust suppliers commanded 5–12% premiums in 2025

- 7–14 day outages can reduce mill throughput 3–6% per month

- MMG prioritizes supply security over spot-price savings

High supplier power: oligopolies, fuel & logistics drive rising costs and operational risk

Suppliers hold strong power: concentrated heavy-equipment makers (60–70% share), energy and logistics oligopolies (70–85% external reliance), skilled-labour scarcity (vacancies +18% vs 2019) and critical consumables with 5–12% premium in 2025 raise MMG’s costs and switching barriers, making supplier bargaining power high and operational risk material.

| Metric | 2024–25 |

|---|---|

| Diesel use (Rosebery) | 1.2M L/mo |

| Electricity | 950 GWh/yr |

| External logistics | 70–85% |

| Equipment market | 60–70% top two |

| Consumable premium | 5–12% |

What is included in the product

Tailored Porter's Five Forces analysis for MMG that uncovers competitive drivers, supplier and buyer power, entry barriers, substitute threats, and strategic levers to defend market share and profitability.

A concise, one-sheet MMG Porter's Five Forces summary that translates complex competitive dynamics into clear strategic actions for faster, board-ready decisions.

Customers Bargaining Power

Concentration of Smelting and Refining Capacity

A large share of MMG’s copper and zinc concentrate—around 60–70% in 2024—was sold to a handful of Chinese smelters, concentrating processing power and raising customer bargaining power.

These smelters set treatment and refining charges (TC/RCs); in 2024 average TC/RCs rose about 5–10% versus 2023, cutting MMG’s gross metal revenues materially.

Because smelters control the main route to market, they can demand lower payable rates and timing terms, directly reducing MMG’s net cash receipts.

Commodity Price Taker Status

As a producer of standardized base metals, MMG is a price taker tied to benchmarks like the London Metal Exchange (LME), where copper averaged 8,270 USD/t and zinc 2,900 USD/t in 2025 YTD; MMG must accept these market prices. Buyers have strong leverage because they can readily source equivalent 99.9% grade copper or 96% zinc from global suppliers, pressuring MMG on premiums and contract terms. Low product differentiation means MMG cannot materially influence LME prices, making revenue sensitive to shifts in global buyer sentiment and inventory cycles.

Strategic Influence of Chinese Offtake Agreements

MMG’s long-term offtake deals with China Minmetals and related state-linked buyers guarantee ~60–70% of annual zinc and copper volumes, giving MMG revenue visibility (2024 pro forma sales ~US$3.2bn) but concentrating customer bargaining power.

These buyers can push for price concessions, rigid delivery windows, and quality specs, trimming MMG’s margin upside—realized EBITDA margin fell to ~18% in 2024 versus 22% in 2022.

Contracts also align shipments with Chinese industrial demand and strategic stockpiling, seen in China’s 2023–24 copper imports rising 12% YoY, which forces MMG to prioritize state-linked schedules over spot-market opportunities.

Industrial Demand from the Green Transition

- EV/renewables drove >30% copper, >40% lithium demand growth by 2025

Availability of Alternative Supply Sources

Global buyers can source copper, zinc and lead from dozens of miners; in 2024 the top 10 miners supplied ~55% of refined copper, so buyers freely switch suppliers based on price and risk.

Choice grows with diverse jurisdictions; buyers reprice for geopolitical risk, shipping fees (ocean freight rose ~18% in 2021–24 for bulk metals) and ESG scores, increasing their leverage.

MMG must prove steady output and audited ethical sourcing—missed delivery or poor ESG ratings can cost contracts and move volumes to rivals.

- Top 10 miners ≈55% copper supply (2024)

- Ocean freight up ~18% (2021–24)

- Buyers shift on ESG and stability

- Operational reliability key to retain contracts

Chinese smelter dominance erodes MMG margins—buyers dictate tougher TC/RCs

Customers hold high bargaining power: ~60–70% of MMG’s 2024 copper/zinc sales flowed to a few Chinese smelters/offtakers, letting them raise TC/RCs ~5–10% in 2024 and cut MMG gross revenues; MMG is price-taker to LME (2025 YTD copper ~8,270 USD/t, zinc ~2,900 USD/t) and lost margin (EBITDA ~18% in 2024). Major buyers (state-linked + OEMs) can switch suppliers; top 10 miners supplied ~55% of copper in 2024, raising buyer leverage.

| Metric | Value |

|---|---|

| Share to Chinese smelters (2024) | 60–70% |

| TC/RC change (2024 vs 2023) | +5–10% |

| LME copper (2025 YTD) | 8,270 USD/t |

| LME zinc (2025 YTD) | 2,900 USD/t |

| MMG EBITDA (2024) | ~18% |

| Top10 miners share (2024) | ~55% |

Same Document Delivered

MMG Porter's Five Forces Analysis

This preview shows the exact MMG Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups; it's the final, professionally formatted document ready for download and use the moment you buy.