Hyundai Mobis Porter's Five Forces Analysis

From Overview to Strategy Blueprint

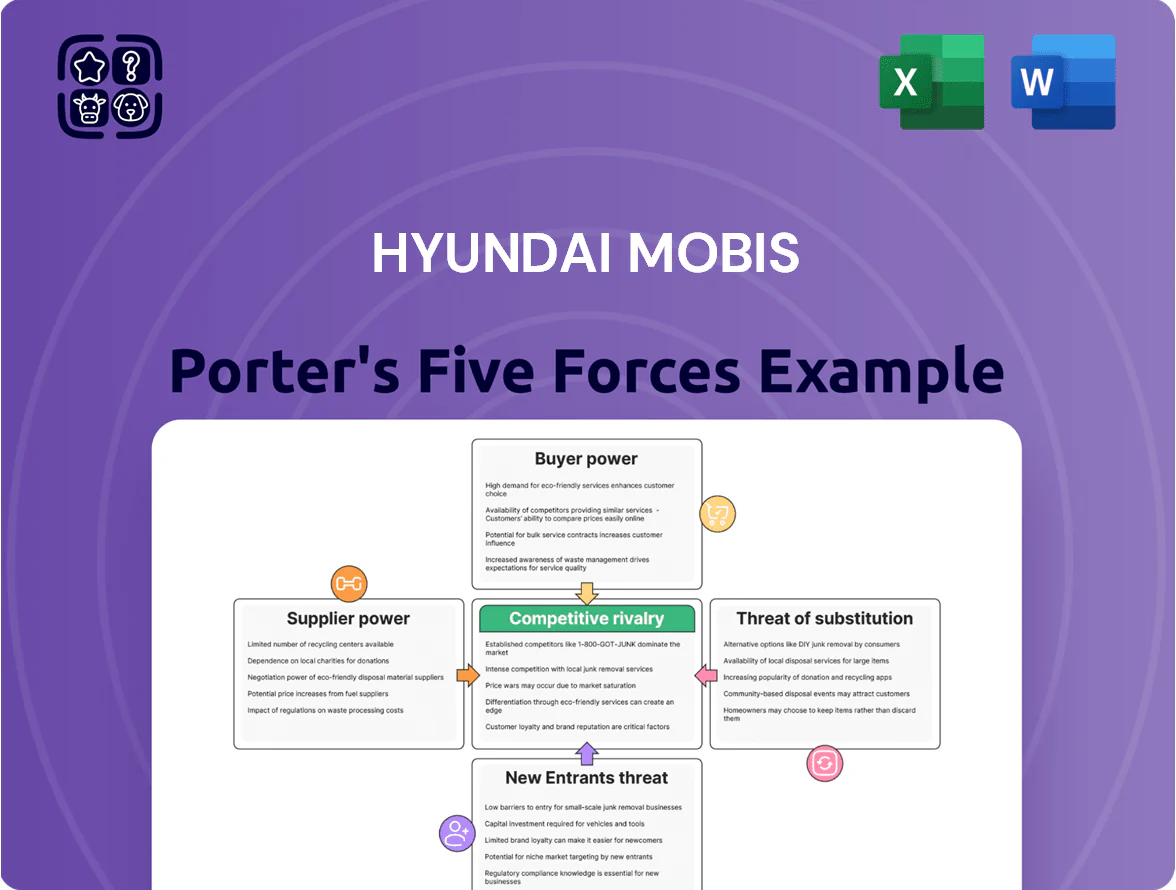

Hyundai Mobis faces moderate supplier leverage due to specialized components, intense rivalry from global auto-part suppliers, and growing buyer bargaining power as automakers push for integrated solutions and lower costs.

Emerging EV and software-focused entrants raise the threat of new competition and substitutes, while high regulatory and capital barriers partially protect incumbents—creating a complex strategic landscape.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Hyundai Mobis’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material price volatility

The cost of steel, aluminum and rare earths for battery components remains a price risk for Hyundai Mobis; steel rose ~18% in 2021–2022 and rare earth prices jumped over 30% in 2023, pressuring margins in 2024 when COGS ticked up ~4% year-over-year.

Hyundai Mobis’ scale—KRW 40+ trillion annual procurement (approx.)—gives leverage, but spot-market swings still affect short-term margins and EBITDA volatility.

The company uses 3–7 year fixed supply contracts and multi-region sourcing (Korea, China, Australia) plus alloy substitutes to limit single-supplier risk and smooth input-cost spikes.

Semiconductor dependency

The shift to Software Defined Vehicles raises Hyundai Mobis’s dependency on high-end chipmakers like NVIDIA and Qualcomm, who supplied ~70% of advanced ADAS/infotainment SoCs globally in 2024; this gives those suppliers strong bargaining power for price and delivery.

These specialized components are critical for L2+ autonomy and OTA systems, so supply constraints can delay model launches and add cost; Hyundai Mobis reported 2024 R&D spend of KRW 1.2 trillion to secure software-hardware integration.

To cut supplier leverage, Hyundai Mobis is scaling in-house chip and semiconductor design efforts—aiming to internalize key SoC IP and lower external procurement exposure by 15–25% over 2025–2027.

Specialized technology partnerships

Suppliers of niche electrification and hydrogen fuel-cell tech hold strong bargaining power for Hyundai Mobis due to scarce expertise and IP; global battery cell patents grew 18% y/y to ~56,000 filings in 2024, concentrating leverage with specialist firms. As automakers shift—EVs were 14% of global car sales in 2024—Mobis must partner with tech owners, raising supplier influence. Still, Mobis and partners are interdependent: Mobis’ 2024 R&D spend of KRW 1.2 trillion anchors joint innovation.

Tier 2 and Tier 3 fragmentation

Lower-tier suppliers of standard mechanical parts for Hyundai Mobis are highly fragmented, with thousands of small vendors globally, which weakens their bargaining power and lets Mobis leverage competition to cut prices.

Because these parts are commoditized, Mobis can switch suppliers quickly; in 2024 its procurement mix showed >60% of commodity spend concentrated in multi-sourced contracts, supporting price pressure and supply flexibility.

This fragmentation helps Mobis keep high efficiency in its traditional component chain, lowering COGS volatility and supporting margins in its Aftermarket and OE businesses.

- Thousands of small vendors → low supplier power

- Commoditized parts → easy switching, lower prices

- 2024: >60% commodity spend in multi-source contracts

- Result: reduced COGS volatility, stable margins

Vertical integration strategies

The Hyundai Motor Group ecosystem gives Hyundai Mobis internal supply synergies that cut external vendor leverage; in 2024 Mobis sourced roughly 52% of modules in‑house, lowering purchase volatility and costs.

By pulling more value‑chain functions into the group, Mobis sets technical standards and contract terms, improving margin control—gross margin rose to 11.8% in 2024.

This alignment buffers Mobis against external supplier pressure in a tight global market where semiconductor shortages pushed supplier leverage up in 2021–22.

- ~52% in‑house module sourcing (2024)

- Gross margin 11.8% (2024)

- Reduced external vendor bargaining

- Stronger internal standards and term control

Mobis scale + R&D cushions COGS volatility as chip/rare‑earth suppliers wield pricing power

Suppliers of advanced chips, rare earths and niche EV/hydrogen tech hold high bargaining power—chip suppliers supplied ~70% of ADAS SoCs in 2024 and battery patents rose 18% y/y—while commoditized parts remain weak; Mobis’ KRW 40+ trillion procurement scale, ~52% in‑house sourcing and KRW 1.2 trillion R&D (2024) lower external leverage and cut COGS volatility (gross margin 11.8% in 2024).

| Metric | 2024 |

|---|---|

| Procurement | KRW 40+ tn |

| In‑house modules | ~52% |

| R&D | KRW 1.2 tn |

| Gross margin | 11.8% |

What is included in the product

Tailored Porter's Five Forces analysis for Hyundai Mobis that uncovers competitive intensity, supplier and buyer power, substitute threats, and entry barriers—highlighting disruptive technologies, strategic vulnerabilities, and defenses that shape its profitability and market positioning.

A one-sheet Porter's Five Forces snapshot for Hyundai Mobis—instantly shows supplier, buyer, entrant, substitute, and rivalry pressures to speed strategic decisions and slide-ready board materials.

Customers Bargaining Power

Concentration of major buyers

About 55% of Hyundai Mobis revenue came from Hyundai Motor Company and Kia in 2024, creating high customer concentration that lets these buyers push for lower prices and stricter quality standards.

That leverage pressures Mobis margins—gross margin fell to 12.8% in 2024—so buyers can demand favorable terms and faster delivery windows.

Mobis is diversifying sales: by 2025 it aims to raise non-affiliated OEM revenue to roughly 30% via deals in Europe and North America, reducing concentrated buyer power.

Demand for cost reduction

Automakers push retail prices down and pass pressure to Tier-1s like Hyundai Mobis, which faced 3–5% annual price-reduction requests from major customers in 2024, per industry supplier surveys. Buyers often demand yearly cost cuts or productivity gains to protect their ~5–7% OEM operating margins, forcing Mobis to deliver efficiencies. Mobis therefore invests in automation and vertical integration—capital expenditure rose to KRW 1.2 trillion in 2024—to preserve profitability under tight pricing. This keeps margin expansion tied to process innovation and scale.

High switching costs for OEMs

High switching costs for OEMs mean once Mobis’s modular parts—like chassis modules or cockpit systems—are integrated into a platform, swapping suppliers can cost hundreds of millions and take 12–36 months, creating technical lock-in that shields Hyundai Mobis from abrupt customer exits.

The average vehicle model lifecycle of ~6–8 years and multi-year supplier contracts secured 2024 revenue stability: Mobis reported KRW 30.2 trillion in 2024 sales, supporting predictable cash flow from locked-in OEM relationships.

Strict quality and safety requirements

Customers force Hyundai Mobis to meet international safety standards and near-zero defect targets; failing this risks recalls—Kia/Hyundai group paid about $300m in recall-related costs in 2023—so buyers can cancel or renegotiate contracts.

That bargaining power compels Mobis to spend heavily: R&D rose to KRW 1.1 trillion in 2024 and quality control capital expenditures increased 18% year-over-year to reduce defect rates to under 0.5%.

- High buyer demands: zero-defect, global safety regs

- Recall risk: ~$300m group cost in 2023

- Capex/R&D: KRW 1.1T R&D (2024), QC capex +18% YoY

After-sales market influence

End-users and independent repair shops form distinct A/S customers; repair shops wield higher bargaining power because they buy in volume and often prefer cheaper third-party parts—aftermarket parts penetration in Korea reached ~28% in 2024, pressuring margins.

Mobis’s genuine parts brand and the rising complexity of vehicle electronics (ECUs, ADAS modules) keep switching costs high; genuine-part sales contributed ~38% of Mobis’s 2024 parts revenue, supporting pricing power.

Still, price-sensitive segments and online marketplaces give customers choice, limiting full margin capture for Mobis despite brand strength.

- Aftermarket share ~28% (Korea, 2024)

- Genuine parts ~38% of Mobis parts revenue (2024)

- Repair shops = higher bargaining power

- Electronics complexity raises switching costs

High Hyundai/Kia Dependence Shrinks Margins as Aftermarket Caps Pricing

High buyer concentration (Hyundai/Kia ≈55% revenue, 2024) gives strong bargaining power, squeezing margins (gross margin 12.8% in 2024) and forcing cost cuts (3–5% price reductions requested). Technical lock‑in (model life 6–8 yrs) and genuine parts (38% parts revenue) limit exits, while aftermarket share (~28% Korea, 2024) and online channels cap pricing.

| Metric | 2024 |

|---|---|

| Customer concentration | ≈55% |

| Gross margin | 12.8% |

| Genuine parts rev | 38% |

| Aftermarket (KR) | 28% |

What You See Is What You Get

Hyundai Mobis Porter's Five Forces Analysis

This preview shows the exact Hyundai Mobis Porter’s Five Forces analysis you’ll receive immediately after purchase—fully formatted, professionally written, and ready for use; no placeholders or mockups.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Hyundai Mobis faces moderate supplier leverage due to specialized components, intense rivalry from global auto-part suppliers, and growing buyer bargaining power as automakers push for integrated solutions and lower costs.

Emerging EV and software-focused entrants raise the threat of new competition and substitutes, while high regulatory and capital barriers partially protect incumbents—creating a complex strategic landscape.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Hyundai Mobis’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material price volatility

The cost of steel, aluminum and rare earths for battery components remains a price risk for Hyundai Mobis; steel rose ~18% in 2021–2022 and rare earth prices jumped over 30% in 2023, pressuring margins in 2024 when COGS ticked up ~4% year-over-year.

Hyundai Mobis’ scale—KRW 40+ trillion annual procurement (approx.)—gives leverage, but spot-market swings still affect short-term margins and EBITDA volatility.

The company uses 3–7 year fixed supply contracts and multi-region sourcing (Korea, China, Australia) plus alloy substitutes to limit single-supplier risk and smooth input-cost spikes.

Semiconductor dependency

The shift to Software Defined Vehicles raises Hyundai Mobis’s dependency on high-end chipmakers like NVIDIA and Qualcomm, who supplied ~70% of advanced ADAS/infotainment SoCs globally in 2024; this gives those suppliers strong bargaining power for price and delivery.

These specialized components are critical for L2+ autonomy and OTA systems, so supply constraints can delay model launches and add cost; Hyundai Mobis reported 2024 R&D spend of KRW 1.2 trillion to secure software-hardware integration.

To cut supplier leverage, Hyundai Mobis is scaling in-house chip and semiconductor design efforts—aiming to internalize key SoC IP and lower external procurement exposure by 15–25% over 2025–2027.

Specialized technology partnerships

Suppliers of niche electrification and hydrogen fuel-cell tech hold strong bargaining power for Hyundai Mobis due to scarce expertise and IP; global battery cell patents grew 18% y/y to ~56,000 filings in 2024, concentrating leverage with specialist firms. As automakers shift—EVs were 14% of global car sales in 2024—Mobis must partner with tech owners, raising supplier influence. Still, Mobis and partners are interdependent: Mobis’ 2024 R&D spend of KRW 1.2 trillion anchors joint innovation.

Tier 2 and Tier 3 fragmentation

Lower-tier suppliers of standard mechanical parts for Hyundai Mobis are highly fragmented, with thousands of small vendors globally, which weakens their bargaining power and lets Mobis leverage competition to cut prices.

Because these parts are commoditized, Mobis can switch suppliers quickly; in 2024 its procurement mix showed >60% of commodity spend concentrated in multi-sourced contracts, supporting price pressure and supply flexibility.

This fragmentation helps Mobis keep high efficiency in its traditional component chain, lowering COGS volatility and supporting margins in its Aftermarket and OE businesses.

- Thousands of small vendors → low supplier power

- Commoditized parts → easy switching, lower prices

- 2024: >60% commodity spend in multi-source contracts

- Result: reduced COGS volatility, stable margins

Vertical integration strategies

The Hyundai Motor Group ecosystem gives Hyundai Mobis internal supply synergies that cut external vendor leverage; in 2024 Mobis sourced roughly 52% of modules in‑house, lowering purchase volatility and costs.

By pulling more value‑chain functions into the group, Mobis sets technical standards and contract terms, improving margin control—gross margin rose to 11.8% in 2024.

This alignment buffers Mobis against external supplier pressure in a tight global market where semiconductor shortages pushed supplier leverage up in 2021–22.

- ~52% in‑house module sourcing (2024)

- Gross margin 11.8% (2024)

- Reduced external vendor bargaining

- Stronger internal standards and term control

Mobis scale + R&D cushions COGS volatility as chip/rare‑earth suppliers wield pricing power

Suppliers of advanced chips, rare earths and niche EV/hydrogen tech hold high bargaining power—chip suppliers supplied ~70% of ADAS SoCs in 2024 and battery patents rose 18% y/y—while commoditized parts remain weak; Mobis’ KRW 40+ trillion procurement scale, ~52% in‑house sourcing and KRW 1.2 trillion R&D (2024) lower external leverage and cut COGS volatility (gross margin 11.8% in 2024).

| Metric | 2024 |

|---|---|

| Procurement | KRW 40+ tn |

| In‑house modules | ~52% |

| R&D | KRW 1.2 tn |

| Gross margin | 11.8% |

What is included in the product

Tailored Porter's Five Forces analysis for Hyundai Mobis that uncovers competitive intensity, supplier and buyer power, substitute threats, and entry barriers—highlighting disruptive technologies, strategic vulnerabilities, and defenses that shape its profitability and market positioning.

A one-sheet Porter's Five Forces snapshot for Hyundai Mobis—instantly shows supplier, buyer, entrant, substitute, and rivalry pressures to speed strategic decisions and slide-ready board materials.

Customers Bargaining Power

Concentration of major buyers

About 55% of Hyundai Mobis revenue came from Hyundai Motor Company and Kia in 2024, creating high customer concentration that lets these buyers push for lower prices and stricter quality standards.

That leverage pressures Mobis margins—gross margin fell to 12.8% in 2024—so buyers can demand favorable terms and faster delivery windows.

Mobis is diversifying sales: by 2025 it aims to raise non-affiliated OEM revenue to roughly 30% via deals in Europe and North America, reducing concentrated buyer power.

Demand for cost reduction

Automakers push retail prices down and pass pressure to Tier-1s like Hyundai Mobis, which faced 3–5% annual price-reduction requests from major customers in 2024, per industry supplier surveys. Buyers often demand yearly cost cuts or productivity gains to protect their ~5–7% OEM operating margins, forcing Mobis to deliver efficiencies. Mobis therefore invests in automation and vertical integration—capital expenditure rose to KRW 1.2 trillion in 2024—to preserve profitability under tight pricing. This keeps margin expansion tied to process innovation and scale.

High switching costs for OEMs

High switching costs for OEMs mean once Mobis’s modular parts—like chassis modules or cockpit systems—are integrated into a platform, swapping suppliers can cost hundreds of millions and take 12–36 months, creating technical lock-in that shields Hyundai Mobis from abrupt customer exits.

The average vehicle model lifecycle of ~6–8 years and multi-year supplier contracts secured 2024 revenue stability: Mobis reported KRW 30.2 trillion in 2024 sales, supporting predictable cash flow from locked-in OEM relationships.

Strict quality and safety requirements

Customers force Hyundai Mobis to meet international safety standards and near-zero defect targets; failing this risks recalls—Kia/Hyundai group paid about $300m in recall-related costs in 2023—so buyers can cancel or renegotiate contracts.

That bargaining power compels Mobis to spend heavily: R&D rose to KRW 1.1 trillion in 2024 and quality control capital expenditures increased 18% year-over-year to reduce defect rates to under 0.5%.

- High buyer demands: zero-defect, global safety regs

- Recall risk: ~$300m group cost in 2023

- Capex/R&D: KRW 1.1T R&D (2024), QC capex +18% YoY

After-sales market influence

End-users and independent repair shops form distinct A/S customers; repair shops wield higher bargaining power because they buy in volume and often prefer cheaper third-party parts—aftermarket parts penetration in Korea reached ~28% in 2024, pressuring margins.

Mobis’s genuine parts brand and the rising complexity of vehicle electronics (ECUs, ADAS modules) keep switching costs high; genuine-part sales contributed ~38% of Mobis’s 2024 parts revenue, supporting pricing power.

Still, price-sensitive segments and online marketplaces give customers choice, limiting full margin capture for Mobis despite brand strength.

- Aftermarket share ~28% (Korea, 2024)

- Genuine parts ~38% of Mobis parts revenue (2024)

- Repair shops = higher bargaining power

- Electronics complexity raises switching costs

High Hyundai/Kia Dependence Shrinks Margins as Aftermarket Caps Pricing

High buyer concentration (Hyundai/Kia ≈55% revenue, 2024) gives strong bargaining power, squeezing margins (gross margin 12.8% in 2024) and forcing cost cuts (3–5% price reductions requested). Technical lock‑in (model life 6–8 yrs) and genuine parts (38% parts revenue) limit exits, while aftermarket share (~28% Korea, 2024) and online channels cap pricing.

| Metric | 2024 |

|---|---|

| Customer concentration | ≈55% |

| Gross margin | 12.8% |

| Genuine parts rev | 38% |

| Aftermarket (KR) | 28% |

What You See Is What You Get

Hyundai Mobis Porter's Five Forces Analysis

This preview shows the exact Hyundai Mobis Porter’s Five Forces analysis you’ll receive immediately after purchase—fully formatted, professionally written, and ready for use; no placeholders or mockups.