Mitsui OSK Lines Boston Consulting Group Matrix

Unlock Strategic Clarity

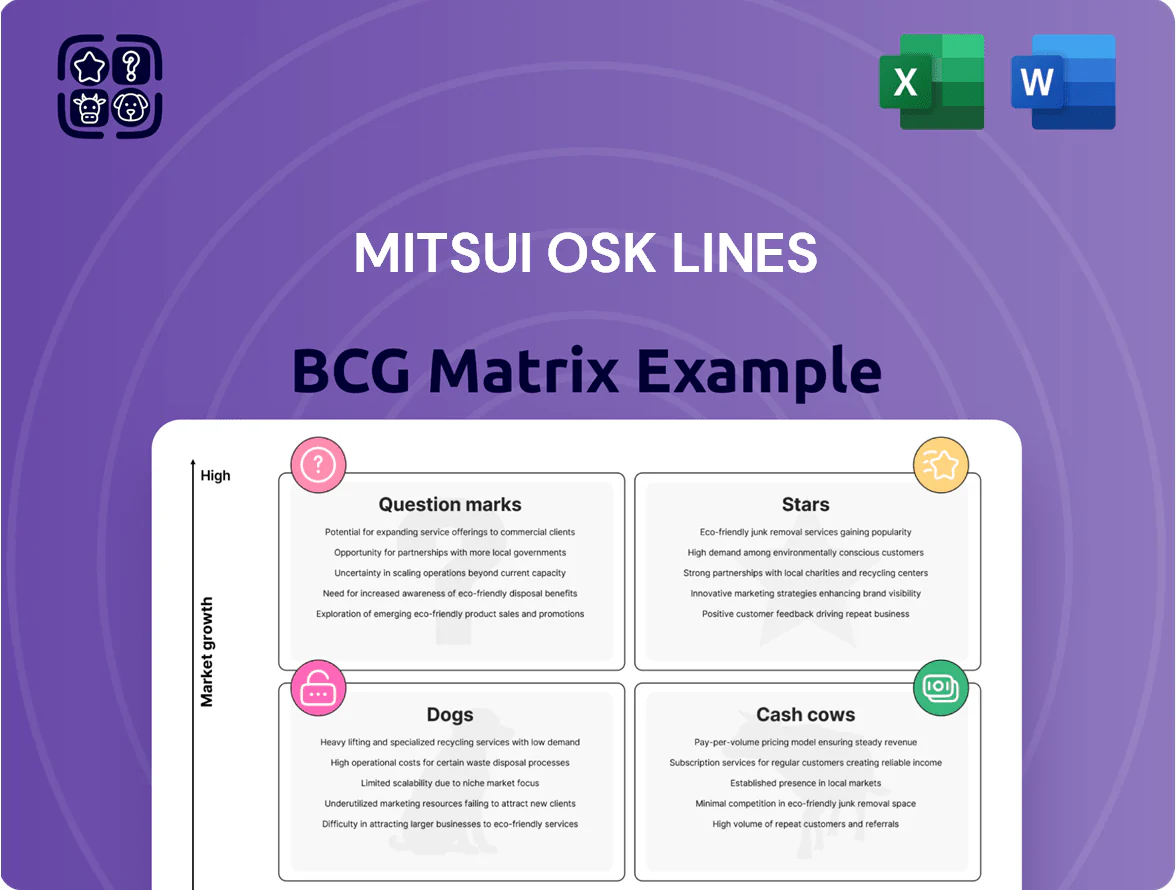

Mitsui O.S.K. Lines' BCG Matrix preview highlights how its core segments—container shipping, bulk carriers, LNG, and logistics—stack up on market growth and relative share, revealing potential Stars and Cash Cows amid industry consolidation and decarbonization pressure. Our snapshot points to high-growth opportunities in LNG and logistics, while certain bulk operations may be Question Marks requiring strategic investment or divestment. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

LNG Transport Services

MOL (Mitsui O.S.K. Lines) holds a top global LNG carrier share near 12% in 2024, keeping LNG transport a Star through 2025 as gas stays a transition fuel; IEA projects global LNG demand up 3.5% in 2025.

Long-term charters with majors like Shell and TotalEnergies cover ~60% of MOL’s LNG fleet revenue through 2027, giving high visibility; Q3 2024 LNG transport EBIT margin averaged ~18%.

Capital spend of JPY 120 billion in 2023–25 targets next-gen low‑emission ME-GI and ammonia-ready carriers, reinforcing MOL as preferred partner for energy security projects.

Car Carrier Business

Car Carrier Business is a Star: high growth and high share as EV adoption drove automotive shipping growth ~8–10% CAGR to 2025, sustaining demand; MOL runs one of the world’s largest PCC fleets (~150 vessels) and reported car carrier revenues ¥200bn in FY2024.

MOL has shifted aggressively to LNG propulsion—about 30 LNG-capable car carriers by end-2025—cutting CO2/SOx to meet IMO rules, but the segment needs continuous capex: estimated $500–700m fleet renewals 2026–28 for larger, heavier BEV loads.

Offshore Wind Support

As a leader in renewables, Mitsui OSK Lines (MOL) has built a strong foothold in offshore wind support, operating specialized vessels and service platforms that address Japan and Asia's rapid decarbonization push.

The Asian offshore wind market is growing fast: Japan aims for 45 GW by 2040 and Asia-Pacific installed capacity reached 9.2 GW in 2024, boosting demand for service vessels.

These operations need heavy upfront capex—vessel unit costs often exceed $60–80m—but offer high revenue growth; MOL reported renewable-related revenue rising ~28% year-on-year in FY2024, showing a first-mover edge.

Ammonia and Hydrogen Carriers

MOL leads transport of ammonia and hydrogen carriers, targeting the clean-fuels market projected to reach $200bn by 2030 (IEA, 2024); MOL’s strategic JV with Kawasaki and Chiyoda gives >30% share in ammonia carrier development as of 2025.

Although scalability is ongoing, this high-growth niche drives MOL’s future revenue—company guidance forecasts clean-fuel-related EBITDA growth of 15–20% CAGR through 2028.

- Market size: ~$200bn by 2030 (IEA 2024)

- MOL share: >30% in ammonia carrier projects (2025)

- EBITDA growth: 15–20% CAGR in clean fuels (guidance to 2028)

- Key partners: Kawasaki, Chiyoda (strategic JVs)

FSRU Operations

FSRU Operations: Floating Storage and Regasification Units (FSRUs) offer fast LNG-to-gas capacity growth; global FSRU capacity reached ~90 mtpa in 2024, growing ~6% YoY, and MOL operates multiple units, holding roughly 8–10% of the deployed FSRU fleet as of Dec 2024.

The unit posts high EBITDA margins—industry peers report 25–35%—but requires capex of $200–400m per new FSRU and elevated OPEX for maintenance and regulatory compliance when entering new regions.

Market dynamics: rising LNG demand in Asia and emerging markets, plus FSRU lead times of 12–24 months, keep growth prospects strong while tying up capital and project risk for MOL.

- High growth: ~6% global FSRU capacity growth 2023–24

- MOL share: ~8–10% of active FSRU fleet (Dec 2024)

- Returns: EBITDA margins ~25–35%

- Capex: $200–400m per FSRU; deployment lead time 12–24 months

MOL’s growth engines: LNG, car carriers, offshore wind & ammonia/H2 — high margins, big capex

MOL’s Stars: LNG (12% global share in 2024), Car Carriers (≈150 PCCs; ¥200bn revenue FY2024), Offshore Wind services (renewables revenue +28% YoY FY2024), Ammonia/H2 carriers (>30% JV share 2025). High margins (LNG EBIT ~18% Q3 2024; FSRU peers 25–35%), heavy capex (JPY120bn 2023–25; $500–700m PCC renewals 2026–28; $200–400m per FSRU).

| Segment | 2024–25 Metrics |

|---|---|

| LNG | 12% share; EBIT ~18% |

| Car Carriers | ≈150 vessels; ¥200bn rev |

| Offshore Wind | Renewables rev +28% YoY |

| Ammonia/H2 | >30% JV share; market $200bn by 2030 |

What is included in the product

BCG Matrix analysis of Mitsui O.S.K. Lines: strategic guidance on Stars, Cash Cows, Question Marks, Dogs with investment, hold, divest recommendations.

One-page overview placing each Mitsui OSK Lines business unit in a BCG quadrant for quick strategic clarity.

Cash Cows

Dry Bulk Fleet

The dry bulk segment is a mature market where Mitsui O.S.K. Lines (MOL) holds a substantial, stable share in transporting iron ore, coal, and grain, contributing roughly ¥120–140 billion in annual EBITDA-equivalent cash flow for the group in 2024.

Growth is low—CAGR near 1–2%—but steady demand keeps utilisation high, letting MOL use surplus cash to fund greener initiatives like ammonia-ready retrofits and green fuel trials.

Digital fleet management and voyage optimisation cut voyage costs by about 5–8% and improved charter margins in 2023–24, boosting free cash flow and sustaining this division as a true cash cow.

Crude Oil Tankers

Mitsui OSK Lines (MOL) operates a large, efficient fleet of Very Large Crude Carriers (VLCCs), with ~40 VLCCs and 12% share of global VLCC capacity as of 2024, serving major oil routes and generating stable charter revenue.

Despite energy transition risks that cap long-term growth, VLCCs delivered ¥85–95 billion in operating cash flow to MOL in FY2023–FY2024, underpinning steady dividends to shareholders.

Management treats crude oil tankers as a cash cow: prioritizing high utilization and dividend extraction while minimizing capex on new oil-only tonnage and redeploying free cash to LNG and ammonia investments.

Real Estate Business

Through subsidiary Daibiru Corporation, Mitsui OSK Lines (MOL) holds ~450,000 m2 of office and retail space in Tokyo and Osaka, yielding stable rents that produced ¥28.7 billion in FY2024 non-shipping revenue for MOL Group.

The real estate arm sits in a mature, low-growth market but delivers predictable cash flow—occupancy 95% in 2024—helping MOL cover fixed costs and shore up liquidity during shipping downturns.

Domestic Ferry and Ro-Ro

MOL dominates Japan’s domestic ferry and Ro-Ro market, serving key routes between Honshu, Hokkaido, Kyushu, and Shikoku and holding an estimated market share ~40% as of 2025; annual ferry segment revenue ~¥35–45 billion (FY2024) provides steady cash flow.

The sector is mature with low growth (<1% CAGR projected 2025–2030) but high entry barriers (port slots, regulatory safety, fleet capex), keeping MOL’s share stable and margins resilient.

Operating cash returns are strong due to predictable demand and low marketing needs; fleet renewal capex is the main ongoing expense, supporting free cash flow in MOL’s consolidated results.

- Market share ~40% (2025)

- Segment revenue ¥35–45B (FY2024)

- Growth <1% CAGR (2025–2030)

- Main capex: fleet renewal

- Low marketing, high stability

Ocean Network Express Equity

MOL investment in Ocean Network Express (ONE) has become a cash cow: ONE reported operating income of $5.1 billion in 2023 for owners (industry source) and MOL’s equity stake generated roughly JPY 45–60 billion in annual investment income in 2022–2024, backing steady dividends amid a consolidated container market.

With container shipping now mature after 2020–22 volatility, ONE’s high market share (~12% global TEU capacity in 2024) provides predictable cash flow that MOL redirects to fund its strategic shift into energy and offshore services.

- ONE ~12% global TEU capacity (2024)

- MOL equity income ~JPY 45–60bn annually (2022–24)

- ONE operating income proxy $5.1bn (2023)

- Funds used to finance MOL pivot to energy/offshore

MOL’s cash cows (~¥300–360B) fund LNG/ammonia pivot as utilization stays high

MOL’s cash cows (dry bulk, VLCCs, real estate, domestic ferries, ONE) generated ~¥300–360B EBITDA-equivalent cash flow in 2023–24, with VLCCs ¥85–95B, dry bulk ¥120–140B, ONE equity income ¥45–60B, real estate ¥28.7B, ferries ¥35–45B; low growth (0–2% CAGR), high utilization, surplus redeployed to LNG/ammonia investments.

| Segment | Cash flow (¥B) | Share |

|---|---|---|

| Dry bulk | 120–140 | ~35–40% |

| VLCCs | 85–95 | ~25–30% |

| ONE | 45–60 | ~15–18% |

| Real estate | 28.7 | ~8–10% |

| Ferries | 35–45 | ~10–12% |

What You See Is What You Get

Mitsui OSK Lines BCG Matrix

The file you're previewing on this page is the final Mitsui O.S.K. Lines BCG Matrix you'll receive after purchase—no watermarks, no demo placeholders—just a fully formatted, strategy-ready report built for clarity and professional use. This preview mirrors the exact document delivered post-purchase, crafted with market-backed analysis and ready for immediate editing, printing, or presentation. Once bought, the full file is instantly downloadable and can be used in client decks, internal planning, or investor discussions without further changes.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

Mitsui O.S.K. Lines' BCG Matrix preview highlights how its core segments—container shipping, bulk carriers, LNG, and logistics—stack up on market growth and relative share, revealing potential Stars and Cash Cows amid industry consolidation and decarbonization pressure. Our snapshot points to high-growth opportunities in LNG and logistics, while certain bulk operations may be Question Marks requiring strategic investment or divestment. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

LNG Transport Services

MOL (Mitsui O.S.K. Lines) holds a top global LNG carrier share near 12% in 2024, keeping LNG transport a Star through 2025 as gas stays a transition fuel; IEA projects global LNG demand up 3.5% in 2025.

Long-term charters with majors like Shell and TotalEnergies cover ~60% of MOL’s LNG fleet revenue through 2027, giving high visibility; Q3 2024 LNG transport EBIT margin averaged ~18%.

Capital spend of JPY 120 billion in 2023–25 targets next-gen low‑emission ME-GI and ammonia-ready carriers, reinforcing MOL as preferred partner for energy security projects.

Car Carrier Business

Car Carrier Business is a Star: high growth and high share as EV adoption drove automotive shipping growth ~8–10% CAGR to 2025, sustaining demand; MOL runs one of the world’s largest PCC fleets (~150 vessels) and reported car carrier revenues ¥200bn in FY2024.

MOL has shifted aggressively to LNG propulsion—about 30 LNG-capable car carriers by end-2025—cutting CO2/SOx to meet IMO rules, but the segment needs continuous capex: estimated $500–700m fleet renewals 2026–28 for larger, heavier BEV loads.

Offshore Wind Support

As a leader in renewables, Mitsui OSK Lines (MOL) has built a strong foothold in offshore wind support, operating specialized vessels and service platforms that address Japan and Asia's rapid decarbonization push.

The Asian offshore wind market is growing fast: Japan aims for 45 GW by 2040 and Asia-Pacific installed capacity reached 9.2 GW in 2024, boosting demand for service vessels.

These operations need heavy upfront capex—vessel unit costs often exceed $60–80m—but offer high revenue growth; MOL reported renewable-related revenue rising ~28% year-on-year in FY2024, showing a first-mover edge.

Ammonia and Hydrogen Carriers

MOL leads transport of ammonia and hydrogen carriers, targeting the clean-fuels market projected to reach $200bn by 2030 (IEA, 2024); MOL’s strategic JV with Kawasaki and Chiyoda gives >30% share in ammonia carrier development as of 2025.

Although scalability is ongoing, this high-growth niche drives MOL’s future revenue—company guidance forecasts clean-fuel-related EBITDA growth of 15–20% CAGR through 2028.

- Market size: ~$200bn by 2030 (IEA 2024)

- MOL share: >30% in ammonia carrier projects (2025)

- EBITDA growth: 15–20% CAGR in clean fuels (guidance to 2028)

- Key partners: Kawasaki, Chiyoda (strategic JVs)

FSRU Operations

FSRU Operations: Floating Storage and Regasification Units (FSRUs) offer fast LNG-to-gas capacity growth; global FSRU capacity reached ~90 mtpa in 2024, growing ~6% YoY, and MOL operates multiple units, holding roughly 8–10% of the deployed FSRU fleet as of Dec 2024.

The unit posts high EBITDA margins—industry peers report 25–35%—but requires capex of $200–400m per new FSRU and elevated OPEX for maintenance and regulatory compliance when entering new regions.

Market dynamics: rising LNG demand in Asia and emerging markets, plus FSRU lead times of 12–24 months, keep growth prospects strong while tying up capital and project risk for MOL.

- High growth: ~6% global FSRU capacity growth 2023–24

- MOL share: ~8–10% of active FSRU fleet (Dec 2024)

- Returns: EBITDA margins ~25–35%

- Capex: $200–400m per FSRU; deployment lead time 12–24 months

MOL’s growth engines: LNG, car carriers, offshore wind & ammonia/H2 — high margins, big capex

MOL’s Stars: LNG (12% global share in 2024), Car Carriers (≈150 PCCs; ¥200bn revenue FY2024), Offshore Wind services (renewables revenue +28% YoY FY2024), Ammonia/H2 carriers (>30% JV share 2025). High margins (LNG EBIT ~18% Q3 2024; FSRU peers 25–35%), heavy capex (JPY120bn 2023–25; $500–700m PCC renewals 2026–28; $200–400m per FSRU).

| Segment | 2024–25 Metrics |

|---|---|

| LNG | 12% share; EBIT ~18% |

| Car Carriers | ≈150 vessels; ¥200bn rev |

| Offshore Wind | Renewables rev +28% YoY |

| Ammonia/H2 | >30% JV share; market $200bn by 2030 |

What is included in the product

BCG Matrix analysis of Mitsui O.S.K. Lines: strategic guidance on Stars, Cash Cows, Question Marks, Dogs with investment, hold, divest recommendations.

One-page overview placing each Mitsui OSK Lines business unit in a BCG quadrant for quick strategic clarity.

Cash Cows

Dry Bulk Fleet

The dry bulk segment is a mature market where Mitsui O.S.K. Lines (MOL) holds a substantial, stable share in transporting iron ore, coal, and grain, contributing roughly ¥120–140 billion in annual EBITDA-equivalent cash flow for the group in 2024.

Growth is low—CAGR near 1–2%—but steady demand keeps utilisation high, letting MOL use surplus cash to fund greener initiatives like ammonia-ready retrofits and green fuel trials.

Digital fleet management and voyage optimisation cut voyage costs by about 5–8% and improved charter margins in 2023–24, boosting free cash flow and sustaining this division as a true cash cow.

Crude Oil Tankers

Mitsui OSK Lines (MOL) operates a large, efficient fleet of Very Large Crude Carriers (VLCCs), with ~40 VLCCs and 12% share of global VLCC capacity as of 2024, serving major oil routes and generating stable charter revenue.

Despite energy transition risks that cap long-term growth, VLCCs delivered ¥85–95 billion in operating cash flow to MOL in FY2023–FY2024, underpinning steady dividends to shareholders.

Management treats crude oil tankers as a cash cow: prioritizing high utilization and dividend extraction while minimizing capex on new oil-only tonnage and redeploying free cash to LNG and ammonia investments.

Real Estate Business

Through subsidiary Daibiru Corporation, Mitsui OSK Lines (MOL) holds ~450,000 m2 of office and retail space in Tokyo and Osaka, yielding stable rents that produced ¥28.7 billion in FY2024 non-shipping revenue for MOL Group.

The real estate arm sits in a mature, low-growth market but delivers predictable cash flow—occupancy 95% in 2024—helping MOL cover fixed costs and shore up liquidity during shipping downturns.

Domestic Ferry and Ro-Ro

MOL dominates Japan’s domestic ferry and Ro-Ro market, serving key routes between Honshu, Hokkaido, Kyushu, and Shikoku and holding an estimated market share ~40% as of 2025; annual ferry segment revenue ~¥35–45 billion (FY2024) provides steady cash flow.

The sector is mature with low growth (<1% CAGR projected 2025–2030) but high entry barriers (port slots, regulatory safety, fleet capex), keeping MOL’s share stable and margins resilient.

Operating cash returns are strong due to predictable demand and low marketing needs; fleet renewal capex is the main ongoing expense, supporting free cash flow in MOL’s consolidated results.

- Market share ~40% (2025)

- Segment revenue ¥35–45B (FY2024)

- Growth <1% CAGR (2025–2030)

- Main capex: fleet renewal

- Low marketing, high stability

Ocean Network Express Equity

MOL investment in Ocean Network Express (ONE) has become a cash cow: ONE reported operating income of $5.1 billion in 2023 for owners (industry source) and MOL’s equity stake generated roughly JPY 45–60 billion in annual investment income in 2022–2024, backing steady dividends amid a consolidated container market.

With container shipping now mature after 2020–22 volatility, ONE’s high market share (~12% global TEU capacity in 2024) provides predictable cash flow that MOL redirects to fund its strategic shift into energy and offshore services.

- ONE ~12% global TEU capacity (2024)

- MOL equity income ~JPY 45–60bn annually (2022–24)

- ONE operating income proxy $5.1bn (2023)

- Funds used to finance MOL pivot to energy/offshore

MOL’s cash cows (~¥300–360B) fund LNG/ammonia pivot as utilization stays high

MOL’s cash cows (dry bulk, VLCCs, real estate, domestic ferries, ONE) generated ~¥300–360B EBITDA-equivalent cash flow in 2023–24, with VLCCs ¥85–95B, dry bulk ¥120–140B, ONE equity income ¥45–60B, real estate ¥28.7B, ferries ¥35–45B; low growth (0–2% CAGR), high utilization, surplus redeployed to LNG/ammonia investments.

| Segment | Cash flow (¥B) | Share |

|---|---|---|

| Dry bulk | 120–140 | ~35–40% |

| VLCCs | 85–95 | ~25–30% |

| ONE | 45–60 | ~15–18% |

| Real estate | 28.7 | ~8–10% |

| Ferries | 35–45 | ~10–12% |

What You See Is What You Get

Mitsui OSK Lines BCG Matrix

The file you're previewing on this page is the final Mitsui O.S.K. Lines BCG Matrix you'll receive after purchase—no watermarks, no demo placeholders—just a fully formatted, strategy-ready report built for clarity and professional use. This preview mirrors the exact document delivered post-purchase, crafted with market-backed analysis and ready for immediate editing, printing, or presentation. Once bought, the full file is instantly downloadable and can be used in client decks, internal planning, or investor discussions without further changes.