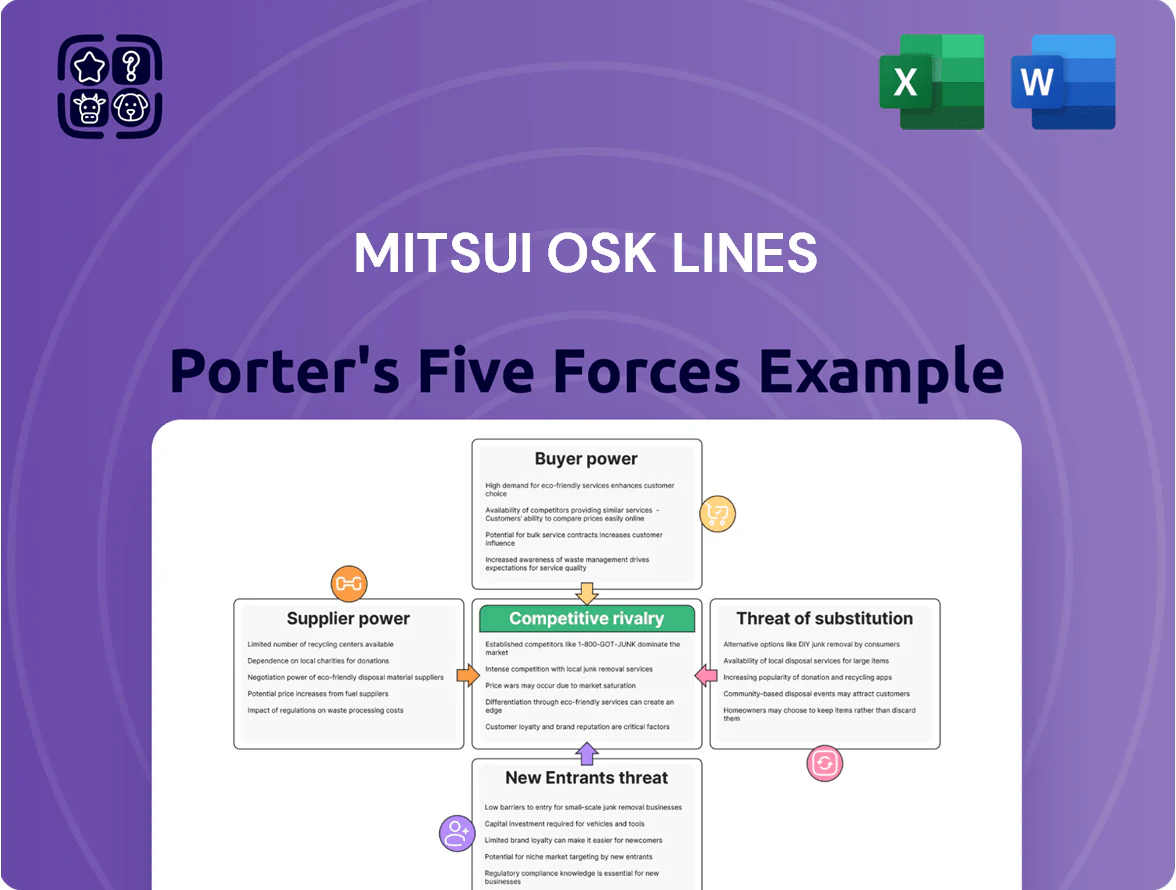

Mitsui OSK Lines Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Mitsui OSK Lines faces intense rivalry from global shipping giants and asset-heavy competitors, while moderate buyer power and rising fuel and regulatory costs squeeze margins; technological shifts and decarbonization create both threat and opportunity.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Mitsui OSK Lines’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Specialized Shipyards

The high-tech vessel market is concentrated: three South Korean builders (Hyundai Heavy, Samsung Heavy, Daewoo) plus top Chinese (Dalian, Hudong) and Japanese yards account for ~70–80% of LNG and green-ship newbuild capacity as of 2025, giving suppliers price and slot leverage over Mitsui OSK Lines.

As MOL shifts to zero-emission and LNG carriers by late 2025, orderbook bottlenecks matter: global green-fuel newbuild slots had ~24–30 month wait times in 2024–25, pushing yards’ negotiating power on price and delivery.

Specialized berth scarcity for ammonia/LNG-ready ships keeps switching costs high; retrofit and dedicated berth investments raised capex per ship by an estimated $20–50m versus conventional builds in 2024, reinforcing suppliers’ strong bargaining position.

Energy and Fuel Provider Dependency

MOL depends on global energy markets for bunker fuel and rising demand for ammonia/methanol; in 2024 fuel costs made up ~22% of operating expenses for large carriers, so suppliers hold pricing leverage. Long-term procurement deals reduce exposure, but 2022–24 oil price swings (Brent ranged $70–120/barrel) showed suppliers can tighten terms via geopolitical shifts. Cleaner-fuel rollout shrinks the supplier pool to firms with ammonia/methanol production and bunkering—raising switching costs and supplier power.

Specialized Technology and Engine Manufacturers

The shift to decarbonization gives a few engine and carbon-capture patent holders strong leverage: these firms control high-efficiency engines and CCGT (carbon capture and storage for ships) kits needed to meet IMO 2030/2050 rules, so supplier power is high. In 2024, only ~5 manufacturers supplied >70% of dual-fuel and methanol-capable marine engines, limiting MOL’s options and raising unit costs and delivery risk for its newbuilds.

Labor Unions and Seafarer Shortages

A tightening global market for skilled maritime officers and crew boosts supplier power: unions and manning agencies command stronger bargaining positions as experienced seafarers grow scarce.

Operating LNG and ammonia carriers needs specialized training and certifications, so retaining qualified personnel raises crew costs and turnover risk for Mitsui OSK Lines (MOL).

By 2025 shortages let labor providers press for higher wages and benefits; IMO data and industry reports show officer deficits up to 15–20% in key pools, pushing crew cost premiums of roughly 10–25%.

- Skilled-officer scarcity: +15–20% (2025)

- Crew cost premium: +10–25% vs 2019

- Higher retention spend: specialized training, bonuses

- Unions/agencies: increased leverage on wage/benefit terms

Port and Terminal Operator Influence

Global port congestion and just ~200 deep-water terminals worldwide that can handle 24k+ TEU mega-vessels give terminal operators outsized leverage over Mitsui O.S.K. Lines (MOL), forcing higher berthing fees and priority bidding to keep schedules intact.

MOL needs guaranteed priority access and sub-24-hour turnarounds in hubs like Shanghai, Rotterdam, and Singapore; delays cost container carriers ~$100–200 per box per day in 2024 estimates, squeezing margins.

In many strategic hubs, scarce alternative berths leave MOL accepting operator fee structures and demurrage rules, raising voyage costs and reducing routing flexibility.

- ~200 global deep-water mega-terminals

- $100–200 per TEU/day delay cost (2024 est.)

- Priority berth + <24h turnaround = critical

- Limited alternatives → weak supplier bargaining

Suppliers Dictate Shipping Costs: Concentrated Yards, Engine Oligopoly & Soaring Delays

Suppliers hold high bargaining power: concentrated green-newbuild yards (70–80% share), 24–30 month slot waits (2024–25), dual-fuel engine oligopoly (~5 makers >70% share in 2024), fuel = ~22% of OPEX (2024), officer shortages +15–20% (2025) and ~200 deep-water mega-terminals driving berth fees and delays ($100–200/TEU/day, 2024).

| Metric | Value |

|---|---|

| Yard concentration | 70–80% |

| Slot wait | 24–30 months |

| Engine suppliers | ~5 firms >70% |

| Fuel share OPEX | ~22% (2024) |

| Officer shortage | +15–20% (2025) |

| Delay cost | $100–200/TEU/day (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Mitsui OSK Lines highlighting competitive rivalry, buyer and supplier power, threats from new entrants and substitutes, and strategic barriers that protect its shipping, logistics, and offshore businesses.

Concise Porter's Five Forces summary for Mitsui O.S.K. Lines—quickly assess competitive intensity and strategic levers to relieve decision-making pain points.

Customers Bargaining Power

Consolidation of Global Shippers

Large retail, automotive and energy clients control concentrated volumes—top 20 shippers accounted for ~35% of container demand in 2024—letting them press Mitsui O.S.K. Lines (MOL) for price cuts or better terms by threatening reallocation.

These power buyers pushed average contract rates down an estimated 8–12% in 2024–25 versus spot peaks, directly squeezing MOL’s EBITDA margins; by end-2025 this buyer leverage remained a primary margin headwind.

Low Switching Costs in Standardized Shipping

For commoditized services like dry bulk and standard container transport, customers can switch carriers easily based on price and schedule; global container spot rates fell 42% year-over-year in 2024, increasing price sensitivity.

Moving goods A to B is seen as a commodity, so brand loyalty is secondary to cost-efficiency; MOL reported a 2024 containership revenue decline of 8% in some trade lanes.

This low switching cost forces Mitsui O.S.K. Lines to cut prices or innovate—MOL invested ¥150 billion in efficiency and digital scheduling in 2024 to protect share.

Availability of Real-Time Market Data

The digital shift gives customers real-time freight rates and vessel spots via platforms and indices, cutting Mitsui O.S.K. Lines' information edge; in 2024, digital bookings grew ~28% in liner trade, raising price visibility.

Instant rate comparators let shippers pick carriers within minutes, so even SMEs negotiate hard using live benchmarks like the SCFI and Baltic indices, which swung 12–35% weekly in 2023–24.

Vertical Integration by Energy Majors

Vertical integration by energy majors—ExxonMobil, Shell, and Saudi Aramco—has seen them add or charter VLCCs and Suezmax tonnage; by 2024 Aramco owned/controlled ~60 tankers, cutting spot demand and raising their negotiation leverage with MOL during tight markets.

Owning tonnage shifts volume from third-party contracts to in-house logistics, so during 2022–24 freight spikes customers pushed down rates; when they charter externally they bid with clear cost benchmarks (voyage cost, bunker, GRI), squeezing MOL margins.

- Majors own ~dozens of tankers each (Aramco ~60, Shell/Exxon dozens)

- Less spot demand in 2022–24 reduced MOL leverage

- Customers' cost transparency tightens rate negotiations

Sensitivity to Global Economic Cycles

The demand for maritime transport is tightly linked to global GDP swings, so customers shift volumes quickly when growth slows, giving them price leverage.

When overcapacity hits, carriers cut rates and accept short-term, flexible contracts to fill ships; in 2025 global container throughput fell ~2.8% vs 2021 peak, boosting buyer bargaining power.

Fluctuating trade in the US, EU, and China through late 2025 kept shippers like Mitsui O.S.K. Lines under pressure to offer spot discounts and flexible terms.

- 2025 container throughput -2.8% from 2021 peak

- High idle capacity raises spot discounts

- Buyers push for flexible, short-term contracts

Shippers’ Concentration, Transparency & Overcapacity Squeeze MOL Pricing Power

Large, concentrated shippers (top 20 ≈35% of 2024 container demand) and digital rate transparency cut MOL’s pricing power; contract rates were ~8–12% below 2024–25 spot peaks, squeezing EBITDA. Overcapacity and -2.8% global container throughput (2025 vs 2021 peak) raise buyer leverage; majors’ owned tankers (Aramco ~60) further reduce spot demand, forcing price/term flexibility.

| Metric | Value |

|---|---|

| Top-20 share (2024) | ~35% |

| Contract discount | 8–12% |

| Container throughput (2025 vs 2021) | -2.8% |

| Aramco tankers (2024) | ~60 |

Same Document Delivered

Mitsui OSK Lines Porter's Five Forces Analysis

This preview shows the exact Mitsui O.S.K. Lines Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. It covers industry rivalry, supplier and buyer power, threat of substitutes, and entry barriers with data-driven insights and concise conclusions. The file is fully formatted and ready for download and use the moment you buy. What you see here is what you get.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Mitsui OSK Lines faces intense rivalry from global shipping giants and asset-heavy competitors, while moderate buyer power and rising fuel and regulatory costs squeeze margins; technological shifts and decarbonization create both threat and opportunity.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Mitsui OSK Lines’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Specialized Shipyards

The high-tech vessel market is concentrated: three South Korean builders (Hyundai Heavy, Samsung Heavy, Daewoo) plus top Chinese (Dalian, Hudong) and Japanese yards account for ~70–80% of LNG and green-ship newbuild capacity as of 2025, giving suppliers price and slot leverage over Mitsui OSK Lines.

As MOL shifts to zero-emission and LNG carriers by late 2025, orderbook bottlenecks matter: global green-fuel newbuild slots had ~24–30 month wait times in 2024–25, pushing yards’ negotiating power on price and delivery.

Specialized berth scarcity for ammonia/LNG-ready ships keeps switching costs high; retrofit and dedicated berth investments raised capex per ship by an estimated $20–50m versus conventional builds in 2024, reinforcing suppliers’ strong bargaining position.

Energy and Fuel Provider Dependency

MOL depends on global energy markets for bunker fuel and rising demand for ammonia/methanol; in 2024 fuel costs made up ~22% of operating expenses for large carriers, so suppliers hold pricing leverage. Long-term procurement deals reduce exposure, but 2022–24 oil price swings (Brent ranged $70–120/barrel) showed suppliers can tighten terms via geopolitical shifts. Cleaner-fuel rollout shrinks the supplier pool to firms with ammonia/methanol production and bunkering—raising switching costs and supplier power.

Specialized Technology and Engine Manufacturers

The shift to decarbonization gives a few engine and carbon-capture patent holders strong leverage: these firms control high-efficiency engines and CCGT (carbon capture and storage for ships) kits needed to meet IMO 2030/2050 rules, so supplier power is high. In 2024, only ~5 manufacturers supplied >70% of dual-fuel and methanol-capable marine engines, limiting MOL’s options and raising unit costs and delivery risk for its newbuilds.

Labor Unions and Seafarer Shortages

A tightening global market for skilled maritime officers and crew boosts supplier power: unions and manning agencies command stronger bargaining positions as experienced seafarers grow scarce.

Operating LNG and ammonia carriers needs specialized training and certifications, so retaining qualified personnel raises crew costs and turnover risk for Mitsui OSK Lines (MOL).

By 2025 shortages let labor providers press for higher wages and benefits; IMO data and industry reports show officer deficits up to 15–20% in key pools, pushing crew cost premiums of roughly 10–25%.

- Skilled-officer scarcity: +15–20% (2025)

- Crew cost premium: +10–25% vs 2019

- Higher retention spend: specialized training, bonuses

- Unions/agencies: increased leverage on wage/benefit terms

Port and Terminal Operator Influence

Global port congestion and just ~200 deep-water terminals worldwide that can handle 24k+ TEU mega-vessels give terminal operators outsized leverage over Mitsui O.S.K. Lines (MOL), forcing higher berthing fees and priority bidding to keep schedules intact.

MOL needs guaranteed priority access and sub-24-hour turnarounds in hubs like Shanghai, Rotterdam, and Singapore; delays cost container carriers ~$100–200 per box per day in 2024 estimates, squeezing margins.

In many strategic hubs, scarce alternative berths leave MOL accepting operator fee structures and demurrage rules, raising voyage costs and reducing routing flexibility.

- ~200 global deep-water mega-terminals

- $100–200 per TEU/day delay cost (2024 est.)

- Priority berth + <24h turnaround = critical

- Limited alternatives → weak supplier bargaining

Suppliers Dictate Shipping Costs: Concentrated Yards, Engine Oligopoly & Soaring Delays

Suppliers hold high bargaining power: concentrated green-newbuild yards (70–80% share), 24–30 month slot waits (2024–25), dual-fuel engine oligopoly (~5 makers >70% share in 2024), fuel = ~22% of OPEX (2024), officer shortages +15–20% (2025) and ~200 deep-water mega-terminals driving berth fees and delays ($100–200/TEU/day, 2024).

| Metric | Value |

|---|---|

| Yard concentration | 70–80% |

| Slot wait | 24–30 months |

| Engine suppliers | ~5 firms >70% |

| Fuel share OPEX | ~22% (2024) |

| Officer shortage | +15–20% (2025) |

| Delay cost | $100–200/TEU/day (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Mitsui OSK Lines highlighting competitive rivalry, buyer and supplier power, threats from new entrants and substitutes, and strategic barriers that protect its shipping, logistics, and offshore businesses.

Concise Porter's Five Forces summary for Mitsui O.S.K. Lines—quickly assess competitive intensity and strategic levers to relieve decision-making pain points.

Customers Bargaining Power

Consolidation of Global Shippers

Large retail, automotive and energy clients control concentrated volumes—top 20 shippers accounted for ~35% of container demand in 2024—letting them press Mitsui O.S.K. Lines (MOL) for price cuts or better terms by threatening reallocation.

These power buyers pushed average contract rates down an estimated 8–12% in 2024–25 versus spot peaks, directly squeezing MOL’s EBITDA margins; by end-2025 this buyer leverage remained a primary margin headwind.

Low Switching Costs in Standardized Shipping

For commoditized services like dry bulk and standard container transport, customers can switch carriers easily based on price and schedule; global container spot rates fell 42% year-over-year in 2024, increasing price sensitivity.

Moving goods A to B is seen as a commodity, so brand loyalty is secondary to cost-efficiency; MOL reported a 2024 containership revenue decline of 8% in some trade lanes.

This low switching cost forces Mitsui O.S.K. Lines to cut prices or innovate—MOL invested ¥150 billion in efficiency and digital scheduling in 2024 to protect share.

Availability of Real-Time Market Data

The digital shift gives customers real-time freight rates and vessel spots via platforms and indices, cutting Mitsui O.S.K. Lines' information edge; in 2024, digital bookings grew ~28% in liner trade, raising price visibility.

Instant rate comparators let shippers pick carriers within minutes, so even SMEs negotiate hard using live benchmarks like the SCFI and Baltic indices, which swung 12–35% weekly in 2023–24.

Vertical Integration by Energy Majors

Vertical integration by energy majors—ExxonMobil, Shell, and Saudi Aramco—has seen them add or charter VLCCs and Suezmax tonnage; by 2024 Aramco owned/controlled ~60 tankers, cutting spot demand and raising their negotiation leverage with MOL during tight markets.

Owning tonnage shifts volume from third-party contracts to in-house logistics, so during 2022–24 freight spikes customers pushed down rates; when they charter externally they bid with clear cost benchmarks (voyage cost, bunker, GRI), squeezing MOL margins.

- Majors own ~dozens of tankers each (Aramco ~60, Shell/Exxon dozens)

- Less spot demand in 2022–24 reduced MOL leverage

- Customers' cost transparency tightens rate negotiations

Sensitivity to Global Economic Cycles

The demand for maritime transport is tightly linked to global GDP swings, so customers shift volumes quickly when growth slows, giving them price leverage.

When overcapacity hits, carriers cut rates and accept short-term, flexible contracts to fill ships; in 2025 global container throughput fell ~2.8% vs 2021 peak, boosting buyer bargaining power.

Fluctuating trade in the US, EU, and China through late 2025 kept shippers like Mitsui O.S.K. Lines under pressure to offer spot discounts and flexible terms.

- 2025 container throughput -2.8% from 2021 peak

- High idle capacity raises spot discounts

- Buyers push for flexible, short-term contracts

Shippers’ Concentration, Transparency & Overcapacity Squeeze MOL Pricing Power

Large, concentrated shippers (top 20 ≈35% of 2024 container demand) and digital rate transparency cut MOL’s pricing power; contract rates were ~8–12% below 2024–25 spot peaks, squeezing EBITDA. Overcapacity and -2.8% global container throughput (2025 vs 2021 peak) raise buyer leverage; majors’ owned tankers (Aramco ~60) further reduce spot demand, forcing price/term flexibility.

| Metric | Value |

|---|---|

| Top-20 share (2024) | ~35% |

| Contract discount | 8–12% |

| Container throughput (2025 vs 2021) | -2.8% |

| Aramco tankers (2024) | ~60 |

Same Document Delivered

Mitsui OSK Lines Porter's Five Forces Analysis

This preview shows the exact Mitsui O.S.K. Lines Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. It covers industry rivalry, supplier and buyer power, threat of substitutes, and entry barriers with data-driven insights and concise conclusions. The file is fully formatted and ready for download and use the moment you buy. What you see here is what you get.