Mitsui OSK Lines PESTLE Analysis

Skip the Research. Get the Strategy.

Explore how geopolitical shifts, fuel price volatility, and tightening environmental regulations are reshaping Mitsui OSK Lines' strategic outlook—our PESTLE highlights risks and opportunities you need to know. Purchase the full analysis for a detailed, ready-to-use report that equips investors, strategists, and managers with actionable intelligence.

Political factors

Geopolitical tensions and trade route security

Ongoing conflicts in the Middle East and instability in the South China Sea have forced MOL to reroute ~12–18% of Asia-Europe voyages in 2024–2025, raising bunker and transit costs and contributing to a 20–35% surge in war-risk insurance premiums for affected voyages.

MOL reports average rerouting delays of 2–6 days per voyage in high-risk periods, reducing available sailing days and depressing annual operating leverage.

These disruptions require continuous coordination with international naval escorts and national authorities; MOL increased security liaison spending by roughly JPY 3–5 billion in FY2024 to protect crew and assets.

Energy security and national strategic interests

The Japanese government’s push for energy security boosts MOL’s LNG and tanker segments—Japan imported about 75% of its fossil fuel needs in 2024, sustaining strong demand for maritime transport.

As a primary carrier for national energy imports, MOL holds long-term charters with state-backed firms; in FY2024 MOL reported ¥1.2 trillion in marine transportation revenue, reflecting stable contract-backed cashflows.

Political alignment insulates MOL from short-term freight swings but mandates compliance with national security rules, including restrictions on cargo origins and enhanced vetting for shipments linked to sanctioned states.

Global trade protectionism and tariff barriers

Rising protectionism in the US and EU has shifted manufacturing toward Mexico and Southeast Asia, cutting Pacific container volumes by an estimated 3-5% in 2023–24 and prompting MOL to reroute capacity. New tariffs on steel, autos and electronics—US tariffs adding up to 10–25% in recent measures—forced MOL to rebalance car carrier and dry-bulk allocation, reducing Asia–Europe auto liftings by about 4% in 2024. MOL must constantly monitor bilateral deals like USMCA and evolving EU trade policy that can rapidly reshape Pacific and Atlantic demand patterns.

Sanctions compliance and international diplomacy

Stringent international sanctions regimes require Mitsui OSK Lines to maintain sophisticated legal and monitoring systems to avoid violations; in 2025 over 60% of major maritime incidents involved sanction-related compliance failures globally.

The end-2025 political climate imposed tighter controls on tech transfers and trades in dual-use goods, directly affecting MOL's RoRo and container routing and lifting compliance costs by an estimated 8–12%.

Non-compliance risks include multi-million-dollar fines and restricted access to correspondent banking; in 2024 global sanction penalties exceeded $5.4 billion, underscoring exposure.

- Require advanced screening systems and staff training

- Elevated compliance costs: ~8–12% increase

- High financial/legal risk: part of $5.4B+ global penalties (2024)

Government subsidies for green maritime technology

Political initiatives like Green Shipping Corridors enable MOL to tap government grants and low-interest loans; Japan pledged JPY 200 billion (2024–2026) for green shipping support, while the UK and US offer similar credit lines for decarbonization projects.

Japan and other flag states incentivize zero-emission vessels and ammonia engines through subsidies covering up to 30–50% of incremental costs, crucial for MOL to defray CAPEX for fleet retrofits.

Active engagement with these programs helps MOL offset estimated USD 10–20 billion needed through 2035 for fleet modernization and IMO 2050 compliance.

- Access to grants/low-rate loans (Japan JPY 200bn 2024–26)

- Subsidies covering 30–50% of incremental green CAPEX

- Offsets USD 10–20bn fleet modernization cost to 2035

MOL faces higher voyage costs and compliance hits amid sanctions—green aid offsets decarb CAPEX

Political risks (conflicts, sanctions, protectionism) raised MOL’s voyage costs: 12–18% rerouting, 2–6 day delays, 20–35% higher war-risk premiums, and ~JPY 3–5bn extra security spend in FY2024; compliance/tech-control costs up 8–12% amid $5.4bn+ global sanction fines (2024), while government green support (Japan JPY 200bn 2024–26) offsets part of USD 10–20bn decarbonization CAPEX to 2035.

| Metric | Value |

|---|---|

| Rerouting share | 12–18% |

| Delay per voyage | 2–6 days |

| War-risk premium rise | 20–35% |

| FY2024 security spend | JPY 3–5bn |

| Compliance cost rise | 8–12% |

| Global sanction fines (2024) | $5.4bn+ |

| Japan green fund | JPY 200bn (2024–26) |

| Decarb CAPEX need | USD 10–20bn to 2035 |

What is included in the product

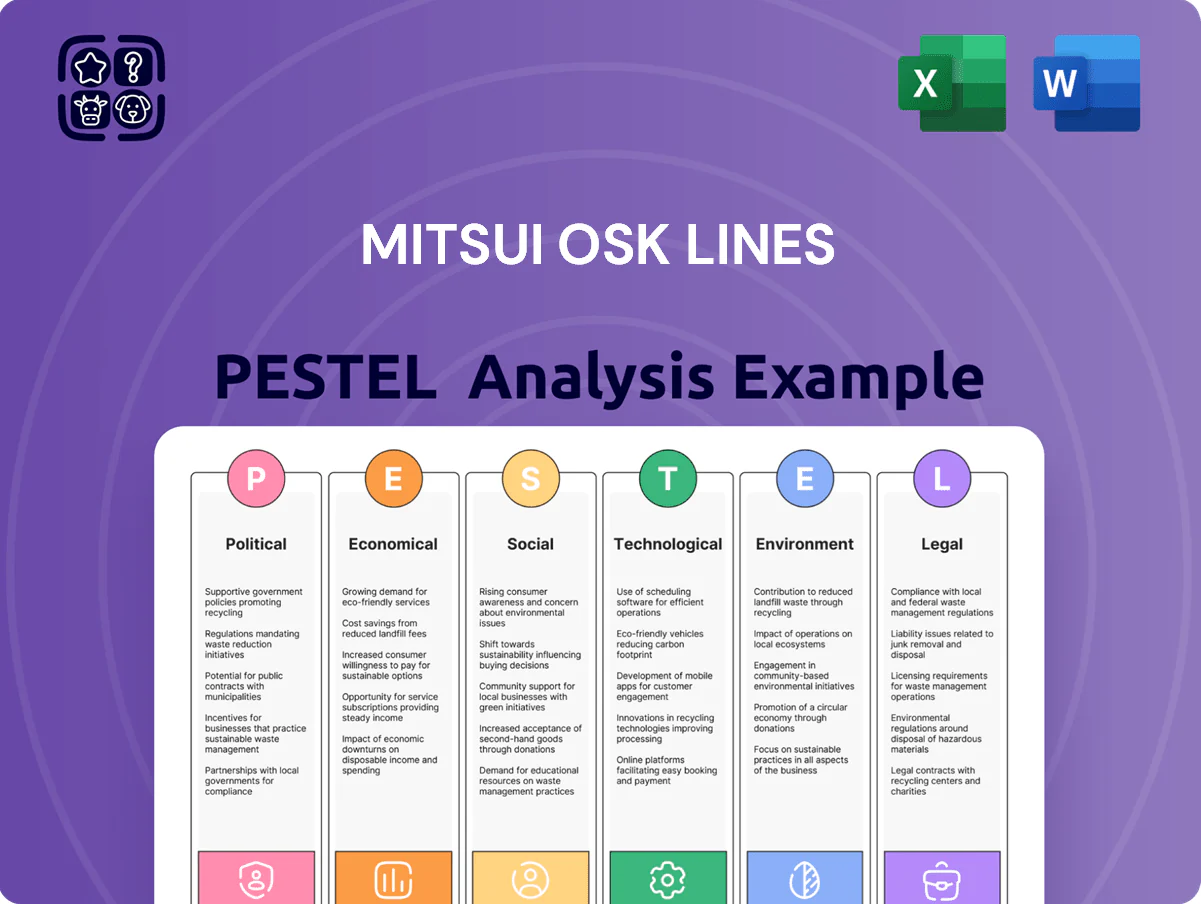

Explores how external macro-environmental factors uniquely affect Mitsui O.S.K. Lines across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to highlight industry-specific threats and opportunities for executives, consultants, and investors.

A concise, visually segmented PESTLE summary for Mitsui O.S.K. Lines that clarifies regulatory, economic, and environmental risks for quick inclusion in presentations or team planning sessions.

Economic factors

Volatility in global commodity prices

Fluctuations in iron ore, coal and grain prices directly affect demand for MOLs dry bulk services; iron ore price swings of 20–35% in 2023–24 altered charter rates and utilization. Economic activity in China and India—accounting for roughly 40–50% of seaborne dry bulk volumes—makes MOL revenue sensitive to those nations industrial output. By end-2025, calmer commodity markets reduced rate volatility, though occasional price spikes still threaten margins.

Impact of fuel price fluctuations

Fuel accounts for roughly 20–30% of MOLs operating costs; in 2024 bunker oil averaged about $650/ton while LNG cargo fuel remained 10–20% higher per energy unit, influencing vessel deployment between HFO and cleaner fuels like LNG or ammonia.

Fleet economics hinge on global oil market stability—crude averaged $80–90/barrel in 2024—and on scalable supply of alternatives: ammonia bunkering remains limited, keeping its price premium elevated.

MOL mitigates volatility via fuel hedging (standardized hedges covering portions of annual consumption) and capital expenditures in energy-efficiency measures—hull optimization, air lubrication, and dual-fuel engines—reducing fuel use intensity by targeted mid-single-digit percentages annually.

Currency exchange rate risks

Mitsui O.S.K. Lines reports in JPY while roughly 40-50% of revenue and many charter contracts are dollar-denominated, exposing the firm to USD/JPY volatility; between 2022–2024 the yen fell ~15% vs USD, amplifying translation effects.

Large swings in USD/JPY can produce material non-operating FX gains or losses—MOL recorded a ¥21.3 billion FX gain in FY2023 linked to exchange movements.

To hedge risk, MOL uses forwards, swaps and currency options and held over $1.2 billion in dollar assets and receivables by end-2024 to offset exposure amid global rate uncertainty.

Interest rate environment and capital financing

The cost of debt is critical for MOL’s capital-intensive fleet renewal; in 2025 MOL planned capital expenditures of about ¥600–700 billion, making borrowing sensitivity high.

Higher policy rates in major markets—e.g., US Fed funds at ~5.25–5.50% in 2024–25—raise newbuild financing costs and lease rates for vessel construction.

MOL’s A-/A3-ish credit profile and access to JPY and USD markets determine its ability to secure competitive long-term financing to meet sustainability and growth targets.

- 2025 capex ~¥600–700bn

- Fed funds ~5.25–5.50% (2024–25)

- Credit rating critical for low-cost JPY/USD debt

Global inflation and operational cost pressure

- Shipbuilding/maintenance +8–12% (2024)

- Seafarer wages +6% (2024)

- Spare parts/port services +10% (2024)

- Target opex savings 3–5% via digitalization

Bulk carriers under pressure: commodity swings, fuel costs, capex and FX hit margins

Commodity-driven demand (China/India ~45% of seaborne bulk) and 20–35% iron-ore price swings in 2023–24 drove charter rates; fuel ~20–30% of opex (bunker ~$650/ton in 2024); 2025 capex ~¥600–700bn increases debt sensitivity amid Fed funds ~5.25–5.50%; yen fell ~15% vs USD (2022–24) creating material FX translation effects.

| Metric | 2024/25 |

|---|---|

| Iron ore price swing | 20–35% |

| Bunker oil | $650/ton (2024) |

| Fuel % of opex | 20–30% |

| Capex | ¥600–700bn (2025) |

| Fed funds | 5.25–5.50% |

| USD/JPY move | Yen −15% (2022–24) |

Preview Before You Purchase

Mitsui OSK Lines PESTLE Analysis

The preview shown here is the exact Mitsui OSK Lines PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Explore how geopolitical shifts, fuel price volatility, and tightening environmental regulations are reshaping Mitsui OSK Lines' strategic outlook—our PESTLE highlights risks and opportunities you need to know. Purchase the full analysis for a detailed, ready-to-use report that equips investors, strategists, and managers with actionable intelligence.

Political factors

Geopolitical tensions and trade route security

Ongoing conflicts in the Middle East and instability in the South China Sea have forced MOL to reroute ~12–18% of Asia-Europe voyages in 2024–2025, raising bunker and transit costs and contributing to a 20–35% surge in war-risk insurance premiums for affected voyages.

MOL reports average rerouting delays of 2–6 days per voyage in high-risk periods, reducing available sailing days and depressing annual operating leverage.

These disruptions require continuous coordination with international naval escorts and national authorities; MOL increased security liaison spending by roughly JPY 3–5 billion in FY2024 to protect crew and assets.

Energy security and national strategic interests

The Japanese government’s push for energy security boosts MOL’s LNG and tanker segments—Japan imported about 75% of its fossil fuel needs in 2024, sustaining strong demand for maritime transport.

As a primary carrier for national energy imports, MOL holds long-term charters with state-backed firms; in FY2024 MOL reported ¥1.2 trillion in marine transportation revenue, reflecting stable contract-backed cashflows.

Political alignment insulates MOL from short-term freight swings but mandates compliance with national security rules, including restrictions on cargo origins and enhanced vetting for shipments linked to sanctioned states.

Global trade protectionism and tariff barriers

Rising protectionism in the US and EU has shifted manufacturing toward Mexico and Southeast Asia, cutting Pacific container volumes by an estimated 3-5% in 2023–24 and prompting MOL to reroute capacity. New tariffs on steel, autos and electronics—US tariffs adding up to 10–25% in recent measures—forced MOL to rebalance car carrier and dry-bulk allocation, reducing Asia–Europe auto liftings by about 4% in 2024. MOL must constantly monitor bilateral deals like USMCA and evolving EU trade policy that can rapidly reshape Pacific and Atlantic demand patterns.

Sanctions compliance and international diplomacy

Stringent international sanctions regimes require Mitsui OSK Lines to maintain sophisticated legal and monitoring systems to avoid violations; in 2025 over 60% of major maritime incidents involved sanction-related compliance failures globally.

The end-2025 political climate imposed tighter controls on tech transfers and trades in dual-use goods, directly affecting MOL's RoRo and container routing and lifting compliance costs by an estimated 8–12%.

Non-compliance risks include multi-million-dollar fines and restricted access to correspondent banking; in 2024 global sanction penalties exceeded $5.4 billion, underscoring exposure.

- Require advanced screening systems and staff training

- Elevated compliance costs: ~8–12% increase

- High financial/legal risk: part of $5.4B+ global penalties (2024)

Government subsidies for green maritime technology

Political initiatives like Green Shipping Corridors enable MOL to tap government grants and low-interest loans; Japan pledged JPY 200 billion (2024–2026) for green shipping support, while the UK and US offer similar credit lines for decarbonization projects.

Japan and other flag states incentivize zero-emission vessels and ammonia engines through subsidies covering up to 30–50% of incremental costs, crucial for MOL to defray CAPEX for fleet retrofits.

Active engagement with these programs helps MOL offset estimated USD 10–20 billion needed through 2035 for fleet modernization and IMO 2050 compliance.

- Access to grants/low-rate loans (Japan JPY 200bn 2024–26)

- Subsidies covering 30–50% of incremental green CAPEX

- Offsets USD 10–20bn fleet modernization cost to 2035

MOL faces higher voyage costs and compliance hits amid sanctions—green aid offsets decarb CAPEX

Political risks (conflicts, sanctions, protectionism) raised MOL’s voyage costs: 12–18% rerouting, 2–6 day delays, 20–35% higher war-risk premiums, and ~JPY 3–5bn extra security spend in FY2024; compliance/tech-control costs up 8–12% amid $5.4bn+ global sanction fines (2024), while government green support (Japan JPY 200bn 2024–26) offsets part of USD 10–20bn decarbonization CAPEX to 2035.

| Metric | Value |

|---|---|

| Rerouting share | 12–18% |

| Delay per voyage | 2–6 days |

| War-risk premium rise | 20–35% |

| FY2024 security spend | JPY 3–5bn |

| Compliance cost rise | 8–12% |

| Global sanction fines (2024) | $5.4bn+ |

| Japan green fund | JPY 200bn (2024–26) |

| Decarb CAPEX need | USD 10–20bn to 2035 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Mitsui O.S.K. Lines across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to highlight industry-specific threats and opportunities for executives, consultants, and investors.

A concise, visually segmented PESTLE summary for Mitsui O.S.K. Lines that clarifies regulatory, economic, and environmental risks for quick inclusion in presentations or team planning sessions.

Economic factors

Volatility in global commodity prices

Fluctuations in iron ore, coal and grain prices directly affect demand for MOLs dry bulk services; iron ore price swings of 20–35% in 2023–24 altered charter rates and utilization. Economic activity in China and India—accounting for roughly 40–50% of seaborne dry bulk volumes—makes MOL revenue sensitive to those nations industrial output. By end-2025, calmer commodity markets reduced rate volatility, though occasional price spikes still threaten margins.

Impact of fuel price fluctuations

Fuel accounts for roughly 20–30% of MOLs operating costs; in 2024 bunker oil averaged about $650/ton while LNG cargo fuel remained 10–20% higher per energy unit, influencing vessel deployment between HFO and cleaner fuels like LNG or ammonia.

Fleet economics hinge on global oil market stability—crude averaged $80–90/barrel in 2024—and on scalable supply of alternatives: ammonia bunkering remains limited, keeping its price premium elevated.

MOL mitigates volatility via fuel hedging (standardized hedges covering portions of annual consumption) and capital expenditures in energy-efficiency measures—hull optimization, air lubrication, and dual-fuel engines—reducing fuel use intensity by targeted mid-single-digit percentages annually.

Currency exchange rate risks

Mitsui O.S.K. Lines reports in JPY while roughly 40-50% of revenue and many charter contracts are dollar-denominated, exposing the firm to USD/JPY volatility; between 2022–2024 the yen fell ~15% vs USD, amplifying translation effects.

Large swings in USD/JPY can produce material non-operating FX gains or losses—MOL recorded a ¥21.3 billion FX gain in FY2023 linked to exchange movements.

To hedge risk, MOL uses forwards, swaps and currency options and held over $1.2 billion in dollar assets and receivables by end-2024 to offset exposure amid global rate uncertainty.

Interest rate environment and capital financing

The cost of debt is critical for MOL’s capital-intensive fleet renewal; in 2025 MOL planned capital expenditures of about ¥600–700 billion, making borrowing sensitivity high.

Higher policy rates in major markets—e.g., US Fed funds at ~5.25–5.50% in 2024–25—raise newbuild financing costs and lease rates for vessel construction.

MOL’s A-/A3-ish credit profile and access to JPY and USD markets determine its ability to secure competitive long-term financing to meet sustainability and growth targets.

- 2025 capex ~¥600–700bn

- Fed funds ~5.25–5.50% (2024–25)

- Credit rating critical for low-cost JPY/USD debt

Global inflation and operational cost pressure

- Shipbuilding/maintenance +8–12% (2024)

- Seafarer wages +6% (2024)

- Spare parts/port services +10% (2024)

- Target opex savings 3–5% via digitalization

Bulk carriers under pressure: commodity swings, fuel costs, capex and FX hit margins

Commodity-driven demand (China/India ~45% of seaborne bulk) and 20–35% iron-ore price swings in 2023–24 drove charter rates; fuel ~20–30% of opex (bunker ~$650/ton in 2024); 2025 capex ~¥600–700bn increases debt sensitivity amid Fed funds ~5.25–5.50%; yen fell ~15% vs USD (2022–24) creating material FX translation effects.

| Metric | 2024/25 |

|---|---|

| Iron ore price swing | 20–35% |

| Bunker oil | $650/ton (2024) |

| Fuel % of opex | 20–30% |

| Capex | ¥600–700bn (2025) |

| Fed funds | 5.25–5.50% |

| USD/JPY move | Yen −15% (2022–24) |

Preview Before You Purchase

Mitsui OSK Lines PESTLE Analysis

The preview shown here is the exact Mitsui OSK Lines PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment decisions.