Molinos Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

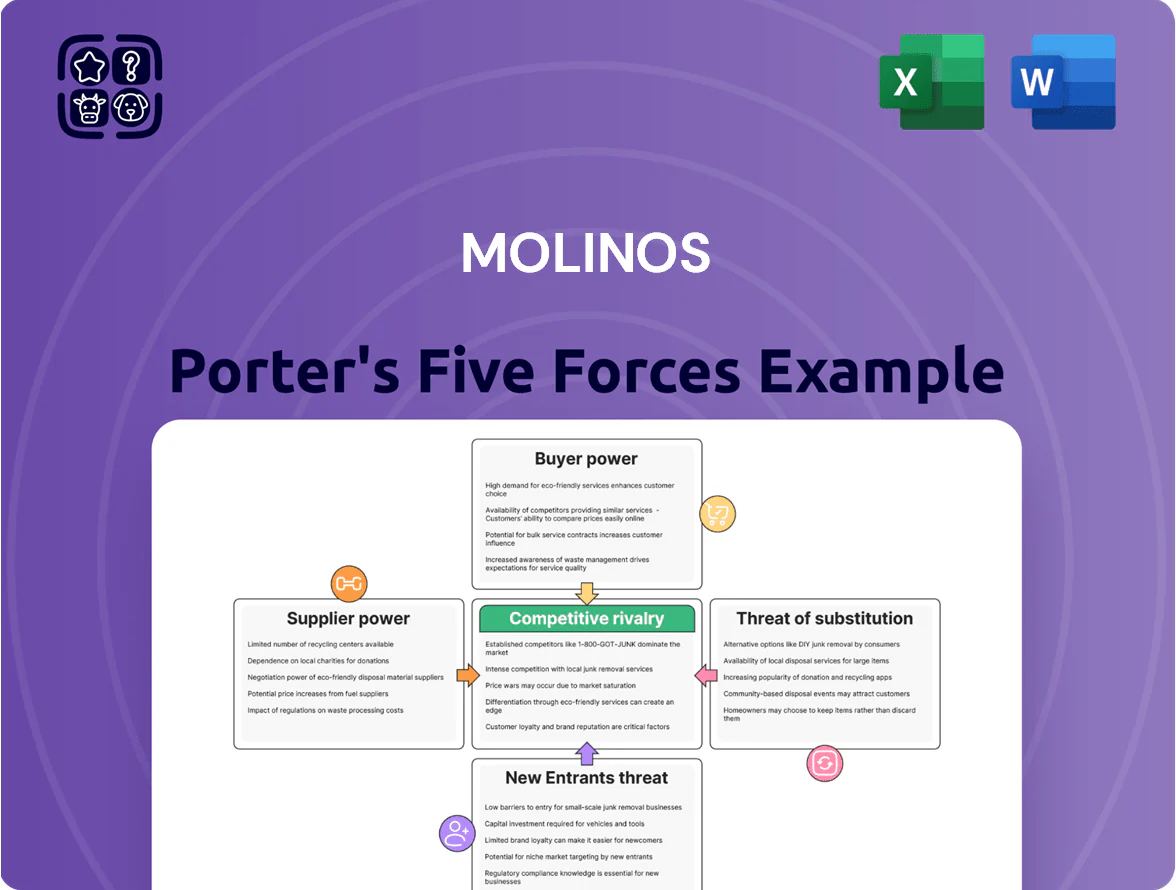

Molinos operates in a competitive food sector shaped by concentrated suppliers, strong buyer expectations, and moderate threat from substitutes and new entrants—factors that collectively compress margins and demand strategic differentiation.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Molinos’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Commodity Price Volatility

Molinos depends on wheat, sunflower seeds, and rice, commodities whose global prices swung by as much as 25% year-over-year in 2024–2025, forcing procurement cost increases that outpaced domestic inflation near 60% in Argentina by end-2025; this squeezed gross margins and pushed Molinos to renegotiate long-term contracts and use hedges, while large grain producers retained pricing power that raises supplier bargaining strength.

Agricultural Input Concentration

A limited number of large agribusinesses supply over 70% of Argentina’s soy and wheat, letting them push prices during strong global demand spikes—soymeal exports rose 12% in 2024, tightening local availability. Molinos uses multiyear purchase contracts and owns processing plants (vertical integration) to smooth costs, yet about 25–30% of its commodity spend remains exposed to spot-market swings.

Exchange Rate Impact

As many inputs are dollar-priced, the 40% cumulative peso devaluation vs USD from Jan 2023–Dec 2024 raised local supply costs materially, and suppliers now price in currency risk via dollar clauses or higher ARS marks; that squeezes Molinos’ margins and increases working capital needs.

Logistics and Energy Costs

Rising energy and fuel costs—Argentina diesel up ~35% year-on-year through 2024—have pushed packaging and transport suppliers to pass higher prices to Molinos, squeezing gross margins.

Domestic logistics are fragmented and unionized; road transport delays and strike risks give carriers strong bargaining power, raising freight volatility by an estimated 12–18% annually.

Molinos must continuously optimize routes, consolidate loads, and renegotiate supplier contracts to protect operating margin; every 1% fuel-cost rise can cut EBITDA by ~0.3 percentage point.

- Diesel +35% YoY (2024)

- Freight volatility +12–18%

- 1% fuel rise → ~0.3pp EBITDA drop

Climate and Harvest Risks

- 27% Argentina soybean drop 2023–24

- 45% grain price spike late 2023

- Weather-risk tools cost ~USD 0.5–1.5m/yr

- Source diversification lowers supply shocks

Suppliers wield power as commodity swings, devaluation and fuel spike boost costs—Molinos hedges

Suppliers hold moderate-high power: concentrated grain suppliers (70% market share), commodity price swings (wheat/sunflower ±25% YoY 2024–25), currency pass-through (40% peso deval 2023–24), fuel/freight inflation (diesel +35% 2024; freight vol +12–18%), and weather-driven shortages (soy -27% 2023–24) push costs; Molinos hedges, long contracts, vertical integration, and regional sourcing to reduce exposure.

| Metric | Value |

|---|---|

| Supplier concentration | 70% |

| Commodity volatility | ±25% YoY |

| Peso devaluation | 40% |

| Diesel (2024) | +35% |

| Soy output drop | -27% |

What is included in the product

Tailored Porter's Five Forces analysis for Molinos highlighting competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry, pinpointing disruptive trends, pricing pressures, and strategic levers to defend market share.

Molinos Porter's Five Forces summarized on one sheet—quickly reveal buyer/supplier leverage, rivalry intensity, and entry threats to guide pricing and M&A moves.

Customers Bargaining Power

Retailer Consolidation

Consumer Price Sensitivity

By end-2025 Argentine consumers remain highly price-sensitive after cumulative inflation near 1,200% since 2019, so Molinos cannot fully pass on cost rises without volume loss; private-label penetration rose to 38% in 2024, showing switch-to-cheaper risk. A 2025 NielsenIQ survey found 62% of shoppers trade down when premium value feels weak, capping Molinos pricing power and pressuring margins.

Low Switching Costs

Low switching costs in F&B mean consumers can swap pasta or oil brands with near-zero effort, so weekly promotions drive trials—NielsenIQ found 42% of Argentine shoppers switched brands for discounts in 2024. Molinos offsets this by spending ~AR$1.2bn on marketing and loyalty in 2023 and maintaining >95% product availability, aiming to keep repeat purchase rates above 60%.

Brand Loyalty Erosion

The rise of digital shopping and price-comparison apps lets Argentine consumers find lower prices instantly, shrinking brand-heritage advantage that Molinos Agro (Molinos Río de la Plata SA) once held; e‑commerce sales in Argentina grew ~28% in 2023, raising price sensitivity. To retain influence, Molinos must scale personalized marketing and digital loyalty: targeted promotions, CRM-driven offers, and app-based rewards to lift repeat-purchase rates above its current category average (~35%).

- 28% e‑commerce growth in Argentina, 2023

- Price apps increase real-time comparison

- Molinos needs CRM, app rewards, personalization

- Target: raise repeat purchases above 35%

Government Price Regulations

The Argentinian government routinely enforces price controls on staples; in 2024-2025 programs covered ~50 food items and capped annual retail increases below inflation, squeezing margins for firms like Molinos Río de la Plata (ticker: MOLI).

These controls act as a collective buyer, reducing Molinos’s pricing power and forcing trade-offs across categories to preserve overall profitability while complying with law.

- 2024: food inflation ~42% vs. regulated price hikes ~20%

- Regulated basket ~50 SKUs affects core pasta, oil, flour

- Margin pressure: gross margin down ~2–3 pp in 2024

Molinos squeezed by promos, price caps and private labels as margins fall to 24.1%

Supermarket chains (60%+ modern trade) and price controls cut Molinos’s bargaining power, forcing ~AR$5.2bn trade promos in 2024 and squeezing gross margin to 24.1% FY2024; consumers’ price sensitivity (cumulative ~1,200% inflation since 2019) and 38% private-label share cap pricing. Low switching costs and 28% e‑commerce growth (2023) raise promo-driven churn; Molinos spent ~AR$1.2bn marketing in 2023 to sustain >95% availability.

| Metric | Value |

|---|---|

| Modern trade share | 60%+ |

| Trade promotions (2024) | AR$5.2bn |

| Gross margin (FY2024) | 24.1% |

| Private-label (2024) | 38% |

| Marketing spend (2023) | AR$1.2bn |

| E‑commerce growth (2023) | 28% |

Preview the Actual Deliverable

Molinos Porter's Five Forces Analysis

This preview shows the exact Molinos Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full version you’ll get—fully formatted, professionally written, and ready for download and use the moment you buy.

No mockups, no samples: this is the actual, complete deliverable you’ll have instant access to after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Molinos operates in a competitive food sector shaped by concentrated suppliers, strong buyer expectations, and moderate threat from substitutes and new entrants—factors that collectively compress margins and demand strategic differentiation.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Molinos’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Commodity Price Volatility

Molinos depends on wheat, sunflower seeds, and rice, commodities whose global prices swung by as much as 25% year-over-year in 2024–2025, forcing procurement cost increases that outpaced domestic inflation near 60% in Argentina by end-2025; this squeezed gross margins and pushed Molinos to renegotiate long-term contracts and use hedges, while large grain producers retained pricing power that raises supplier bargaining strength.

Agricultural Input Concentration

A limited number of large agribusinesses supply over 70% of Argentina’s soy and wheat, letting them push prices during strong global demand spikes—soymeal exports rose 12% in 2024, tightening local availability. Molinos uses multiyear purchase contracts and owns processing plants (vertical integration) to smooth costs, yet about 25–30% of its commodity spend remains exposed to spot-market swings.

Exchange Rate Impact

As many inputs are dollar-priced, the 40% cumulative peso devaluation vs USD from Jan 2023–Dec 2024 raised local supply costs materially, and suppliers now price in currency risk via dollar clauses or higher ARS marks; that squeezes Molinos’ margins and increases working capital needs.

Logistics and Energy Costs

Rising energy and fuel costs—Argentina diesel up ~35% year-on-year through 2024—have pushed packaging and transport suppliers to pass higher prices to Molinos, squeezing gross margins.

Domestic logistics are fragmented and unionized; road transport delays and strike risks give carriers strong bargaining power, raising freight volatility by an estimated 12–18% annually.

Molinos must continuously optimize routes, consolidate loads, and renegotiate supplier contracts to protect operating margin; every 1% fuel-cost rise can cut EBITDA by ~0.3 percentage point.

- Diesel +35% YoY (2024)

- Freight volatility +12–18%

- 1% fuel rise → ~0.3pp EBITDA drop

Climate and Harvest Risks

- 27% Argentina soybean drop 2023–24

- 45% grain price spike late 2023

- Weather-risk tools cost ~USD 0.5–1.5m/yr

- Source diversification lowers supply shocks

Suppliers wield power as commodity swings, devaluation and fuel spike boost costs—Molinos hedges

Suppliers hold moderate-high power: concentrated grain suppliers (70% market share), commodity price swings (wheat/sunflower ±25% YoY 2024–25), currency pass-through (40% peso deval 2023–24), fuel/freight inflation (diesel +35% 2024; freight vol +12–18%), and weather-driven shortages (soy -27% 2023–24) push costs; Molinos hedges, long contracts, vertical integration, and regional sourcing to reduce exposure.

| Metric | Value |

|---|---|

| Supplier concentration | 70% |

| Commodity volatility | ±25% YoY |

| Peso devaluation | 40% |

| Diesel (2024) | +35% |

| Soy output drop | -27% |

What is included in the product

Tailored Porter's Five Forces analysis for Molinos highlighting competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry, pinpointing disruptive trends, pricing pressures, and strategic levers to defend market share.

Molinos Porter's Five Forces summarized on one sheet—quickly reveal buyer/supplier leverage, rivalry intensity, and entry threats to guide pricing and M&A moves.

Customers Bargaining Power

Retailer Consolidation

Consumer Price Sensitivity

By end-2025 Argentine consumers remain highly price-sensitive after cumulative inflation near 1,200% since 2019, so Molinos cannot fully pass on cost rises without volume loss; private-label penetration rose to 38% in 2024, showing switch-to-cheaper risk. A 2025 NielsenIQ survey found 62% of shoppers trade down when premium value feels weak, capping Molinos pricing power and pressuring margins.

Low Switching Costs

Low switching costs in F&B mean consumers can swap pasta or oil brands with near-zero effort, so weekly promotions drive trials—NielsenIQ found 42% of Argentine shoppers switched brands for discounts in 2024. Molinos offsets this by spending ~AR$1.2bn on marketing and loyalty in 2023 and maintaining >95% product availability, aiming to keep repeat purchase rates above 60%.

Brand Loyalty Erosion

The rise of digital shopping and price-comparison apps lets Argentine consumers find lower prices instantly, shrinking brand-heritage advantage that Molinos Agro (Molinos Río de la Plata SA) once held; e‑commerce sales in Argentina grew ~28% in 2023, raising price sensitivity. To retain influence, Molinos must scale personalized marketing and digital loyalty: targeted promotions, CRM-driven offers, and app-based rewards to lift repeat-purchase rates above its current category average (~35%).

- 28% e‑commerce growth in Argentina, 2023

- Price apps increase real-time comparison

- Molinos needs CRM, app rewards, personalization

- Target: raise repeat purchases above 35%

Government Price Regulations

The Argentinian government routinely enforces price controls on staples; in 2024-2025 programs covered ~50 food items and capped annual retail increases below inflation, squeezing margins for firms like Molinos Río de la Plata (ticker: MOLI).

These controls act as a collective buyer, reducing Molinos’s pricing power and forcing trade-offs across categories to preserve overall profitability while complying with law.

- 2024: food inflation ~42% vs. regulated price hikes ~20%

- Regulated basket ~50 SKUs affects core pasta, oil, flour

- Margin pressure: gross margin down ~2–3 pp in 2024

Molinos squeezed by promos, price caps and private labels as margins fall to 24.1%

Supermarket chains (60%+ modern trade) and price controls cut Molinos’s bargaining power, forcing ~AR$5.2bn trade promos in 2024 and squeezing gross margin to 24.1% FY2024; consumers’ price sensitivity (cumulative ~1,200% inflation since 2019) and 38% private-label share cap pricing. Low switching costs and 28% e‑commerce growth (2023) raise promo-driven churn; Molinos spent ~AR$1.2bn marketing in 2023 to sustain >95% availability.

| Metric | Value |

|---|---|

| Modern trade share | 60%+ |

| Trade promotions (2024) | AR$5.2bn |

| Gross margin (FY2024) | 24.1% |

| Private-label (2024) | 38% |

| Marketing spend (2023) | AR$1.2bn |

| E‑commerce growth (2023) | 28% |

Preview the Actual Deliverable

Molinos Porter's Five Forces Analysis

This preview shows the exact Molinos Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full version you’ll get—fully formatted, professionally written, and ready for download and use the moment you buy.

No mockups, no samples: this is the actual, complete deliverable you’ll have instant access to after payment.