Molinos PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic trends, and technological advances are shaping Molinos’s prospects in our concise PESTLE snapshot—insightful for investors and strategists alike; purchase the full analysis to unlock detailed risks, opportunities, and actionable recommendations tailored to real-world decisions.

Political factors

Government Deregulation Policies

Export Tax and Retention Policies

Changes in Argentina's export tax and retention policies are central for Molinos, which exported about 28% of its 2024 revenues; recent government moves trimmed soy and wheat export duties from peaks of 33% in 2022 to around 18–23% in 2024, but fiscal needs leave potential reversals likely.

International Trade Agreements

Domestic Political Stability

The executive's ability to pass reforms affects Molinos' operating costs and tax exposure; Argentina's reform-driven 2024 budget aimed to cut the fiscal deficit from 3.6% of GDP in 2023 to 2.1% in 2024, altering subsidy and tariff risks relevant to food processors.

Social stability and labor relations matter: national strikes in 2023 impacted 12% of food sector logistics days; strong union management reduces downtime and preserves distribution across 3,000+ retail outlets Molinos serves.

Political volatility can trigger sudden regulatory shifts—import restrictions and price controls in 2023 raised input cost volatility by an estimated 8–12%, forcing rapid procurement and pricing adjustments.

- Fiscal reform progress: deficit cut target 2024 — 2.1% of GDP

- 2023 strikes affected ~12% of logistics days

- Input cost volatility from 2023 policies: +8–12%

Public-Private Infrastructure Investment

Government moves to privatize and upgrade railways and ports—Argentina planned $6.7bn in transport investments for 2024–2025—can cut Molinos’ inland-to-port logistics costs by up to 15% by improving cadence and capacity.

Political choices on Parana River dredging, with 2024 depth targets of 34 feet, directly influence bulk export tariff and transshipment expenses; deeper drafts lower ship waiting and freight premiums.

Better links from provinces like Santa Fe and Córdoba reduce truck haul distances, trimming raw-material transport spend and boosting plant throughput and margins.

- 2024–25 transport capex $6.7bn

- Potential logistics cost reduction ~15%

- Parana target depth 34 feet in 2024

- Key sourcing provinces: Santa Fe, Córdoba

Molinos: Milei reforms, logistics capex boost EBITDA +4.8pp, cut costs ~15%

| Metric | Value |

|---|---|

| FY2025 EBITDA margin change | +4.8pp |

| Export share (2024) | 28% |

| Export duties (2024) | 18–23% |

| Logistics capex (2024–25) | $6.7bn |

| Logistics cost cut potential | ~15% |

| Parana depth target (2024) | 34 ft |

| Strikes impact (2023) | ~12% logistics days |

What is included in the product

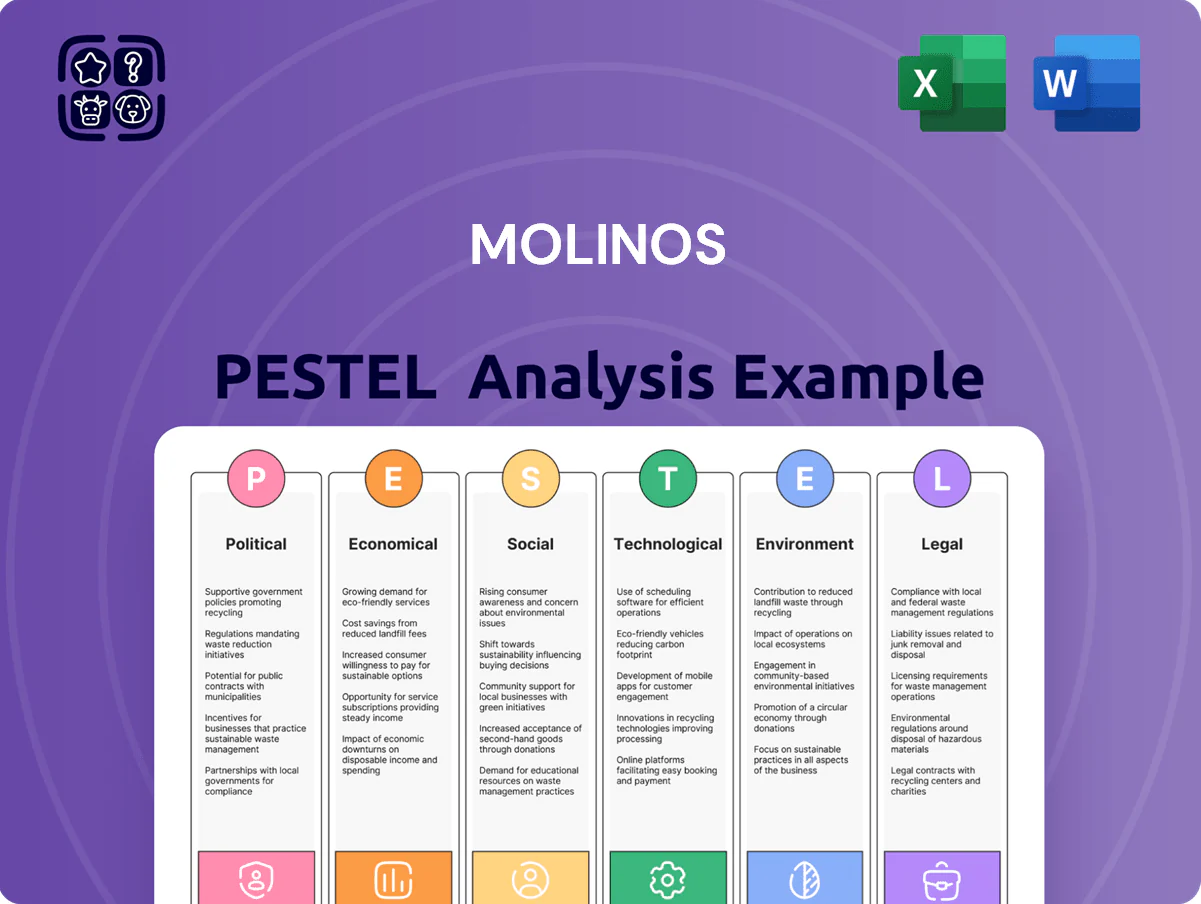

Explores how external macro-environmental factors uniquely affect Molinos across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and regional industry trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Condenses Molinos’ full PESTLE into a concise, shareable brief that teams can drop into presentations, annotate for local context, and use to align on external risks and strategic positioning.

Economic factors

Inflation and Macroeconomic Stabilization

By late 2025 Argentina's push toward single-digit annual inflation—official CPI fell from ~143% in 2023 to 92% in 2024 and projected ~9-10% by year-end 2025—directly affects Molinos' planning, simplifying cost forecasts and enabling multi-year supplier and retailer contracts. Lower inflation reduces working capital strain and hedging costs, improving margin visibility. During the transition Molinos must still manage residual monthly inflation spikes and shifting consumer real-income expectations while calibrating pricing and inventory strategies.

Currency Exchange Rate Dynamics

The recent narrowing of Argentina’s official and parallel exchange rates—by 2025 the blue peso spread fell to under 15% from peaks above 100% in 2022—eases Molinos’ cross-border flows for importing machinery and exporting goods, simplifying cash management. A more predictable FX backdrop supports foreign‑currency debt servicing and tighter hedging, lowering realized FX cost volatility. However, a sharp peso devaluation (monthly drops of 10%+ seen in past crises) would still raise import costs for inputs and packaging.

Consumer Purchasing Power

Recovery in real wages—Argentina's real wages rose ~6% in 2024 after inflation-adjusted declines—boosts demand for Molinos' value-added lines like frozen foods and premium pastas, which grew ~8% YoY in 2024 according to company reports.

Policies promoting employment and cutting household taxes correlate with higher sales volumes across Molinos' portfolio; employment recovered to ~43% formal sector growth in 2024 supporting consumption.

During austerity, consumers shift to generics or staples: private-label and basic pasta volumes rose ~5–7% in recessionary quarters of 2023–2024, pressuring Molinos' margin mix.

Global Commodity Price Fluctuations

As a major processor of wheat, sunflower and soy, Molinos is highly exposed to cyclical commodity markets; 2024 Argentine wheat exports fell 12% y/y, pushing local wheat prices up ~18% in H2 2024 and raising Molinos input costs.

Supply shocks—Black Sea disruptions and La Niña weather—can spike global prices or create export windfalls; soybean meal rose 22% in 2024 amid tighter global stocks.

Molinos uses futures, options and physical hedges; its 2024 risk-management reduced raw-material cost volatility by an estimated 40% versus unhedged exposure.

- High exposure to wheat/sunflower/soy price cycles

- 2024: local wheat +18%, soybean meal +22%

- Supply shocks (Black Sea, La Niña) materially affect costs

- Hedging program cut volatility ~40% in 2024

Access to Capital and Interest Rates

Normalization with international credit markets has increased Argentina's access to financing, with sovereign bond spreads narrowing to ~650 bps in 2025 from over 1,200 bps in 2020, improving project financing prospects for Molinos.

Lower domestic lending rates—policy rate down to ~60% in 2024 from >100% in 2023—reduce debt service costs, enabling plant upgrades and capacity expansion.

This financial backdrop supports Molinos' industrial modernization strategy by lowering capital costs and expanding financing options for long-term projects.

- Bond spread improvement: ~650 bps (2025)

- Policy rate: ~60% (2024)

- Enables capex for modernization and capacity expansion

Lower inflation, tighter spreads and hedging cut costs; premium demand rises despite commodity risks

Lower inflation (CPI 92% in 2024 → ~9–10% projected end-2025) and narrower blue spread (<15% in 2025) improve margin visibility, FX predictability and capex financing; real wages +6% (2024) lift premium product demand while commodity swings (wheat +18%, soybean meal +22% in 2024) and supply shocks remain key input risks; hedging cut raw-cost volatility ~40% in 2024.

| Metric | Value |

|---|---|

| CPI 2024 | 92% |

| Proj CPI end-2025 | ~9–10% |

| Blue spread 2025 | <15% |

| Wheat (H2 2024) | +18% |

| Soybean meal 2024 | +22% |

| Hedging impact 2024 | -40% vol |

Preview Before You Purchase

Molinos PESTLE Analysis

The preview shown here is the exact Molinos PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic trends, and technological advances are shaping Molinos’s prospects in our concise PESTLE snapshot—insightful for investors and strategists alike; purchase the full analysis to unlock detailed risks, opportunities, and actionable recommendations tailored to real-world decisions.

Political factors

Government Deregulation Policies

Export Tax and Retention Policies

Changes in Argentina's export tax and retention policies are central for Molinos, which exported about 28% of its 2024 revenues; recent government moves trimmed soy and wheat export duties from peaks of 33% in 2022 to around 18–23% in 2024, but fiscal needs leave potential reversals likely.

International Trade Agreements

Domestic Political Stability

The executive's ability to pass reforms affects Molinos' operating costs and tax exposure; Argentina's reform-driven 2024 budget aimed to cut the fiscal deficit from 3.6% of GDP in 2023 to 2.1% in 2024, altering subsidy and tariff risks relevant to food processors.

Social stability and labor relations matter: national strikes in 2023 impacted 12% of food sector logistics days; strong union management reduces downtime and preserves distribution across 3,000+ retail outlets Molinos serves.

Political volatility can trigger sudden regulatory shifts—import restrictions and price controls in 2023 raised input cost volatility by an estimated 8–12%, forcing rapid procurement and pricing adjustments.

- Fiscal reform progress: deficit cut target 2024 — 2.1% of GDP

- 2023 strikes affected ~12% of logistics days

- Input cost volatility from 2023 policies: +8–12%

Public-Private Infrastructure Investment

Government moves to privatize and upgrade railways and ports—Argentina planned $6.7bn in transport investments for 2024–2025—can cut Molinos’ inland-to-port logistics costs by up to 15% by improving cadence and capacity.

Political choices on Parana River dredging, with 2024 depth targets of 34 feet, directly influence bulk export tariff and transshipment expenses; deeper drafts lower ship waiting and freight premiums.

Better links from provinces like Santa Fe and Córdoba reduce truck haul distances, trimming raw-material transport spend and boosting plant throughput and margins.

- 2024–25 transport capex $6.7bn

- Potential logistics cost reduction ~15%

- Parana target depth 34 feet in 2024

- Key sourcing provinces: Santa Fe, Córdoba

Molinos: Milei reforms, logistics capex boost EBITDA +4.8pp, cut costs ~15%

| Metric | Value |

|---|---|

| FY2025 EBITDA margin change | +4.8pp |

| Export share (2024) | 28% |

| Export duties (2024) | 18–23% |

| Logistics capex (2024–25) | $6.7bn |

| Logistics cost cut potential | ~15% |

| Parana depth target (2024) | 34 ft |

| Strikes impact (2023) | ~12% logistics days |

What is included in the product

Explores how external macro-environmental factors uniquely affect Molinos across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and regional industry trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Condenses Molinos’ full PESTLE into a concise, shareable brief that teams can drop into presentations, annotate for local context, and use to align on external risks and strategic positioning.

Economic factors

Inflation and Macroeconomic Stabilization

By late 2025 Argentina's push toward single-digit annual inflation—official CPI fell from ~143% in 2023 to 92% in 2024 and projected ~9-10% by year-end 2025—directly affects Molinos' planning, simplifying cost forecasts and enabling multi-year supplier and retailer contracts. Lower inflation reduces working capital strain and hedging costs, improving margin visibility. During the transition Molinos must still manage residual monthly inflation spikes and shifting consumer real-income expectations while calibrating pricing and inventory strategies.

Currency Exchange Rate Dynamics

The recent narrowing of Argentina’s official and parallel exchange rates—by 2025 the blue peso spread fell to under 15% from peaks above 100% in 2022—eases Molinos’ cross-border flows for importing machinery and exporting goods, simplifying cash management. A more predictable FX backdrop supports foreign‑currency debt servicing and tighter hedging, lowering realized FX cost volatility. However, a sharp peso devaluation (monthly drops of 10%+ seen in past crises) would still raise import costs for inputs and packaging.

Consumer Purchasing Power

Recovery in real wages—Argentina's real wages rose ~6% in 2024 after inflation-adjusted declines—boosts demand for Molinos' value-added lines like frozen foods and premium pastas, which grew ~8% YoY in 2024 according to company reports.

Policies promoting employment and cutting household taxes correlate with higher sales volumes across Molinos' portfolio; employment recovered to ~43% formal sector growth in 2024 supporting consumption.

During austerity, consumers shift to generics or staples: private-label and basic pasta volumes rose ~5–7% in recessionary quarters of 2023–2024, pressuring Molinos' margin mix.

Global Commodity Price Fluctuations

As a major processor of wheat, sunflower and soy, Molinos is highly exposed to cyclical commodity markets; 2024 Argentine wheat exports fell 12% y/y, pushing local wheat prices up ~18% in H2 2024 and raising Molinos input costs.

Supply shocks—Black Sea disruptions and La Niña weather—can spike global prices or create export windfalls; soybean meal rose 22% in 2024 amid tighter global stocks.

Molinos uses futures, options and physical hedges; its 2024 risk-management reduced raw-material cost volatility by an estimated 40% versus unhedged exposure.

- High exposure to wheat/sunflower/soy price cycles

- 2024: local wheat +18%, soybean meal +22%

- Supply shocks (Black Sea, La Niña) materially affect costs

- Hedging program cut volatility ~40% in 2024

Access to Capital and Interest Rates

Normalization with international credit markets has increased Argentina's access to financing, with sovereign bond spreads narrowing to ~650 bps in 2025 from over 1,200 bps in 2020, improving project financing prospects for Molinos.

Lower domestic lending rates—policy rate down to ~60% in 2024 from >100% in 2023—reduce debt service costs, enabling plant upgrades and capacity expansion.

This financial backdrop supports Molinos' industrial modernization strategy by lowering capital costs and expanding financing options for long-term projects.

- Bond spread improvement: ~650 bps (2025)

- Policy rate: ~60% (2024)

- Enables capex for modernization and capacity expansion

Lower inflation, tighter spreads and hedging cut costs; premium demand rises despite commodity risks

Lower inflation (CPI 92% in 2024 → ~9–10% projected end-2025) and narrower blue spread (<15% in 2025) improve margin visibility, FX predictability and capex financing; real wages +6% (2024) lift premium product demand while commodity swings (wheat +18%, soybean meal +22% in 2024) and supply shocks remain key input risks; hedging cut raw-cost volatility ~40% in 2024.

| Metric | Value |

|---|---|

| CPI 2024 | 92% |

| Proj CPI end-2025 | ~9–10% |

| Blue spread 2025 | <15% |

| Wheat (H2 2024) | +18% |

| Soybean meal 2024 | +22% |

| Hedging impact 2024 | -40% vol |

Preview Before You Purchase

Molinos PESTLE Analysis

The preview shown here is the exact Molinos PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.