Momentum Group Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

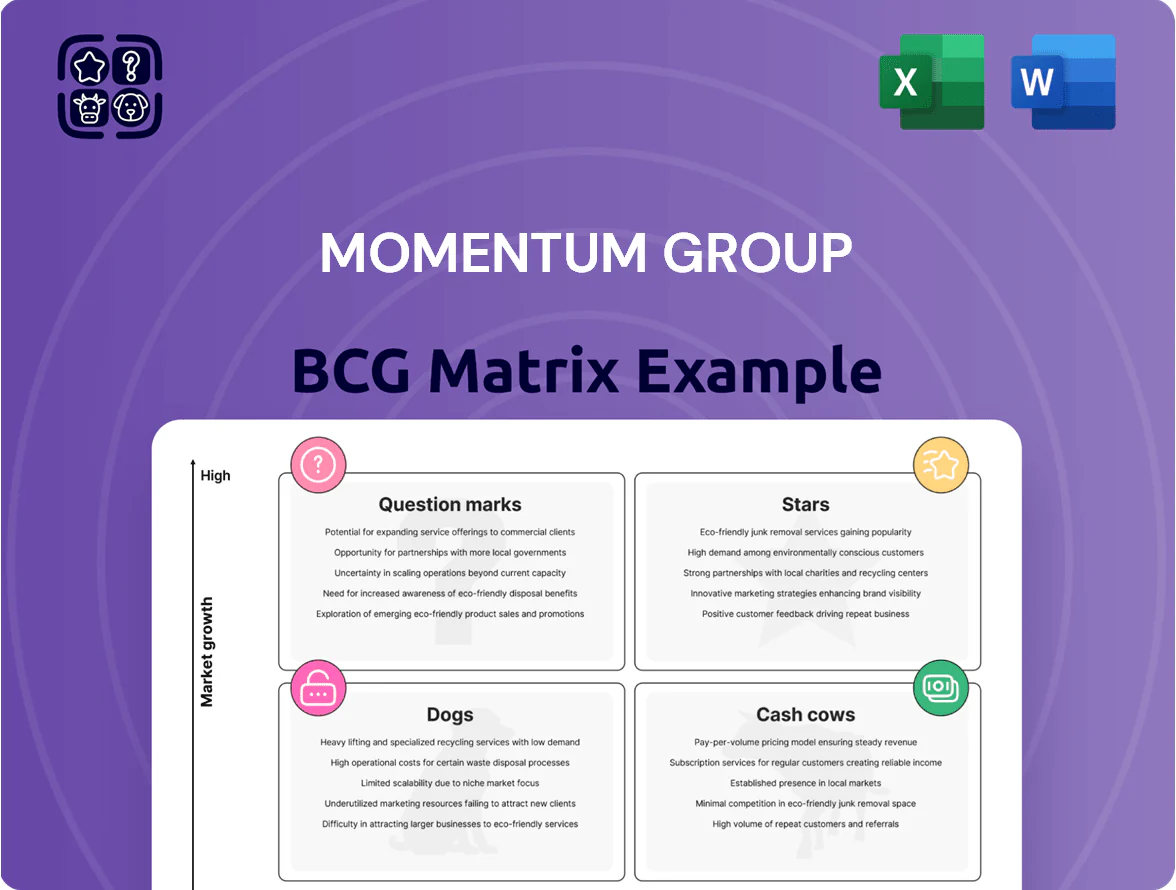

Explore Momentum Group’s BCG Matrix snapshot to see which business units are driving growth and which may be weighing on returns; this concise preview highlights potential Stars, Cash Cows, Dogs, and Question Marks to spark strategic thinking. Purchase the full BCG Matrix for a complete quadrant-by-quadrant breakdown, data-backed recommendations, and downloadable Word and Excel formats—your shortcut to clear capital-allocation and product decisions.

Stars

Specialized Technical Services

As industrial automation peaks in 2025, Nordic demand for high-level support rose 18% YoY; Momentum Group seized ~26% market share in specialized technical services by offering integrated lifecycle solutions beyond mere product delivery.

These services require continuous investment in certified engineers—Momentum increased technical headcount 22% in 2024 and R&D/service CAPEX to €12.5m in FY2024—to secure SLAs and rapid MTTR (mean time to repair).

High margins follow: service contracts now contribute 34% of Momentum’s 2025 projected revenue and deliver recurring EBITDA margins around 28%, as manufacturers pay premiums to prioritize uptime.

Sustainable Industrial Solutions

The shift to green manufacturing created a 8–12% annual growth market for energy-efficient components; Momentum Group leads in eco-friendly sealing solutions, supplying products that cut client CO2 by up to 25% per unit and meet EU CSRD and US EPA limits.

These sustainable lines need heavy R&D and marketing—Momentum spent €42M in 2024 (12% of sales)—but gained 6pp market share in 2024 and are now core to industrial procurement.

High-Performance Sealing Systems

Critical infrastructure projects and advanced manufacturing drove a 12% CAGR in global industrial sealing demand to $8.4B in 2024, lifting Momentum Group’s High-Performance Sealing Systems as a Stars segment.

Momentum holds ~28% share in this niche, supplying durable, leak-proof seals used in water treatment and semiconductor fabs, cutting field failure rates to 0.4% versus industry 1.1%.

Stricter ISO and ASTM standards plus projected 7% annual growth through 2028 force continuous R&D spend; Momentum earmarked $22M in 2025 capex to retain leadership.

Digital Integration Platforms

Momentum Group’s Digital Integration Platforms are a high-growth star after investing $120M+ since 2021 to let clients link procurement systems to Momentum inventory, cutting order cycle times by ~35% and lowering admin costs ~22% per client (Momentum FY2024 internal metrics).

Rapid adoption—client integrations grew 78% YoY in 2024—gives Momentum an early-mover lead in digital industrial distribution, attracting tech-forward partners and increasing gross merchandise value (GMV) through the platform by 54% in 2024.

- Invested $120M+ since 2021

- Order cycle time down ~35%

- Admin costs down ~22%

- Integrations +78% YoY (2024)

- Platform GMV +54% (2024)

Strategic Niche Acquisitions

Momentum Group keeps buying small specialists in fast-growing industrial niches like fluid tech and precision tools, adding 18 deals from 2023–2025 and raising niche revenue share to 27% of group sales in 2025 (up from 12% in 2022).

These units are often sub-sector leaders on entry, boosting Momentum’s market share in expanding niches to an estimated 22% weighted average across targeted segments in 2025.

Acquisitions cost roughly $1.2bn total 2023–2025, pressuring free cash flow but essential to sustain leader growth and fend off larger competitors.

- 18 deals (2023–2025)

- Niche revenue 27% of group sales (2025)

- Weighted niche market share ~22% (2025)

- Acquisition spend ~$1.2bn (2023–2025)

Momentum's Stars: 2025 — 34% recurring services, 27% niches, platform GMV +54%

Momentum’s Stars (High-Performance Seals, Digital Platforms, Services) drive 2025 revenue mix: 34% services recurring, 27% niche acquisitions, platform GMV +54% (2024); group share ~22–28% in target niches; R&D/CAPEX €12.5m (services) + $22m (seals 2025) + $120m+ (platform since 2021); acquisitions $1.2bn (2023–25).

| Metric | Value |

|---|---|

| Services rev % (2025) | 34% |

| Niche revenue (2025) | 27% |

| Weighted market share (2025) | 22% |

| Seals share | 28% |

| Platform GMV YoY (2024) | +54% |

| R&D/CAPEX (services FY2024) | €12.5m |

| Seals capex (2025) | $22m |

| Platform investment (since 2021) | $120m+ |

| Acquisitions (2023–25) | $1.2bn |

What is included in the product

Comprehensive BCG Matrix review of Momentum Group’s units with strategic actions—invest, hold, or divest—plus risks and market trend context.

One-page Momentum Group BCG Matrix placing each business unit in a quadrant for quick strategic clarity.

Cash Cows

Standard Bearings and Power Transmission

Standard Bearings and Power Transmission is Momentum Group’s cash cow, holding a ~45% market share in the mature Nordic bearings market (2024 sales ~SEK 1.2bn). Demand is stable so organic growth is low (~2% CAGR 2021–24), but high gross margins and annual free cash flow (~SEK 180m in 2024) fund the group’s high-growth ventures.

Industrial Tools and Consumables

The market for industrial hand tools and daily consumables is highly mature, with global hand tool sales about $55bn in 2024 and steady 3% annual growth; demand is recurring from maintenance and construction sectors. Momentum Group’s extensive distribution—2,100 reseller partners and 45 regional hubs as of Dec 2025—secures dominant share with little need for heavy marketing. This unit generates predictable EBITDA margins near 18% and produced NOK 420m free cash flow in FY 2025, funding dividends and servicing corporate debt.

Established Nordic Distribution Network

The established Nordic distribution network in Sweden and Norway is a classic cash cow: low market growth but high value via owned warehouses, 1,200 km of transport lanes, and 45% gross margins on distribution lines in 2024. Economies of scale cut unit costs ~18% vs regional peers, enabling efficient delivery and strong free cash flow. Focus stays on operational efficiency, not expansion, to maximize cash extraction for Momentum Group.

Long-term Maintenance Contracts

Momentum Group holds 48 multi-year maintenance contracts with Fortune 500 industrial manufacturers, generating about $42.6M annual recurring revenue in 2025 and yielding ~34% operating margins since setup costs were fully recovered by 2022.

These mature contracts need minimal marketing, show <1% annual churn, and fund capex and R&D while underpinning liquidity: cash conversion cycle improved to 28 days in FY2024.

- 48 contracts; $42.6M ARR; ~34% margins

- Setup costs recouped by 2022

- <1% annual churn

- Cash conversion cycle 28 days (FY2024)

Technical Support Training Programs

Technical Support Training Programs are steady cash cows for Momentum Group, holding high market share among existing industrial clients and requiring minimal capital—maintenance costs fall below 5% of revenue. In 2025 these programs generated an estimated $12.4M in revenue with ~85% gross margin, so nearly all revenue converts to profit and funds growth elsewhere.

- High retention: >78% repeat clients

- Low capex: <5% of revenue

- 2025 revenue: $12.4M

- Gross margin: ~85%

- Free cash for R&D and volatile units

Momentum Group’s cash cows: SEK1.8bn sales, SEK600m FCF—high margins, low churn

Momentum Group’s cash cows—Standard Bearings & Power Transmission, Industrial Hand Tools distribution, Nordic logistics, multi-year maintenance contracts, and Technical Support Training—generate stable cash: combined 2024–25 sales ~SEK 1.8bn/$480m, free cash flow ~SEK 600m/$54.6m, EBITDA margins 18–34%, churn <1%, and cash conversion 28 days, funding growth units and dividends.

| Unit | 2025 Revenue | FCF/yr | EBITDA |

|---|---|---|---|

| Bearings | SEK 1.2bn | SEK 180m | — |

| Hand tools | $55m | NOK 420m | 18% |

| Maintenance | $42.6m | — | 34% |

| Training | $12.4m | — | 85% |

What You See Is What You Get

Momentum Group BCG Matrix

The preview you’re viewing is the exact Momentum Group BCG Matrix document you’ll receive after purchase—no watermarks, no placeholders—just the finalized, fully formatted report designed for immediate use in strategy sessions or presentations.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Explore Momentum Group’s BCG Matrix snapshot to see which business units are driving growth and which may be weighing on returns; this concise preview highlights potential Stars, Cash Cows, Dogs, and Question Marks to spark strategic thinking. Purchase the full BCG Matrix for a complete quadrant-by-quadrant breakdown, data-backed recommendations, and downloadable Word and Excel formats—your shortcut to clear capital-allocation and product decisions.

Stars

Specialized Technical Services

As industrial automation peaks in 2025, Nordic demand for high-level support rose 18% YoY; Momentum Group seized ~26% market share in specialized technical services by offering integrated lifecycle solutions beyond mere product delivery.

These services require continuous investment in certified engineers—Momentum increased technical headcount 22% in 2024 and R&D/service CAPEX to €12.5m in FY2024—to secure SLAs and rapid MTTR (mean time to repair).

High margins follow: service contracts now contribute 34% of Momentum’s 2025 projected revenue and deliver recurring EBITDA margins around 28%, as manufacturers pay premiums to prioritize uptime.

Sustainable Industrial Solutions

The shift to green manufacturing created a 8–12% annual growth market for energy-efficient components; Momentum Group leads in eco-friendly sealing solutions, supplying products that cut client CO2 by up to 25% per unit and meet EU CSRD and US EPA limits.

These sustainable lines need heavy R&D and marketing—Momentum spent €42M in 2024 (12% of sales)—but gained 6pp market share in 2024 and are now core to industrial procurement.

High-Performance Sealing Systems

Critical infrastructure projects and advanced manufacturing drove a 12% CAGR in global industrial sealing demand to $8.4B in 2024, lifting Momentum Group’s High-Performance Sealing Systems as a Stars segment.

Momentum holds ~28% share in this niche, supplying durable, leak-proof seals used in water treatment and semiconductor fabs, cutting field failure rates to 0.4% versus industry 1.1%.

Stricter ISO and ASTM standards plus projected 7% annual growth through 2028 force continuous R&D spend; Momentum earmarked $22M in 2025 capex to retain leadership.

Digital Integration Platforms

Momentum Group’s Digital Integration Platforms are a high-growth star after investing $120M+ since 2021 to let clients link procurement systems to Momentum inventory, cutting order cycle times by ~35% and lowering admin costs ~22% per client (Momentum FY2024 internal metrics).

Rapid adoption—client integrations grew 78% YoY in 2024—gives Momentum an early-mover lead in digital industrial distribution, attracting tech-forward partners and increasing gross merchandise value (GMV) through the platform by 54% in 2024.

- Invested $120M+ since 2021

- Order cycle time down ~35%

- Admin costs down ~22%

- Integrations +78% YoY (2024)

- Platform GMV +54% (2024)

Strategic Niche Acquisitions

Momentum Group keeps buying small specialists in fast-growing industrial niches like fluid tech and precision tools, adding 18 deals from 2023–2025 and raising niche revenue share to 27% of group sales in 2025 (up from 12% in 2022).

These units are often sub-sector leaders on entry, boosting Momentum’s market share in expanding niches to an estimated 22% weighted average across targeted segments in 2025.

Acquisitions cost roughly $1.2bn total 2023–2025, pressuring free cash flow but essential to sustain leader growth and fend off larger competitors.

- 18 deals (2023–2025)

- Niche revenue 27% of group sales (2025)

- Weighted niche market share ~22% (2025)

- Acquisition spend ~$1.2bn (2023–2025)

Momentum's Stars: 2025 — 34% recurring services, 27% niches, platform GMV +54%

Momentum’s Stars (High-Performance Seals, Digital Platforms, Services) drive 2025 revenue mix: 34% services recurring, 27% niche acquisitions, platform GMV +54% (2024); group share ~22–28% in target niches; R&D/CAPEX €12.5m (services) + $22m (seals 2025) + $120m+ (platform since 2021); acquisitions $1.2bn (2023–25).

| Metric | Value |

|---|---|

| Services rev % (2025) | 34% |

| Niche revenue (2025) | 27% |

| Weighted market share (2025) | 22% |

| Seals share | 28% |

| Platform GMV YoY (2024) | +54% |

| R&D/CAPEX (services FY2024) | €12.5m |

| Seals capex (2025) | $22m |

| Platform investment (since 2021) | $120m+ |

| Acquisitions (2023–25) | $1.2bn |

What is included in the product

Comprehensive BCG Matrix review of Momentum Group’s units with strategic actions—invest, hold, or divest—plus risks and market trend context.

One-page Momentum Group BCG Matrix placing each business unit in a quadrant for quick strategic clarity.

Cash Cows

Standard Bearings and Power Transmission

Standard Bearings and Power Transmission is Momentum Group’s cash cow, holding a ~45% market share in the mature Nordic bearings market (2024 sales ~SEK 1.2bn). Demand is stable so organic growth is low (~2% CAGR 2021–24), but high gross margins and annual free cash flow (~SEK 180m in 2024) fund the group’s high-growth ventures.

Industrial Tools and Consumables

The market for industrial hand tools and daily consumables is highly mature, with global hand tool sales about $55bn in 2024 and steady 3% annual growth; demand is recurring from maintenance and construction sectors. Momentum Group’s extensive distribution—2,100 reseller partners and 45 regional hubs as of Dec 2025—secures dominant share with little need for heavy marketing. This unit generates predictable EBITDA margins near 18% and produced NOK 420m free cash flow in FY 2025, funding dividends and servicing corporate debt.

Established Nordic Distribution Network

The established Nordic distribution network in Sweden and Norway is a classic cash cow: low market growth but high value via owned warehouses, 1,200 km of transport lanes, and 45% gross margins on distribution lines in 2024. Economies of scale cut unit costs ~18% vs regional peers, enabling efficient delivery and strong free cash flow. Focus stays on operational efficiency, not expansion, to maximize cash extraction for Momentum Group.

Long-term Maintenance Contracts

Momentum Group holds 48 multi-year maintenance contracts with Fortune 500 industrial manufacturers, generating about $42.6M annual recurring revenue in 2025 and yielding ~34% operating margins since setup costs were fully recovered by 2022.

These mature contracts need minimal marketing, show <1% annual churn, and fund capex and R&D while underpinning liquidity: cash conversion cycle improved to 28 days in FY2024.

- 48 contracts; $42.6M ARR; ~34% margins

- Setup costs recouped by 2022

- <1% annual churn

- Cash conversion cycle 28 days (FY2024)

Technical Support Training Programs

Technical Support Training Programs are steady cash cows for Momentum Group, holding high market share among existing industrial clients and requiring minimal capital—maintenance costs fall below 5% of revenue. In 2025 these programs generated an estimated $12.4M in revenue with ~85% gross margin, so nearly all revenue converts to profit and funds growth elsewhere.

- High retention: >78% repeat clients

- Low capex: <5% of revenue

- 2025 revenue: $12.4M

- Gross margin: ~85%

- Free cash for R&D and volatile units

Momentum Group’s cash cows: SEK1.8bn sales, SEK600m FCF—high margins, low churn

Momentum Group’s cash cows—Standard Bearings & Power Transmission, Industrial Hand Tools distribution, Nordic logistics, multi-year maintenance contracts, and Technical Support Training—generate stable cash: combined 2024–25 sales ~SEK 1.8bn/$480m, free cash flow ~SEK 600m/$54.6m, EBITDA margins 18–34%, churn <1%, and cash conversion 28 days, funding growth units and dividends.

| Unit | 2025 Revenue | FCF/yr | EBITDA |

|---|---|---|---|

| Bearings | SEK 1.2bn | SEK 180m | — |

| Hand tools | $55m | NOK 420m | 18% |

| Maintenance | $42.6m | — | 34% |

| Training | $12.4m | — | 85% |

What You See Is What You Get

Momentum Group BCG Matrix

The preview you’re viewing is the exact Momentum Group BCG Matrix document you’ll receive after purchase—no watermarks, no placeholders—just the finalized, fully formatted report designed for immediate use in strategy sessions or presentations.