Momentum Metropolitan Holdings Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

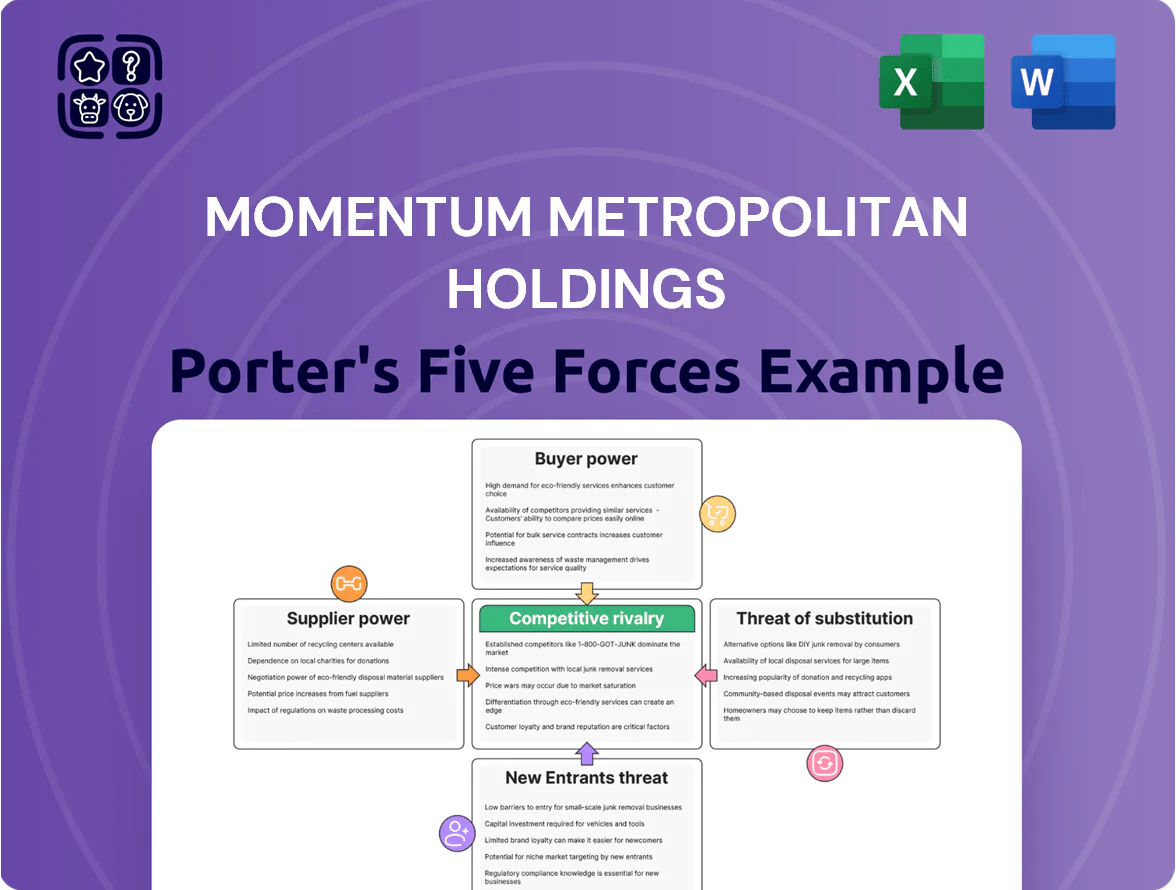

Momentum Metropolitan faces moderate buyer power and regulatory complexity, with competitive pressure from established insurers and fintech entrants challenging margins while capital requirements and distribution partnerships temper supplier influence.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Momentum Metropolitan Holdings’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Reinsurance Market Concentration

Reinsurance capacity is vital for Momentum Metropolitan when covering large or catastrophic losses, and a small number of global reinsurers—Munich Re, Swiss Re, Hannover Re—hold major bargaining power. By Q4 2025, global reinsurance rates rose ~25–40% after consecutive hard market cycles, pushing Momentum to either absorb higher ceded premium costs or raise retail pricing. Higher premiums squeeze margins; ceded ratios and capital buffers will guide the group’s choice.

Specialized Actuarial and Tech Talent

The supply of actuarial and data-science talent in South Africa is tight; only about 1,800 qualified actuaries nationally in 2024, concentrating demand for Momentum Metropolitan Holdings (MMH). As MMH adopts AI for underwriting, specialized tech professionals gain bargaining power, pushing salaries 15–35% above traditional actuarial paybands per 2024 industry surveys. Global tech firms and local fintechs compete fiercely, raising MMH’s hiring and retention costs and squeezing margins.

Critical IT and Cloud Infrastructure

Momentum Metropolitan depends on third-party cloud and core-banking providers, with top vendors holding long-term contracts that block easy exits; switching costs and technical complexity can exceed millions—industry estimates put migration of a large insurer at $20–100m and 12–24 months.

By 2025 digital transformation will drive most efficiency gains, so dependence on a few global tech vendors (AWS, Microsoft, Oracle) is a clear strategic vulnerability that can affect uptime, compliance, and margins.

Financial Data and Rating Agencies

Access to real-time market data and credit ratings is critical for Momentum Metropolitan Holdings’ asset management and investment units; Bloomberg and Refinitiv (Reuters) command ~60–80% market share for institutional terminals and S&P, Moody’s, and Fitch dominate credit intelligence, giving suppliers high bargaining power.

These services cost tens of millions annually for large institutions; fees are largely non-negotiable and act as fixed overheads for the group’s specialised arms, reducing margin flexibility.

- Critical: real-time data essential

- Major providers: Bloomberg, Refinitiv, S&P, Moody’s, Fitch

- Market share: ~60–80% terminals

- Cost impact: tens of millions/year, fixed

Regulatory and Compliance Bodies

Regulatory bodies like the Prudential Authority act as de facto suppliers by granting the legal licence to operate in South Africa; Momentum Metropolitan must meet Twin Peaks rules that raised compliance costs—estimated at ~R1.2bn group-wide in 2024—for governance, reporting and conduct requirements.

These regulators set capital adequacy ratios and solvency rules, giving them ultimate control over the group’s operational scope and dividend capacity; Momentum held a reported group capital adequacy cover of 1.6x at FY 2024, which regulators monitor closely.

- Prudential Authority = licence supplier

- Twin Peaks compliance ≈ R1.2bn (2024)

- Regulators set capital/dividend limits

- Group capital cover 1.6x (FY 2024)

Momentum Metropolitan faces strong supplier squeeze: rising reinsurance, talent & compliance costs

Suppliers (reinsurers, talent, cloud/data vendors, regulators) hold high bargaining power for Momentum Metropolitan: reinsurance rate hikes ~25–40% by Q4 2025, actuarial supply ~1,800 SA actuaries (2024) with specialized pay premia 15–35%, cloud migration costs $20–100m (12–24 months), data vendors 60–80% terminal share costing tens of millions/year, Twin Peaks compliance ≈ R1.2bn (2024), group capital cover 1.6x (FY2024).

| Supplier | Key metric |

|---|---|

| Reinsurance | Rates +25–40% (Q4 2025) |

| Actuarial talent | ~1,800 SA actuaries (2024); pay +15–35% |

| Cloud/core vendors | Migration $20–100m; 12–24 months |

| Market data & ratings | 60–80% terminals; tens of millions/yr |

| Regulators | Twin Peaks cost ≈ R1.2bn (2024); capital cover 1.6x |

What is included in the product

Tailored Porter's Five Forces analysis for Momentum Metropolitan Holdings, uncovering competitive drivers, customer and supplier influence, and barriers to entry that shape its profitability and strategic positioning.

A concise Porter's Five Forces one-sheet for Momentum Metropolitan Holdings—instant clarity on competitive pressures to speed boardroom decisions and strategic pivots.

Customers Bargaining Power

Retail Price Sensitivity and Comparison

Individual South African consumers are highly price-sensitive after years of weak GDP growth and 7–10% prime rates; 2024 FNB data showed 45% cut discretionary spend, raising churn risk for insurers like Momentum Metropolitan.

Digital comparison sites and apps grew 32% YoY in 2024, letting customers compare premiums and investment returns in minutes, so price transparency forces Momentum to match rates and service levels or lose customers.

Corporate Client Negotiation Leverage

Large corporate clients buying Momentum Metropolitan Holdings’ (JSE:MTM) employee benefits and group health schemes hold high bargaining power, often representing 1,000–50,000+ members and pushing for fee cuts; in 2024 South African group schemes saw average premium discounts of 8–12% for large-volume contracts.

Such clients negotiate lower admin fees and stricter claims terms, forcing Momentum to deliver tailored plans and tech-enabled cost management; losing a 10,000-member scheme can cut annual gross written premiums by millions of rand.

Low Switching Costs in Wealth Management

Low switching costs in wealth management mean clients can move portfolios quickly; by 2024 robo-advisors and platforms handled over 1.2 trillion USD globally, making transfers easier and lowering inertia.

Clients can shift discretionary savings if peers offer 50–100 bps lower fees or visibly better net-of-fee returns, so Momentum Metropolitan must sustain top-quartile performance and fee transparency.

Mobility pressures the group to deliver personalized advice; industry data show digital adopters have 20–30% higher retention when advisory personalization is strong.

Demand for Integrated Digital Experiences

By end-2025 customers expect seamless digital interactions—mobile claims, real-time investment tracking—raising churn risk if Momentum Metropolitan Holdings lags; global insurance digital adoption hit 68% in 2024 and South African online engagement rose 12% YoY in 2024, so tech-savvy clients will switch to digital-first rivals.

- 68% global digital insurance adoption (2024)

- South Africa online engagement +12% YoY (2024)

- Higher churn if digital delivery lags

Consumer Advocacy and Regulatory Protection

South Africa’s Policyholder Protection Rules and the FAIS amendments raise transparency and dispute rights, letting consumers challenge insurers and boosting their bargaining power; Momentum Metropolitan reported a 6% rise in complaints resolved in favour of policyholders in FY2024, signaling higher scrutiny.

This forces Momentum Metropolitan to uphold strict ethics, clearer disclosures, and faster claims handling to avoid fines—Regulator fines for 2023–24 averaged R14m across major insurers.

- Policyholder rules increase transparency

- 6% more favourable complaint outcomes FY2024

- R14m average regulator fine 2023–24

Rising Consumer Power: Discounts, Digital Transparency and Regulatory Leverage

Customers hold strong bargaining power: price-sensitive retail clients (45% cut discretionary spend, 2024 FNB) and large corporate schemes (8–12% volume discounts, 2024) force rate and fee compression; digital transparency (32% YoY growth in comparison apps, 2024) and 68% global digital adoption (2024) raise churn risk; regulator action (6% more favourable complaints FY2024; avg fines R14m) boosts consumer leverage.

| Metric | 2024 Value |

|---|---|

| Retail cut discretionary spend | 45% |

| Comparison apps growth | 32% YoY |

| Global digital adoption | 68% |

| Large-scheme discounts | 8–12% |

| Complaints favourable to policyholders | +6% |

| Avg regulator fine | R14m |

What You See Is What You Get

Momentum Metropolitan Holdings Porter's Five Forces Analysis

This preview shows the exact Momentum Metropolitan Holdings Porter's Five Forces analysis you'll receive immediately after purchase—fully written, formatted, and ready for download with no placeholders or samples.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Momentum Metropolitan faces moderate buyer power and regulatory complexity, with competitive pressure from established insurers and fintech entrants challenging margins while capital requirements and distribution partnerships temper supplier influence.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Momentum Metropolitan Holdings’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Reinsurance Market Concentration

Reinsurance capacity is vital for Momentum Metropolitan when covering large or catastrophic losses, and a small number of global reinsurers—Munich Re, Swiss Re, Hannover Re—hold major bargaining power. By Q4 2025, global reinsurance rates rose ~25–40% after consecutive hard market cycles, pushing Momentum to either absorb higher ceded premium costs or raise retail pricing. Higher premiums squeeze margins; ceded ratios and capital buffers will guide the group’s choice.

Specialized Actuarial and Tech Talent

The supply of actuarial and data-science talent in South Africa is tight; only about 1,800 qualified actuaries nationally in 2024, concentrating demand for Momentum Metropolitan Holdings (MMH). As MMH adopts AI for underwriting, specialized tech professionals gain bargaining power, pushing salaries 15–35% above traditional actuarial paybands per 2024 industry surveys. Global tech firms and local fintechs compete fiercely, raising MMH’s hiring and retention costs and squeezing margins.

Critical IT and Cloud Infrastructure

Momentum Metropolitan depends on third-party cloud and core-banking providers, with top vendors holding long-term contracts that block easy exits; switching costs and technical complexity can exceed millions—industry estimates put migration of a large insurer at $20–100m and 12–24 months.

By 2025 digital transformation will drive most efficiency gains, so dependence on a few global tech vendors (AWS, Microsoft, Oracle) is a clear strategic vulnerability that can affect uptime, compliance, and margins.

Financial Data and Rating Agencies

Access to real-time market data and credit ratings is critical for Momentum Metropolitan Holdings’ asset management and investment units; Bloomberg and Refinitiv (Reuters) command ~60–80% market share for institutional terminals and S&P, Moody’s, and Fitch dominate credit intelligence, giving suppliers high bargaining power.

These services cost tens of millions annually for large institutions; fees are largely non-negotiable and act as fixed overheads for the group’s specialised arms, reducing margin flexibility.

- Critical: real-time data essential

- Major providers: Bloomberg, Refinitiv, S&P, Moody’s, Fitch

- Market share: ~60–80% terminals

- Cost impact: tens of millions/year, fixed

Regulatory and Compliance Bodies

Regulatory bodies like the Prudential Authority act as de facto suppliers by granting the legal licence to operate in South Africa; Momentum Metropolitan must meet Twin Peaks rules that raised compliance costs—estimated at ~R1.2bn group-wide in 2024—for governance, reporting and conduct requirements.

These regulators set capital adequacy ratios and solvency rules, giving them ultimate control over the group’s operational scope and dividend capacity; Momentum held a reported group capital adequacy cover of 1.6x at FY 2024, which regulators monitor closely.

- Prudential Authority = licence supplier

- Twin Peaks compliance ≈ R1.2bn (2024)

- Regulators set capital/dividend limits

- Group capital cover 1.6x (FY 2024)

Momentum Metropolitan faces strong supplier squeeze: rising reinsurance, talent & compliance costs

Suppliers (reinsurers, talent, cloud/data vendors, regulators) hold high bargaining power for Momentum Metropolitan: reinsurance rate hikes ~25–40% by Q4 2025, actuarial supply ~1,800 SA actuaries (2024) with specialized pay premia 15–35%, cloud migration costs $20–100m (12–24 months), data vendors 60–80% terminal share costing tens of millions/year, Twin Peaks compliance ≈ R1.2bn (2024), group capital cover 1.6x (FY2024).

| Supplier | Key metric |

|---|---|

| Reinsurance | Rates +25–40% (Q4 2025) |

| Actuarial talent | ~1,800 SA actuaries (2024); pay +15–35% |

| Cloud/core vendors | Migration $20–100m; 12–24 months |

| Market data & ratings | 60–80% terminals; tens of millions/yr |

| Regulators | Twin Peaks cost ≈ R1.2bn (2024); capital cover 1.6x |

What is included in the product

Tailored Porter's Five Forces analysis for Momentum Metropolitan Holdings, uncovering competitive drivers, customer and supplier influence, and barriers to entry that shape its profitability and strategic positioning.

A concise Porter's Five Forces one-sheet for Momentum Metropolitan Holdings—instant clarity on competitive pressures to speed boardroom decisions and strategic pivots.

Customers Bargaining Power

Retail Price Sensitivity and Comparison

Individual South African consumers are highly price-sensitive after years of weak GDP growth and 7–10% prime rates; 2024 FNB data showed 45% cut discretionary spend, raising churn risk for insurers like Momentum Metropolitan.

Digital comparison sites and apps grew 32% YoY in 2024, letting customers compare premiums and investment returns in minutes, so price transparency forces Momentum to match rates and service levels or lose customers.

Corporate Client Negotiation Leverage

Large corporate clients buying Momentum Metropolitan Holdings’ (JSE:MTM) employee benefits and group health schemes hold high bargaining power, often representing 1,000–50,000+ members and pushing for fee cuts; in 2024 South African group schemes saw average premium discounts of 8–12% for large-volume contracts.

Such clients negotiate lower admin fees and stricter claims terms, forcing Momentum to deliver tailored plans and tech-enabled cost management; losing a 10,000-member scheme can cut annual gross written premiums by millions of rand.

Low Switching Costs in Wealth Management

Low switching costs in wealth management mean clients can move portfolios quickly; by 2024 robo-advisors and platforms handled over 1.2 trillion USD globally, making transfers easier and lowering inertia.

Clients can shift discretionary savings if peers offer 50–100 bps lower fees or visibly better net-of-fee returns, so Momentum Metropolitan must sustain top-quartile performance and fee transparency.

Mobility pressures the group to deliver personalized advice; industry data show digital adopters have 20–30% higher retention when advisory personalization is strong.

Demand for Integrated Digital Experiences

By end-2025 customers expect seamless digital interactions—mobile claims, real-time investment tracking—raising churn risk if Momentum Metropolitan Holdings lags; global insurance digital adoption hit 68% in 2024 and South African online engagement rose 12% YoY in 2024, so tech-savvy clients will switch to digital-first rivals.

- 68% global digital insurance adoption (2024)

- South Africa online engagement +12% YoY (2024)

- Higher churn if digital delivery lags

Consumer Advocacy and Regulatory Protection

South Africa’s Policyholder Protection Rules and the FAIS amendments raise transparency and dispute rights, letting consumers challenge insurers and boosting their bargaining power; Momentum Metropolitan reported a 6% rise in complaints resolved in favour of policyholders in FY2024, signaling higher scrutiny.

This forces Momentum Metropolitan to uphold strict ethics, clearer disclosures, and faster claims handling to avoid fines—Regulator fines for 2023–24 averaged R14m across major insurers.

- Policyholder rules increase transparency

- 6% more favourable complaint outcomes FY2024

- R14m average regulator fine 2023–24

Rising Consumer Power: Discounts, Digital Transparency and Regulatory Leverage

Customers hold strong bargaining power: price-sensitive retail clients (45% cut discretionary spend, 2024 FNB) and large corporate schemes (8–12% volume discounts, 2024) force rate and fee compression; digital transparency (32% YoY growth in comparison apps, 2024) and 68% global digital adoption (2024) raise churn risk; regulator action (6% more favourable complaints FY2024; avg fines R14m) boosts consumer leverage.

| Metric | 2024 Value |

|---|---|

| Retail cut discretionary spend | 45% |

| Comparison apps growth | 32% YoY |

| Global digital adoption | 68% |

| Large-scheme discounts | 8–12% |

| Complaints favourable to policyholders | +6% |

| Avg regulator fine | R14m |

What You See Is What You Get

Momentum Metropolitan Holdings Porter's Five Forces Analysis

This preview shows the exact Momentum Metropolitan Holdings Porter's Five Forces analysis you'll receive immediately after purchase—fully written, formatted, and ready for download with no placeholders or samples.