Momentum Metropolitan Holdings PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock how political shifts, economic cycles, and technological disruption are reshaping Momentum Metropolitan Holdings—and turn those insights into strategic advantage; purchase the full PESTLE analysis for a detailed, ready-to-use breakdown that helps investors and planners forecast risks and spot growth opportunities instantly.

Political factors

South African Coalition Government Stability

The formation of the Government of National Unity after the 2024 election — with parties holding roughly 53% (ANC-led bloc) and opposition coalition at 47% in Parliament — directly affects Momentum Metropolitan’s operating outlook, as multi-party cooperation will shape fiscal discipline, projected 2025 budget deficit targets (around 3.5% of GDP) and structural reforms in financial services; sustained coalition stability is therefore key to investor confidence and predictable regulatory policy.

National Health Insurance Implementation

The progression of the National Health Insurance Act creates material uncertainty for Momentum Metropolitan’s health insurance and administration segments, with public debate and court challenges delaying full rollout beyond the 2024 policy milestones; private medical scheme membership stood at about 8.6 million in 2024, a key exposure for the group.

Geopolitical Volatility and Pan-African Relations

Momentum Metropolitan's operations across 9 African markets, where cross-border premiums contributed about 14% of group revenue in FY2024, are sensitive to regional political shifts and evolving trade agreements.

Political instability or rising protectionism—evident in recent tariffs and capital controls in parts of East and West Africa—can disrupt cross-border capital flows and the group's service delivery and solvency management.

Monitoring diplomatic relations and African Continental Free Trade Area developments is vital for Momentum Metropolitan's international growth strategy and for mitigating risks to R62.5bn of assets under management outside South Africa (2024).

Public Infrastructure and Service Delivery

Political effectiveness in restoring energy, logistics and water infrastructure affects underwriting costs and claims frequency; South Africa's rolling power cuts cost the economy an estimated ZAR 45–50 billion annually in 2023–24, raising operational and claim risks for Momentum Metropolitan Holdings.

Persistent failures in state-owned enterprises shrink insurable asset pools and consumer disposable income; Eskom, Transnet and municipal water outages contributed to GDP growth slipping to 0.6% in 2024, contracting premium growth potential.

The insurer's performance is tied to government execution of the Economic Reconstruction and Recovery Plan, which targets ZAR 1.2 trillion in investment over five years—successful delivery would expand commercial and retail insurance demand.

- Energy outages: ~ZAR 45–50bn economic loss (2023–24)

- GDP growth: 0.6% in 2024, limiting premium expansion

- Recovery Plan: ZAR 1.2tn investment target over five years

Broad-Based Black Economic Empowerment Policy

As a major financial services player, Momentum Metropolitan must meet evolving B-BBEE codes and transformation targets; the Financial Sector Charter review in 2024 proposed increased procurement and ownership scoring that could affect its compliance metrics and client eligibility.

Compliance is a legal requirement and prerequisite for securing government contracts and maintaining its social license—Momentum reported a Level 2 contributor status in 2023, which supports access to preferential procurement.

Shifts in political rhetoric around ownership and procurement targets through 2025 require continuous strategic alignment across HR, procurement and M&A to protect revenue streams tied to public-sector business.

- 2023: Momentum reported Level 2 B-BBEE

- 2024: Financial Sector Charter review proposes tighter procurement/ownership targets

- Risk: loss of government contracts if non-compliant

Momentum Metropolitan outlook hinges on political stability, NHI and Eskom losses

Political stability of the 2024 Government of National Unity, NHI progress, SOE performance and B-BBEE/Financial Sector Charter reforms materially affect Momentum Metropolitan’s revenue, claims and access to public contracts; key metrics: GDP growth 0.6% (2024), private medical scheme membership ~8.6m (2024), non‑SA AUM R62.5bn (2024), Eskom-related economic loss ZAR45–50bn (2023–24).

| Metric | Value |

|---|---|

| GDP growth (2024) | 0.6% |

| Private medical scheme members (2024) | 8.6m |

| Non‑SA AUM (2024) | R62.5bn |

| Eskom economic loss (2023–24) | ZAR45–50bn |

What is included in the product

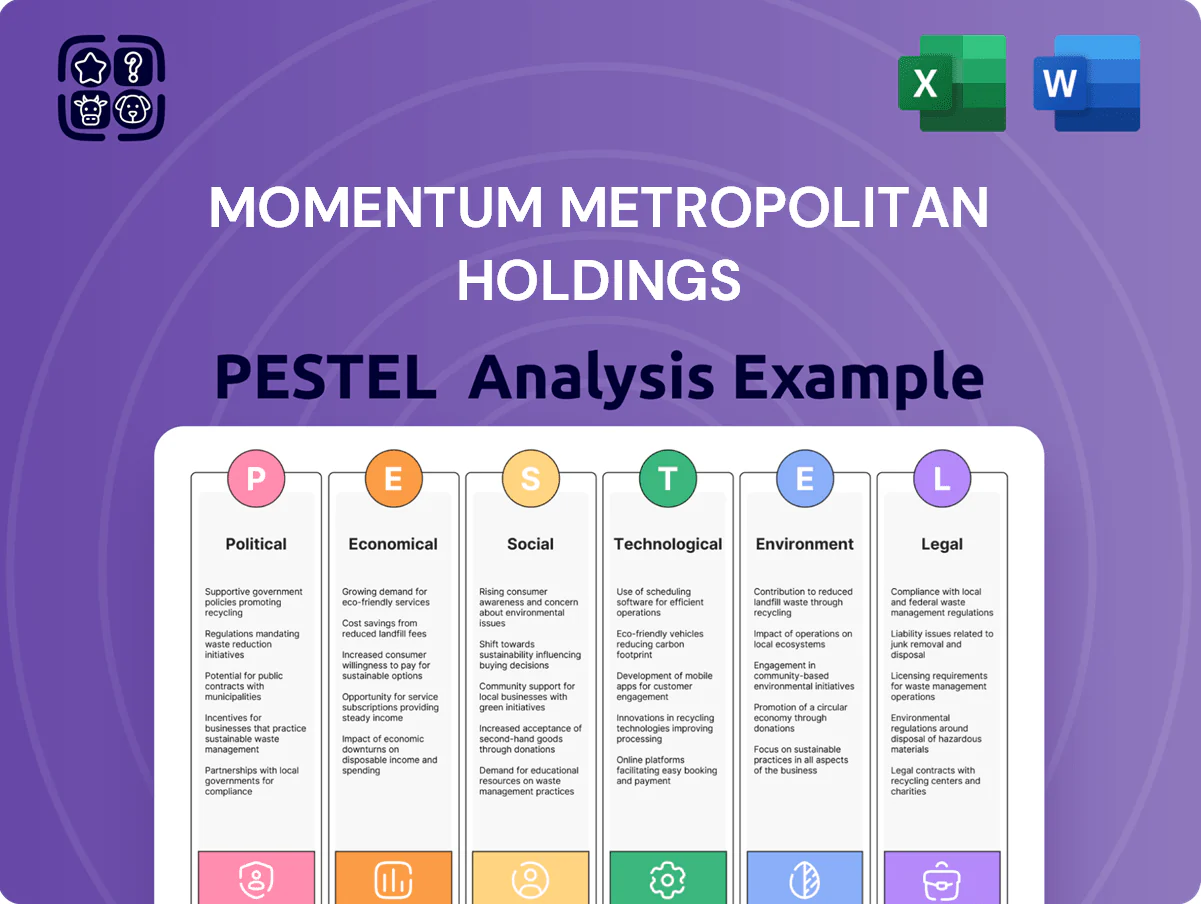

Explores how external macro-environmental factors uniquely affect Momentum Metropolitan Holdings across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific insights to identify risks and opportunities for executives, investors, and strategists.

Provides a concise, visually segmented PESTLE summary of Momentum Metropolitan Holdings that’s easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Interest Rate Cycle and Monetary Policy

The South African Reserve Bank’s policy rate at 8.25% (Feb 2026) directly affects Momentum Metropolitan’s investment income and liability valuations; higher rates boosted fixed-income yields, contributing to a 2025 investment return uptick of ~3.2% year-on-year, while also reducing demand for credit life products. A prolonged high-rate environment supports portfolio yields but suppresses single-premium sales; a shift to a cutting cycle could raise consumer spending yet compress margins on savings and guaranteed products.

Inflationary Pressure on Claims and Expenses

Persistent inflation, with South African CPI averaging 5.9% in 2024 and medical inflation near 8–10%, is lifting claims costs in Momentum Metropolitan’s short-term and health books; motor parts price inflation of c.12% in 2024 further increases motor claim severity. The group faces trade-offs raising premiums—Momentum’s 2024 short-term loss ratio rose to ~70% in parts of the book—against losing price-sensitive customers. Controlling opex, where wage and supplier cost inflation ran 6–9% in 2024, is critical to protect normalized earnings.

Low GDP Growth and Consumer Resilience

Subdued GDP growth in South Africa—0.7% in 2024 IMF estimate—constrains expansion of the total addressable market for Momentum Metropolitan's financial services, limiting new premium and asset-gathering opportunities.

High unemployment at 32.9% (Q4 2024, Stats SA) and stagnant real household incomes dampen demand for discretionary investments and life insurance, pressuring sales volumes and persistency.

The group’s performance hinges on gaining share in this low-growth environment via competitive pricing, digital distribution and product innovation as seen in its 2024 strategy to lift market penetration and protect margins.

Currency Exchange Rate Fluctuations

The volatility of the South African Rand, which depreciated about 6% vs the US dollar in 2024, affects Momentum Metropolitan Holdings by altering reported offshore earnings and raising costs for imported IT—pressure on margins for 2024/25 technology investments.

While a weaker Rand can boost the ZAR valuation of offshore assets, episodes of depreciation often reflect macro instability; Momentum uses hedging and geographic diversification to manage FX exposure.

- 2024 ZAR/USD move ~-6%: higher IT import costs

- Weaker Rand increases local value of offshore assets

- Hedging and geographic diversification used to mitigate risk

Capital Market Performance

Momentum Metropolitan’s fee income closely tracks JSE and global equity performance; a 10% rise in the JSE Top 40 in 2024 lifted AUM industry-wide, and Momentum reported AUM of ~R580bn in FY2024, boosting performance fees, while 2022-23 downturns showed vulnerability via capital outflows.

The group’s diversified portfolios—mix of cash, bonds, equities and alternatives—aim to limit volatility, with multi-asset mandates reducing drawdowns by an estimated 4–6% in stressed periods.

- FY2024 AUM ~R580bn

- JSE Top 40 +10% in 2024 (example market rebound)

- Diversification reduced drawdown ~4–6%

SARB hikes lift bond income as inflation, weak GDP and ZAR squeeze demand and costs

Higher SARB rates (8.25% Feb 2026) raised 2025 bond yields, aiding investment income; CPI 5.9% (2024) and medical inflation ~8–10% increased claims and costs; GDP ~0.7% (2024) and unemployment 32.9% cut demand; ZAR -6% vs USD (2024) hit IT costs but uplifted offshore AUM (FY2024 AUM ~R580bn).

| Metric | Value |

|---|---|

| SARB rate | 8.25% Feb 2026 |

| CPI 2024 | 5.9% |

| GDP 2024 | 0.7% |

| Unemployment Q4 2024 | 32.9% |

| ZAR vs USD 2024 | -6% |

| FY2024 AUM | ~R580bn |

Same Document Delivered

Momentum Metropolitan Holdings PESTLE Analysis

The preview shown here is the exact Momentum Metropolitan Holdings PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic analysis and decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Unlock how political shifts, economic cycles, and technological disruption are reshaping Momentum Metropolitan Holdings—and turn those insights into strategic advantage; purchase the full PESTLE analysis for a detailed, ready-to-use breakdown that helps investors and planners forecast risks and spot growth opportunities instantly.

Political factors

South African Coalition Government Stability

The formation of the Government of National Unity after the 2024 election — with parties holding roughly 53% (ANC-led bloc) and opposition coalition at 47% in Parliament — directly affects Momentum Metropolitan’s operating outlook, as multi-party cooperation will shape fiscal discipline, projected 2025 budget deficit targets (around 3.5% of GDP) and structural reforms in financial services; sustained coalition stability is therefore key to investor confidence and predictable regulatory policy.

National Health Insurance Implementation

The progression of the National Health Insurance Act creates material uncertainty for Momentum Metropolitan’s health insurance and administration segments, with public debate and court challenges delaying full rollout beyond the 2024 policy milestones; private medical scheme membership stood at about 8.6 million in 2024, a key exposure for the group.

Geopolitical Volatility and Pan-African Relations

Momentum Metropolitan's operations across 9 African markets, where cross-border premiums contributed about 14% of group revenue in FY2024, are sensitive to regional political shifts and evolving trade agreements.

Political instability or rising protectionism—evident in recent tariffs and capital controls in parts of East and West Africa—can disrupt cross-border capital flows and the group's service delivery and solvency management.

Monitoring diplomatic relations and African Continental Free Trade Area developments is vital for Momentum Metropolitan's international growth strategy and for mitigating risks to R62.5bn of assets under management outside South Africa (2024).

Public Infrastructure and Service Delivery

Political effectiveness in restoring energy, logistics and water infrastructure affects underwriting costs and claims frequency; South Africa's rolling power cuts cost the economy an estimated ZAR 45–50 billion annually in 2023–24, raising operational and claim risks for Momentum Metropolitan Holdings.

Persistent failures in state-owned enterprises shrink insurable asset pools and consumer disposable income; Eskom, Transnet and municipal water outages contributed to GDP growth slipping to 0.6% in 2024, contracting premium growth potential.

The insurer's performance is tied to government execution of the Economic Reconstruction and Recovery Plan, which targets ZAR 1.2 trillion in investment over five years—successful delivery would expand commercial and retail insurance demand.

- Energy outages: ~ZAR 45–50bn economic loss (2023–24)

- GDP growth: 0.6% in 2024, limiting premium expansion

- Recovery Plan: ZAR 1.2tn investment target over five years

Broad-Based Black Economic Empowerment Policy

As a major financial services player, Momentum Metropolitan must meet evolving B-BBEE codes and transformation targets; the Financial Sector Charter review in 2024 proposed increased procurement and ownership scoring that could affect its compliance metrics and client eligibility.

Compliance is a legal requirement and prerequisite for securing government contracts and maintaining its social license—Momentum reported a Level 2 contributor status in 2023, which supports access to preferential procurement.

Shifts in political rhetoric around ownership and procurement targets through 2025 require continuous strategic alignment across HR, procurement and M&A to protect revenue streams tied to public-sector business.

- 2023: Momentum reported Level 2 B-BBEE

- 2024: Financial Sector Charter review proposes tighter procurement/ownership targets

- Risk: loss of government contracts if non-compliant

Momentum Metropolitan outlook hinges on political stability, NHI and Eskom losses

Political stability of the 2024 Government of National Unity, NHI progress, SOE performance and B-BBEE/Financial Sector Charter reforms materially affect Momentum Metropolitan’s revenue, claims and access to public contracts; key metrics: GDP growth 0.6% (2024), private medical scheme membership ~8.6m (2024), non‑SA AUM R62.5bn (2024), Eskom-related economic loss ZAR45–50bn (2023–24).

| Metric | Value |

|---|---|

| GDP growth (2024) | 0.6% |

| Private medical scheme members (2024) | 8.6m |

| Non‑SA AUM (2024) | R62.5bn |

| Eskom economic loss (2023–24) | ZAR45–50bn |

What is included in the product

Explores how external macro-environmental factors uniquely affect Momentum Metropolitan Holdings across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific insights to identify risks and opportunities for executives, investors, and strategists.

Provides a concise, visually segmented PESTLE summary of Momentum Metropolitan Holdings that’s easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Interest Rate Cycle and Monetary Policy

The South African Reserve Bank’s policy rate at 8.25% (Feb 2026) directly affects Momentum Metropolitan’s investment income and liability valuations; higher rates boosted fixed-income yields, contributing to a 2025 investment return uptick of ~3.2% year-on-year, while also reducing demand for credit life products. A prolonged high-rate environment supports portfolio yields but suppresses single-premium sales; a shift to a cutting cycle could raise consumer spending yet compress margins on savings and guaranteed products.

Inflationary Pressure on Claims and Expenses

Persistent inflation, with South African CPI averaging 5.9% in 2024 and medical inflation near 8–10%, is lifting claims costs in Momentum Metropolitan’s short-term and health books; motor parts price inflation of c.12% in 2024 further increases motor claim severity. The group faces trade-offs raising premiums—Momentum’s 2024 short-term loss ratio rose to ~70% in parts of the book—against losing price-sensitive customers. Controlling opex, where wage and supplier cost inflation ran 6–9% in 2024, is critical to protect normalized earnings.

Low GDP Growth and Consumer Resilience

Subdued GDP growth in South Africa—0.7% in 2024 IMF estimate—constrains expansion of the total addressable market for Momentum Metropolitan's financial services, limiting new premium and asset-gathering opportunities.

High unemployment at 32.9% (Q4 2024, Stats SA) and stagnant real household incomes dampen demand for discretionary investments and life insurance, pressuring sales volumes and persistency.

The group’s performance hinges on gaining share in this low-growth environment via competitive pricing, digital distribution and product innovation as seen in its 2024 strategy to lift market penetration and protect margins.

Currency Exchange Rate Fluctuations

The volatility of the South African Rand, which depreciated about 6% vs the US dollar in 2024, affects Momentum Metropolitan Holdings by altering reported offshore earnings and raising costs for imported IT—pressure on margins for 2024/25 technology investments.

While a weaker Rand can boost the ZAR valuation of offshore assets, episodes of depreciation often reflect macro instability; Momentum uses hedging and geographic diversification to manage FX exposure.

- 2024 ZAR/USD move ~-6%: higher IT import costs

- Weaker Rand increases local value of offshore assets

- Hedging and geographic diversification used to mitigate risk

Capital Market Performance

Momentum Metropolitan’s fee income closely tracks JSE and global equity performance; a 10% rise in the JSE Top 40 in 2024 lifted AUM industry-wide, and Momentum reported AUM of ~R580bn in FY2024, boosting performance fees, while 2022-23 downturns showed vulnerability via capital outflows.

The group’s diversified portfolios—mix of cash, bonds, equities and alternatives—aim to limit volatility, with multi-asset mandates reducing drawdowns by an estimated 4–6% in stressed periods.

- FY2024 AUM ~R580bn

- JSE Top 40 +10% in 2024 (example market rebound)

- Diversification reduced drawdown ~4–6%

SARB hikes lift bond income as inflation, weak GDP and ZAR squeeze demand and costs

Higher SARB rates (8.25% Feb 2026) raised 2025 bond yields, aiding investment income; CPI 5.9% (2024) and medical inflation ~8–10% increased claims and costs; GDP ~0.7% (2024) and unemployment 32.9% cut demand; ZAR -6% vs USD (2024) hit IT costs but uplifted offshore AUM (FY2024 AUM ~R580bn).

| Metric | Value |

|---|---|

| SARB rate | 8.25% Feb 2026 |

| CPI 2024 | 5.9% |

| GDP 2024 | 0.7% |

| Unemployment Q4 2024 | 32.9% |

| ZAR vs USD 2024 | -6% |

| FY2024 AUM | ~R580bn |

Same Document Delivered

Momentum Metropolitan Holdings PESTLE Analysis

The preview shown here is the exact Momentum Metropolitan Holdings PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic analysis and decision-making.