Moncler PESTLE Analysis

Skip the Research. Get the Strategy.

Unlock how political shifts, economic trends, and evolving consumer preferences shape Moncler's strategy and risk profile with our concise PESTLE snapshot—then dive deeper with the full analysis for actionable insights. Purchase the complete PESTLE to get a ready-to-use, fully sourced report ideal for investors, consultants, and strategy teams.

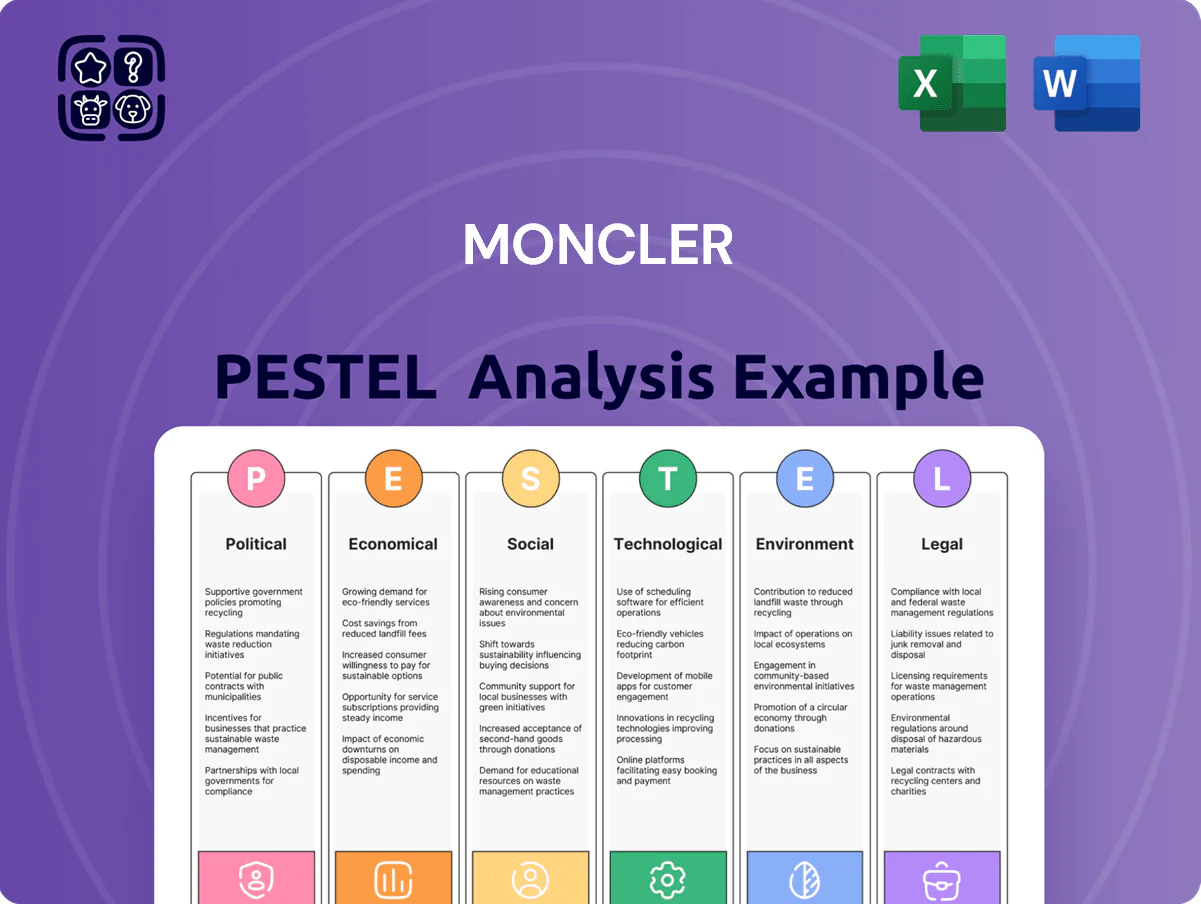

Political factors

Geopolitical Trade Relations

Moncler remains sensitive to EU-US-China trade tensions; in 2024 exports to China and the US accounted for roughly 30% and 28% of revenue respectively, so tariff shifts materially affect margins.

Increased tariffs or non-tariff barriers would raise landed costs—Moncler reported a gross margin of 66.3% in 2024, leaving limited cushion for price increases without hurting demand.

Management must adjust sourcing, pricing and hedging strategies to protect the ~€2.4bn FY 2024 net revenue and sustain competitive positioning in the global luxury market.

Stability in Key Regions

Political instability in the Middle East and Eastern Europe has weighed on luxury tourism and consumer confidence; global arrivals fell 45% in conflict-affected corridors in 2024, denting high-spend footfall in cities like Milan and Paris.

Moncler, which reported 2024 retail sales of €2.1bn, must monitor regional conflicts that could disrupt retail traffic in major fashion capitals where tourists account for an estimated 30–40% of luxury store sales.

Geographic diversification—Moncler's 2024 network included 240 directly operated stores across 35 countries—remains key to mitigating localized political shocks and smoothing revenue volatility.

Taxation and Luxury Levies

Government decisions on VAT hikes or luxury levies in markets like China or Brazil can cut demand quickly—China raised some consumption taxes affecting premium goods in 2024, and luxury segment sales growth slowed to 2% YoY in key cities. In Europe, proposals to tighten tax-free shopping for tourists could lower revenue at flagship stores—tourist spending accounted for ~18% of Moncler’s retail sales in 2023. Analysts model these policy risks into quarterly DTC margin forecasts, trimming near-term EBITDA by up to 150–200 bps under adverse scenarios.

Support for Made in Italy

The Italian government’s pro-fashion policies and 2024 incentives, including a reported €250m package for textile-tech and Made in Italy promotion, reinforce Moncler’s manufacturing base and protect its premium supply chain.

Tax credits and grants for domestic production lower operating costs and safeguard quality standards, supporting Moncler’s brand heritage and pricing power in luxury outerwear.

Political alignment creates a stable backdrop for long-term capital expenditure; Moncler invested €60m–€80m in Italian manufacturing capacity in 2023–24, benefiting from these measures.

- €250m national support (2024) for textiles

- €60m–€80m Moncler capex in Italy (2023–24)

- Incentives protect supply chain and premium quality

Global Regulatory Alignment

As Moncler sells in 70+ countries, aligning with varying trade policies and sanctions regimes is mandatory to protect 2024 revenues that rose 10% to €2.1bn and FY margins; breaches of export controls can halt shipments and hit sales rapidly.

Maintaining compliance with evolving EU, US and UK sanctions lists requires an advanced legal and political monitoring framework—Moncler’s 2024 compliance spend likely rose in line with industry averages (~0.5–1% of revenue).

Failure to adapt risks severe reputational, regulatory and operational costs, including fines, lost market access and supply-chain disruptions affecting inventory and Q4 sales peaks.

- Operates in 70+ countries; 2024 revenue €2.1bn (+10%)

- Compliance spend estimated ~0.5–1% of revenue

- Risks: fines, lost market access, supply-chain disruption

Moncler at Trade Crossroads: 58% Revenue in US/China, Margins & Growth at Risk

Moncler is exposed to EU-US-China trade tensions—China and US made up ~30% and ~28% of 2024 revenue—so tariffs and VAT/luxury levy changes can compress its 66.3% gross margin and trim FY2024 €2.4bn net revenue; geographic diversification (240 stores, 70+ countries) and €60–80m Italian capex mitigate localized shocks while compliance costs (~0.5–1% revenue) protect market access.

| Metric | 2024 |

|---|---|

| Revenue (net) | €2.4bn |

| Gross margin | 66.3% |

| China revenue share | ~30% |

| US revenue share | ~28% |

| Direct stores | 240 (35 countries) |

| Capex Italy (23–24) | €60–80m |

| Compliance spend est. | ~0.5–1% rev |

What is included in the product

Explores how external macro-environmental factors uniquely affect Moncler across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trends to highlight sector-specific risks and opportunities.

Condensed Moncler PESTLE insights that you can paste into presentations or meeting notes for quick alignment on external risks, market trends, and regulatory impacts.

Economic factors

Global Inflationary Pressures

Persistent global inflation—CPI at 6.8% in OECD nations in 2024—raises input costs for down, fabrics and logistics while eroding purchasing power among aspirational buyers. Moncler’s premium positioning and 2024 gross margin ~66% afford pricing power to pass through higher costs to wealthy clients. Still, sustained pressure on the middle class may constrain demand for Moncler’s entry-level lines and impact mid-market growth.

Currency Exchange Volatility

As Moncler reports in euros while earning ~38% of 2024 revenue in USD and ~12% in RMB, FX swings materially affect reported EBIT; a 5% EUR appreciation vs USD in 2024 would have reduced euro-reported sales by roughly 1.9%.

Currency moves also change regional price competitiveness—stronger yuan narrows margins in China, while USD strength can make products pricier in dollar markets.

Moncler discloses active hedging: forward contracts and options covered a significant portion of 2024 dollar exposures, stabilizing cash flows amid heightened 2023–24 forex volatility.

Economic Growth in Asia

China and Japan drive Moncler’s late-2025 top-line: Greater China accounted for ~34% of group sales in 2024 and Japan ~9%, making regional GDP and consumer sentiment critical. A 2024–25 Chinese growth slowdown (GDP growth easing to ~4.5% in 2024) or weaker luxury spending could cause sizeable revenue swings. Strategists monitor monthly retail sales, tourism arrivals, and regional PMI to adjust inventory and cut marketing quickly.

Interest Rate Environments

Central bank rate hikes since 2022 raised Moncler’s weighted average cost of debt and discounted future cash flows, pressuring valuations; ECB policy rates at 4.0% in Dec 2025 would materially lift discount rates versus 2021 lows near 0.0%.

Higher rates have cooled M&A and capex appetite across luxury peers—global luxury deal volume fell ~28% in 2023—while a stabilizing rate backdrop in late 2025 could prompt renewed store rollouts and IT/warehouse upgrades.

- WACD up with policy tightening; ECB ~4.0% (Dec 2025)

- Luxury M&A volume down ~28% (2023)

- Stabilizing rates late 2025 may revive store expansion

Consumer Confidence Trends

Consumer confidence among high-net-worth individuals strongly influences demand for Moncler’s discretionary outerwear; global UHNW household wealth rose 6.1% to about USD 31.5 trillion in 2024, supporting luxury spending resilience.

Moncler tracks consumer confidence indices and its own retail traffic—group retail sales grew 14% LFL in FY 2024—to forecast seasonal demand and align production cycles.

Luxury sector resilience often diverges from GDP: global personal luxury goods market grew ~8% in 2024 versus ~3% global GDP growth, necessitating specialized analysis.

- HNWI wealth +6.1% (2024)

- Moncler FY24 retail LFL +14%

- Personal luxury goods market +8% (2024)

Moncler: Strong margins and FX hedges cushion inflation and China exposure

Inflation (OECD CPI 6.8% 2024) raises input/logistics costs but Moncler’s ~66% gross margin and pricing power support pass-through; FX exposure (38% USD, 12% RMB) and hedging (2024 forwards/options) moderate reported EBIT volatility; Greater China ~34% and Japan ~9% of 2024 sales make regional GDP/consumer trends crucial; ECB rates ~4.0% (Dec 2025) lift WACC and damp M&A/capex.

| Metric | Value |

|---|---|

| Gross margin | ~66% |

| Revenue USD/RMB | 38% / 12% |

| Greater China sales | ~34% |

| OECD CPI 2024 | 6.8% |

| ECB rate Dec 2025 | ~4.0% |

Preview Before You Purchase

Moncler PESTLE Analysis

The preview shown here is the exact Moncler PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use.

No placeholders or teasers: the content, structure, and layout visible here are exactly what you’ll download immediately after buying.

This is the real, finished file—professionally structured and ready for analysis or presentation without further edits.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Unlock how political shifts, economic trends, and evolving consumer preferences shape Moncler's strategy and risk profile with our concise PESTLE snapshot—then dive deeper with the full analysis for actionable insights. Purchase the complete PESTLE to get a ready-to-use, fully sourced report ideal for investors, consultants, and strategy teams.

Political factors

Geopolitical Trade Relations

Moncler remains sensitive to EU-US-China trade tensions; in 2024 exports to China and the US accounted for roughly 30% and 28% of revenue respectively, so tariff shifts materially affect margins.

Increased tariffs or non-tariff barriers would raise landed costs—Moncler reported a gross margin of 66.3% in 2024, leaving limited cushion for price increases without hurting demand.

Management must adjust sourcing, pricing and hedging strategies to protect the ~€2.4bn FY 2024 net revenue and sustain competitive positioning in the global luxury market.

Stability in Key Regions

Political instability in the Middle East and Eastern Europe has weighed on luxury tourism and consumer confidence; global arrivals fell 45% in conflict-affected corridors in 2024, denting high-spend footfall in cities like Milan and Paris.

Moncler, which reported 2024 retail sales of €2.1bn, must monitor regional conflicts that could disrupt retail traffic in major fashion capitals where tourists account for an estimated 30–40% of luxury store sales.

Geographic diversification—Moncler's 2024 network included 240 directly operated stores across 35 countries—remains key to mitigating localized political shocks and smoothing revenue volatility.

Taxation and Luxury Levies

Government decisions on VAT hikes or luxury levies in markets like China or Brazil can cut demand quickly—China raised some consumption taxes affecting premium goods in 2024, and luxury segment sales growth slowed to 2% YoY in key cities. In Europe, proposals to tighten tax-free shopping for tourists could lower revenue at flagship stores—tourist spending accounted for ~18% of Moncler’s retail sales in 2023. Analysts model these policy risks into quarterly DTC margin forecasts, trimming near-term EBITDA by up to 150–200 bps under adverse scenarios.

Support for Made in Italy

The Italian government’s pro-fashion policies and 2024 incentives, including a reported €250m package for textile-tech and Made in Italy promotion, reinforce Moncler’s manufacturing base and protect its premium supply chain.

Tax credits and grants for domestic production lower operating costs and safeguard quality standards, supporting Moncler’s brand heritage and pricing power in luxury outerwear.

Political alignment creates a stable backdrop for long-term capital expenditure; Moncler invested €60m–€80m in Italian manufacturing capacity in 2023–24, benefiting from these measures.

- €250m national support (2024) for textiles

- €60m–€80m Moncler capex in Italy (2023–24)

- Incentives protect supply chain and premium quality

Global Regulatory Alignment

As Moncler sells in 70+ countries, aligning with varying trade policies and sanctions regimes is mandatory to protect 2024 revenues that rose 10% to €2.1bn and FY margins; breaches of export controls can halt shipments and hit sales rapidly.

Maintaining compliance with evolving EU, US and UK sanctions lists requires an advanced legal and political monitoring framework—Moncler’s 2024 compliance spend likely rose in line with industry averages (~0.5–1% of revenue).

Failure to adapt risks severe reputational, regulatory and operational costs, including fines, lost market access and supply-chain disruptions affecting inventory and Q4 sales peaks.

- Operates in 70+ countries; 2024 revenue €2.1bn (+10%)

- Compliance spend estimated ~0.5–1% of revenue

- Risks: fines, lost market access, supply-chain disruption

Moncler at Trade Crossroads: 58% Revenue in US/China, Margins & Growth at Risk

Moncler is exposed to EU-US-China trade tensions—China and US made up ~30% and ~28% of 2024 revenue—so tariffs and VAT/luxury levy changes can compress its 66.3% gross margin and trim FY2024 €2.4bn net revenue; geographic diversification (240 stores, 70+ countries) and €60–80m Italian capex mitigate localized shocks while compliance costs (~0.5–1% revenue) protect market access.

| Metric | 2024 |

|---|---|

| Revenue (net) | €2.4bn |

| Gross margin | 66.3% |

| China revenue share | ~30% |

| US revenue share | ~28% |

| Direct stores | 240 (35 countries) |

| Capex Italy (23–24) | €60–80m |

| Compliance spend est. | ~0.5–1% rev |

What is included in the product

Explores how external macro-environmental factors uniquely affect Moncler across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trends to highlight sector-specific risks and opportunities.

Condensed Moncler PESTLE insights that you can paste into presentations or meeting notes for quick alignment on external risks, market trends, and regulatory impacts.

Economic factors

Global Inflationary Pressures

Persistent global inflation—CPI at 6.8% in OECD nations in 2024—raises input costs for down, fabrics and logistics while eroding purchasing power among aspirational buyers. Moncler’s premium positioning and 2024 gross margin ~66% afford pricing power to pass through higher costs to wealthy clients. Still, sustained pressure on the middle class may constrain demand for Moncler’s entry-level lines and impact mid-market growth.

Currency Exchange Volatility

As Moncler reports in euros while earning ~38% of 2024 revenue in USD and ~12% in RMB, FX swings materially affect reported EBIT; a 5% EUR appreciation vs USD in 2024 would have reduced euro-reported sales by roughly 1.9%.

Currency moves also change regional price competitiveness—stronger yuan narrows margins in China, while USD strength can make products pricier in dollar markets.

Moncler discloses active hedging: forward contracts and options covered a significant portion of 2024 dollar exposures, stabilizing cash flows amid heightened 2023–24 forex volatility.

Economic Growth in Asia

China and Japan drive Moncler’s late-2025 top-line: Greater China accounted for ~34% of group sales in 2024 and Japan ~9%, making regional GDP and consumer sentiment critical. A 2024–25 Chinese growth slowdown (GDP growth easing to ~4.5% in 2024) or weaker luxury spending could cause sizeable revenue swings. Strategists monitor monthly retail sales, tourism arrivals, and regional PMI to adjust inventory and cut marketing quickly.

Interest Rate Environments

Central bank rate hikes since 2022 raised Moncler’s weighted average cost of debt and discounted future cash flows, pressuring valuations; ECB policy rates at 4.0% in Dec 2025 would materially lift discount rates versus 2021 lows near 0.0%.

Higher rates have cooled M&A and capex appetite across luxury peers—global luxury deal volume fell ~28% in 2023—while a stabilizing rate backdrop in late 2025 could prompt renewed store rollouts and IT/warehouse upgrades.

- WACD up with policy tightening; ECB ~4.0% (Dec 2025)

- Luxury M&A volume down ~28% (2023)

- Stabilizing rates late 2025 may revive store expansion

Consumer Confidence Trends

Consumer confidence among high-net-worth individuals strongly influences demand for Moncler’s discretionary outerwear; global UHNW household wealth rose 6.1% to about USD 31.5 trillion in 2024, supporting luxury spending resilience.

Moncler tracks consumer confidence indices and its own retail traffic—group retail sales grew 14% LFL in FY 2024—to forecast seasonal demand and align production cycles.

Luxury sector resilience often diverges from GDP: global personal luxury goods market grew ~8% in 2024 versus ~3% global GDP growth, necessitating specialized analysis.

- HNWI wealth +6.1% (2024)

- Moncler FY24 retail LFL +14%

- Personal luxury goods market +8% (2024)

Moncler: Strong margins and FX hedges cushion inflation and China exposure

Inflation (OECD CPI 6.8% 2024) raises input/logistics costs but Moncler’s ~66% gross margin and pricing power support pass-through; FX exposure (38% USD, 12% RMB) and hedging (2024 forwards/options) moderate reported EBIT volatility; Greater China ~34% and Japan ~9% of 2024 sales make regional GDP/consumer trends crucial; ECB rates ~4.0% (Dec 2025) lift WACC and damp M&A/capex.

| Metric | Value |

|---|---|

| Gross margin | ~66% |

| Revenue USD/RMB | 38% / 12% |

| Greater China sales | ~34% |

| OECD CPI 2024 | 6.8% |

| ECB rate Dec 2025 | ~4.0% |

Preview Before You Purchase

Moncler PESTLE Analysis

The preview shown here is the exact Moncler PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use.

No placeholders or teasers: the content, structure, and layout visible here are exactly what you’ll download immediately after buying.

This is the real, finished file—professionally structured and ready for analysis or presentation without further edits.