Monro PESTLE Analysis

Skip the Research. Get the Strategy.

Explore how political shifts, economic pressures, and tech advances are reshaping Monro’s prospects in our concise PESTLE snapshot—then unlock the full analysis for actionable strategies and risk forecasts tailored to investors and strategists. Buy the complete PESTLE now for the detailed insights you need to make smarter, faster decisions.

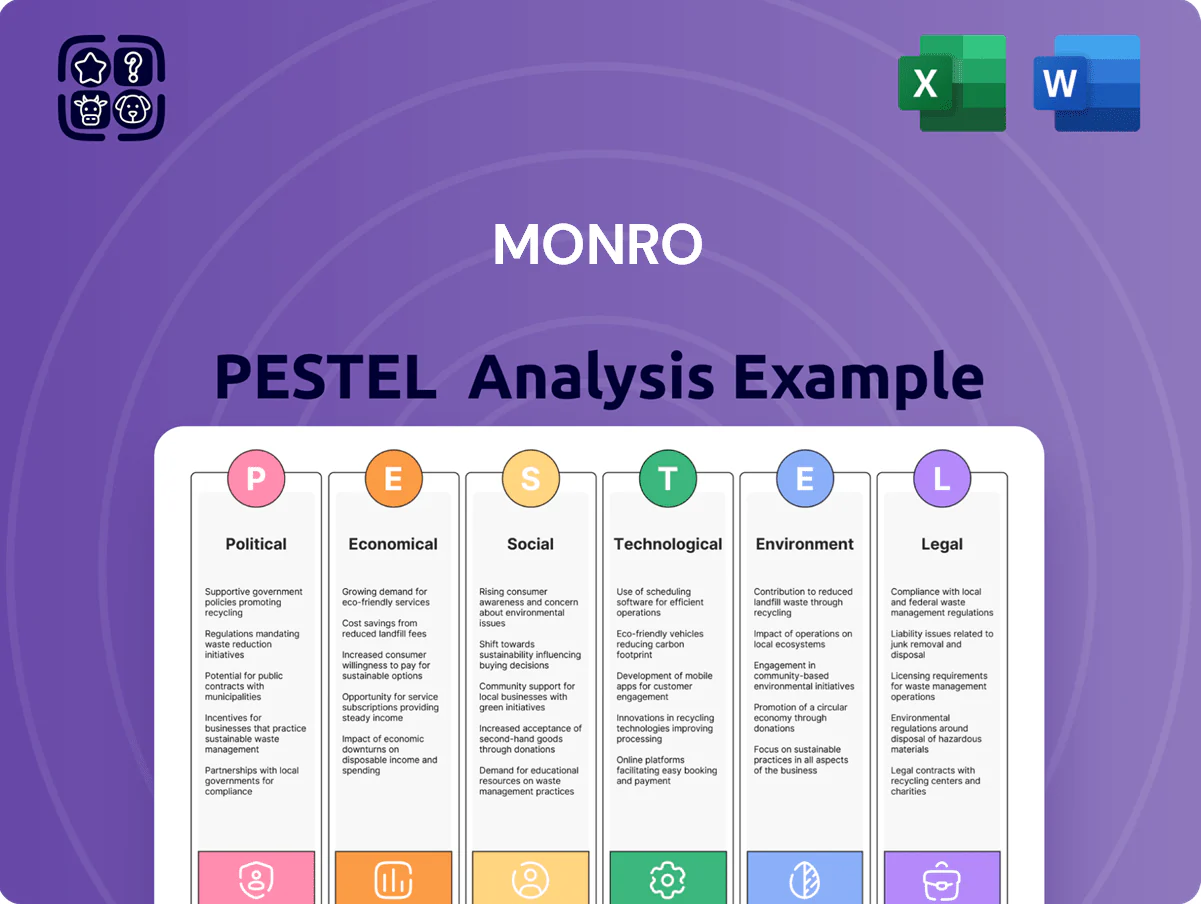

Political factors

Trade policy and tire tariffs

International trade agreements and tariffs on imported tires, especially from Southeast Asia and China, directly affect Monro’s procurement costs; U.S. duties rose to as high as 15% on some Chinese tire imports in 2024, pressuring input prices.

By late 2025 shifting trade alliances and protectionist measures have increased volatility, prompting Monro to diversify suppliers; inventory from non-China sources grew to 28% of tire purchases in FY2025.

These political decisions influence retail pricing and gross margins: Monro reported tire gross margins of 34.2% in FY2025, down 1.1 ppt year-over-year, partly due to tariff-driven cost pass-through limits.

Infrastructure investment legislation

Federal and state infrastructure funding — including the 2021 Bipartisan Infrastructure Law which allocated $110bn for roads and bridges and continued 2024–25 state bond programs — affects vehicle miles and wear, reducing some suspension claims but increasing overall miles-driven service demand.

Infrastructure packages increasingly fund EV charging; the US had ~185,000 public chargers as of end-2024, creating aftermarket EV service opportunities Monro can target for new revenue streams.

Heightened political focus on transportation safety has supported expansion of state mandatory inspection laws; states with strict inspection regimes see higher per-vehicle spend on undercarriage and safety services, directly benefiting Monro’s volumes.

Labor and wage regulations

Changes in federal and state minimum wages—26 states increased rates in 2024, with 2025 proposals pending—raise labor costs across Monro’s ~1,300 service centers, potentially adding millions to annual payroll given average technician wages near $22–$28/hr.

Stronger union protections and pro-labor administrations increase bargaining leverage, forcing Monro to balance higher compensation against 2024 gross margin pressure (U.S. Automotive Repair sector avg gross margin ~37%).

State certification mandates and ASE-related requirements narrow the talent pool; training investments and certification costs per technician (estimated $1,000–$3,000) affect staffing flexibility and operational budgets.

Corporate tax policy

Adjustments to corporate tax rates and capital expenditure depreciation rules directly affect Monro's net income and cash flow available for reinvestment; a 1 percentage point tax increase on Monro's 2024 effective tax rate (~22%) would reduce pre-tax margins and free cash flow.

By end-2025, federal and state green incentives—such as 2024 Inflation Reduction Act credits and potential state grants—could subsidize up to 30% of qualifying facility upgrade costs, improving ROI on shop modernization.

Monitoring fiscal policy shifts is essential for Monro's capital allocation and its 2025 expansion plans, given planned CAPEX of roughly $80–100 million annually and sensitivity to tax-driven cash flow changes.

- Tax rate moves alter net income and FCF

- Depreciation rules impact timing of deductions

- IRA and state credits may offset ~30% of green CAPEX

- Annual CAPEX ~$80–100M influences expansion

Automotive industry mandates

Government mandates phasing out internal combustion engines and tightening CAFE standards are accelerating EV adoption—global EV sales hit 14 million in 2023 and EVs reached ~13% of US new-vehicle sales in 2024, pressuring Monro to expand EV/hybrid service capabilities.

Political pressure to cut transport emissions forces Monro to transition from routine oil-change revenue (about 30% of some tire-and-service shops' aftermarket income) toward battery diagnostics, high-voltage training, and new tooling investments.

Aligning with these regulations is critical for Monro to retain market relevance as EVs rise; failure to adapt risks share loss amid a market shifting ~20–30% faster to electrification in key regions by 2025.

- EVs ~13% US new sales (2024)

- Global EV sales 14M (2023)

- Service mix shift: oil-change revenue risk

- Need for battery diagnostics, HV training, tooling

Tariff-driven tire costs squeeze margins as EV infrastructure and wages reshape demand

Political factors: tariffs on Chinese/Southeast Asian tires (U.S. duties up to 15% in 2024) raised input costs; FY2025 non-China tire sourcing grew to 28%, tire gross margin fell to 34.2%. Infrastructure and IRA incentives (185,000 public chargers end-2024; up to 30% green CAPEX offsets) shift demand toward EV services. Wage increases (26 states in 2024) and certification costs ($1–3k/tech) raise operating expenses.

| Metric | Value |

|---|---|

| Tire gross margin FY2025 | 34.2% |

| Non-China tire purchases FY2025 | 28% |

| Public EV chargers (end-2024) | ~185,000 |

| States raising wages (2024) | 26 |

What is included in the product

Explores how macro-environmental factors uniquely affect Monro across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven sub-points and forward-looking insights to inform strategy, risk mitigation, and investor communications.

Provides a concise, visually segmented PESTLE summary for Monro that can be dropped into presentations or planning sessions to quickly align teams on external risks and market positioning.

Economic factors

Average vehicle age trends

The U.S. average vehicle age rose to a record 12.5 years in 2024, boosting demand for Monro’s service lines as owners delay purchases; with new car transaction prices near $47,000 in 2025, consumers opt to maintain existing vehicles. This trend supports steady revenue for high-margin repairs—brakes, exhaust, engine diagnostics—which accounted for over 60% of Monro’s service revenue in recent quarters, reinforcing long-term service demand.

Interest rate environment

Fluctuations in interest rates alter Monro Inc.’s cost of debt for acquisitions and store renovations; after the US Fed funds rate rose from near-zero in 2021 to a 5.25–5.50% target range by Dec 2023–2024, Monro’s borrowing costs and capex financing face upward pressure.

Inflationary pressure on parts

Persistent inflation in parts and raw materials—rubber prices up about 14% YoY through 2025—forced Monro to adopt sophisticated pricing, targeting a 160–180 bps gross margin protection while monitoring demand elasticity to avoid share loss to independents.

As of end-2025 Monro reported supply-chain cost mitigation via bulk purchasing and vendor contracts covering roughly 55% of volume, reducing input-cost volatility and supporting 2025 adjusted EBITDA margins near 11.5%.

Consumer disposable income

Consumer disposable income influences Monro’s mix of preventative maintenance versus emergency repairs; US median household disposable income was about $64,000 in 2023, and declines in 2024–2025 regional employment shocks correlated with lower service frequency.

In downturns customers delay non-essential services like wheel alignments or premium tires, reducing higher-margin sales and pressuring same-store sales growth—Monro reported a 2.5% comps decline in parts/other categories in 2023.

Monro monitors regional economic indicators and adjusts promotions and financing—offering deferred-payment plans and targeted discounts in high-unemployment areas where unemployment rates rose to 5.0% in some regions by 2024.

- Disposable income tied to service frequency; median US disposable income ~$64k (2023)

- Downturns cut non-essential services; Monro saw 2.5% decline in parts/other comps (2023)

- Regional tailoring: financing offers, promos in areas with unemployment up to ~5.0% (2024)

Fuel price volatility

Fuel price volatility indirectly affects Monro by changing vehicle miles traveled; US average retail gasoline rose to about 3.70 USD/gal in 2024 versus 3.53 USD/gal in 2023, which historically reduced discretionary driving and slowed tire wear.

Monro’s same-store sales have correlated with miles driven; a 1–2% drop in VMT can reduce tire/maintenance demand noticeably, tying firm performance to energy market stability.

- High fuel prices → lower VMT → reduced tire wear and routine repairs

- 2024 US avg gas ≈ 3.70 USD/gal, up from 2023 ≈ 3.53 USD/gal

- Monro revenue sensitive to short-term VMT fluctuations

Aging fleet, high prices boost service demand as inflation and rates squeeze margins

Rising average vehicle age (12.5 years in 2024) and high new-car prices (~$47k in 2025) support service demand; Monro’s 2025 adjusted EBITDA ~11.5% aided by 55% vendor-covered volumes. Inflation raised parts costs (~+14% rubber YoY) and borrowing costs after Fed rates reached 5.25–5.50% (2024), pressuring margins and capex.

| Metric | Value |

|---|---|

| Avg vehicle age | 12.5 yrs (2024) |

| New-car price | $47,000 (2025) |

| Rubber costs | +14% YoY (2025) |

| Vendor-covered volume | 55% (2025) |

| Adj. EBITDA margin | ~11.5% (2025) |

| Fed funds | 5.25–5.50% (2024) |

Preview Before You Purchase

Monro PESTLE Analysis

The preview shown here is the exact Monro PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Explore how political shifts, economic pressures, and tech advances are reshaping Monro’s prospects in our concise PESTLE snapshot—then unlock the full analysis for actionable strategies and risk forecasts tailored to investors and strategists. Buy the complete PESTLE now for the detailed insights you need to make smarter, faster decisions.

Political factors

Trade policy and tire tariffs

International trade agreements and tariffs on imported tires, especially from Southeast Asia and China, directly affect Monro’s procurement costs; U.S. duties rose to as high as 15% on some Chinese tire imports in 2024, pressuring input prices.

By late 2025 shifting trade alliances and protectionist measures have increased volatility, prompting Monro to diversify suppliers; inventory from non-China sources grew to 28% of tire purchases in FY2025.

These political decisions influence retail pricing and gross margins: Monro reported tire gross margins of 34.2% in FY2025, down 1.1 ppt year-over-year, partly due to tariff-driven cost pass-through limits.

Infrastructure investment legislation

Federal and state infrastructure funding — including the 2021 Bipartisan Infrastructure Law which allocated $110bn for roads and bridges and continued 2024–25 state bond programs — affects vehicle miles and wear, reducing some suspension claims but increasing overall miles-driven service demand.

Infrastructure packages increasingly fund EV charging; the US had ~185,000 public chargers as of end-2024, creating aftermarket EV service opportunities Monro can target for new revenue streams.

Heightened political focus on transportation safety has supported expansion of state mandatory inspection laws; states with strict inspection regimes see higher per-vehicle spend on undercarriage and safety services, directly benefiting Monro’s volumes.

Labor and wage regulations

Changes in federal and state minimum wages—26 states increased rates in 2024, with 2025 proposals pending—raise labor costs across Monro’s ~1,300 service centers, potentially adding millions to annual payroll given average technician wages near $22–$28/hr.

Stronger union protections and pro-labor administrations increase bargaining leverage, forcing Monro to balance higher compensation against 2024 gross margin pressure (U.S. Automotive Repair sector avg gross margin ~37%).

State certification mandates and ASE-related requirements narrow the talent pool; training investments and certification costs per technician (estimated $1,000–$3,000) affect staffing flexibility and operational budgets.

Corporate tax policy

Adjustments to corporate tax rates and capital expenditure depreciation rules directly affect Monro's net income and cash flow available for reinvestment; a 1 percentage point tax increase on Monro's 2024 effective tax rate (~22%) would reduce pre-tax margins and free cash flow.

By end-2025, federal and state green incentives—such as 2024 Inflation Reduction Act credits and potential state grants—could subsidize up to 30% of qualifying facility upgrade costs, improving ROI on shop modernization.

Monitoring fiscal policy shifts is essential for Monro's capital allocation and its 2025 expansion plans, given planned CAPEX of roughly $80–100 million annually and sensitivity to tax-driven cash flow changes.

- Tax rate moves alter net income and FCF

- Depreciation rules impact timing of deductions

- IRA and state credits may offset ~30% of green CAPEX

- Annual CAPEX ~$80–100M influences expansion

Automotive industry mandates

Government mandates phasing out internal combustion engines and tightening CAFE standards are accelerating EV adoption—global EV sales hit 14 million in 2023 and EVs reached ~13% of US new-vehicle sales in 2024, pressuring Monro to expand EV/hybrid service capabilities.

Political pressure to cut transport emissions forces Monro to transition from routine oil-change revenue (about 30% of some tire-and-service shops' aftermarket income) toward battery diagnostics, high-voltage training, and new tooling investments.

Aligning with these regulations is critical for Monro to retain market relevance as EVs rise; failure to adapt risks share loss amid a market shifting ~20–30% faster to electrification in key regions by 2025.

- EVs ~13% US new sales (2024)

- Global EV sales 14M (2023)

- Service mix shift: oil-change revenue risk

- Need for battery diagnostics, HV training, tooling

Tariff-driven tire costs squeeze margins as EV infrastructure and wages reshape demand

Political factors: tariffs on Chinese/Southeast Asian tires (U.S. duties up to 15% in 2024) raised input costs; FY2025 non-China tire sourcing grew to 28%, tire gross margin fell to 34.2%. Infrastructure and IRA incentives (185,000 public chargers end-2024; up to 30% green CAPEX offsets) shift demand toward EV services. Wage increases (26 states in 2024) and certification costs ($1–3k/tech) raise operating expenses.

| Metric | Value |

|---|---|

| Tire gross margin FY2025 | 34.2% |

| Non-China tire purchases FY2025 | 28% |

| Public EV chargers (end-2024) | ~185,000 |

| States raising wages (2024) | 26 |

What is included in the product

Explores how macro-environmental factors uniquely affect Monro across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven sub-points and forward-looking insights to inform strategy, risk mitigation, and investor communications.

Provides a concise, visually segmented PESTLE summary for Monro that can be dropped into presentations or planning sessions to quickly align teams on external risks and market positioning.

Economic factors

Average vehicle age trends

The U.S. average vehicle age rose to a record 12.5 years in 2024, boosting demand for Monro’s service lines as owners delay purchases; with new car transaction prices near $47,000 in 2025, consumers opt to maintain existing vehicles. This trend supports steady revenue for high-margin repairs—brakes, exhaust, engine diagnostics—which accounted for over 60% of Monro’s service revenue in recent quarters, reinforcing long-term service demand.

Interest rate environment

Fluctuations in interest rates alter Monro Inc.’s cost of debt for acquisitions and store renovations; after the US Fed funds rate rose from near-zero in 2021 to a 5.25–5.50% target range by Dec 2023–2024, Monro’s borrowing costs and capex financing face upward pressure.

Inflationary pressure on parts

Persistent inflation in parts and raw materials—rubber prices up about 14% YoY through 2025—forced Monro to adopt sophisticated pricing, targeting a 160–180 bps gross margin protection while monitoring demand elasticity to avoid share loss to independents.

As of end-2025 Monro reported supply-chain cost mitigation via bulk purchasing and vendor contracts covering roughly 55% of volume, reducing input-cost volatility and supporting 2025 adjusted EBITDA margins near 11.5%.

Consumer disposable income

Consumer disposable income influences Monro’s mix of preventative maintenance versus emergency repairs; US median household disposable income was about $64,000 in 2023, and declines in 2024–2025 regional employment shocks correlated with lower service frequency.

In downturns customers delay non-essential services like wheel alignments or premium tires, reducing higher-margin sales and pressuring same-store sales growth—Monro reported a 2.5% comps decline in parts/other categories in 2023.

Monro monitors regional economic indicators and adjusts promotions and financing—offering deferred-payment plans and targeted discounts in high-unemployment areas where unemployment rates rose to 5.0% in some regions by 2024.

- Disposable income tied to service frequency; median US disposable income ~$64k (2023)

- Downturns cut non-essential services; Monro saw 2.5% decline in parts/other comps (2023)

- Regional tailoring: financing offers, promos in areas with unemployment up to ~5.0% (2024)

Fuel price volatility

Fuel price volatility indirectly affects Monro by changing vehicle miles traveled; US average retail gasoline rose to about 3.70 USD/gal in 2024 versus 3.53 USD/gal in 2023, which historically reduced discretionary driving and slowed tire wear.

Monro’s same-store sales have correlated with miles driven; a 1–2% drop in VMT can reduce tire/maintenance demand noticeably, tying firm performance to energy market stability.

- High fuel prices → lower VMT → reduced tire wear and routine repairs

- 2024 US avg gas ≈ 3.70 USD/gal, up from 2023 ≈ 3.53 USD/gal

- Monro revenue sensitive to short-term VMT fluctuations

Aging fleet, high prices boost service demand as inflation and rates squeeze margins

Rising average vehicle age (12.5 years in 2024) and high new-car prices (~$47k in 2025) support service demand; Monro’s 2025 adjusted EBITDA ~11.5% aided by 55% vendor-covered volumes. Inflation raised parts costs (~+14% rubber YoY) and borrowing costs after Fed rates reached 5.25–5.50% (2024), pressuring margins and capex.

| Metric | Value |

|---|---|

| Avg vehicle age | 12.5 yrs (2024) |

| New-car price | $47,000 (2025) |

| Rubber costs | +14% YoY (2025) |

| Vendor-covered volume | 55% (2025) |

| Adj. EBITDA margin | ~11.5% (2025) |

| Fed funds | 5.25–5.50% (2024) |

Preview Before You Purchase

Monro PESTLE Analysis

The preview shown here is the exact Monro PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.