Montrose SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Montrose shows solid niche positioning with recurring revenue and strong client relationships, yet faces margin pressure from rising costs and intensified competition; our full SWOT unpacks these dynamics with evidence-based implications and strategic options. Purchase the complete SWOT analysis to receive a professionally formatted Word report and editable Excel matrix—perfect for investors, consultants, and executives needing actionable, presentation-ready insights.

Strengths

Comprehensive Service Portfolio

Montrose offers a full suite of environmental services—air quality testing, water treatment, and soil remediation—enabling cross-sell and larger contracts; in 2024 these integrated services helped drive Montrose Environmental Group’s revenue to $1.2 billion, up 9% year-over-year.

Proven M&A Execution

Montrose has repeatedly bought niche environmental firms—completing 28 acquisitions from 2018–2025—expanding into 12 new states and three countries; deals were mostly accretive, lifting adjusted EBITDA margin from 15.2% in 2019 to 18.7% in 2024. These bolt-ons added specialized IP in air quality and industrial hygiene, helping Montrose scale revenue from $420m (2018) to $1.1bn (2024) and cement its role as a consolidator in a fragmented market.

Strong Regulatory Expertise

Montrose Environmental Group keeps a deep bench of technical experts who navigate local, state, and federal environmental regulations, supporting clients across 50+ U.S. jurisdictions and 7 countries as of 2025.

Their PFAS (per- and polyfluoroalkyl substances) compliance teams helped clients avoid regulatory penalties totaling an estimated $12–18 million in 2024 by implementing treatment and monitoring plans.

Montrose’s ability to interpret emerging rules and deploy remediation reduces client legal risk and protects revenue, helping retain long-term contracts that generated roughly 65% of service revenue in 2024.

Resilient Recurring Revenue

A large share of Montrose Environmental Group’s revenue comes from multi-year contracts and legally mandated recurring testing, creating stable, predictable cash flow—Montrose reported 72% recurring revenue in FY2024 (ended Dec 31, 2024).

That recurring base helped the company sustain adjusted EBITDA margins of ~15% in 2024 despite soft markets, insulating it from short-term economic swings.

Environmental compliance is mission-critical, so demand for testing and monitoring stays high across cycles; Montrose’s backlog was $640 million at year-end 2024, underscoring contract visibility.

- 72% recurring revenue (FY2024)

- $640M backlog (Dec 31, 2024)

Proprietary Technology Solutions

Montrose: $1.2B revenue, 28 acquisitions, 72% recurring, 18.7% EBITDA—R&D fuels premium growth

Montrose’s integrated services and 28 acquisitions (2018–2025) grew revenue to $1.2B in 2024 and lifted adjusted EBITDA to ~18.7% from 15.2% (2019→2024), with 72% recurring revenue and a $640M backlog at Dec 31, 2024; >$25M R&D (2025) cuts field-to-report ~40% and reduces on-site hours ~15%, enabling premium pricing and strong retention.

| Metric | Value |

|---|---|

| Revenue (2024) | $1.2B |

| Recurring rev (FY2024) | 72% |

| Backlog (Dec 31, 2024) | $640M |

| Adj. EBITDA margin (2024) | ~18.7% |

| Acquisitions (2018–2025) | 28 |

| R&D spend (2025) | >$25M |

What is included in the product

Provides a clear SWOT framework for analyzing Montrose’s business strategy, highlighting internal capabilities, market strengths, operational gaps, growth drivers, and external opportunities and risks shaping its competitive position.

Delivers a concise Montrose SWOT summary for rapid strategic alignment and stakeholder-ready presentations.

Weaknesses

High Financial Leverage

Montrose has financed rapid acquisitions with heavy debt, pushing net leverage to about 4.1x LTM adjusted EBITDA as of Q3 2025, which leaves a highly leveraged balance sheet.

Annual interest expense rose to roughly $220 million in 2024, compressing net margins and reducing funds for organic investments or dividends.

Servicing this debt is a constant executive focus, and rising U.S. rates since 2022 have increased refinancing risk and interest volatility.

Integration Complexity Risks

Human Capital Dependency

The business depends on specialized environmental engineers and scientists; 62% of Montrose’s billable hours in 2024 came from staff with advanced certifications, raising operational risk if they leave.

Intense sector competition pushed average hiring costs up 18% in 2023–24 and wage inflation raised technical salaries by ~10%, squeezing margins.

Loss of top experts would hit project delivery: projects requiring niche permits and modeling could see timelines slip by 30% and revenue drop per project by an estimated $120k.

Geographic Concentration Issues

Despite expansion, Montrose Environmental Group reported about 72% of 2024 revenue from North America, leaving it exposed to U.S. economic swings and changes in federal or state environmental policy that could cut demand for remediation and consulting services.

Lack of broader international diversification limits access to higher-growth markets in APAC and LATAM, where CAGR for environmental services was ~8–10% in 2023–24 versus ~3–4% in North America.

- 72% revenue from North America (2024)

- High sensitivity to U.S. policy shifts

- Missed APAC/LATAM growth ~8–10% CAGR

Variable Project Margins

Montrose's use of fixed-price contracts exposes it to margin compression when unexpected technical issues or supply-chain delays raise costs; in 2024 the company reported a 210 basis-point decline in gross margin on projects with cost overruns, increasing quarterly earnings volatility.

If project costs exceed estimates Montrose absorbs the loss, contributing to a 12% swing in quarterly operating income in FY2024; strengthening project management and cost estimating is a priority to stabilize margins.

- Fixed-price risk: higher cost exposure

- 2024: 210 bps gross margin hit on overrun projects

- FY2024: 12% quarterly operating income swing

- Action: better PM and cost-estimation needed

Heavy M&A lifts leverage to 4.1x, margin squeeze and refi risk amid integration strain

Heavy M&A debt raised net leverage to ~4.1x LTM EBITDA (Q3 2025) and interest expense ~ $220M (2024), squeezing margins and refi risk; 12 deals since 2021 created integration strain, 8% higher turnover in acquired units (2024) and risked 6–9% slip in FY2025 synergies; 72% revenue from North America (2024) limits growth exposure; fixed-price overruns cut gross margin by 210bps in 2024.

| Metric | Value |

|---|---|

| Net leverage | 4.1x (Q3 2025) |

| Interest expense | $220M (2024) |

| Revenue NA | 72% (2024) |

| Margin hit on overruns | 210bps (2024) |

What You See Is What You Get

Montrose SWOT Analysis

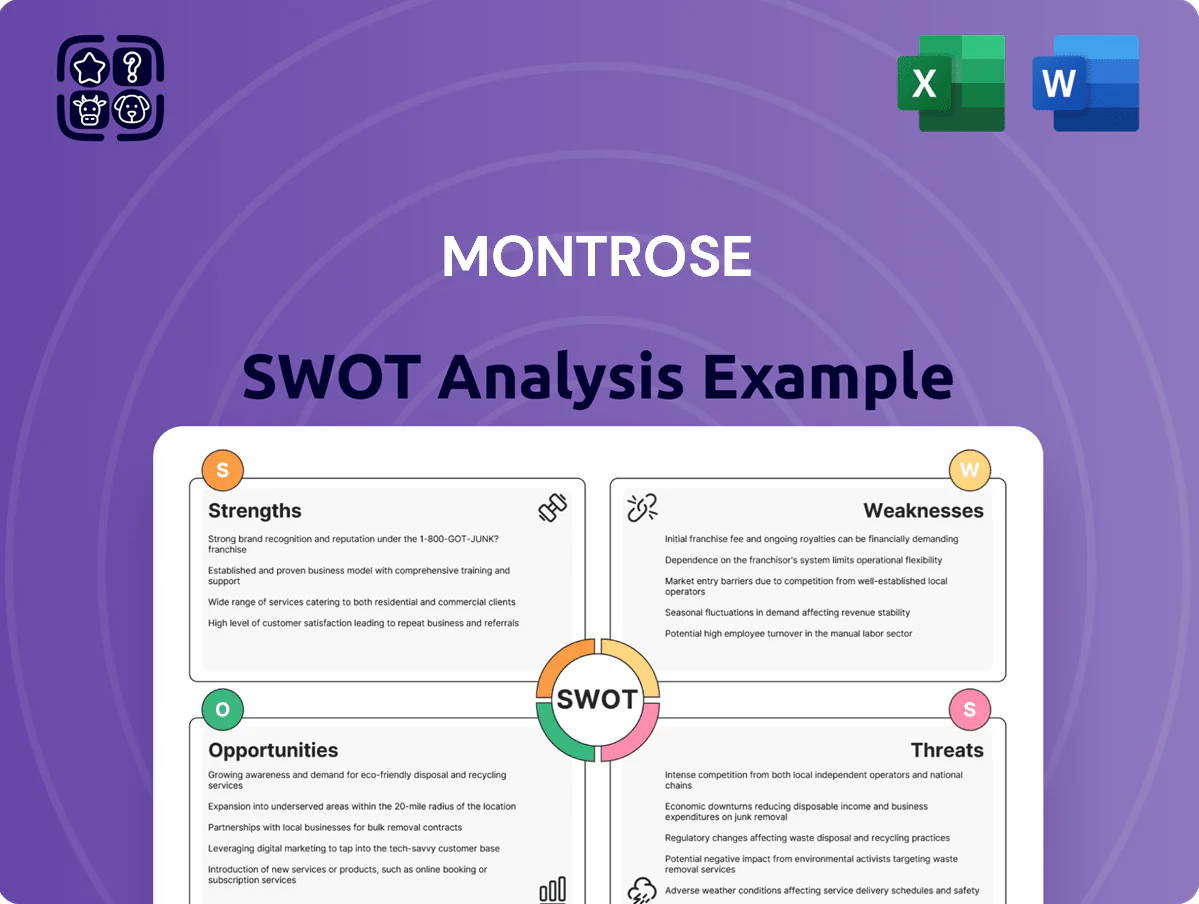

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is pulled from the final, editable file. You’re viewing a live preview of the real analysis document; the complete, detailed version is unlocked after checkout. Get a look now—buy to download the entire report immediately.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Insightful Decisions Backed by Expert Research

Montrose shows solid niche positioning with recurring revenue and strong client relationships, yet faces margin pressure from rising costs and intensified competition; our full SWOT unpacks these dynamics with evidence-based implications and strategic options. Purchase the complete SWOT analysis to receive a professionally formatted Word report and editable Excel matrix—perfect for investors, consultants, and executives needing actionable, presentation-ready insights.

Strengths

Comprehensive Service Portfolio

Montrose offers a full suite of environmental services—air quality testing, water treatment, and soil remediation—enabling cross-sell and larger contracts; in 2024 these integrated services helped drive Montrose Environmental Group’s revenue to $1.2 billion, up 9% year-over-year.

Proven M&A Execution

Montrose has repeatedly bought niche environmental firms—completing 28 acquisitions from 2018–2025—expanding into 12 new states and three countries; deals were mostly accretive, lifting adjusted EBITDA margin from 15.2% in 2019 to 18.7% in 2024. These bolt-ons added specialized IP in air quality and industrial hygiene, helping Montrose scale revenue from $420m (2018) to $1.1bn (2024) and cement its role as a consolidator in a fragmented market.

Strong Regulatory Expertise

Montrose Environmental Group keeps a deep bench of technical experts who navigate local, state, and federal environmental regulations, supporting clients across 50+ U.S. jurisdictions and 7 countries as of 2025.

Their PFAS (per- and polyfluoroalkyl substances) compliance teams helped clients avoid regulatory penalties totaling an estimated $12–18 million in 2024 by implementing treatment and monitoring plans.

Montrose’s ability to interpret emerging rules and deploy remediation reduces client legal risk and protects revenue, helping retain long-term contracts that generated roughly 65% of service revenue in 2024.

Resilient Recurring Revenue

A large share of Montrose Environmental Group’s revenue comes from multi-year contracts and legally mandated recurring testing, creating stable, predictable cash flow—Montrose reported 72% recurring revenue in FY2024 (ended Dec 31, 2024).

That recurring base helped the company sustain adjusted EBITDA margins of ~15% in 2024 despite soft markets, insulating it from short-term economic swings.

Environmental compliance is mission-critical, so demand for testing and monitoring stays high across cycles; Montrose’s backlog was $640 million at year-end 2024, underscoring contract visibility.

- 72% recurring revenue (FY2024)

- $640M backlog (Dec 31, 2024)

Proprietary Technology Solutions

Montrose: $1.2B revenue, 28 acquisitions, 72% recurring, 18.7% EBITDA—R&D fuels premium growth

Montrose’s integrated services and 28 acquisitions (2018–2025) grew revenue to $1.2B in 2024 and lifted adjusted EBITDA to ~18.7% from 15.2% (2019→2024), with 72% recurring revenue and a $640M backlog at Dec 31, 2024; >$25M R&D (2025) cuts field-to-report ~40% and reduces on-site hours ~15%, enabling premium pricing and strong retention.

| Metric | Value |

|---|---|

| Revenue (2024) | $1.2B |

| Recurring rev (FY2024) | 72% |

| Backlog (Dec 31, 2024) | $640M |

| Adj. EBITDA margin (2024) | ~18.7% |

| Acquisitions (2018–2025) | 28 |

| R&D spend (2025) | >$25M |

What is included in the product

Provides a clear SWOT framework for analyzing Montrose’s business strategy, highlighting internal capabilities, market strengths, operational gaps, growth drivers, and external opportunities and risks shaping its competitive position.

Delivers a concise Montrose SWOT summary for rapid strategic alignment and stakeholder-ready presentations.

Weaknesses

High Financial Leverage

Montrose has financed rapid acquisitions with heavy debt, pushing net leverage to about 4.1x LTM adjusted EBITDA as of Q3 2025, which leaves a highly leveraged balance sheet.

Annual interest expense rose to roughly $220 million in 2024, compressing net margins and reducing funds for organic investments or dividends.

Servicing this debt is a constant executive focus, and rising U.S. rates since 2022 have increased refinancing risk and interest volatility.

Integration Complexity Risks

Human Capital Dependency

The business depends on specialized environmental engineers and scientists; 62% of Montrose’s billable hours in 2024 came from staff with advanced certifications, raising operational risk if they leave.

Intense sector competition pushed average hiring costs up 18% in 2023–24 and wage inflation raised technical salaries by ~10%, squeezing margins.

Loss of top experts would hit project delivery: projects requiring niche permits and modeling could see timelines slip by 30% and revenue drop per project by an estimated $120k.

Geographic Concentration Issues

Despite expansion, Montrose Environmental Group reported about 72% of 2024 revenue from North America, leaving it exposed to U.S. economic swings and changes in federal or state environmental policy that could cut demand for remediation and consulting services.

Lack of broader international diversification limits access to higher-growth markets in APAC and LATAM, where CAGR for environmental services was ~8–10% in 2023–24 versus ~3–4% in North America.

- 72% revenue from North America (2024)

- High sensitivity to U.S. policy shifts

- Missed APAC/LATAM growth ~8–10% CAGR

Variable Project Margins

Montrose's use of fixed-price contracts exposes it to margin compression when unexpected technical issues or supply-chain delays raise costs; in 2024 the company reported a 210 basis-point decline in gross margin on projects with cost overruns, increasing quarterly earnings volatility.

If project costs exceed estimates Montrose absorbs the loss, contributing to a 12% swing in quarterly operating income in FY2024; strengthening project management and cost estimating is a priority to stabilize margins.

- Fixed-price risk: higher cost exposure

- 2024: 210 bps gross margin hit on overrun projects

- FY2024: 12% quarterly operating income swing

- Action: better PM and cost-estimation needed

Heavy M&A lifts leverage to 4.1x, margin squeeze and refi risk amid integration strain

Heavy M&A debt raised net leverage to ~4.1x LTM EBITDA (Q3 2025) and interest expense ~ $220M (2024), squeezing margins and refi risk; 12 deals since 2021 created integration strain, 8% higher turnover in acquired units (2024) and risked 6–9% slip in FY2025 synergies; 72% revenue from North America (2024) limits growth exposure; fixed-price overruns cut gross margin by 210bps in 2024.

| Metric | Value |

|---|---|

| Net leverage | 4.1x (Q3 2025) |

| Interest expense | $220M (2024) |

| Revenue NA | 72% (2024) |

| Margin hit on overruns | 210bps (2024) |

What You See Is What You Get

Montrose SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is pulled from the final, editable file. You’re viewing a live preview of the real analysis document; the complete, detailed version is unlocked after checkout. Get a look now—buy to download the entire report immediately.