Morita Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

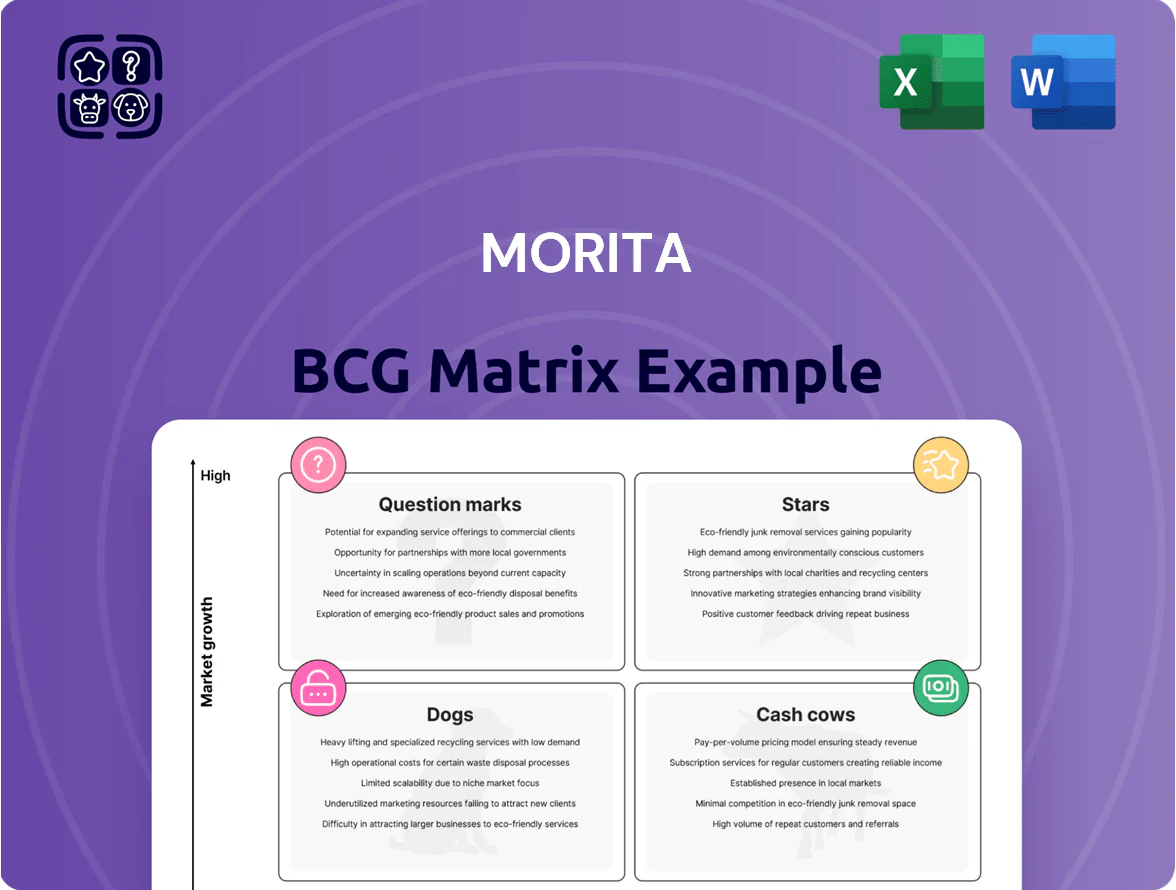

The Morita BCG Matrix offers a concise snapshot of product portfolios—mapping market share and growth to reveal Stars, Cash Cows, Question Marks, and Dogs—helping you spot where to invest, harvest, or divest. This preview highlights core placements, but the full BCG Matrix delivers quadrant-level data, prioritized strategic moves, and actionable recommendations tailored to Morita’s market dynamics. Purchase the complete report to get editable Word and Excel files, rich commentary, and a ready-to-use roadmap for smarter capital allocation and product strategy.

Stars

Electric Fire Fighting Vehicles

As of late 2025 demand for zero-emission emergency vehicles surged—global municipal procurement for electric fire trucks rose ~42% YoY—driven by carbon neutrality targets; Morita leads this niche by embedding proprietary high-energy battery packs into heavy-duty chassis.

Morita is scaling production with a ¥30 billion (≈$200M) capex program to fulfill international orders from eco-conscious cities in Europe and Japan.

These electric units are a high-growth Stars quadrant play but need sustained marketing spend to defend premium pricing and achieve estimated 25% market share by 2027.

Smart Disaster Management Systems

Morita’s Smart Disaster Management Systems sit as a Star: they hold a leading share in the IoT disaster-prevention market, which McKinsey estimated at $6.4B globally in 2025 and growing ~18% CAGR. These AI-driven platforms cut city response times by up to 35% in pilot deployments and optimize resource allocation via real-time sensors and cloud analytics. The segment’s double-digit growth fuels revenue upside but burned ~$42M in R&D and cloud spend in 2025, pressuring free cash flow. If Morita sustains its tech lead, these systems could be the company’s main profit engine over 2026–2035.

Advanced Plastic Recycling Plants

As 2025 circular-economy rules tighten, Morita’s Advanced Plastic Recycling Plants are Stars: revenues rose 38% in 2024–25 to ¥46.2bn, driven by demand for automated sorting of mixed polymers.

The environmental division leads with AI-driven optical sorters that recover 92% of PET/HDPE blends, but R&D spend equals 14% of unit sales to match material-science advances.

High cash generation is offset by heavy reinvestment; free cash flow margin sits near 6% as capital expenditures run at ¥8.4bn annually to secure long-term dominance.

Southeast Asian Fire-Fighting Expansion

Morita dominates Vietnam and Indonesia, where urban infrastructure spending rose 9.8% in 2024, gaining ~32% market share vs ~18% for European rivals; localized plants cut lead times by 25% and lowered costs 14% YoY.

Continued capex into distribution is required to repel 10–15% cheaper regional entrants and to absorb 120k units/year excess manufacturing capacity.

- 2024 urban infra growth 9.8%

- Morita market share ~32%

- Cost reduction 14% YoY

- Excess capacity 120k units/yr

Next-Generation Aerial Ladders

Next-Generation Aerial Ladders sit in Morita’s Cash Cow quadrant: global high-rise demand keeps segment revenue growth at ~6–8% annually while Morita holds ~42% market share in premium ladder trucks as of 2025, driven by superior engineering and reliability.

Promotion costs run ~5–7% of unit price to support exports to APAC/EU/ME, offsetting a flat domestic market; R&D spend equals ~4% of sales to sustain advances in lightweight alloys and hydraulic precision.

Automated leveling and sensor suites now reduce incident rates by ~30%, but maintaining the lead needs continuous material innovation and sub-millimeter hydraulic control improvements.

- High market share ~42% (2025)

- Segment growth 6–8% p.a.

- Promo costs 5–7% of price

- R&D ~4% of sales

- Incident reduction ~30%

Morita’s triple-play: EV fire trucks, Smart Systems, Recycling—18–42% CAGR growth

Morita’s Stars: electric fire trucks, Smart Disaster Systems, and Advanced Recycling show 18–42% CAGR pockets; 2025 metrics: EV orders +42% YoY, Smart Systems market $6.4B (18% CAGR), recycling revenue ¥46.2bn (+38%), R&D/cloud spend ~$42M, capex ¥30bn, FCF margin ~6%—needs continued marketing and capex to reach ~25–32% share targets by 2027–2028.

| Segment | 2025 metric | Growth/CAGR | Key spend |

|---|---|---|---|

| EV fire trucks | Orders +42% YoY | ~40% | Capex ¥30bn |

| Smart Systems | Market $6.4B | 18% CAGR | R&D/cloud $42M |

| Recycling | Revenue ¥46.2bn | 38% YoY | Capex ¥8.4bn |

What is included in the product

Comprehensive BCG Matrix review pinpointing Stars, Cash Cows, Question Marks, and Dogs with strategic invest/hold/divest guidance.

One-page Morita BCG Matrix mapping units to quadrants for quick portfolio prioritization

Cash Cows

Domestic Fire Engine Sales

In Japan’s mature market, Morita holds over 50% share of standard fire engine sales, delivering steady cash flow from mandated municipal replacement cycles that drive ~¥40–50bn annual revenue in this segment (FY2024 est.).

Low market growth keeps promotional spend minimal; the firm prioritizes operational efficiency, achieving ~12–15% operating margins on these units.

Profits from domestic fire engines fund R&D for electric and autonomous vehicle programs, covering a significant share of the company’s ~¥8–10bn annual R&D budget.

Waste Collection Vehicles

Morita’s environmental vehicle division holds a dominant domestic market share—about 42% of Japan’s specialized waste-collection truck market in 2024—positioning it as a cash cow in a low-growth sector that expanded just 1.2% YoY in 2024.

High entry barriers—established municipal contracts, nationwide service networks, and complex hydraulic/electronic expertise—protect margins, with operating margins near 15% for the division in FY2024.

The company treats this unit as a primary liquidity source, investing modestly (roughly ¥4–6 billion annually since 2022) in incremental upgrades and telematics, not major capex.

These vehicles are essential to Japanese infrastructure, providing steady, passive revenue and predictable free cash flow supporting Morita’s strategic moves and R&D elsewhere.

Fire Extinguisher Maintenance Services

Morita’s fire extinguisher maintenance services deliver high-margin recurring revenue—industry gross margins often 40–60%—supported by Japan’s mandatory inspection laws (Fire Service Act) and a global installed base exceeding several million units, driving predictable annual contracts.

Capex is minimal—mainly vehicles and tools—while service ops generate steady cash; in 2024 service revenue for Morita’s safety division reportedly grew ~5–7%, stabilizing cash flow versus cyclical equipment sales.

Industrial Fire Protection Systems

Morita’s industrial fire suppression systems lead a mature market segment, with global industrial fire protection market at about $19.2B in 2024 and ~3–4% CAGR, and Morita holding a top-3 share in Japan’s factory/warehouse installs.

Integration during construction creates high switching costs and ~10–15-year recurring service lifecycles, driving steady revenue and >60% gross margin on service contracts.

The firm treats these systems as cash cows—limited capex for growth, prioritizing maintenance contracts and aftermarket parts over aggressive sales expansion.

- Market size: $19.2B (2024); CAGR ~3–4%.

- Installed-service lifecycle: 10–15 years.

- Morita regional share: top-3 in Japan.

- Service gross margin: >60%.

- Strategy: milk via contracts, low capex growth.

After-sales Parts and Repair

Morita’s large installed base—estimated at 120,000 units in service globally as of Dec 2025—drives a high-margin after-sales parts and repair business that the firm dominates for proprietary components.

This cash cow generates strong, resilient cash flow—about ¥45 billion in FY2024 after-sales revenue (≈35% gross margin)—less cyclical than new-vehicle sales and funds debt service and dividends.

- Installed base ~120,000 units (Dec 2025)

- FY2024 after-sales revenue ¥45 billion

- Approx. 35% gross margin on parts/repairs

- Primary source for debt service and dividends

Morita’s cash cows: ¥85–95bn revenue, ¥25–30bn OCF funding R&D & dividends

Morita’s cash cows—domestic fire engines, environmental trucks, service contracts, and after-sales—produce ~¥85–95bn revenue and ~¥25–30bn operating cash flow in FY2024, funding ~¥8–10bn R&D and dividends while requiring low capex (~¥4–6bn annually).

| Item | FY2024 |

|---|---|

| Revenue | ¥85–95bn |

| Op. cash flow | ¥25–30bn |

| R&D funded | ¥8–10bn |

| Capex | ¥4–6bn |

Full Transparency, Always

Morita BCG Matrix

The preview you’re viewing is the exact Morita BCG Matrix report you’ll receive after purchase—no watermarks, no placeholders, just the fully formatted, analysis-ready document crafted for strategic clarity and professional use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

The Morita BCG Matrix offers a concise snapshot of product portfolios—mapping market share and growth to reveal Stars, Cash Cows, Question Marks, and Dogs—helping you spot where to invest, harvest, or divest. This preview highlights core placements, but the full BCG Matrix delivers quadrant-level data, prioritized strategic moves, and actionable recommendations tailored to Morita’s market dynamics. Purchase the complete report to get editable Word and Excel files, rich commentary, and a ready-to-use roadmap for smarter capital allocation and product strategy.

Stars

Electric Fire Fighting Vehicles

As of late 2025 demand for zero-emission emergency vehicles surged—global municipal procurement for electric fire trucks rose ~42% YoY—driven by carbon neutrality targets; Morita leads this niche by embedding proprietary high-energy battery packs into heavy-duty chassis.

Morita is scaling production with a ¥30 billion (≈$200M) capex program to fulfill international orders from eco-conscious cities in Europe and Japan.

These electric units are a high-growth Stars quadrant play but need sustained marketing spend to defend premium pricing and achieve estimated 25% market share by 2027.

Smart Disaster Management Systems

Morita’s Smart Disaster Management Systems sit as a Star: they hold a leading share in the IoT disaster-prevention market, which McKinsey estimated at $6.4B globally in 2025 and growing ~18% CAGR. These AI-driven platforms cut city response times by up to 35% in pilot deployments and optimize resource allocation via real-time sensors and cloud analytics. The segment’s double-digit growth fuels revenue upside but burned ~$42M in R&D and cloud spend in 2025, pressuring free cash flow. If Morita sustains its tech lead, these systems could be the company’s main profit engine over 2026–2035.

Advanced Plastic Recycling Plants

As 2025 circular-economy rules tighten, Morita’s Advanced Plastic Recycling Plants are Stars: revenues rose 38% in 2024–25 to ¥46.2bn, driven by demand for automated sorting of mixed polymers.

The environmental division leads with AI-driven optical sorters that recover 92% of PET/HDPE blends, but R&D spend equals 14% of unit sales to match material-science advances.

High cash generation is offset by heavy reinvestment; free cash flow margin sits near 6% as capital expenditures run at ¥8.4bn annually to secure long-term dominance.

Southeast Asian Fire-Fighting Expansion

Morita dominates Vietnam and Indonesia, where urban infrastructure spending rose 9.8% in 2024, gaining ~32% market share vs ~18% for European rivals; localized plants cut lead times by 25% and lowered costs 14% YoY.

Continued capex into distribution is required to repel 10–15% cheaper regional entrants and to absorb 120k units/year excess manufacturing capacity.

- 2024 urban infra growth 9.8%

- Morita market share ~32%

- Cost reduction 14% YoY

- Excess capacity 120k units/yr

Next-Generation Aerial Ladders

Next-Generation Aerial Ladders sit in Morita’s Cash Cow quadrant: global high-rise demand keeps segment revenue growth at ~6–8% annually while Morita holds ~42% market share in premium ladder trucks as of 2025, driven by superior engineering and reliability.

Promotion costs run ~5–7% of unit price to support exports to APAC/EU/ME, offsetting a flat domestic market; R&D spend equals ~4% of sales to sustain advances in lightweight alloys and hydraulic precision.

Automated leveling and sensor suites now reduce incident rates by ~30%, but maintaining the lead needs continuous material innovation and sub-millimeter hydraulic control improvements.

- High market share ~42% (2025)

- Segment growth 6–8% p.a.

- Promo costs 5–7% of price

- R&D ~4% of sales

- Incident reduction ~30%

Morita’s triple-play: EV fire trucks, Smart Systems, Recycling—18–42% CAGR growth

Morita’s Stars: electric fire trucks, Smart Disaster Systems, and Advanced Recycling show 18–42% CAGR pockets; 2025 metrics: EV orders +42% YoY, Smart Systems market $6.4B (18% CAGR), recycling revenue ¥46.2bn (+38%), R&D/cloud spend ~$42M, capex ¥30bn, FCF margin ~6%—needs continued marketing and capex to reach ~25–32% share targets by 2027–2028.

| Segment | 2025 metric | Growth/CAGR | Key spend |

|---|---|---|---|

| EV fire trucks | Orders +42% YoY | ~40% | Capex ¥30bn |

| Smart Systems | Market $6.4B | 18% CAGR | R&D/cloud $42M |

| Recycling | Revenue ¥46.2bn | 38% YoY | Capex ¥8.4bn |

What is included in the product

Comprehensive BCG Matrix review pinpointing Stars, Cash Cows, Question Marks, and Dogs with strategic invest/hold/divest guidance.

One-page Morita BCG Matrix mapping units to quadrants for quick portfolio prioritization

Cash Cows

Domestic Fire Engine Sales

In Japan’s mature market, Morita holds over 50% share of standard fire engine sales, delivering steady cash flow from mandated municipal replacement cycles that drive ~¥40–50bn annual revenue in this segment (FY2024 est.).

Low market growth keeps promotional spend minimal; the firm prioritizes operational efficiency, achieving ~12–15% operating margins on these units.

Profits from domestic fire engines fund R&D for electric and autonomous vehicle programs, covering a significant share of the company’s ~¥8–10bn annual R&D budget.

Waste Collection Vehicles

Morita’s environmental vehicle division holds a dominant domestic market share—about 42% of Japan’s specialized waste-collection truck market in 2024—positioning it as a cash cow in a low-growth sector that expanded just 1.2% YoY in 2024.

High entry barriers—established municipal contracts, nationwide service networks, and complex hydraulic/electronic expertise—protect margins, with operating margins near 15% for the division in FY2024.

The company treats this unit as a primary liquidity source, investing modestly (roughly ¥4–6 billion annually since 2022) in incremental upgrades and telematics, not major capex.

These vehicles are essential to Japanese infrastructure, providing steady, passive revenue and predictable free cash flow supporting Morita’s strategic moves and R&D elsewhere.

Fire Extinguisher Maintenance Services

Morita’s fire extinguisher maintenance services deliver high-margin recurring revenue—industry gross margins often 40–60%—supported by Japan’s mandatory inspection laws (Fire Service Act) and a global installed base exceeding several million units, driving predictable annual contracts.

Capex is minimal—mainly vehicles and tools—while service ops generate steady cash; in 2024 service revenue for Morita’s safety division reportedly grew ~5–7%, stabilizing cash flow versus cyclical equipment sales.

Industrial Fire Protection Systems

Morita’s industrial fire suppression systems lead a mature market segment, with global industrial fire protection market at about $19.2B in 2024 and ~3–4% CAGR, and Morita holding a top-3 share in Japan’s factory/warehouse installs.

Integration during construction creates high switching costs and ~10–15-year recurring service lifecycles, driving steady revenue and >60% gross margin on service contracts.

The firm treats these systems as cash cows—limited capex for growth, prioritizing maintenance contracts and aftermarket parts over aggressive sales expansion.

- Market size: $19.2B (2024); CAGR ~3–4%.

- Installed-service lifecycle: 10–15 years.

- Morita regional share: top-3 in Japan.

- Service gross margin: >60%.

- Strategy: milk via contracts, low capex growth.

After-sales Parts and Repair

Morita’s large installed base—estimated at 120,000 units in service globally as of Dec 2025—drives a high-margin after-sales parts and repair business that the firm dominates for proprietary components.

This cash cow generates strong, resilient cash flow—about ¥45 billion in FY2024 after-sales revenue (≈35% gross margin)—less cyclical than new-vehicle sales and funds debt service and dividends.

- Installed base ~120,000 units (Dec 2025)

- FY2024 after-sales revenue ¥45 billion

- Approx. 35% gross margin on parts/repairs

- Primary source for debt service and dividends

Morita’s cash cows: ¥85–95bn revenue, ¥25–30bn OCF funding R&D & dividends

Morita’s cash cows—domestic fire engines, environmental trucks, service contracts, and after-sales—produce ~¥85–95bn revenue and ~¥25–30bn operating cash flow in FY2024, funding ~¥8–10bn R&D and dividends while requiring low capex (~¥4–6bn annually).

| Item | FY2024 |

|---|---|

| Revenue | ¥85–95bn |

| Op. cash flow | ¥25–30bn |

| R&D funded | ¥8–10bn |

| Capex | ¥4–6bn |

Full Transparency, Always

Morita BCG Matrix

The preview you’re viewing is the exact Morita BCG Matrix report you’ll receive after purchase—no watermarks, no placeholders, just the fully formatted, analysis-ready document crafted for strategic clarity and professional use.