Morito Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

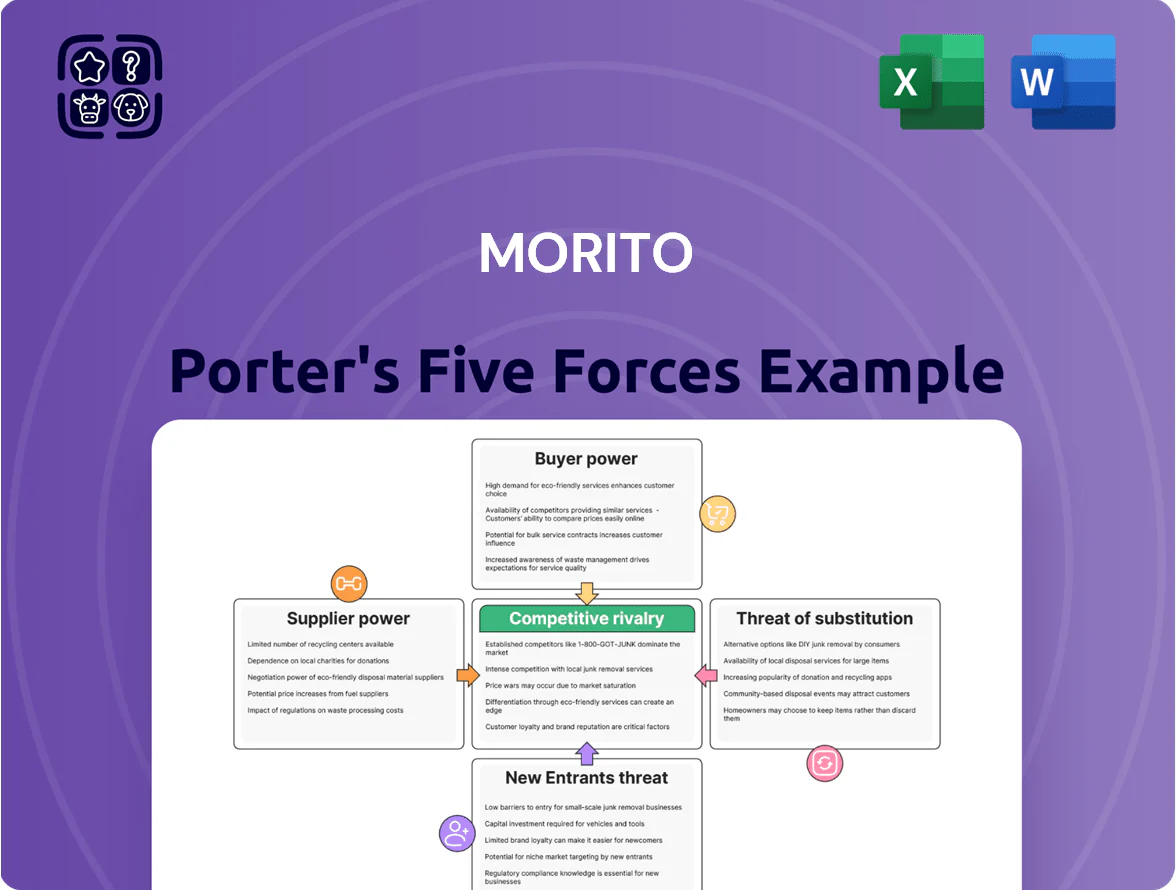

Morito’s Five Forces snapshot highlights key dynamics—supplier leverage in specialized components, moderate buyer power, niche rivalry, limited substitutes, and entry barriers tied to technical know-how.

This brief overview only scratches the surface; unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, data-driven visuals, and strategic implications for Morito.

Ready to act? Purchase the complete report for a consultant-grade, presentation-ready breakdown tailored to investors and strategists.

Suppliers Bargaining Power

Raw material price volatility

Specialized material requirements

Certain high-performance plastics and medical-grade materials come from a handful of certified global vendors, giving suppliers price and delivery leverage—industry data shows single-source supply can raise input price volatility by 12–18% and lead times by 30% vs diversified sourcing (2024). For Morito, this is acute in medical devices; maintaining strategic partnerships and committing to high-volume orders (examples: 3–5 year offtake contracts, 20–40% volume rebates) secures prioritized supply and mitigates a 5–10% revenue-at-risk from delays.

Global logistics and energy costs

Suppliers of energy and international shipping account for roughly 18–25% of Morito’s COGS; Japan’s average industrial electricity price rose to ¥30.5/kWh in 2024, up 6% year-over-year, and global container rates spiked 34% in late 2023 during bottlenecks, pressuring margins.

If Morito can’t pass costs to customers, EBITDA could fall 2–4 percentage points; to defend margins it sources across Southeast Asia and Vietnam (now ~28% of buys) and cut factory yield loss by 12% in 2024 through lean line upgrades.

Supplier fragmentation in basic components

Supplier fragmentation for standard metal fasteners and basic plastic parts remains high; global market share for top 10 suppliers in fasteners is under 25% as of 2025, so Morito can source from many small vendors.

This low concentration lets Morito switch suppliers to chase ~5–10% price differences and maintain quality, keeping supplier bargaining power low for these items.

- Top-10 fastener share <25% (2025)

- Typical price swing used: 5–10%

- Multiple vetted vendors per region: 8–15

Technological integration with partners

Morito partners with suppliers on R&D for sustainable and recycled materials, creating mutual dependence that shifts supplier power toward collaboration; 2024 joint projects accounted for ~22% of Morito’s materials capex and reduced material costs by 6% year-over-year.

This deep tech integration raises switching costs—losing access to proprietary eco-materials and co-developed processes could cut product margin by ~150–250 basis points in the first year.

- Joint R&D tie-up: 22% of materials capex (2024)

- Y/Y material cost reduction: 6% (2024)

- Switching-cost margin hit: 150–250 bps

Supplier leverage splits: commodities spike, fasteners offer savings; R&D locks margins

| Metric | Value |

|---|---|

| Steel/polyolefin price change (2024) | +18% / +22% |

| Long-term contract coverage | ~40% |

| Top-10 fastener share (2025) | <25% |

| Joint R&D share of materials capex (2024) | 22% |

| Switching-cost margin hit | 150–250 bps |

What is included in the product

Tailored Porter's Five Forces analysis for Morito that uncovers competitive drivers, supplier and buyer power, entry threats, substitutes, and emerging disruptors—supported by industry data and strategic commentary for use in investor materials or internal strategy decks.

Compact Morito Porter's Five Forces snapshot that quantifies competitive pressures, letting you pinpoint strategic threats and relief actions in seconds for faster, clearer decision-making.

Customers Bargaining Power

Concentration of major apparel brands

Major global fashion and athletic brands place orders that can represent 20–35% of a contract supplier’s annual volume; for Morito losing one such client could cut revenue by an estimated 10–18% based on 2024 sales mix. These buyers push for lower unit prices and tightened ESG (environment, social, governance) specs—forcing Morito to invest in cleaner dyeing tech and audit costs that can raise per-unit production expense by 3–6%.

Low switching costs for standard fasteners

Low switching costs for standard fasteners mean buyers can pivot to Southeast Asian suppliers offering up to 30–50% lower unit prices for generic buttons, eyelets, and basic industrial fasteners, pressuring Morito to stand out on quality, on-time delivery, and after-sales support.

Morito counters by deepening technical integration with clients’ design and engineering teams, converting commodity purchases into system-level partnerships that historically raise client retention by ~15–25% and margin per account by ~200–400 basis points.

Demand for sustainable and ethical sourcing

By end-2025, 68% of industrial buyers rank eco-friendly components and transparent supply chains as decisive purchase criteria, giving customers real power to reject vendors lacking strict ESG standards.

This buyer leverage makes sustainability a market-access gate: procurement teams at 40% of top global brands now require third-party ESG audits and 2030 decarbonization plans for suppliers.

Morito responded with a $42 million green capex program (2023–25) for low-carbon materials and traceability tech, preserving contracts with high-value conscious brands and reducing carbon intensity by 18%.

Customization and technical specifications

In automotive and medical markets, buyers demand highly specific, certified components meeting ISO 26262 (auto) and ISO 13485 (medical) standards, which makes supplier switches slow and costly—supplier qualification can take 6–18 months and cost >$200k per line change.

Morito’s niche engineering know-how and 12% R&D-to-sales ratio (2024) narrows customers’ leverage by reducing requalification needs and offering tailored designs that competitors struggle to match.

- Qualification time: 6–18 months

- Qualification cost: >$200k per line

- Morito R&D/sales: 12% (2024)

- Standards: ISO 26262, ISO 13485

Price sensitivity in mass markets

In Morito's budget apparel and consumer goods segments, price drives over 70% of purchase decisions, pushing buyers to use domestic and international quotes to shave margins by 3–7 percentage points.

Morito counters with a global production footprint—factories in Vietnam, Bangladesh, and Mexico—cutting logistics and labor costs so gross margins stay near 18–22% despite pressure.

High buyer leverage pressures margins; ESG & capex provide partial protection

Buyers hold high leverage: top-brand orders equal 20–35% of suppliers’ volume; losing one client may cut Morito revenue 10–18% (2024 mix). Price drives >70% of budget-segment purchases, trimming margins 3–7ppt, while 68% of buyers prioritize ESG and 40% require third-party audits. Qualification takes 6–18 months and >$200k per line, helping Morito’s 12% R&D/sales and $42M green capex shield margins (18–22%).

Preview Before You Purchase

Morito Porter's Five Forces Analysis

This preview shows the exact Morito Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document covers competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights and data-driven observations. It's fully formatted and ready for download the moment you buy. Use it as-is for decision-making, presentations, or strategy work.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Morito’s Five Forces snapshot highlights key dynamics—supplier leverage in specialized components, moderate buyer power, niche rivalry, limited substitutes, and entry barriers tied to technical know-how.

This brief overview only scratches the surface; unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, data-driven visuals, and strategic implications for Morito.

Ready to act? Purchase the complete report for a consultant-grade, presentation-ready breakdown tailored to investors and strategists.

Suppliers Bargaining Power

Raw material price volatility

Specialized material requirements

Certain high-performance plastics and medical-grade materials come from a handful of certified global vendors, giving suppliers price and delivery leverage—industry data shows single-source supply can raise input price volatility by 12–18% and lead times by 30% vs diversified sourcing (2024). For Morito, this is acute in medical devices; maintaining strategic partnerships and committing to high-volume orders (examples: 3–5 year offtake contracts, 20–40% volume rebates) secures prioritized supply and mitigates a 5–10% revenue-at-risk from delays.

Global logistics and energy costs

Suppliers of energy and international shipping account for roughly 18–25% of Morito’s COGS; Japan’s average industrial electricity price rose to ¥30.5/kWh in 2024, up 6% year-over-year, and global container rates spiked 34% in late 2023 during bottlenecks, pressuring margins.

If Morito can’t pass costs to customers, EBITDA could fall 2–4 percentage points; to defend margins it sources across Southeast Asia and Vietnam (now ~28% of buys) and cut factory yield loss by 12% in 2024 through lean line upgrades.

Supplier fragmentation in basic components

Supplier fragmentation for standard metal fasteners and basic plastic parts remains high; global market share for top 10 suppliers in fasteners is under 25% as of 2025, so Morito can source from many small vendors.

This low concentration lets Morito switch suppliers to chase ~5–10% price differences and maintain quality, keeping supplier bargaining power low for these items.

- Top-10 fastener share <25% (2025)

- Typical price swing used: 5–10%

- Multiple vetted vendors per region: 8–15

Technological integration with partners

Morito partners with suppliers on R&D for sustainable and recycled materials, creating mutual dependence that shifts supplier power toward collaboration; 2024 joint projects accounted for ~22% of Morito’s materials capex and reduced material costs by 6% year-over-year.

This deep tech integration raises switching costs—losing access to proprietary eco-materials and co-developed processes could cut product margin by ~150–250 basis points in the first year.

- Joint R&D tie-up: 22% of materials capex (2024)

- Y/Y material cost reduction: 6% (2024)

- Switching-cost margin hit: 150–250 bps

Supplier leverage splits: commodities spike, fasteners offer savings; R&D locks margins

| Metric | Value |

|---|---|

| Steel/polyolefin price change (2024) | +18% / +22% |

| Long-term contract coverage | ~40% |

| Top-10 fastener share (2025) | <25% |

| Joint R&D share of materials capex (2024) | 22% |

| Switching-cost margin hit | 150–250 bps |

What is included in the product

Tailored Porter's Five Forces analysis for Morito that uncovers competitive drivers, supplier and buyer power, entry threats, substitutes, and emerging disruptors—supported by industry data and strategic commentary for use in investor materials or internal strategy decks.

Compact Morito Porter's Five Forces snapshot that quantifies competitive pressures, letting you pinpoint strategic threats and relief actions in seconds for faster, clearer decision-making.

Customers Bargaining Power

Concentration of major apparel brands

Major global fashion and athletic brands place orders that can represent 20–35% of a contract supplier’s annual volume; for Morito losing one such client could cut revenue by an estimated 10–18% based on 2024 sales mix. These buyers push for lower unit prices and tightened ESG (environment, social, governance) specs—forcing Morito to invest in cleaner dyeing tech and audit costs that can raise per-unit production expense by 3–6%.

Low switching costs for standard fasteners

Low switching costs for standard fasteners mean buyers can pivot to Southeast Asian suppliers offering up to 30–50% lower unit prices for generic buttons, eyelets, and basic industrial fasteners, pressuring Morito to stand out on quality, on-time delivery, and after-sales support.

Morito counters by deepening technical integration with clients’ design and engineering teams, converting commodity purchases into system-level partnerships that historically raise client retention by ~15–25% and margin per account by ~200–400 basis points.

Demand for sustainable and ethical sourcing

By end-2025, 68% of industrial buyers rank eco-friendly components and transparent supply chains as decisive purchase criteria, giving customers real power to reject vendors lacking strict ESG standards.

This buyer leverage makes sustainability a market-access gate: procurement teams at 40% of top global brands now require third-party ESG audits and 2030 decarbonization plans for suppliers.

Morito responded with a $42 million green capex program (2023–25) for low-carbon materials and traceability tech, preserving contracts with high-value conscious brands and reducing carbon intensity by 18%.

Customization and technical specifications

In automotive and medical markets, buyers demand highly specific, certified components meeting ISO 26262 (auto) and ISO 13485 (medical) standards, which makes supplier switches slow and costly—supplier qualification can take 6–18 months and cost >$200k per line change.

Morito’s niche engineering know-how and 12% R&D-to-sales ratio (2024) narrows customers’ leverage by reducing requalification needs and offering tailored designs that competitors struggle to match.

- Qualification time: 6–18 months

- Qualification cost: >$200k per line

- Morito R&D/sales: 12% (2024)

- Standards: ISO 26262, ISO 13485

Price sensitivity in mass markets

In Morito's budget apparel and consumer goods segments, price drives over 70% of purchase decisions, pushing buyers to use domestic and international quotes to shave margins by 3–7 percentage points.

Morito counters with a global production footprint—factories in Vietnam, Bangladesh, and Mexico—cutting logistics and labor costs so gross margins stay near 18–22% despite pressure.

High buyer leverage pressures margins; ESG & capex provide partial protection

Buyers hold high leverage: top-brand orders equal 20–35% of suppliers’ volume; losing one client may cut Morito revenue 10–18% (2024 mix). Price drives >70% of budget-segment purchases, trimming margins 3–7ppt, while 68% of buyers prioritize ESG and 40% require third-party audits. Qualification takes 6–18 months and >$200k per line, helping Morito’s 12% R&D/sales and $42M green capex shield margins (18–22%).

Preview Before You Purchase

Morito Porter's Five Forces Analysis

This preview shows the exact Morito Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document covers competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights and data-driven observations. It's fully formatted and ready for download the moment you buy. Use it as-is for decision-making, presentations, or strategy work.