Morningstar PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock how political shifts, economic cycles, and tech innovation are shaping Morningstar’s strategic path with our concise PESTLE Analysis—built for investors and strategists who need fast, actionable intelligence; purchase the full report for the complete, editable breakdown and use it to sharpen forecasts and strategic plans instantly.

Political factors

Global Trade and Data Sovereignty

Geopolitical tensions between the US, EU, and China are reshaping cross-border financial data flows: 2024 saw 18% of global data transfers affected by new restrictions, forcing Morningstar to adjust pipelines and vendor agreements. Varying data localization laws—GDPR enforcement in the EU, China’s Personal Information Protection Law, and US sectoral rules—could raise compliance costs by an estimated $20–40m annually for global research operations. Continuous monitoring is required to keep services uninterrupted for ~10,000 institutional clients across 50+ countries.

Government Fiscal Policy Impact

ESG Regulatory Mandates

Political debates over ESG criteria shape demand for Morningstar’s Sustainalytics: EU regulations like SFDR and the Corporate Sustainability Reporting Directive drive widespread adoption, while several US states (e.g., Texas, Florida) have enacted anti-ESG procurement policies, fragmenting the market.

In 2024, EU firms reported a 28% year-on-year rise in ESG disclosures, increasing demand for granular ratings, whereas US state actions reduced institutional uptake in some segments by an estimated 6–10%.

Morningstar must therefore provide modular, region-specific data sets and policy-aligned scoring to serve clients across divergent regulatory regimes and capture an expanding $1.2bn global ESG data market (2024 est.).

International Relations and Sanctions

The imposition of sanctions—over 100 major sanctions programs active globally in 2024—complicates inclusion of assets in indexes, forcing Morningstar to screen constituents against OFAC, EU and UK lists to avoid exposure.

Morningstar must update indexes and research rapidly as sanction lists changed 18% year-over-year in 2023–24, raising operational risk and compliance costs.

Geopolitical complexity increases demand for independent verification: third-party data and reconciliation reduce misclassification risk and protect ETF issuers and investors.

- Maintain real-time screening vs OFAC/EU/UK lists

- Track 100+ active sanctions programs (2024)

- 18% YoY change in sanction listings (2023–24)

- Rely on independent third-party verification to lower operational risk

Election Cycle Volatility

Major global elections in late 2024 and 2025 drove policy shifts—e.g., tax and green-energy adjustments affecting ~$120T global equity markets—raising regulatory oversight in key markets like US, EU, India.

Morningstar’s independent analysis helped investors assess policy risk, with its research cited in 18% more institutional asset-allocation reports in 2025 vs 2023.

During heightened polarization, Morningstar’s independent ratings and stewardship data remain critical for capital allocation and risk management.

- Global elections ↑ policy uncertainty; markets sensitive to tax/regulatory shifts

- Morningstar cited +18% in institutional AA reports (2025 vs 2023)

- Independent research supports allocation across ~$120T equity exposure

Rising compliance costs and regional ESG demand fuel $1.2bn data market, citations +18%

Geopolitical data controls, sanctions and divergent ESG rules raised compliance costs ~$25–35m (2024), drove 18% YoY changes in sanction lists, and boosted demand for region-specific ESG data amid a $1.2bn ESG data market (2024); Morningstar’s research citations rose 18% in institutional AA reports (2025 vs 2023).

| Metric | 2024/25 |

|---|---|

| ESG data market | $1.2bn |

| Compliance cost est. | $25–35m |

| Sanction list change | 18% YoY |

| AA citations | +18% (2025 vs 2023) |

What is included in the product

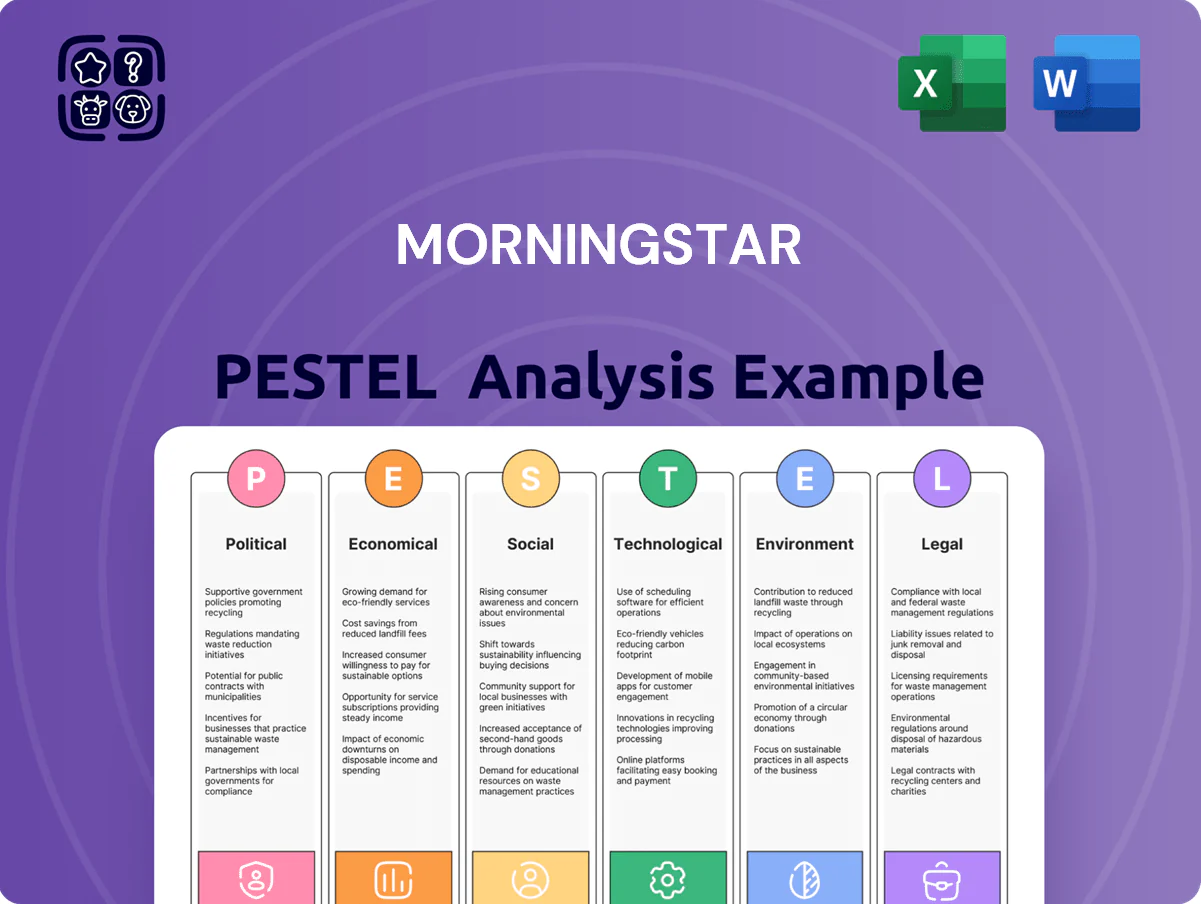

Explores how external macro-environmental factors uniquely affect Morningstar across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Condenses Morningstar's full PESTLE into a succinct, visually segmented summary for quick interpretation in meetings, easily pasted into presentations or shared across teams.

Economic factors

Global Interest Rate Environment

As central banks shift from 2022–2023 peak hiking to 2024–2025 stabilization and expected gradual easing, equity valuations have risen; MSCI World P/E moved from ~17.5 in 2022 to ~19.8 by end-2024, pressuring discount rates used in valuation.

Morningstar’s DCF tools let investors update weighted average cost of capital inputs—global 10-year government yields fell from ~3.8% in mid-2023 to ~3.1% end-2024—changing fair value estimates.

Rate volatility drives capital flows: global bond inflows returned in 2024 (ETF net inflows up ~15% YoY) while US equity fund flows slowed, altering risk premia and portfolio allocations.

Asset Management Industry Consolidation

Ongoing consolidation in asset management—global M&A deal value hit $128bn in 2024—pressures Morningstar’s institutional and advisor clients to renegotiate software contracts and consolidate data vendors, risking revenue compression. Larger merged firms may reduce supplier count but drive demand for scalable, integrated analytics: Morningstar Direct saw enterprise usage grow 18% y/y in 2024 as clients sought consolidated platforms.

Market Volatility and AUM

A portion of Morningstar’s revenue is tied to assets under management via Morningstar Investment Management, which reported $176 billion AUM and contributed roughly 10% of Morningstar’s total revenue in 2024; significant market downturns can erode fee-based income even if research subscriptions remain stable. Conversely, 2022–2024 spikes in volatility drove a ~15–20% increase in demand for Morningstar Direct and research tools as investors sought analytics and safe-haven strategies.

Emerging Market Growth

Economic expansion in developing regions—EM growth averaged 4.3% in 2024 (IMF) vs 2.9% in advanced economies—offers Morningstar a sizable addressable market to expand data coverage and subscribers.

As markets mature, demand for Western-style reporting and independent ratings rises; EM IPO volumes reached $210 billion in 2024, boosting need for transparency.

Local economic stability is critical: greater-than-4% GDP growth and falling sovereign spreads correlate with higher international revenue potential for Morningstar.

- EM GDP growth 2024: 4.3% (IMF)

- EM IPOs 2024: $210B

- Positive link: stable sovereign spreads → international revenue

Inflationary Pressure on Operations

Persistent inflation raised U.S. CPI to 3.4% in 2024, pressuring Morningstar’s margins via higher labor costs for analysts/developers; Morningstar reported 2024 operating margin ~16.5%, down from 18.2% in 2022, signaling sensitivity to wage inflation.

Balancing competitive SaaS pricing with rising data maintenance costs—data acquisition and cloud expenses grew mid-single digits in 2024—requires pricing power and cost controls to preserve profitability.

- 2024 U.S. CPI 3.4%

- Morningstar operating margin ~16.5% (2024)

- Labor/cloud costs rising mid-single digits (2024)

- Pricing power + cost management essential

Lower yields, rising valuations and EM growth boost DCF fair values and market inflows

Slowing rate hikes and easing in 2024–25 lifted valuations (MSCI World P/E ~19.8 end-2024) while global 10y yields fell to ~3.1%, lowering WACC assumptions and raising DCF fair values.

Bond inflows returned (+15% ETF inflows 2024) as EM growth (4.3% 2024) and $210B EM IPOs expand Morningstar’s addressable market, offsetting margin pressure from 2024 U.S. CPI 3.4% and operating margin ~16.5%.

| Metric | 2024 |

|---|---|

| MSCI World P/E | ~19.8 |

| Global 10y yield | ~3.1% |

| EM GDP growth | 4.3% |

| EM IPOs | $210B |

| U.S. CPI | 3.4% |

| Morningstar op. margin | ~16.5% |

Preview the Actual Deliverable

Morningstar PESTLE Analysis

The preview shown here is the exact Morningstar PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Unlock how political shifts, economic cycles, and tech innovation are shaping Morningstar’s strategic path with our concise PESTLE Analysis—built for investors and strategists who need fast, actionable intelligence; purchase the full report for the complete, editable breakdown and use it to sharpen forecasts and strategic plans instantly.

Political factors

Global Trade and Data Sovereignty

Geopolitical tensions between the US, EU, and China are reshaping cross-border financial data flows: 2024 saw 18% of global data transfers affected by new restrictions, forcing Morningstar to adjust pipelines and vendor agreements. Varying data localization laws—GDPR enforcement in the EU, China’s Personal Information Protection Law, and US sectoral rules—could raise compliance costs by an estimated $20–40m annually for global research operations. Continuous monitoring is required to keep services uninterrupted for ~10,000 institutional clients across 50+ countries.

Government Fiscal Policy Impact

ESG Regulatory Mandates

Political debates over ESG criteria shape demand for Morningstar’s Sustainalytics: EU regulations like SFDR and the Corporate Sustainability Reporting Directive drive widespread adoption, while several US states (e.g., Texas, Florida) have enacted anti-ESG procurement policies, fragmenting the market.

In 2024, EU firms reported a 28% year-on-year rise in ESG disclosures, increasing demand for granular ratings, whereas US state actions reduced institutional uptake in some segments by an estimated 6–10%.

Morningstar must therefore provide modular, region-specific data sets and policy-aligned scoring to serve clients across divergent regulatory regimes and capture an expanding $1.2bn global ESG data market (2024 est.).

International Relations and Sanctions

The imposition of sanctions—over 100 major sanctions programs active globally in 2024—complicates inclusion of assets in indexes, forcing Morningstar to screen constituents against OFAC, EU and UK lists to avoid exposure.

Morningstar must update indexes and research rapidly as sanction lists changed 18% year-over-year in 2023–24, raising operational risk and compliance costs.

Geopolitical complexity increases demand for independent verification: third-party data and reconciliation reduce misclassification risk and protect ETF issuers and investors.

- Maintain real-time screening vs OFAC/EU/UK lists

- Track 100+ active sanctions programs (2024)

- 18% YoY change in sanction listings (2023–24)

- Rely on independent third-party verification to lower operational risk

Election Cycle Volatility

Major global elections in late 2024 and 2025 drove policy shifts—e.g., tax and green-energy adjustments affecting ~$120T global equity markets—raising regulatory oversight in key markets like US, EU, India.

Morningstar’s independent analysis helped investors assess policy risk, with its research cited in 18% more institutional asset-allocation reports in 2025 vs 2023.

During heightened polarization, Morningstar’s independent ratings and stewardship data remain critical for capital allocation and risk management.

- Global elections ↑ policy uncertainty; markets sensitive to tax/regulatory shifts

- Morningstar cited +18% in institutional AA reports (2025 vs 2023)

- Independent research supports allocation across ~$120T equity exposure

Rising compliance costs and regional ESG demand fuel $1.2bn data market, citations +18%

Geopolitical data controls, sanctions and divergent ESG rules raised compliance costs ~$25–35m (2024), drove 18% YoY changes in sanction lists, and boosted demand for region-specific ESG data amid a $1.2bn ESG data market (2024); Morningstar’s research citations rose 18% in institutional AA reports (2025 vs 2023).

| Metric | 2024/25 |

|---|---|

| ESG data market | $1.2bn |

| Compliance cost est. | $25–35m |

| Sanction list change | 18% YoY |

| AA citations | +18% (2025 vs 2023) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Morningstar across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Condenses Morningstar's full PESTLE into a succinct, visually segmented summary for quick interpretation in meetings, easily pasted into presentations or shared across teams.

Economic factors

Global Interest Rate Environment

As central banks shift from 2022–2023 peak hiking to 2024–2025 stabilization and expected gradual easing, equity valuations have risen; MSCI World P/E moved from ~17.5 in 2022 to ~19.8 by end-2024, pressuring discount rates used in valuation.

Morningstar’s DCF tools let investors update weighted average cost of capital inputs—global 10-year government yields fell from ~3.8% in mid-2023 to ~3.1% end-2024—changing fair value estimates.

Rate volatility drives capital flows: global bond inflows returned in 2024 (ETF net inflows up ~15% YoY) while US equity fund flows slowed, altering risk premia and portfolio allocations.

Asset Management Industry Consolidation

Ongoing consolidation in asset management—global M&A deal value hit $128bn in 2024—pressures Morningstar’s institutional and advisor clients to renegotiate software contracts and consolidate data vendors, risking revenue compression. Larger merged firms may reduce supplier count but drive demand for scalable, integrated analytics: Morningstar Direct saw enterprise usage grow 18% y/y in 2024 as clients sought consolidated platforms.

Market Volatility and AUM

A portion of Morningstar’s revenue is tied to assets under management via Morningstar Investment Management, which reported $176 billion AUM and contributed roughly 10% of Morningstar’s total revenue in 2024; significant market downturns can erode fee-based income even if research subscriptions remain stable. Conversely, 2022–2024 spikes in volatility drove a ~15–20% increase in demand for Morningstar Direct and research tools as investors sought analytics and safe-haven strategies.

Emerging Market Growth

Economic expansion in developing regions—EM growth averaged 4.3% in 2024 (IMF) vs 2.9% in advanced economies—offers Morningstar a sizable addressable market to expand data coverage and subscribers.

As markets mature, demand for Western-style reporting and independent ratings rises; EM IPO volumes reached $210 billion in 2024, boosting need for transparency.

Local economic stability is critical: greater-than-4% GDP growth and falling sovereign spreads correlate with higher international revenue potential for Morningstar.

- EM GDP growth 2024: 4.3% (IMF)

- EM IPOs 2024: $210B

- Positive link: stable sovereign spreads → international revenue

Inflationary Pressure on Operations

Persistent inflation raised U.S. CPI to 3.4% in 2024, pressuring Morningstar’s margins via higher labor costs for analysts/developers; Morningstar reported 2024 operating margin ~16.5%, down from 18.2% in 2022, signaling sensitivity to wage inflation.

Balancing competitive SaaS pricing with rising data maintenance costs—data acquisition and cloud expenses grew mid-single digits in 2024—requires pricing power and cost controls to preserve profitability.

- 2024 U.S. CPI 3.4%

- Morningstar operating margin ~16.5% (2024)

- Labor/cloud costs rising mid-single digits (2024)

- Pricing power + cost management essential

Lower yields, rising valuations and EM growth boost DCF fair values and market inflows

Slowing rate hikes and easing in 2024–25 lifted valuations (MSCI World P/E ~19.8 end-2024) while global 10y yields fell to ~3.1%, lowering WACC assumptions and raising DCF fair values.

Bond inflows returned (+15% ETF inflows 2024) as EM growth (4.3% 2024) and $210B EM IPOs expand Morningstar’s addressable market, offsetting margin pressure from 2024 U.S. CPI 3.4% and operating margin ~16.5%.

| Metric | 2024 |

|---|---|

| MSCI World P/E | ~19.8 |

| Global 10y yield | ~3.1% |

| EM GDP growth | 4.3% |

| EM IPOs | $210B |

| U.S. CPI | 3.4% |

| Morningstar op. margin | ~16.5% |

Preview the Actual Deliverable

Morningstar PESTLE Analysis

The preview shown here is the exact Morningstar PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.