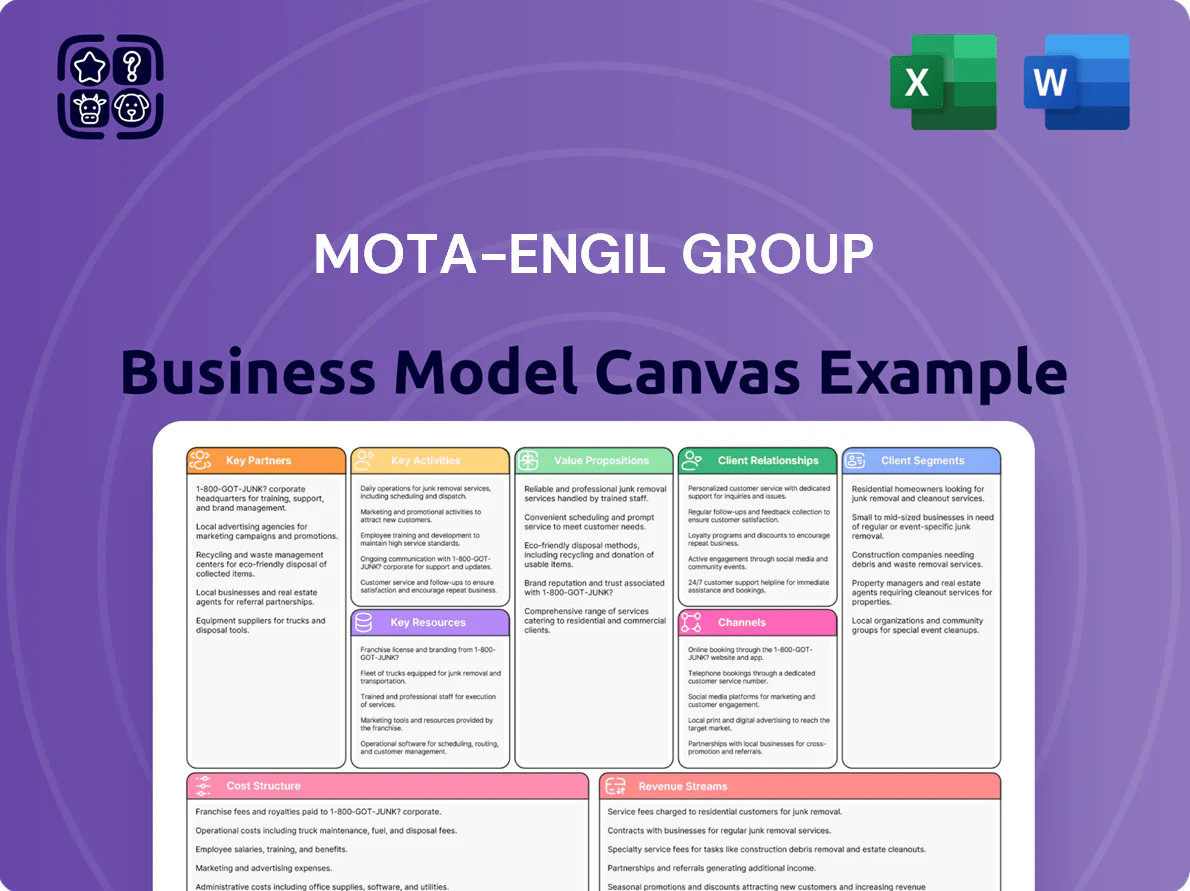

Mota-Engil Group Business Model Canvas

Mota-Engil Business Model Canvas: Compact Strategic Blueprint for Investors & Advisors

Unlock the full strategic blueprint behind Mota-Engil Group with our Business Model Canvas—condensed insights on value propositions, key partners, revenue streams and cost drivers that explain how the group wins projects and scales globally; perfect for investors, consultants, and entrepreneurs seeking a ready-to-use, editable framework to benchmark strategy and drive decisions.

Partnerships

Strategic Alliance with China Communications Construction Company

The 2017 equity stake by China Communications Construction Company (CCCC) gives Mota-Engil stronger balance-sheet support and global procurement access, helping secure >€4.2bn in new international contracts from 2021–2025. By end-2025 the alliance enabled joint bids on mega-tenders, raising Mota-Engil’s large-project win rate in Africa, Latin America and Europe to ~28% of group backlog.

Financial Institutions and Export Credit Agencies

Mota-Engil relies on international banks and export credit agencies (ECAs) to secure project financing and performance bonds, with syndicated loans and ECA-backed facilities covering ~40% of its €1.2bn 2024 capex program. These partners mitigate long-term infrastructure risk in emerging markets and help structure complex project-finance deals that maintain liquidity across the project lifecycle, often providing tenors up to 15 years.

Local Joint Venture Partners

In Africa and Latin America Mota-Engil forms local joint ventures to meet local-content rules and speed permits, pairing Mota-Engil’s engineering and EPC (engineering, procurement, construction) capacity with partners’ market access and logistics; by 2024 these JVs accounted for ~38% of the Group’s regional backlog and reduced project delays by ~20%, lowering political/operational risk and improving community acceptance.

Specialized Technology and Equipment Suppliers

The group holds multi-year contracts with global OEMs like Caterpillar and Herrenknecht, securing heavy machinery for tunneling, bridge and mining projects; these agreements cut CAPEX volatility and saved an estimated €45m in 2024 through fleet-standardization and bulk procurement.

Ongoing R&D and supplier collaboration ensure access to energy-efficient kit tied to Mota-Engil’s 2026 target of a 20% reduction in fleet CO2 intensity versus 2021, via hybrid drives and fuel-efficiency upgrades.

- Long-term OEM contracts (Caterpillar, Herrenknecht)

- €45m 2024 savings from procurement

- Targets: −20% fleet CO2 intensity by 2026 vs 2021

- Access to hybrid and low-emission equipment

National and Municipal Government Bodies

The group treats national and municipal governments as strategic partners, using Public-Private Partnerships (PPPs) to share risk and revenue in long-term concessions that underpin its multi-year €6.1bn backlog (FY2024) and 2024 revenue of €4.3bn.

- PPPs secure long-term cashflows and concession fees

- Governments provide regulatory support and project pipelines

- Shared capex reduces balance-sheet strain

Mota‑Engil €6.1bn backlog powered by CCCC, banks/ECAs, JVs, OEMs — €45m savings, -20% CO2

CCCC stake (2017) plus banks/ECAs, OEMs and local JVs underpin Mota-Engil’s €6.1bn backlog (FY2024), €4.3bn 2024 revenue, ~38% regional JV backlog, ~40% capex via ECA/loans, €45m 2024 procurement savings and target −20% fleet CO2 by 2026.

| Partner | Role | Key metric |

|---|---|---|

| CCCC | Equity & bids | €4.2bn new contracts (2021–25) |

| Banks/ECAs | Financing | ~40% capex via ECA/loans |

| Local JVs | Market access | 38% regional backlog |

| OEMs | Equipment | €45m savings (2024) |

| Governments | PPPs/concessions | €6.1bn backlog (FY2024) |

What is included in the product

A concise, pre-written Business Model Canvas for Mota-Engil detailing its nine blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure—aligned with its construction, engineering, and concessions strategy.

High-level, editable Business Model Canvas that distills Mota-Engil Group’s infrastructure and concessions strategy into a one-page tool, saving hours of formatting while enabling quick comparison, collaborative adaptation, and focused boardroom discussions.

Activities

Engineering and Large-Scale Construction

The core activity is designing, managing and executing complex civil works—highways, railways and bridges—driving 68% of group revenue and €1.2bn backlog at year-end 2025; projects use BIM, Lean and EPC contracts to meet fixed deadlines and 95% on-time delivery targets.

Environment and Waste Management Services

Mota-Engil operates municipal and industrial waste collection, treatment and recovery, running 12 treatment plants in Portugal, Poland and Angola and processing ~1.2 Mt/year (2024).

These circular-economy services (material recovery, energy-from-waste) generated €142m recurring revenue in 2024, stabilizing cash flow versus construction cycles.

Mining Support and Contract Mining

Mota-Engil provides end-to-end mining support—site preparation, excavation, and mineral transport—using a 2,300+ unit heavy-equipment fleet to serve major operations in Africa and Latin America. By 2025, mining services contributed ~14% of group revenue (≈€420m in 2024) as demand for transition minerals rose 18% y/y, cementing contract mining as a strategic growth pillar.

Infrastructure Concession Management

Managing long-term concessions for transport and water, Mota‑Engil runs operation and maintenance across asset lifecycles to sustain service levels and cashflows; its 2024 concessions backlog was ~€1.2bn, with EBITDA margins on concessions typically 20–30%.

This requires financial models forecasting 20–30 year cashflows, traffic/consumption growth rates (2–4%/yr), capex schedules, and discount rates ~7–9% to optimise returns.

- Long-term O&M and lifecycle oversight

- €1.2bn 2024 concessions backlog

- EBITDA margins ~20–30%

- Forecast horizons 20–30 years

- Discount rates ~7–9%

Energy and Industrial Maintenance

Mota-Engil develops energy infrastructure—including solar and wind projects and distribution networks—and delivers industrial maintenance for plants, supporting clients’ operational continuity and grid modernization.

In 2024 Mota-Engil reported €1.9bn revenue in engineering & construction and invested in renewables expansion amid Europe’s 2030 decarbonization targets.

- Builds renewables + grids

- Industrial maintenance for energy/manufacturing

- Supports decarbonization & grid modernisation

- 2024 group E&C revenue ~€1.9bn

Mota‑Engil: €1.9bn E&C + €1.2bn civil backlog, diversified in waste, mining & concessions

Mota‑Engil designs and delivers complex civil works (68% revenue; €1.2bn backlog 2025), runs waste services (12 plants; ~1.2Mt/yr; €142m recurring 2024), provides mining services (2,300+ fleet; ~14% revenue ≈€420m 2024), manages concessions (€1.2bn backlog 2024; EBITDA 20–30%) and builds renewables/grids (E&C revenue ~€1.9bn 2024).

| Activity | Key metric |

|---|---|

| Civil works | 68% rev, €1.2bn backlog (2025) |

| Waste | 12 plants, ~1.2Mt/yr, €142m (2024) |

| Mining | 2,300+ fleet, ~14% rev ≈€420m (2024) |

| Concessions | €1.2bn backlog (2024), EBITDA 20–30% |

| Energy/E&C | €1.9bn revenue (2024) |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the actual Mota-Engil Group Business Model Canvas—not a mockup. When you purchase, you’ll receive this same comprehensive file, fully formatted and ready to edit, present, or share. The delivered package includes the complete Canvas with all sections intact, in the same professional layout you see here. No placeholders, no surprises—what you preview is what you get.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Mota-Engil Business Model Canvas: Compact Strategic Blueprint for Investors & Advisors

Unlock the full strategic blueprint behind Mota-Engil Group with our Business Model Canvas—condensed insights on value propositions, key partners, revenue streams and cost drivers that explain how the group wins projects and scales globally; perfect for investors, consultants, and entrepreneurs seeking a ready-to-use, editable framework to benchmark strategy and drive decisions.

Partnerships

Strategic Alliance with China Communications Construction Company

The 2017 equity stake by China Communications Construction Company (CCCC) gives Mota-Engil stronger balance-sheet support and global procurement access, helping secure >€4.2bn in new international contracts from 2021–2025. By end-2025 the alliance enabled joint bids on mega-tenders, raising Mota-Engil’s large-project win rate in Africa, Latin America and Europe to ~28% of group backlog.

Financial Institutions and Export Credit Agencies

Mota-Engil relies on international banks and export credit agencies (ECAs) to secure project financing and performance bonds, with syndicated loans and ECA-backed facilities covering ~40% of its €1.2bn 2024 capex program. These partners mitigate long-term infrastructure risk in emerging markets and help structure complex project-finance deals that maintain liquidity across the project lifecycle, often providing tenors up to 15 years.

Local Joint Venture Partners

In Africa and Latin America Mota-Engil forms local joint ventures to meet local-content rules and speed permits, pairing Mota-Engil’s engineering and EPC (engineering, procurement, construction) capacity with partners’ market access and logistics; by 2024 these JVs accounted for ~38% of the Group’s regional backlog and reduced project delays by ~20%, lowering political/operational risk and improving community acceptance.

Specialized Technology and Equipment Suppliers

The group holds multi-year contracts with global OEMs like Caterpillar and Herrenknecht, securing heavy machinery for tunneling, bridge and mining projects; these agreements cut CAPEX volatility and saved an estimated €45m in 2024 through fleet-standardization and bulk procurement.

Ongoing R&D and supplier collaboration ensure access to energy-efficient kit tied to Mota-Engil’s 2026 target of a 20% reduction in fleet CO2 intensity versus 2021, via hybrid drives and fuel-efficiency upgrades.

- Long-term OEM contracts (Caterpillar, Herrenknecht)

- €45m 2024 savings from procurement

- Targets: −20% fleet CO2 intensity by 2026 vs 2021

- Access to hybrid and low-emission equipment

National and Municipal Government Bodies

The group treats national and municipal governments as strategic partners, using Public-Private Partnerships (PPPs) to share risk and revenue in long-term concessions that underpin its multi-year €6.1bn backlog (FY2024) and 2024 revenue of €4.3bn.

- PPPs secure long-term cashflows and concession fees

- Governments provide regulatory support and project pipelines

- Shared capex reduces balance-sheet strain

Mota‑Engil €6.1bn backlog powered by CCCC, banks/ECAs, JVs, OEMs — €45m savings, -20% CO2

CCCC stake (2017) plus banks/ECAs, OEMs and local JVs underpin Mota-Engil’s €6.1bn backlog (FY2024), €4.3bn 2024 revenue, ~38% regional JV backlog, ~40% capex via ECA/loans, €45m 2024 procurement savings and target −20% fleet CO2 by 2026.

| Partner | Role | Key metric |

|---|---|---|

| CCCC | Equity & bids | €4.2bn new contracts (2021–25) |

| Banks/ECAs | Financing | ~40% capex via ECA/loans |

| Local JVs | Market access | 38% regional backlog |

| OEMs | Equipment | €45m savings (2024) |

| Governments | PPPs/concessions | €6.1bn backlog (FY2024) |

What is included in the product

A concise, pre-written Business Model Canvas for Mota-Engil detailing its nine blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure—aligned with its construction, engineering, and concessions strategy.

High-level, editable Business Model Canvas that distills Mota-Engil Group’s infrastructure and concessions strategy into a one-page tool, saving hours of formatting while enabling quick comparison, collaborative adaptation, and focused boardroom discussions.

Activities

Engineering and Large-Scale Construction

The core activity is designing, managing and executing complex civil works—highways, railways and bridges—driving 68% of group revenue and €1.2bn backlog at year-end 2025; projects use BIM, Lean and EPC contracts to meet fixed deadlines and 95% on-time delivery targets.

Environment and Waste Management Services

Mota-Engil operates municipal and industrial waste collection, treatment and recovery, running 12 treatment plants in Portugal, Poland and Angola and processing ~1.2 Mt/year (2024).

These circular-economy services (material recovery, energy-from-waste) generated €142m recurring revenue in 2024, stabilizing cash flow versus construction cycles.

Mining Support and Contract Mining

Mota-Engil provides end-to-end mining support—site preparation, excavation, and mineral transport—using a 2,300+ unit heavy-equipment fleet to serve major operations in Africa and Latin America. By 2025, mining services contributed ~14% of group revenue (≈€420m in 2024) as demand for transition minerals rose 18% y/y, cementing contract mining as a strategic growth pillar.

Infrastructure Concession Management

Managing long-term concessions for transport and water, Mota‑Engil runs operation and maintenance across asset lifecycles to sustain service levels and cashflows; its 2024 concessions backlog was ~€1.2bn, with EBITDA margins on concessions typically 20–30%.

This requires financial models forecasting 20–30 year cashflows, traffic/consumption growth rates (2–4%/yr), capex schedules, and discount rates ~7–9% to optimise returns.

- Long-term O&M and lifecycle oversight

- €1.2bn 2024 concessions backlog

- EBITDA margins ~20–30%

- Forecast horizons 20–30 years

- Discount rates ~7–9%

Energy and Industrial Maintenance

Mota-Engil develops energy infrastructure—including solar and wind projects and distribution networks—and delivers industrial maintenance for plants, supporting clients’ operational continuity and grid modernization.

In 2024 Mota-Engil reported €1.9bn revenue in engineering & construction and invested in renewables expansion amid Europe’s 2030 decarbonization targets.

- Builds renewables + grids

- Industrial maintenance for energy/manufacturing

- Supports decarbonization & grid modernisation

- 2024 group E&C revenue ~€1.9bn

Mota‑Engil: €1.9bn E&C + €1.2bn civil backlog, diversified in waste, mining & concessions

Mota‑Engil designs and delivers complex civil works (68% revenue; €1.2bn backlog 2025), runs waste services (12 plants; ~1.2Mt/yr; €142m recurring 2024), provides mining services (2,300+ fleet; ~14% revenue ≈€420m 2024), manages concessions (€1.2bn backlog 2024; EBITDA 20–30%) and builds renewables/grids (E&C revenue ~€1.9bn 2024).

| Activity | Key metric |

|---|---|

| Civil works | 68% rev, €1.2bn backlog (2025) |

| Waste | 12 plants, ~1.2Mt/yr, €142m (2024) |

| Mining | 2,300+ fleet, ~14% rev ≈€420m (2024) |

| Concessions | €1.2bn backlog (2024), EBITDA 20–30% |

| Energy/E&C | €1.9bn revenue (2024) |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the actual Mota-Engil Group Business Model Canvas—not a mockup. When you purchase, you’ll receive this same comprehensive file, fully formatted and ready to edit, present, or share. The delivered package includes the complete Canvas with all sections intact, in the same professional layout you see here. No placeholders, no surprises—what you preview is what you get.