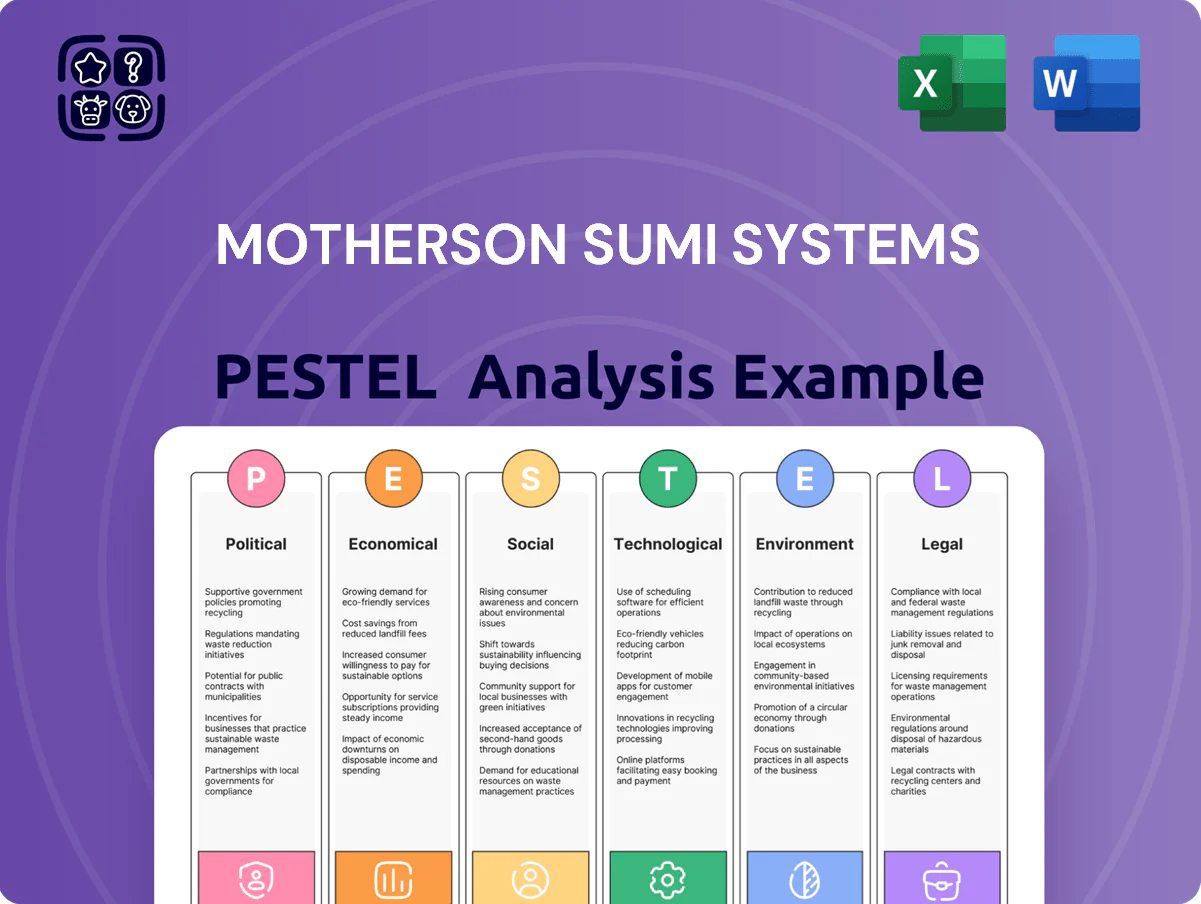

Motherson Sumi Systems PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain strategic clarity on Motherson Sumi Systems with our concise PESTLE overview—highlighting regulatory pressures, supply-chain vulnerabilities, EV-driven tech shifts, and sustainability risks shaping future margins; purchase the full analysis to access detailed scenarios, actionable recommendations, and editable charts for immediate use.

Political factors

Geopolitical Trade Relations

Operating in over 40 countries as of late 2025, Motherson Sumi Systems faces heightened exposure to shifting trade alliances and rising protectionism—OECD reports 12% increase in trade-restrictive measures since 2021—threatening cross-border flow of its automotive components. Trade tensions between major economies risk disrupting supply chains and logistics, prompting the company to expand local manufacturing hubs; Motherson’s international revenue mix was ~60% in FY2024, underscoring the need for geographic diversification. Management must navigate tariff volatility and regulatory divergence to preserve global supply chain resilience and protect margins.

Government EV Incentives

India’s PLI scheme for auto and drone components, allocating INR 25,938 crore in 2021–22, continues to incentivize Motherson Sumi Systems to localize high-tech EV components; the company reported FY2024 auto revenues of INR 46,000 crore, with EV-related product lines growing double digits year-on-year. Sustained political backing for renewables and EV targets (30% new vehicle EV share by 2030 per NITI Aayog discussions) supports MSSL’s long-term capex and localization strategy.

Regulatory Stability in Emerging Markets

Expansion into emerging markets requires navigating diverse political landscapes and varying regulatory stability; Motherson reported 28% of FY2024 revenue from APAC and Africa, exposing it to shifting rules that can raise compliance costs by an estimated 2–4% of operating margins in volatile periods.

Political shifts in Southeast Asia and Africa have previously affected supply-chain lead times by up to 15% and capex risk; Motherson limits exposure through local JV structures and government liaison teams.

The company mitigates risk by maintaining strong government relationships and diversifying its footprint across 41 countries, with FY2024 capex of ~USD 320 million supporting geographically balanced growth.

Foreign Direct Investment Policies

Changes in FDI rules in India, US, and EU affect Motherson Sumi Systems’ acquisition pace; India’s 2023 FDI policy liberalizations supported inbound deals, aiding Samvardhana Motherson’s $1.4bn 2022–24 deal flow.

Liberalized regimes enable smoother integration of global subsidiaries, improving consolidation of 2024 revenues of €6.8bn across auto components operations.

Heightened scrutiny on cross-border tech investments, especially in the US and EU, could slow future moves into electronics and ADAS, where Motherson targets double-digit growth.

- FDI liberalization aided $1.4bn deal activity (2022–24)

- 2024 consolidated revenues €6.8bn facilitate integrations

- Stricter tech-sector scrutiny in US/EU poses regulatory risk

Global Conflict and Supply Routes

Ongoing regional conflicts in 2025 have forced rerouting of logistics, increasing average lead times by ~12% and pushing shipping costs up about 9% year-over-year for global auto suppliers like Motherson Sumi Systems.

Political instability in key transit corridors has led the company to raise buffer inventory—estimates suggest a 15% rise in working capital tied to inventory—and to diversify into air and multimodal transport options.

Active geopolitical risk management remains critical to secure uninterrupted parts delivery to global OEMs, protecting revenue streams that generated INR 1.2 trillion in consolidated FY 2024–25 sales.

- Lead times +12%

- Shipping costs +9% YoY

- Inventory-related working capital +15%

- FY24–25 consolidated sales INR 1.2 trillion

Motherson faces trade and policy headwinds amid rising supply costs and EV-focused incentives

Political risks—trade protectionism (OECD: trade-restrictive measures +12% since 2021), FDI rule shifts (India liberalized 2023), and tech-investment scrutiny in US/EU—impact Motherson’s cross-border M&A ($1.4bn deals 2022–24), supply-chain costs (lead times +12%, shipping +9%) and FY24–25 consolidated sales INR 1.2tn; PLI incentives (INR 25,938cr) support EV localization and capex (~USD 320m FY2024).

| Metric | Value |

|---|---|

| Trade measures change | +12% |

| Lead times | +12% |

| Shipping cost YoY | +9% |

| FY24–25 sales | INR 1.2tn |

What is included in the product

Explores how external macro-environmental factors uniquely affect Motherson Sumi Systems across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and sector-specific examples to inform strategy and risk management.

A concise PESTLE snapshot of Motherson Sumi Systems, segmented by Political, Economic, Social, Technological, Legal, and Environmental factors for quick reference in meetings or presentations.

Economic factors

Global Interest Rate Environment

As of late 2025, stabilized global policy rates—US Fed at 5.25–5.50%, ECB ~3.75%, RBI at 6.50%—directly affect Motherson Sumi Systems’ debt servicing for frequent acquisitions; sustained high rates have compressed margins and raised blended borrowing costs above 6% for recent deals, while any easing could cut acquisition financing costs by 100–200 basis points, so treasury must track Fed, ECB and RBI moves closely.

Raw Material Price Volatility

Fluctuations in copper, aluminum and high-grade polymer prices directly alter Motherson Sumi Systems production costs for wiring harnesses and modules; copper rose ~22% in 2024 while aluminum gained ~18%, squeezing gross margins. The company uses pass-through contracts with many OEM clients to transfer cost increases, but timing lags have caused quarterly EBITDA volatility—Q3 2024 margin swing ~120 bps. Efficient commodity hedging remains critical; Motherson reported hedging exposures covering roughly 45% of near-term metal needs as of FY2024.

Currency Exchange Fluctuations

Motherson Sumi Systems reports over 50% of FY2024 revenue from Europe, North America and Japan, exposing it to EUR, USD and JPY swings; a 5% INR appreciation vs these currencies could cut reported revenue by ~2–3% (FY2024 consolidated turnover Rs 1,23,750 crore).

INR depreciation conversely boosts translated revenues but raises imported input costs; FY2024 operating margin sensitivity to a 5% FX move estimated at ~40–80 bps.

The company maintains centralized treasury and hedging programs—forward contracts and natural hedges—to manage multi-currency cash flows and reduce translation volatility.

Consumer Spending and Auto Demand

The global auto cycle affects Motherson Sumi Systems as macro slowdowns cut new-vehicle demand; global light-vehicle sales slipped 3% in 2024 to about 78.6 million units, pressuring supplier order books and OEM production plans.

Lower consumer confidence in 2024 led to deferred purchases, reducing OEM component orders; however by 2025 demand has tilted toward premium segments, which showed resilience with luxury vehicle sales up ~4% year-on-year.

- 2024 global light-vehicle sales ≈ 78.6M (-3%)

- Deferred purchases lowered OEM orders in 2024

- Premium segment growth ~+4% in 2025, offering stability

Inflationary Pressures on Labor

Rising wages in Eastern Europe and Mexico have pushed manufacturing labor costs up 6–9% YoY in 2023–2024, increasing overhead for Motherson Sumi’s wiring harness and seating operations.

To offset this, the company accelerated automation investments—capital expenditure rose to €1.1bn in FY2024—and launched operational excellence programs improving productivity by ~8%.

Balancing cost competitiveness with fair pay remains critical as average hourly wages climb; Motherson targets efficiency gains to protect margins while complying with labor standards.

- Wage inflation 6–9% YoY (EE/Mexico, 2023–24)

- FY2024 capex €1.1bn—automation focus

- Productivity gains ~8% via OPEX programs

- Strategy: efficiency to maintain margins while ensuring fair compensation

Rising rates, commodity shocks and FX hit margins — easing could cut costs 100–200bps

High global rates (Fed 5.25–5.50%, ECB ~3.75%, RBI 6.50% in late 2025) raised blended borrowing costs >6%, squeezing margins on acquisitions; easing could lower costs 100–200 bps. Commodity spikes (copper +22%, aluminum +18% in 2024) increased input costs; hedges cover ~45% near-term needs. FX moves: 5% INR appreciation cuts reported revenue ~2–3% (FY2024 turnover Rs 1,23,750 crore); 5% FX shift alters operating margin ~40–80 bps.

| Metric | Value |

|---|---|

| FY2024 Revenue | Rs 1,23,750 crore |

| Blended borrowing cost | >6% |

| Copper/Aluminum (2024) | +22% / +18% |

| Hedging coverage | ~45% |

| FX sensitivity (5% INR) | Revenue -2–3%; Margin ±40–80 bps |

Same Document Delivered

Motherson Sumi Systems PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; it contains a concise PESTLE analysis of Motherson Sumi Systems covering political, economic, social, technological, legal, and environmental factors to inform strategic decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain strategic clarity on Motherson Sumi Systems with our concise PESTLE overview—highlighting regulatory pressures, supply-chain vulnerabilities, EV-driven tech shifts, and sustainability risks shaping future margins; purchase the full analysis to access detailed scenarios, actionable recommendations, and editable charts for immediate use.

Political factors

Geopolitical Trade Relations

Operating in over 40 countries as of late 2025, Motherson Sumi Systems faces heightened exposure to shifting trade alliances and rising protectionism—OECD reports 12% increase in trade-restrictive measures since 2021—threatening cross-border flow of its automotive components. Trade tensions between major economies risk disrupting supply chains and logistics, prompting the company to expand local manufacturing hubs; Motherson’s international revenue mix was ~60% in FY2024, underscoring the need for geographic diversification. Management must navigate tariff volatility and regulatory divergence to preserve global supply chain resilience and protect margins.

Government EV Incentives

India’s PLI scheme for auto and drone components, allocating INR 25,938 crore in 2021–22, continues to incentivize Motherson Sumi Systems to localize high-tech EV components; the company reported FY2024 auto revenues of INR 46,000 crore, with EV-related product lines growing double digits year-on-year. Sustained political backing for renewables and EV targets (30% new vehicle EV share by 2030 per NITI Aayog discussions) supports MSSL’s long-term capex and localization strategy.

Regulatory Stability in Emerging Markets

Expansion into emerging markets requires navigating diverse political landscapes and varying regulatory stability; Motherson reported 28% of FY2024 revenue from APAC and Africa, exposing it to shifting rules that can raise compliance costs by an estimated 2–4% of operating margins in volatile periods.

Political shifts in Southeast Asia and Africa have previously affected supply-chain lead times by up to 15% and capex risk; Motherson limits exposure through local JV structures and government liaison teams.

The company mitigates risk by maintaining strong government relationships and diversifying its footprint across 41 countries, with FY2024 capex of ~USD 320 million supporting geographically balanced growth.

Foreign Direct Investment Policies

Changes in FDI rules in India, US, and EU affect Motherson Sumi Systems’ acquisition pace; India’s 2023 FDI policy liberalizations supported inbound deals, aiding Samvardhana Motherson’s $1.4bn 2022–24 deal flow.

Liberalized regimes enable smoother integration of global subsidiaries, improving consolidation of 2024 revenues of €6.8bn across auto components operations.

Heightened scrutiny on cross-border tech investments, especially in the US and EU, could slow future moves into electronics and ADAS, where Motherson targets double-digit growth.

- FDI liberalization aided $1.4bn deal activity (2022–24)

- 2024 consolidated revenues €6.8bn facilitate integrations

- Stricter tech-sector scrutiny in US/EU poses regulatory risk

Global Conflict and Supply Routes

Ongoing regional conflicts in 2025 have forced rerouting of logistics, increasing average lead times by ~12% and pushing shipping costs up about 9% year-over-year for global auto suppliers like Motherson Sumi Systems.

Political instability in key transit corridors has led the company to raise buffer inventory—estimates suggest a 15% rise in working capital tied to inventory—and to diversify into air and multimodal transport options.

Active geopolitical risk management remains critical to secure uninterrupted parts delivery to global OEMs, protecting revenue streams that generated INR 1.2 trillion in consolidated FY 2024–25 sales.

- Lead times +12%

- Shipping costs +9% YoY

- Inventory-related working capital +15%

- FY24–25 consolidated sales INR 1.2 trillion

Motherson faces trade and policy headwinds amid rising supply costs and EV-focused incentives

Political risks—trade protectionism (OECD: trade-restrictive measures +12% since 2021), FDI rule shifts (India liberalized 2023), and tech-investment scrutiny in US/EU—impact Motherson’s cross-border M&A ($1.4bn deals 2022–24), supply-chain costs (lead times +12%, shipping +9%) and FY24–25 consolidated sales INR 1.2tn; PLI incentives (INR 25,938cr) support EV localization and capex (~USD 320m FY2024).

| Metric | Value |

|---|---|

| Trade measures change | +12% |

| Lead times | +12% |

| Shipping cost YoY | +9% |

| FY24–25 sales | INR 1.2tn |

What is included in the product

Explores how external macro-environmental factors uniquely affect Motherson Sumi Systems across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and sector-specific examples to inform strategy and risk management.

A concise PESTLE snapshot of Motherson Sumi Systems, segmented by Political, Economic, Social, Technological, Legal, and Environmental factors for quick reference in meetings or presentations.

Economic factors

Global Interest Rate Environment

As of late 2025, stabilized global policy rates—US Fed at 5.25–5.50%, ECB ~3.75%, RBI at 6.50%—directly affect Motherson Sumi Systems’ debt servicing for frequent acquisitions; sustained high rates have compressed margins and raised blended borrowing costs above 6% for recent deals, while any easing could cut acquisition financing costs by 100–200 basis points, so treasury must track Fed, ECB and RBI moves closely.

Raw Material Price Volatility

Fluctuations in copper, aluminum and high-grade polymer prices directly alter Motherson Sumi Systems production costs for wiring harnesses and modules; copper rose ~22% in 2024 while aluminum gained ~18%, squeezing gross margins. The company uses pass-through contracts with many OEM clients to transfer cost increases, but timing lags have caused quarterly EBITDA volatility—Q3 2024 margin swing ~120 bps. Efficient commodity hedging remains critical; Motherson reported hedging exposures covering roughly 45% of near-term metal needs as of FY2024.

Currency Exchange Fluctuations

Motherson Sumi Systems reports over 50% of FY2024 revenue from Europe, North America and Japan, exposing it to EUR, USD and JPY swings; a 5% INR appreciation vs these currencies could cut reported revenue by ~2–3% (FY2024 consolidated turnover Rs 1,23,750 crore).

INR depreciation conversely boosts translated revenues but raises imported input costs; FY2024 operating margin sensitivity to a 5% FX move estimated at ~40–80 bps.

The company maintains centralized treasury and hedging programs—forward contracts and natural hedges—to manage multi-currency cash flows and reduce translation volatility.

Consumer Spending and Auto Demand

The global auto cycle affects Motherson Sumi Systems as macro slowdowns cut new-vehicle demand; global light-vehicle sales slipped 3% in 2024 to about 78.6 million units, pressuring supplier order books and OEM production plans.

Lower consumer confidence in 2024 led to deferred purchases, reducing OEM component orders; however by 2025 demand has tilted toward premium segments, which showed resilience with luxury vehicle sales up ~4% year-on-year.

- 2024 global light-vehicle sales ≈ 78.6M (-3%)

- Deferred purchases lowered OEM orders in 2024

- Premium segment growth ~+4% in 2025, offering stability

Inflationary Pressures on Labor

Rising wages in Eastern Europe and Mexico have pushed manufacturing labor costs up 6–9% YoY in 2023–2024, increasing overhead for Motherson Sumi’s wiring harness and seating operations.

To offset this, the company accelerated automation investments—capital expenditure rose to €1.1bn in FY2024—and launched operational excellence programs improving productivity by ~8%.

Balancing cost competitiveness with fair pay remains critical as average hourly wages climb; Motherson targets efficiency gains to protect margins while complying with labor standards.

- Wage inflation 6–9% YoY (EE/Mexico, 2023–24)

- FY2024 capex €1.1bn—automation focus

- Productivity gains ~8% via OPEX programs

- Strategy: efficiency to maintain margins while ensuring fair compensation

Rising rates, commodity shocks and FX hit margins — easing could cut costs 100–200bps

High global rates (Fed 5.25–5.50%, ECB ~3.75%, RBI 6.50% in late 2025) raised blended borrowing costs >6%, squeezing margins on acquisitions; easing could lower costs 100–200 bps. Commodity spikes (copper +22%, aluminum +18% in 2024) increased input costs; hedges cover ~45% near-term needs. FX moves: 5% INR appreciation cuts reported revenue ~2–3% (FY2024 turnover Rs 1,23,750 crore); 5% FX shift alters operating margin ~40–80 bps.

| Metric | Value |

|---|---|

| FY2024 Revenue | Rs 1,23,750 crore |

| Blended borrowing cost | >6% |

| Copper/Aluminum (2024) | +22% / +18% |

| Hedging coverage | ~45% |

| FX sensitivity (5% INR) | Revenue -2–3%; Margin ±40–80 bps |

Same Document Delivered

Motherson Sumi Systems PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; it contains a concise PESTLE analysis of Motherson Sumi Systems covering political, economic, social, technological, legal, and environmental factors to inform strategic decisions.