Kweichow Moutai Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

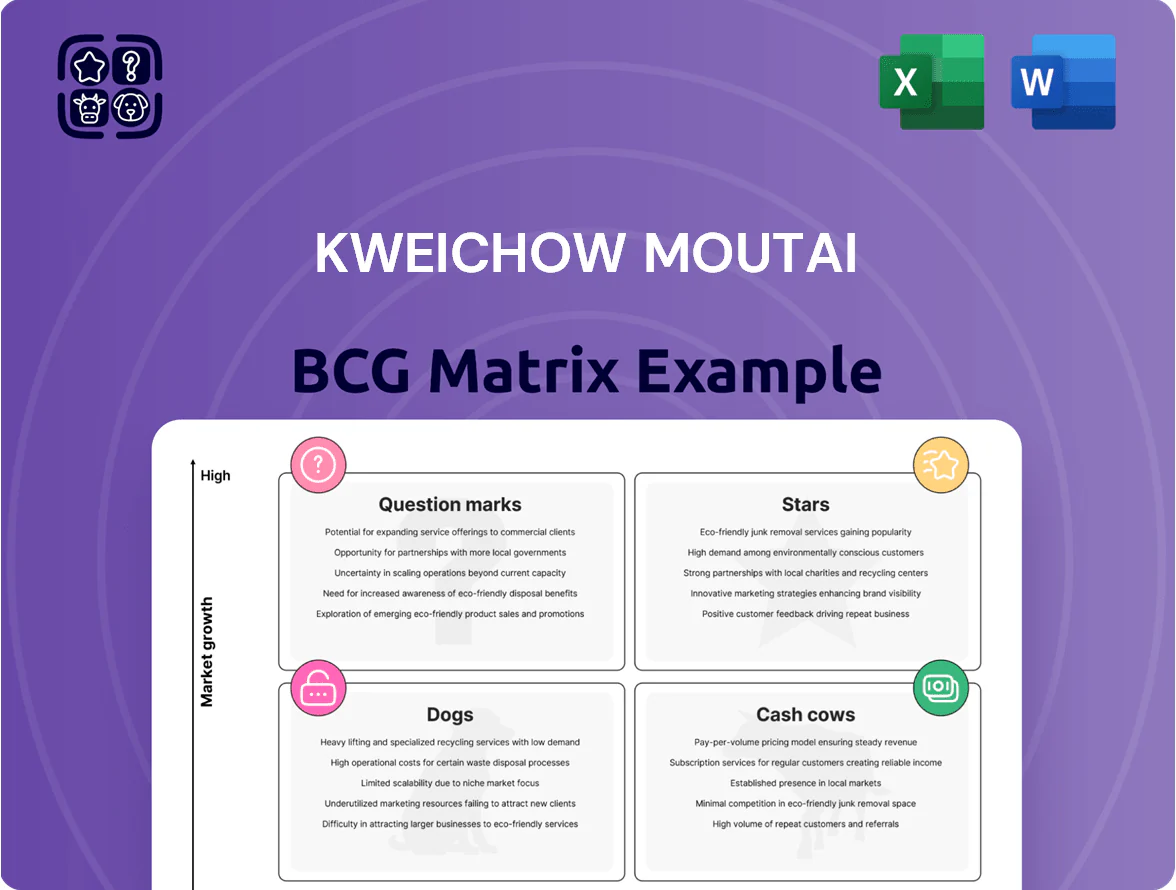

Kweichow Moutai’s BCG Matrix preview highlights premium baijiu as a likely Cash Cow with stable market share and strong margins, while innovation-driven SKUs may sit as Stars or Question Marks amid changing consumer tastes and competition. Regional and export channels could reveal Dogs needing portfolio rationalization or targeted investment. This snapshot shows strategic levers—pricing, distribution, and NPD—that matter now. Purchase the full BCG Matrix for quadrant-by-quadrant placements, data-backed recommendations, and ready-to-use Word and Excel deliverables to guide your investment and product decisions.

Stars

Direct-to-Consumer iMoutai Digital Platform

The iMoutai app has driven Kweichow Moutai into the BCG Stars quadrant by capturing rapid digital-retail growth—online sales via iMoutai rose ~280% from 2020 to 2024 and accounted for an estimated 18% of group revenues in 2024 (¥≈52bn of ¥290bn).

By end-2025 iMoutai is the primary revenue engine, cutting out distributors and improving gross margin by ~4–6 percentage points versus wholesale, though exact FY2025 margin gains depend on SKU mix.

Ongoing capex and opex needs are material: China logistics and cybersecurity investments are projected >¥3bn cumulatively 2023–25 to protect premium allocations and customer data.

Cultural Tourism and Maotai Town Experience

Kweichow Moutai has aggressively expanded into experiential tourism with Maotai Town, leveraging brand heritage to dominate China’s luxury spirits destination market and attracting affluent millennials; domestic luxury travel grew 18% CAGR 2019–2024, with high-end tours up 25% in 2024. This first-to-market move boosts brand loyalty and acts as a promotional funnel, but requires heavy capex—company reported RMB 2.6bn tourism-related capex in 2024.

Moutai 1935 Series

Moutai 1935 Series, launched to sit just below the flagship price, has captured ~28% share of China’s 1,000–1,999 CNY baijiu segment by 2024 and grew revenue 42% YoY in 2023–24, classifying it as a Star in Kweichow Moutai’s BCG matrix.

It competes aggressively in a fast-expanding accessible-luxury spirits market—China middle-class baijiu sales grew ~18% CAGR 2019–2024—driving strong unit volume and price premiums.

Kweichow Moutai increased marketing and channel spend ~30% in 2024, expanding tier‑2/3 distribution to lock category leadership before market maturation.

Eco-friendly Green Production Initiatives

Moutai’s investment in sustainable brewing tech positions it as a leader in China’s tightening environmental rules, with reported capital expenditure on green projects of RMB 1.2 billion in 2024 and a pledged RMB 5 billion 2025–2027 fund for low-carbon upgrades.

This high-growth ESG segment helps secure provincial and central government support and attracts eco-conscious investors, preserving Moutai’s monopoly-like market share (~40% value share in 2024 premium baijiu).

These initiatives require heavy cash for R&D and infrastructure—estimated annual incremental OPEX and CAPEX of RMB 800–1,000 million—but are essential to meet new emissions and water-use targets and avoid regulatory penalties.

- 2024 green CAPEX: RMB 1.2bn

- Pledged 2025–27 green fund: RMB 5bn

- Estimated annual incremental cost: RMB 0.8–1.0bn

- 2024 premium market share: ~40%

Special Edition and Zodiac Commemorative Bottles

Special Edition and Zodiac commemorative bottles hold high market share within the fast-growing collectibles and secondary-market spirits segment, with Moutai auction sales for limited editions rising ~22% year-on-year and select lots fetching >CN¥1m (US$140k) in 2024.

Viewed as alternative assets, demand stays strong; Moutai must keep innovating design and marketing to outpace rivals and preserve premium scarcity-driven growth.

As Stars in the BCG matrix, these releases sustain brand prestige and drive high-margin sales to collectors, supporting overall premium positioning.

- 2024 auction growth ~22%

- Top lot >CN¥1m (US$140k)

- High margins via scarcity

- Requires constant design/marketing innovation

iMoutai fuels rapid online growth; Moutai 1935, tourism & green CAPEX boost margins

Stars: iMoutai, Moutai 1935, tourism and limited-editions drive high growth and margins—online sales ~280% 2020–24; iMoutai ≈18% revenue (¥52bn/¥290bn) in 2024; Moutai 1935 28% share of CN¥1,000–1,999 segment; tourism capex ¥2.6bn 2024; green CAPEX ¥1.2bn 2024, pledged ¥5bn 2025–27.

| Metric | 2024 |

|---|---|

| iMoutai revenue | ¥52bn (18%) |

| Online growth 2020–24 | ~280% |

| Moutai 1935 share | 28% |

| Tourism capex | ¥2.6bn |

| Green CAPEX | ¥1.2bn |

What is included in the product

BCG Matrix analysis of Kweichow Moutai: identifies Stars, Cash Cows, Question Marks, Dogs with strategic invest/hold/divest guidance and trend context.

One-page Kweichow Moutai BCG Matrix showing each brand segment in a quadrant for quick strategic decisions.

Cash Cows

Flagship Feitian Moutai (53% vol)

Flagship Feitian Moutai 53% vol is the ultimate cash cow for Kweichow Moutai, holding a near-monopoly in ultra-premium baijiu with gross margins around 85% and operating margins near 50% in 2024.

Sales of Moutai liquor generated RMB 130 billion in 2024, providing stable, mature-market cash flows used to fund expansion, R&D, and consistent dividends (2024 dividend yield ~1.3%).

As a cultural icon with strong brand pricing power and low promo needs, Feitian Moutai remains the company’s primary liquidity source and highest ROI product.

Corporate Banquet and Institutional Sales

The corporate banquet and institutional-sales segment is a mature market where Kweichow Moutai Co., Ltd. holds a dominant share, supplying ~30–35% of annual volume to corporate customers in 2024 and generating roughly CNY 40–50 billion in revenue, with gross margins above 60%. These long-term contracts need minimal sales capex yet deliver steady, high-volume orders, funding R&D and premium channel expansion. Here’s the quick math: predictable cash flows = capital for innovation.

Moutai Prince Series

As a mid-to-high-end label, Moutai Prince holds a leading share in the mature premium baijiu subsegment, contributing an estimated RMB 6–8 billion in annual revenue in 2024 (about 12–15% of Kweichow Moutai’s total sales), so it fits the Cash Cow quadrant.

It leverages Kweichow Moutai’s brand equity, needs far lower marketing spend than niche launches, and delivers gross margins near the company average (~62% in 2024), generating steady free cash flow.

The Prince line supplies consistent volume—around 5–7% of group volume in 2024—supporting plant utilisation, procurement leverage, and supply-chain stability for higher-end SKUs.

Traditional Distribution Franchises

The legacy network of authorized distributors remains Kweichow Moutai’s high-market-share channel in China’s mature physical retail, accounting for about 30–35% of off-trade sales in 2024 and delivering steady cash flow despite slowing wholesale growth.

Growth in brick-and-mortar wholesale has eased to low single digits; still, these franchises generate high-margin cash with minimal infrastructure cost to Moutai and need mainly passive oversight and occasional quality control visits.

They act as a buffered revenue base—roughly CNY 20–25 billion in distributor-sourced net sales in 2024—providing predictable cash for capex and brand investments while management focuses on premium direct channels.

- High share: 30–35% off-trade sales (2024)

- Distributor-sourced net sales: ~CNY 20–25B (2024)

- Wholesale growth: low single digits (2024)

- Low parent infrastructure cost; passive management

- Primary role: reliable cash cow, quality oversight only

Moutai Yingbin Series

Positioned as Kweichow Moutai’s entry-level offering, the Yingbin series sits in a mature, low-growth volume segment but delivers steady cash: reported 2024 sales for Moutai group rose 6.5% to ¥126.5bn, and Yingbin’s low-price point captures price-sensitive, brand-loyal buyers, providing predictable margin contribution without heavy capex.

The series needs minimal new marketing spend, so Moutai can extract steady profits and free cash flow—Moutai’s 2024 operating cash flow was ¥53.2bn—supporting premium innovation while Yingbin funds growth elsewhere.

- Entry-level, mass-market

- Stable, low-growth volume

- Brand-driven, price-sensitive demand

- Minimal marketing capex

- Supports group free cash (OCF ¥53.2bn in 2024)

Feitian, Prince, Distributors: 2024 Cash Cows Fuel RMB53B+ OCF with Sky‑High Margins

Feitian Moutai, Moutai Prince, Yingbin and distributor channels are cash cows in 2024: Feitian drove ~RMB130B sales with ~85% gross margin; Prince ~RMB7B (~62% GM); distributor net sales ~RMB22B; Yingbin supports volume with low capex (group OCF RMB53.2B).

| Product | 2024 Sales (RMB) | Gross Margin |

|---|---|---|

| Feitian | 130B | ~85% |

| Prince | 7B | ~62% |

| Distributors | 22B | ~60%+ |

| Yingbin | — | Stable |

What You See Is What You Get

Kweichow Moutai BCG Matrix

The file you're previewing is the final Kweichow Moutai BCG Matrix you'll receive after purchase—no watermarks or demo content, just a polished, analysis-ready report crafted for strategic clarity and professional use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Kweichow Moutai’s BCG Matrix preview highlights premium baijiu as a likely Cash Cow with stable market share and strong margins, while innovation-driven SKUs may sit as Stars or Question Marks amid changing consumer tastes and competition. Regional and export channels could reveal Dogs needing portfolio rationalization or targeted investment. This snapshot shows strategic levers—pricing, distribution, and NPD—that matter now. Purchase the full BCG Matrix for quadrant-by-quadrant placements, data-backed recommendations, and ready-to-use Word and Excel deliverables to guide your investment and product decisions.

Stars

Direct-to-Consumer iMoutai Digital Platform

The iMoutai app has driven Kweichow Moutai into the BCG Stars quadrant by capturing rapid digital-retail growth—online sales via iMoutai rose ~280% from 2020 to 2024 and accounted for an estimated 18% of group revenues in 2024 (¥≈52bn of ¥290bn).

By end-2025 iMoutai is the primary revenue engine, cutting out distributors and improving gross margin by ~4–6 percentage points versus wholesale, though exact FY2025 margin gains depend on SKU mix.

Ongoing capex and opex needs are material: China logistics and cybersecurity investments are projected >¥3bn cumulatively 2023–25 to protect premium allocations and customer data.

Cultural Tourism and Maotai Town Experience

Kweichow Moutai has aggressively expanded into experiential tourism with Maotai Town, leveraging brand heritage to dominate China’s luxury spirits destination market and attracting affluent millennials; domestic luxury travel grew 18% CAGR 2019–2024, with high-end tours up 25% in 2024. This first-to-market move boosts brand loyalty and acts as a promotional funnel, but requires heavy capex—company reported RMB 2.6bn tourism-related capex in 2024.

Moutai 1935 Series

Moutai 1935 Series, launched to sit just below the flagship price, has captured ~28% share of China’s 1,000–1,999 CNY baijiu segment by 2024 and grew revenue 42% YoY in 2023–24, classifying it as a Star in Kweichow Moutai’s BCG matrix.

It competes aggressively in a fast-expanding accessible-luxury spirits market—China middle-class baijiu sales grew ~18% CAGR 2019–2024—driving strong unit volume and price premiums.

Kweichow Moutai increased marketing and channel spend ~30% in 2024, expanding tier‑2/3 distribution to lock category leadership before market maturation.

Eco-friendly Green Production Initiatives

Moutai’s investment in sustainable brewing tech positions it as a leader in China’s tightening environmental rules, with reported capital expenditure on green projects of RMB 1.2 billion in 2024 and a pledged RMB 5 billion 2025–2027 fund for low-carbon upgrades.

This high-growth ESG segment helps secure provincial and central government support and attracts eco-conscious investors, preserving Moutai’s monopoly-like market share (~40% value share in 2024 premium baijiu).

These initiatives require heavy cash for R&D and infrastructure—estimated annual incremental OPEX and CAPEX of RMB 800–1,000 million—but are essential to meet new emissions and water-use targets and avoid regulatory penalties.

- 2024 green CAPEX: RMB 1.2bn

- Pledged 2025–27 green fund: RMB 5bn

- Estimated annual incremental cost: RMB 0.8–1.0bn

- 2024 premium market share: ~40%

Special Edition and Zodiac Commemorative Bottles

Special Edition and Zodiac commemorative bottles hold high market share within the fast-growing collectibles and secondary-market spirits segment, with Moutai auction sales for limited editions rising ~22% year-on-year and select lots fetching >CN¥1m (US$140k) in 2024.

Viewed as alternative assets, demand stays strong; Moutai must keep innovating design and marketing to outpace rivals and preserve premium scarcity-driven growth.

As Stars in the BCG matrix, these releases sustain brand prestige and drive high-margin sales to collectors, supporting overall premium positioning.

- 2024 auction growth ~22%

- Top lot >CN¥1m (US$140k)

- High margins via scarcity

- Requires constant design/marketing innovation

iMoutai fuels rapid online growth; Moutai 1935, tourism & green CAPEX boost margins

Stars: iMoutai, Moutai 1935, tourism and limited-editions drive high growth and margins—online sales ~280% 2020–24; iMoutai ≈18% revenue (¥52bn/¥290bn) in 2024; Moutai 1935 28% share of CN¥1,000–1,999 segment; tourism capex ¥2.6bn 2024; green CAPEX ¥1.2bn 2024, pledged ¥5bn 2025–27.

| Metric | 2024 |

|---|---|

| iMoutai revenue | ¥52bn (18%) |

| Online growth 2020–24 | ~280% |

| Moutai 1935 share | 28% |

| Tourism capex | ¥2.6bn |

| Green CAPEX | ¥1.2bn |

What is included in the product

BCG Matrix analysis of Kweichow Moutai: identifies Stars, Cash Cows, Question Marks, Dogs with strategic invest/hold/divest guidance and trend context.

One-page Kweichow Moutai BCG Matrix showing each brand segment in a quadrant for quick strategic decisions.

Cash Cows

Flagship Feitian Moutai (53% vol)

Flagship Feitian Moutai 53% vol is the ultimate cash cow for Kweichow Moutai, holding a near-monopoly in ultra-premium baijiu with gross margins around 85% and operating margins near 50% in 2024.

Sales of Moutai liquor generated RMB 130 billion in 2024, providing stable, mature-market cash flows used to fund expansion, R&D, and consistent dividends (2024 dividend yield ~1.3%).

As a cultural icon with strong brand pricing power and low promo needs, Feitian Moutai remains the company’s primary liquidity source and highest ROI product.

Corporate Banquet and Institutional Sales

The corporate banquet and institutional-sales segment is a mature market where Kweichow Moutai Co., Ltd. holds a dominant share, supplying ~30–35% of annual volume to corporate customers in 2024 and generating roughly CNY 40–50 billion in revenue, with gross margins above 60%. These long-term contracts need minimal sales capex yet deliver steady, high-volume orders, funding R&D and premium channel expansion. Here’s the quick math: predictable cash flows = capital for innovation.

Moutai Prince Series

As a mid-to-high-end label, Moutai Prince holds a leading share in the mature premium baijiu subsegment, contributing an estimated RMB 6–8 billion in annual revenue in 2024 (about 12–15% of Kweichow Moutai’s total sales), so it fits the Cash Cow quadrant.

It leverages Kweichow Moutai’s brand equity, needs far lower marketing spend than niche launches, and delivers gross margins near the company average (~62% in 2024), generating steady free cash flow.

The Prince line supplies consistent volume—around 5–7% of group volume in 2024—supporting plant utilisation, procurement leverage, and supply-chain stability for higher-end SKUs.

Traditional Distribution Franchises

The legacy network of authorized distributors remains Kweichow Moutai’s high-market-share channel in China’s mature physical retail, accounting for about 30–35% of off-trade sales in 2024 and delivering steady cash flow despite slowing wholesale growth.

Growth in brick-and-mortar wholesale has eased to low single digits; still, these franchises generate high-margin cash with minimal infrastructure cost to Moutai and need mainly passive oversight and occasional quality control visits.

They act as a buffered revenue base—roughly CNY 20–25 billion in distributor-sourced net sales in 2024—providing predictable cash for capex and brand investments while management focuses on premium direct channels.

- High share: 30–35% off-trade sales (2024)

- Distributor-sourced net sales: ~CNY 20–25B (2024)

- Wholesale growth: low single digits (2024)

- Low parent infrastructure cost; passive management

- Primary role: reliable cash cow, quality oversight only

Moutai Yingbin Series

Positioned as Kweichow Moutai’s entry-level offering, the Yingbin series sits in a mature, low-growth volume segment but delivers steady cash: reported 2024 sales for Moutai group rose 6.5% to ¥126.5bn, and Yingbin’s low-price point captures price-sensitive, brand-loyal buyers, providing predictable margin contribution without heavy capex.

The series needs minimal new marketing spend, so Moutai can extract steady profits and free cash flow—Moutai’s 2024 operating cash flow was ¥53.2bn—supporting premium innovation while Yingbin funds growth elsewhere.

- Entry-level, mass-market

- Stable, low-growth volume

- Brand-driven, price-sensitive demand

- Minimal marketing capex

- Supports group free cash (OCF ¥53.2bn in 2024)

Feitian, Prince, Distributors: 2024 Cash Cows Fuel RMB53B+ OCF with Sky‑High Margins

Feitian Moutai, Moutai Prince, Yingbin and distributor channels are cash cows in 2024: Feitian drove ~RMB130B sales with ~85% gross margin; Prince ~RMB7B (~62% GM); distributor net sales ~RMB22B; Yingbin supports volume with low capex (group OCF RMB53.2B).

| Product | 2024 Sales (RMB) | Gross Margin |

|---|---|---|

| Feitian | 130B | ~85% |

| Prince | 7B | ~62% |

| Distributors | 22B | ~60%+ |

| Yingbin | — | Stable |

What You See Is What You Get

Kweichow Moutai BCG Matrix

The file you're previewing is the final Kweichow Moutai BCG Matrix you'll receive after purchase—no watermarks or demo content, just a polished, analysis-ready report crafted for strategic clarity and professional use.