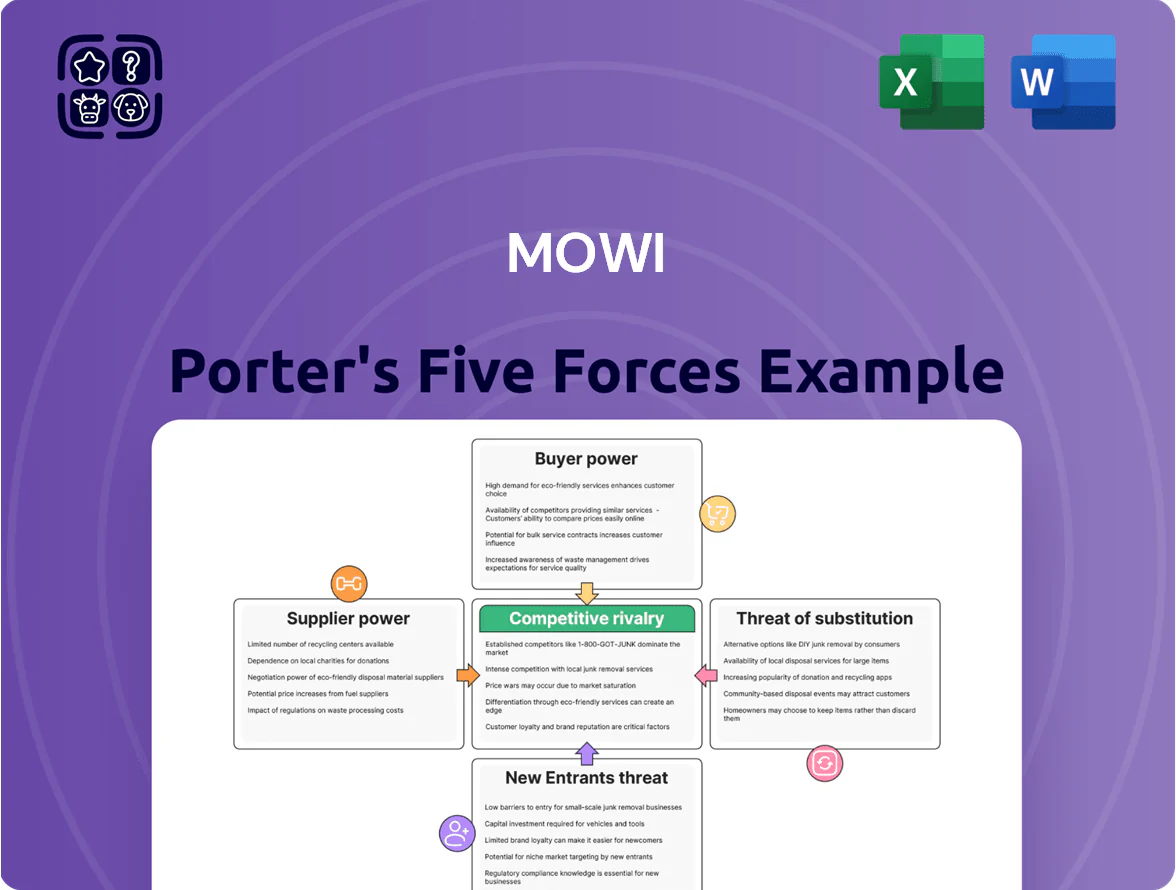

Mowi Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Mowi faces moderate supplier power, intense rivalry among global seafood producers, growing buyer sophistication, manageable threat of new entrants, and rising pressure from substitutes—especially alternative proteins; this snapshot highlights critical tensions shaping margins and growth prospects. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Mowi’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Vertical Integration of Feed Production

Mowi cuts supplier power by running its own feed mills, lowering feed cost exposure that is about 50% of production costs; in 2024 internal feed reduced purchased feed spend by roughly €250m vs peers.

Raw Material Commodity Exposure

Despite Mowi’s internal feed production, it remains exposed to global suppliers of fishmeal, fish oil and soy, which are priced on commodity markets; fishmeal rose ~18% in 2024 and soymeal averaged $420/ton in 2024, forcing price-taking behavior.

Environmental shocks—Peruvian anchovy stocks and 2023-24 South American droughts—pushed volatility: fish oil swung ±25% year-to-year, raising feed input cost variability for Mowi.

Even with processing control, Mowi’s gross margin in 2024 (reported 17.8%) felt pressure from input inflation, showing limited pass-through power over these foundational feed ingredients.

Specialized Equipment and Technology Providers

The aquaculture sector depends on a few specialized suppliers for automated feeding systems and sea‑cage tech, giving suppliers moderate bargaining power due to high technical specs and growing digitalization; global aquaculture tech market was valued at $3.8bn in 2024, up 7% y/y. Mowi’s 2024 revenue of NOK 74.5bn and 1.2m tonnes harvested lets it negotiate volume discounts, long‑term contracts, or co‑develop proprietary systems. Still, supplier concentration raises switching costs and capex lead times of 6–18 months.

Genetics and Biological Assets

Access to high-quality salmon eggs and genetics drives yield and disease resistance, giving specialized genetics firms modest leverage; global elite suppliers control ~30% of elite Atlantic salmon strains as of 2025.

Mowi mitigates this by running in-house breeding and strain development—its genetic program produced a 12% yield gain and 18% lower sea lice susceptibility in trials through 2024.

This internal capability cuts reliance on external broodstock, lowering supply-disruption risk and price exposure.

- In-house breeding → 12% yield gain (2024)

- 18% lower sea lice susceptibility (2024)

- External suppliers hold ~30% elite strain share (2025)

Regulatory and Licensing Constraints

Government bodies act as suppliers of the right to operate via farming licenses; in Norway and Chile limited new licenses raise entry barriers and give the state leverage over expansion.

For Mowi (market cap ~11.2bn USD as of Dec 31, 2025) license constraints shape capacity growth: Norway issued 0–2 new open-pen licenses yearly since 2020; Chile tightened zones in 2023, reducing available sea space by ~12% in key regions.

Regulatory control effectively governs Mowi’s primary input—sea space—forcing strategic permits, fallowing plans, and higher capex per site.

- State issues core input: farming licenses

- Norway: ~0–2 new licenses/yr since 2020

- Chile: 2023 zoning cut ~12% sea space in key regions

- High barriers limit expansion, raise negotiation power of regulators

Mowi cuts €250m feed costs, boosts yield 12% but still exposed to feed price swings

Mowi reduces supplier power via in‑house feed and genetics—internal feed cut purchased spend ~€250m in 2024; breeding gains: +12% yield, −18% sea‑lice susceptibility (2024). Still exposed to commodity feed swings (fishmeal +18% in 2024; soymeal ~$420/ton 2024) and concentrated tech suppliers; licenses (Norway 0–2/yr; Chile −12% sea space 2023) constrain expansion.

| Metric | 2024/2025 |

|---|---|

| Purchased feed saved | ~€250m (2024) |

| Gross margin | 17.8% (2024) |

| Fishmeal price | +18% (2024) |

| Soymeal | $420/ton (2024) |

| Yield gain | +12% (2024) |

| Sea‑lice susceptibility | −18% (2024) |

| Market cap | ~$11.2bn (Dec 31, 2025) |

What is included in the product

Tailored Porter's Five Forces analysis for Mowi, identifying competitive intensity, supplier and buyer power, entry barriers, substitutes, and emerging threats to its market share and profitability.

A concise Porter's Five Forces one-sheet for Mowi—instantly highlights competitive pressures and supplier/customer risks to speed strategic decisions.

Customers Bargaining Power

Retail Consolidation and Volume Demands

Large global retailers like Walmart, Tesco and Carrefour account for a substantial share of market demand; in 2024 Mowi reported 34% of sales to retail channels, leaving those buyers with strong leverage due to volume and scale.

They push strict quality, ASC/MSC sustainability certification and price pressure; typical retail margin targets can compress supplier EBIT by 2–4 percentage points.

Mowi counters with year-round supply stability—2024 harvest volumes of 435,000 tonnes and integrated processing—making it harder for smaller farmers to match consistency and scale.

Brand Differentiation and Consumer Loyalty

Mowi has spent over NOK 1.2 billion on branding and marketing since 2019 to elevate MOWI as a premium salmon label, cutting commodity pricing pressure and boosting direct consumer pull.

Stronger brand equity reduced retailer switch risk; Mowi reported a 7.8% CAGR in value‑brand sales vs 2.1% for private labels in 2021–2024, shifting negotiations toward quality and origin.

Consumers now cite health and provenance first: 61% of surveyed buyers in 2024 chose MOWI for origin/health claims, lowering buyer price sensitivity and intermediary leverage.

Foodservice Sector Fragmentation

The foodservice and restaurant sector is far more fragmented than retail, lowering collective buyer power; in 2024 the top 50 US restaurant chains held only ~35% market share, so no single buyer dominates Mowi’s volumes.

Large distributors like Sysco (2024 revenue $72.6B) matter, but chefs demand varied cuts and value-added products, letting Mowi sell higher-margin specialty SKUs.

Serving casual dining, fine dining, and institutional channels diversifies demand and helped Mowi keep gross margin near 23% in 2024 despite retail price wars.

Switching Costs for Large Scale Buyers

For major processors and distributors, switching from Mowi risks supply gaps because Mowi operates the world’s largest Atlantic salmon network, with 2024 sales of NOK 62.6bn and 1.2m tonnes harvested capacity, creating logistical stickiness.

Mowi’s certified traceability and 2024 ESG metrics—85% of farms ASC-certified and a 22% reduction in CO2 intensity since 2018—align with buyers’ sustainability targets, raising switching friction.

The cost to replace a reliable partner plus integration and audit expenses gives Mowi modest pricing leverage over large-scale customers.

- 2024 sales NOK 62.6bn

- 1.2m t harvest capacity

- 85% ASC-certified farms (2024)

- 22% CO2 intensity cut since 2018

Price Sensitivity in Commodity Markets

- ~28% industry spot volume (2024)

- Mowi fixed‑price contracts ≈60% of sales (2024)

- Value‑added products ≈18% of Mowi revenue

Mowi’s scale and contracts curb buyer power—premium ASC supply boosts margins

Buyers (large retailers, distributors, spot traders) wield strong leverage via volume, quality and price demands, but Mowi’s scale (2024 sales NOK 62.6bn, 1.2m t capacity), 60% fixed‑price contracts, 85% ASC farms and branding reduce switch risk and spot exposure, allowing modest pricing power and higher-margin value‑added sales (~18%).

| Metric | 2024 |

|---|---|

| Sales | NOK 62.6bn |

| Capacity | 1.2m t |

| ASC farms | 85% |

| Fixed contracts | ≈60% |

| Value‑added | ≈18% |

Preview the Actual Deliverable

Mowi Porter's Five Forces Analysis

This preview shows the exact Mowi Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. It’s the fully formatted, final document, ready for download and use the moment you buy. The file contains in-depth evaluation of competitive rivalry, supplier and buyer power, threat of substitution, and barriers to entry tailored to Mowi. No surprises—this is the deliverable.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Mowi faces moderate supplier power, intense rivalry among global seafood producers, growing buyer sophistication, manageable threat of new entrants, and rising pressure from substitutes—especially alternative proteins; this snapshot highlights critical tensions shaping margins and growth prospects. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Mowi’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Vertical Integration of Feed Production

Mowi cuts supplier power by running its own feed mills, lowering feed cost exposure that is about 50% of production costs; in 2024 internal feed reduced purchased feed spend by roughly €250m vs peers.

Raw Material Commodity Exposure

Despite Mowi’s internal feed production, it remains exposed to global suppliers of fishmeal, fish oil and soy, which are priced on commodity markets; fishmeal rose ~18% in 2024 and soymeal averaged $420/ton in 2024, forcing price-taking behavior.

Environmental shocks—Peruvian anchovy stocks and 2023-24 South American droughts—pushed volatility: fish oil swung ±25% year-to-year, raising feed input cost variability for Mowi.

Even with processing control, Mowi’s gross margin in 2024 (reported 17.8%) felt pressure from input inflation, showing limited pass-through power over these foundational feed ingredients.

Specialized Equipment and Technology Providers

The aquaculture sector depends on a few specialized suppliers for automated feeding systems and sea‑cage tech, giving suppliers moderate bargaining power due to high technical specs and growing digitalization; global aquaculture tech market was valued at $3.8bn in 2024, up 7% y/y. Mowi’s 2024 revenue of NOK 74.5bn and 1.2m tonnes harvested lets it negotiate volume discounts, long‑term contracts, or co‑develop proprietary systems. Still, supplier concentration raises switching costs and capex lead times of 6–18 months.

Genetics and Biological Assets

Access to high-quality salmon eggs and genetics drives yield and disease resistance, giving specialized genetics firms modest leverage; global elite suppliers control ~30% of elite Atlantic salmon strains as of 2025.

Mowi mitigates this by running in-house breeding and strain development—its genetic program produced a 12% yield gain and 18% lower sea lice susceptibility in trials through 2024.

This internal capability cuts reliance on external broodstock, lowering supply-disruption risk and price exposure.

- In-house breeding → 12% yield gain (2024)

- 18% lower sea lice susceptibility (2024)

- External suppliers hold ~30% elite strain share (2025)

Regulatory and Licensing Constraints

Government bodies act as suppliers of the right to operate via farming licenses; in Norway and Chile limited new licenses raise entry barriers and give the state leverage over expansion.

For Mowi (market cap ~11.2bn USD as of Dec 31, 2025) license constraints shape capacity growth: Norway issued 0–2 new open-pen licenses yearly since 2020; Chile tightened zones in 2023, reducing available sea space by ~12% in key regions.

Regulatory control effectively governs Mowi’s primary input—sea space—forcing strategic permits, fallowing plans, and higher capex per site.

- State issues core input: farming licenses

- Norway: ~0–2 new licenses/yr since 2020

- Chile: 2023 zoning cut ~12% sea space in key regions

- High barriers limit expansion, raise negotiation power of regulators

Mowi cuts €250m feed costs, boosts yield 12% but still exposed to feed price swings

Mowi reduces supplier power via in‑house feed and genetics—internal feed cut purchased spend ~€250m in 2024; breeding gains: +12% yield, −18% sea‑lice susceptibility (2024). Still exposed to commodity feed swings (fishmeal +18% in 2024; soymeal ~$420/ton 2024) and concentrated tech suppliers; licenses (Norway 0–2/yr; Chile −12% sea space 2023) constrain expansion.

| Metric | 2024/2025 |

|---|---|

| Purchased feed saved | ~€250m (2024) |

| Gross margin | 17.8% (2024) |

| Fishmeal price | +18% (2024) |

| Soymeal | $420/ton (2024) |

| Yield gain | +12% (2024) |

| Sea‑lice susceptibility | −18% (2024) |

| Market cap | ~$11.2bn (Dec 31, 2025) |

What is included in the product

Tailored Porter's Five Forces analysis for Mowi, identifying competitive intensity, supplier and buyer power, entry barriers, substitutes, and emerging threats to its market share and profitability.

A concise Porter's Five Forces one-sheet for Mowi—instantly highlights competitive pressures and supplier/customer risks to speed strategic decisions.

Customers Bargaining Power

Retail Consolidation and Volume Demands

Large global retailers like Walmart, Tesco and Carrefour account for a substantial share of market demand; in 2024 Mowi reported 34% of sales to retail channels, leaving those buyers with strong leverage due to volume and scale.

They push strict quality, ASC/MSC sustainability certification and price pressure; typical retail margin targets can compress supplier EBIT by 2–4 percentage points.

Mowi counters with year-round supply stability—2024 harvest volumes of 435,000 tonnes and integrated processing—making it harder for smaller farmers to match consistency and scale.

Brand Differentiation and Consumer Loyalty

Mowi has spent over NOK 1.2 billion on branding and marketing since 2019 to elevate MOWI as a premium salmon label, cutting commodity pricing pressure and boosting direct consumer pull.

Stronger brand equity reduced retailer switch risk; Mowi reported a 7.8% CAGR in value‑brand sales vs 2.1% for private labels in 2021–2024, shifting negotiations toward quality and origin.

Consumers now cite health and provenance first: 61% of surveyed buyers in 2024 chose MOWI for origin/health claims, lowering buyer price sensitivity and intermediary leverage.

Foodservice Sector Fragmentation

The foodservice and restaurant sector is far more fragmented than retail, lowering collective buyer power; in 2024 the top 50 US restaurant chains held only ~35% market share, so no single buyer dominates Mowi’s volumes.

Large distributors like Sysco (2024 revenue $72.6B) matter, but chefs demand varied cuts and value-added products, letting Mowi sell higher-margin specialty SKUs.

Serving casual dining, fine dining, and institutional channels diversifies demand and helped Mowi keep gross margin near 23% in 2024 despite retail price wars.

Switching Costs for Large Scale Buyers

For major processors and distributors, switching from Mowi risks supply gaps because Mowi operates the world’s largest Atlantic salmon network, with 2024 sales of NOK 62.6bn and 1.2m tonnes harvested capacity, creating logistical stickiness.

Mowi’s certified traceability and 2024 ESG metrics—85% of farms ASC-certified and a 22% reduction in CO2 intensity since 2018—align with buyers’ sustainability targets, raising switching friction.

The cost to replace a reliable partner plus integration and audit expenses gives Mowi modest pricing leverage over large-scale customers.

- 2024 sales NOK 62.6bn

- 1.2m t harvest capacity

- 85% ASC-certified farms (2024)

- 22% CO2 intensity cut since 2018

Price Sensitivity in Commodity Markets

- ~28% industry spot volume (2024)

- Mowi fixed‑price contracts ≈60% of sales (2024)

- Value‑added products ≈18% of Mowi revenue

Mowi’s scale and contracts curb buyer power—premium ASC supply boosts margins

Buyers (large retailers, distributors, spot traders) wield strong leverage via volume, quality and price demands, but Mowi’s scale (2024 sales NOK 62.6bn, 1.2m t capacity), 60% fixed‑price contracts, 85% ASC farms and branding reduce switch risk and spot exposure, allowing modest pricing power and higher-margin value‑added sales (~18%).

| Metric | 2024 |

|---|---|

| Sales | NOK 62.6bn |

| Capacity | 1.2m t |

| ASC farms | 85% |

| Fixed contracts | ≈60% |

| Value‑added | ≈18% |

Preview the Actual Deliverable

Mowi Porter's Five Forces Analysis

This preview shows the exact Mowi Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. It’s the fully formatted, final document, ready for download and use the moment you buy. The file contains in-depth evaluation of competitive rivalry, supplier and buyer power, threat of substitution, and barriers to entry tailored to Mowi. No surprises—this is the deliverable.