MTR Porter's Five Forces Analysis

Don't Miss the Bigger Picture

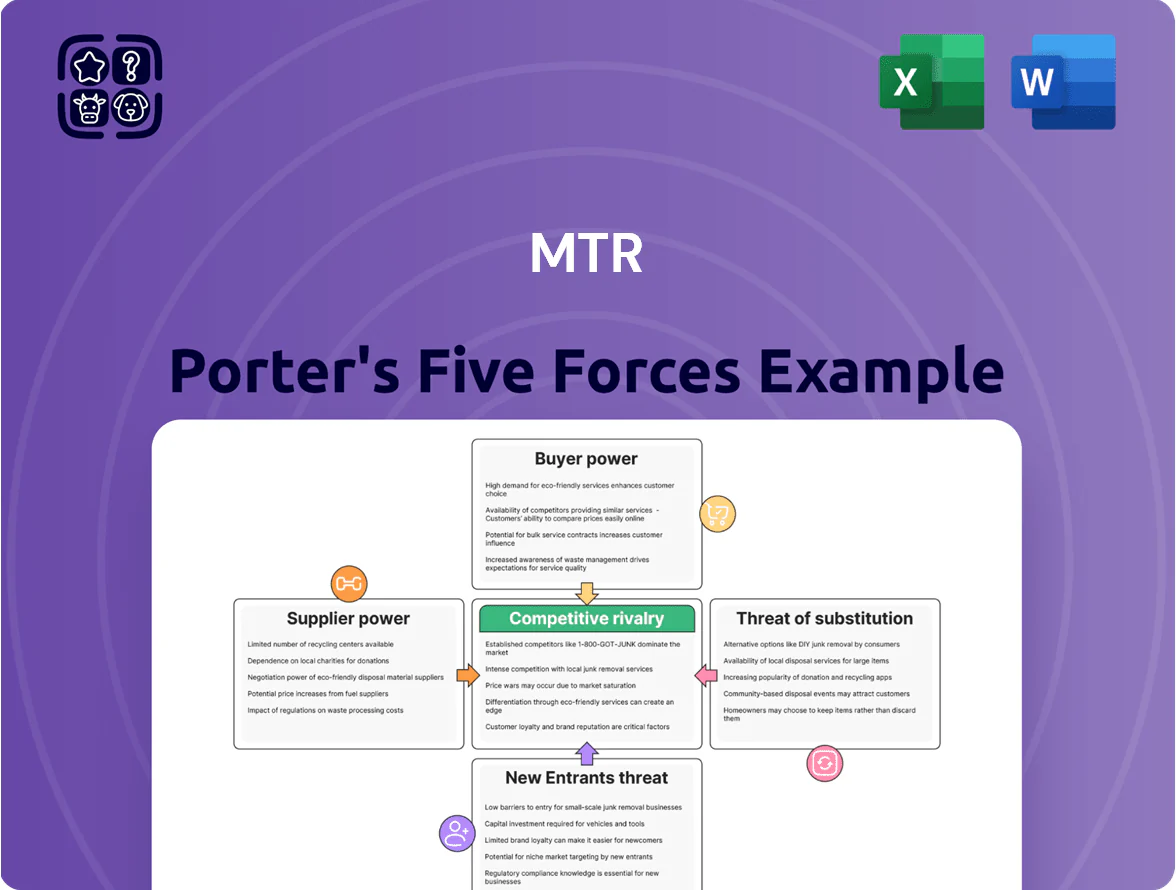

MTR faces complex competitive pressures—from strong buyer expectations and regulatory oversight to substitution risks and concentrated supplier dynamics—impacting margins and growth potential.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore MTR’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Rolling Stock Manufacturers

The market for high-speed trains and metro carriages is concentrated among CRRC, Alstom, and Siemens, which together held roughly 60–70% of global rolling stock supply by 2023; MTR faces high switching costs because equipment must meet stringent safety and signalling standards and ensure technical compatibility, so these suppliers wield strong leverage in 2024–2025 procurement and long-term maintenance talks, often securing premium margins and multi-year spare-part clauses.

Energy Provider Dependency

MTR is one of Hong Kong’s largest electricity users, consuming roughly 1.6 TWh in 2024 and buying mainly from local monopolies CLP Power and HK Electric, which gives suppliers strong leverage. MTR’s large volume gives some bargaining room, but it is effectively a price taker on fuel clause adjustments and exposed to global LNG and coal volatility—Hong Kong import fuel costs rose ~18% in 2023. The 2025 green-energy mandate forces MTR to source certified renewables, narrowing suppliers to certified providers and raising contract premiums.

Specialized Engineering and Construction Services

Major MTR line extensions need specialist civil engineers able to handle projects often exceeding HKD 10–20 billion per contract; globally consolidated firms dominate this segment.

In Hong Kong in 2025, the Construction Industry Council reported a 12% skilled-labor shortfall, leaving fewer than 10 contractors with proven metro-scale delivery capacity.

That scarcity lets contractors charge 8–15% higher premiums and push for greater risk-sharing, shifting cost and schedule risk onto MTR in recent tender outcomes.

Technological and Signaling System Providers

Government Land Supply and Policy

MTR, as a Rail-plus-Property developer, relies on the Hong Kong government for land grants and development rights; the government supplies the core input for MTR’s highest-margin property segment.

Policy moves—land premium adjustments or housing quota changes slated by late 2025—can cut or boost property margin; in 2024 MTR property profit before tax was HKD 12.4bn, so a 10% premium rise could swing ~HKD 1.24bn.

The government thus holds near-absolute supplier power over MTR’s land pipeline, timing, and project scale, constraining MTR’s bargaining on price and pace.

- 2024 property PBT HKD 12.4bn

- 10% land premium change ~HKD 1.24bn impact

- Govt controls land grants, quotas, timing

- Policy shifts by late 2025 are material risk

Suppliers’ clout makes MTR a price-taker: concentrated vendors, long contracts, high premiums

Suppliers exert strong bargaining power: rolling-stock and signalling are concentrated (CRRC, Alstom, Siemens, Thales) with 60–70% market share by 2023; long 10–25y contracts and high switching costs raise premiums (8–15% on construction, 10–25y maintenance margins). Energy suppliers (CLP, HK Electric) and HK government (land grants; 2024 property PBT HKD 12.4bn) further concentrate supplier power, making MTR largely a price taker.

| Item | 2023–2025 |

|---|---|

| Rolling-stock share | 60–70% |

| Contract length | 10–25 yrs |

| Construction premium | +8–15% |

| Property PBT | HKD 12.4bn (2024) |

What is included in the product

Concise Porter’s Five Forces analysis tailored for MTR, uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats that influence pricing, profitability, and strategic positioning.

A clear, one-sheet Porter’s Five Forces summary tailored for MTR—instantly shows competitive pressures and strategic levers for faster, data-driven transit decisions.

Customers Bargaining Power

Individual Commuter Price Sensitivity

Institutional Property Tenants

Large-scale commercial tenants in MTR-owned malls and office towers hold moderate bargaining power: Hong Kong CBD office vacancy hit 8.2% in Q3 2025, giving tenants leverage on rent and fit-out concessions.

Premium retailers now demand guaranteed footfall and tighter property management; MTR reports average mall daily footfall of 220k in 2024, a selling point but not enough alone.

MTR’s locations remain superior, yet decentralised business districts raised suburban office supply by 14% since 2020, offering tenants real alternatives.

Government Transport Authorities in Global Markets

When MTR bids for railway franchises in Europe, Australia or Mainland China, government transport authorities hold immense power, setting strict KPIs, safety standards and financial penalties in tenders; for example, UK and Australian contracts often include up to 10% revenue-at-risk linked to performance. As MTR pushes to diversify revenue from Hong Kong by end-2025, international operations rose to ~18% of group revenue in 2024, forcing acceptance of narrower margins—operating margins on some overseas contracts reported near 3–5% versus 15% in Hong Kong.

Advertising and Retail Licensees

Businesses renting kiosk space or advertising panels in MTR stations face digital disruption: mobile ad spend grew 18% in 2024 to account for 66% of global ad spend, giving advertisers alternatives outside the MTR network.

Consequently, customer bargaining power rises and MTR must offer integrated marketing solutions and location-based analytics; in 2025, data-driven ad pricing and real-time audience metrics will be essential to retain high-value clients.

- Mobile ad share 66% (2024)

- Mobile ad growth +18% (2024)

- Need: location analytics, real-time metrics

- Goal: protect ad revenue vs digital channels

Property Homebuyers

Individual buyers of MTR-linked homes face higher leverage from 2025 interest-rate normalization and weak GDP growth; Hong Kong mortgage approvals fell 12% YoY in 2024, so many buyers negotiate or delay purchases.

Proximity to stations still boosts demand, but MTR and partners must compete on build quality, launch discounts, 0.5–2.0% subsidized mortgage spreads, and lifestyle amenities to close deals.

MTR under pressure: rising rider leverage, tenant bargaining & shifting ad landscape

MTR faces rising customer bargaining power: 5.7M weekday riders (2024) and HKD 6.3bn operating profit (2024) make fare moves politically sensitive; commercial tenants leverage 8.2% CBD vacancy (Q3 2025) and suburban office growth +14% since 2020; ad clients shift as mobile ad share 66% (2024) so MTR needs location analytics; mortgage approvals −12% YoY (2024) boost buyer negotiation.

| Metric | Value |

|---|---|

| Weekday ridership (2024) | 5.7M |

| Operating profit (2024) | HKD 6.3bn |

| CBD vacancy (Q3 2025) | 8.2% |

| Suburban office supply change (2020–25) | +14% |

| Mobile ad share (2024) | 66% |

| Mobile ad growth (2024) | +18% |

| Mortgage approvals YoY (2024) | −12% |

Preview Before You Purchase

MTR Porter's Five Forces Analysis

This preview shows the exact MTR Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples—fully formatted and ready for download and use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

MTR faces complex competitive pressures—from strong buyer expectations and regulatory oversight to substitution risks and concentrated supplier dynamics—impacting margins and growth potential.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore MTR’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Rolling Stock Manufacturers

The market for high-speed trains and metro carriages is concentrated among CRRC, Alstom, and Siemens, which together held roughly 60–70% of global rolling stock supply by 2023; MTR faces high switching costs because equipment must meet stringent safety and signalling standards and ensure technical compatibility, so these suppliers wield strong leverage in 2024–2025 procurement and long-term maintenance talks, often securing premium margins and multi-year spare-part clauses.

Energy Provider Dependency

MTR is one of Hong Kong’s largest electricity users, consuming roughly 1.6 TWh in 2024 and buying mainly from local monopolies CLP Power and HK Electric, which gives suppliers strong leverage. MTR’s large volume gives some bargaining room, but it is effectively a price taker on fuel clause adjustments and exposed to global LNG and coal volatility—Hong Kong import fuel costs rose ~18% in 2023. The 2025 green-energy mandate forces MTR to source certified renewables, narrowing suppliers to certified providers and raising contract premiums.

Specialized Engineering and Construction Services

Major MTR line extensions need specialist civil engineers able to handle projects often exceeding HKD 10–20 billion per contract; globally consolidated firms dominate this segment.

In Hong Kong in 2025, the Construction Industry Council reported a 12% skilled-labor shortfall, leaving fewer than 10 contractors with proven metro-scale delivery capacity.

That scarcity lets contractors charge 8–15% higher premiums and push for greater risk-sharing, shifting cost and schedule risk onto MTR in recent tender outcomes.

Technological and Signaling System Providers

Government Land Supply and Policy

MTR, as a Rail-plus-Property developer, relies on the Hong Kong government for land grants and development rights; the government supplies the core input for MTR’s highest-margin property segment.

Policy moves—land premium adjustments or housing quota changes slated by late 2025—can cut or boost property margin; in 2024 MTR property profit before tax was HKD 12.4bn, so a 10% premium rise could swing ~HKD 1.24bn.

The government thus holds near-absolute supplier power over MTR’s land pipeline, timing, and project scale, constraining MTR’s bargaining on price and pace.

- 2024 property PBT HKD 12.4bn

- 10% land premium change ~HKD 1.24bn impact

- Govt controls land grants, quotas, timing

- Policy shifts by late 2025 are material risk

Suppliers’ clout makes MTR a price-taker: concentrated vendors, long contracts, high premiums

Suppliers exert strong bargaining power: rolling-stock and signalling are concentrated (CRRC, Alstom, Siemens, Thales) with 60–70% market share by 2023; long 10–25y contracts and high switching costs raise premiums (8–15% on construction, 10–25y maintenance margins). Energy suppliers (CLP, HK Electric) and HK government (land grants; 2024 property PBT HKD 12.4bn) further concentrate supplier power, making MTR largely a price taker.

| Item | 2023–2025 |

|---|---|

| Rolling-stock share | 60–70% |

| Contract length | 10–25 yrs |

| Construction premium | +8–15% |

| Property PBT | HKD 12.4bn (2024) |

What is included in the product

Concise Porter’s Five Forces analysis tailored for MTR, uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats that influence pricing, profitability, and strategic positioning.

A clear, one-sheet Porter’s Five Forces summary tailored for MTR—instantly shows competitive pressures and strategic levers for faster, data-driven transit decisions.

Customers Bargaining Power

Individual Commuter Price Sensitivity

Institutional Property Tenants

Large-scale commercial tenants in MTR-owned malls and office towers hold moderate bargaining power: Hong Kong CBD office vacancy hit 8.2% in Q3 2025, giving tenants leverage on rent and fit-out concessions.

Premium retailers now demand guaranteed footfall and tighter property management; MTR reports average mall daily footfall of 220k in 2024, a selling point but not enough alone.

MTR’s locations remain superior, yet decentralised business districts raised suburban office supply by 14% since 2020, offering tenants real alternatives.

Government Transport Authorities in Global Markets

When MTR bids for railway franchises in Europe, Australia or Mainland China, government transport authorities hold immense power, setting strict KPIs, safety standards and financial penalties in tenders; for example, UK and Australian contracts often include up to 10% revenue-at-risk linked to performance. As MTR pushes to diversify revenue from Hong Kong by end-2025, international operations rose to ~18% of group revenue in 2024, forcing acceptance of narrower margins—operating margins on some overseas contracts reported near 3–5% versus 15% in Hong Kong.

Advertising and Retail Licensees

Businesses renting kiosk space or advertising panels in MTR stations face digital disruption: mobile ad spend grew 18% in 2024 to account for 66% of global ad spend, giving advertisers alternatives outside the MTR network.

Consequently, customer bargaining power rises and MTR must offer integrated marketing solutions and location-based analytics; in 2025, data-driven ad pricing and real-time audience metrics will be essential to retain high-value clients.

- Mobile ad share 66% (2024)

- Mobile ad growth +18% (2024)

- Need: location analytics, real-time metrics

- Goal: protect ad revenue vs digital channels

Property Homebuyers

Individual buyers of MTR-linked homes face higher leverage from 2025 interest-rate normalization and weak GDP growth; Hong Kong mortgage approvals fell 12% YoY in 2024, so many buyers negotiate or delay purchases.

Proximity to stations still boosts demand, but MTR and partners must compete on build quality, launch discounts, 0.5–2.0% subsidized mortgage spreads, and lifestyle amenities to close deals.

MTR under pressure: rising rider leverage, tenant bargaining & shifting ad landscape

MTR faces rising customer bargaining power: 5.7M weekday riders (2024) and HKD 6.3bn operating profit (2024) make fare moves politically sensitive; commercial tenants leverage 8.2% CBD vacancy (Q3 2025) and suburban office growth +14% since 2020; ad clients shift as mobile ad share 66% (2024) so MTR needs location analytics; mortgage approvals −12% YoY (2024) boost buyer negotiation.

| Metric | Value |

|---|---|

| Weekday ridership (2024) | 5.7M |

| Operating profit (2024) | HKD 6.3bn |

| CBD vacancy (Q3 2025) | 8.2% |

| Suburban office supply change (2020–25) | +14% |

| Mobile ad share (2024) | 66% |

| Mobile ad growth (2024) | +18% |

| Mortgage approvals YoY (2024) | −12% |

Preview Before You Purchase

MTR Porter's Five Forces Analysis

This preview shows the exact MTR Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples—fully formatted and ready for download and use.