MTR PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

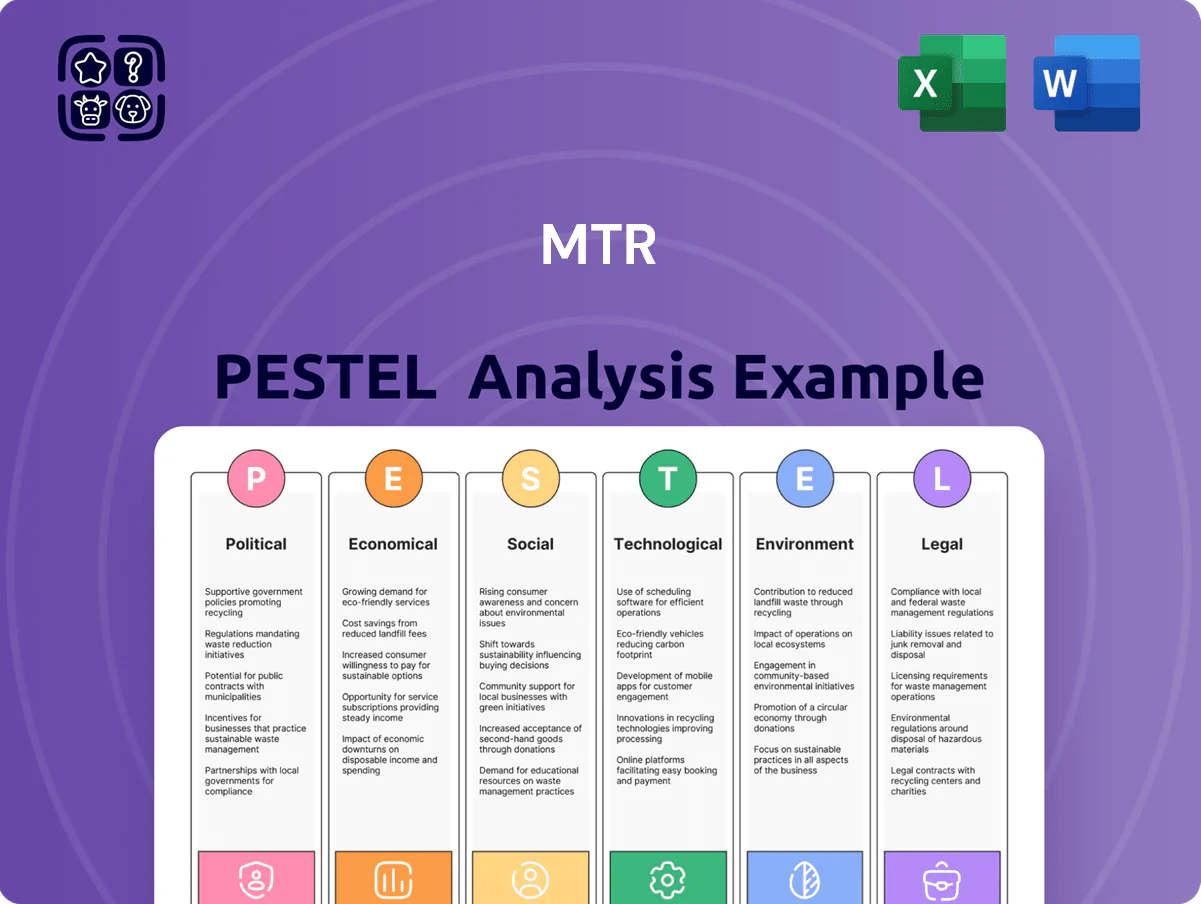

Discover how political, economic, social, technological, legal, and environmental forces are shaping MTR’s strategy and operations—our concise PESTLE snapshot highlights key external risks and opportunities. Ideal for investors, consultants, and strategists, the full PESTLE provides detailed evidence, implications, and actionable recommendations. Purchase now to download the complete, ready-to-use analysis and make smarter decisions fast.

Political factors

Government Shareholding and Public Policy

The Hong Kong Government holds a 75.01% effective interest in MTR Corporation, aligning corporate strategy with city urban development and enabling priority access to land grants that contributed HKD 2.6 billion in property-related income in FY2024; however, state ownership creates political pressure on fare adjustments and service standards, while decisions on new extensions—such as the 2023 approval for the Northern Link—reflect planning priorities over short-term commercial returns.

Greater Bay Area Integration

MTR is central to Greater Bay Area integration, operating cross-boundary rail like the Guangzhou–Shenzhen–Hong Kong Express Rail Link and participating in regional projects that carried over 1.2 billion journeys in Guangdong-Hong Kong-Macao corridors in 2024, boosting demand for high-speed and inter-city services. Strong political backing for seamless travel under national strategies (14th Five-Year Plan/GBA initiatives) supports MTR’s mainland expansion, targeting revenue growth from China operations which contributed HKD 18.3 billion in 2024, with further opportunities through 2026.

Geopolitical Risks in Overseas Markets

The corporation’s operations across Europe, Australia and mainland China face exposure to geopolitical shifts and local political instability, with 2024 franchise renewals and consultancy bids in Hong Kong and the UK potentially affecting revenue streams (international segment contributed ~28% of HK$56.5bn 2023 revenue). Political tensions can delay contracts or franchise extensions, risking service disruptions and capex schedules; MTR must preserve neutrality and professional credibility to protect tender success rates and franchise renewal prospects.

Land Supply and Housing Mandates

The Hong Kong government’s land policy shapes MTR’s Rail-plus-Property model by controlling site availability and timing; in 2024 MTR secured 5 major sites yielding an estimated HKD 28bn GDV, illustrating policy impact on project pipelines.

Mandates to boost public housing—targeting 82,000 flats in 2023–24—can limit high-end private development, pressuring margins as private GDV per unit often exceeds public by 30–50%.

Executive leadership must balance social housing obligations with shareholder returns, where property profit contributed ~40% of MTR’s FY2024 operating profit, making allocation decisions politically sensitive.

- Government land timings directly affect project cashflows and GDV (e.g., HKD 28bn from 2024 sites)

- Public housing mandates (82,000 flats 2023–24) reduce private development scope

- Property profits ~40% of FY2024 operating profit—tension between social duty and shareholder returns

Public Scrutiny and Legislative Oversight

MTR faces intense Legislative Council scrutiny over operations and new projects; in 2024 the Council probed delays in the Shatin to Central Link after a HK$19.6 billion budget overspend and schedule slippage, heightening calls for executive accountability.

Any further delays or cost overruns trigger political backlash and potential hearings—MTR reported a 3.8% FY2024 decline in Hong Kong ridership revenues, increasing pressure for transparent project stewardship.

- MTR must maintain high transparency with LegCo and public amid budget overruns (HK$19.6bn cited) and ridership revenue drops (3.8% FY2024).

State-backed MTR: Property-driven profits, mainland growth, and geopolitical revenue risk

State ownership (75.01%) aligns MTR with HK urban policy and land grants (HKD 2.6bn property income FY2024) but constrains fare moves; Greater Bay Area and national plans supported mainland revenue HKD 18.3bn (2024); international exposure (~28% of HK$56.5bn 2023 revenue) risks geopolitical impacts; property profit ~40% of FY2024 operating profit, with HKD 28bn GDV from five 2024 sites.

| Metric | Value |

|---|---|

| Govt stake | 75.01% |

| Property income FY2024 | HKD 2.6bn |

| Mainland revenue 2024 | HKD 18.3bn |

| International share (2023) | ~28% |

| Property profit share FY2024 | ~40% |

| GDV from 2024 sites | HKD 28bn |

What is included in the product

Explores how macro-environmental forces uniquely affect MTR across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities.

Condenses MTR's full PESTLE into a clean, shareable summary—visually segmented by category and written in plain language—so teams can quickly align on external risks, regulatory impacts, and strategic implications during meetings or presentations.

Economic factors

Property Market Volatility

MTR depends on property profits for ~20-30% of recurring income; late 2025 HK residential prices fell about 5-8% year-on-year, tightening cash flow timing and reducing expected land-tender proceeds. A cooling market has already delayed several joint-venture launches and could compress developer bid prices by an estimated 10-15%, forcing MTR to defer projects or seek alternative financing.

Interest Rate Environment

The 2025 global rate tightening raised Hong Kong interbank HIBOR to around 1.8%–2.2% (5y average 2024–25), increasing MTR’s borrowing costs for capital projects and elevating interest expense on HKD-denominated debt; higher mortgage rates cut buyer affordability, with Hong Kong mortgage approvals down ~12% YoY in 2024.

Recovery of Tourism and Cross-Boundary Travel

The economic health of MTR is closely tied to tourist and cross-boundary commuter volumes; by end-2025 international and mainland visitor arrivals returned to about 98% of 2019 levels, driving a sharp rebound in station retail and advertising income. Non-fare revenue rose c.28% year-on-year in 2025, lifting total non-fare contribution to roughly 22% of MTR Group revenue. Recovery has been crucial to sustain profitability on high-margin airport and boundary links, where ridership recovered to c.90–105% of pre-pandemic levels by late 2025.

Inflationary Pressures on Operational Costs

Rising labor, electricity and materials costs have squeezed MTR’s margins; Hong Kong CPI rose 3.9% in 2024 and global steel and electricity prices increased ~15–25% YoY, pushing 2024 operating expenses higher across its network.

MTR must enforce tight cost controls and productivity gains—targeting efficiency improvements and capex reprioritisation—to offset input-price inflation eroding farebox and rental income.

Sustained inflation complicates fare renegotiations, as real-wage pressures and 2024 household cost-of-living concerns constrain public acceptance of fare rises.

- 2024 HK CPI +3.9%; energy/materials +15–25% YoY

- Focus: cost-control, productivity, capex reprioritisation

- Fare increases politically sensitive amid real-wage pressure

Diversification of Revenue Streams

To reduce Hong Kong market risk, MTR has expanded international operations—managing rail franchises and consultancy in the UK, Sweden, Australia and Mainland China—generating about HKD 9–11 billion of non-HK revenue in FY2024–25, diversifying income away from property cycles.

These overseas contracts lower concentration risk but typically yield slimmer operating margins (often mid-single digits vs. double-digit margins from Hong Kong's integrated property-plus-rail model), pressuring group-wide ROE.

- Non-HK revenue ~HKD 9–11bn (FY2024–25)

- Overseas margins mid-single digits vs Hong Kong double-digit margins

- Diversification lowers property-cycle dependence

MTR margins squeezed as rising costs and weaker property profits force capex reprioritisation

MTR faces squeezed margins from 2024 HK CPI +3.9% and input costs +15–25% YoY; property profits (20–30% of recurring income) weakened as 2025 HK home prices fell ~5–8% YoY, delaying JV launches and compressing bids ~10–15%. Non-fare recovery lifted revenue, with non-HK revenue ~HKD 9–11bn (FY2024–25) but lower margins (mid-single vs HK double-digit), forcing capex reprioritisation.

| Metric | 2024–25 |

|---|---|

| HK CPI | +3.9% |

| Input costs | +15–25% YoY |

| Property income | 20–30% recurring |

| HK home prices | -5–8% YoY (late 2025) |

| Non-HK rev | HKD 9–11bn |

Full Version Awaits

MTR PESTLE Analysis

The preview shown here is the exact MTR PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and analysis visible in this preview are the same file you’ll download instantly after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political, economic, social, technological, legal, and environmental forces are shaping MTR’s strategy and operations—our concise PESTLE snapshot highlights key external risks and opportunities. Ideal for investors, consultants, and strategists, the full PESTLE provides detailed evidence, implications, and actionable recommendations. Purchase now to download the complete, ready-to-use analysis and make smarter decisions fast.

Political factors

Government Shareholding and Public Policy

The Hong Kong Government holds a 75.01% effective interest in MTR Corporation, aligning corporate strategy with city urban development and enabling priority access to land grants that contributed HKD 2.6 billion in property-related income in FY2024; however, state ownership creates political pressure on fare adjustments and service standards, while decisions on new extensions—such as the 2023 approval for the Northern Link—reflect planning priorities over short-term commercial returns.

Greater Bay Area Integration

MTR is central to Greater Bay Area integration, operating cross-boundary rail like the Guangzhou–Shenzhen–Hong Kong Express Rail Link and participating in regional projects that carried over 1.2 billion journeys in Guangdong-Hong Kong-Macao corridors in 2024, boosting demand for high-speed and inter-city services. Strong political backing for seamless travel under national strategies (14th Five-Year Plan/GBA initiatives) supports MTR’s mainland expansion, targeting revenue growth from China operations which contributed HKD 18.3 billion in 2024, with further opportunities through 2026.

Geopolitical Risks in Overseas Markets

The corporation’s operations across Europe, Australia and mainland China face exposure to geopolitical shifts and local political instability, with 2024 franchise renewals and consultancy bids in Hong Kong and the UK potentially affecting revenue streams (international segment contributed ~28% of HK$56.5bn 2023 revenue). Political tensions can delay contracts or franchise extensions, risking service disruptions and capex schedules; MTR must preserve neutrality and professional credibility to protect tender success rates and franchise renewal prospects.

Land Supply and Housing Mandates

The Hong Kong government’s land policy shapes MTR’s Rail-plus-Property model by controlling site availability and timing; in 2024 MTR secured 5 major sites yielding an estimated HKD 28bn GDV, illustrating policy impact on project pipelines.

Mandates to boost public housing—targeting 82,000 flats in 2023–24—can limit high-end private development, pressuring margins as private GDV per unit often exceeds public by 30–50%.

Executive leadership must balance social housing obligations with shareholder returns, where property profit contributed ~40% of MTR’s FY2024 operating profit, making allocation decisions politically sensitive.

- Government land timings directly affect project cashflows and GDV (e.g., HKD 28bn from 2024 sites)

- Public housing mandates (82,000 flats 2023–24) reduce private development scope

- Property profits ~40% of FY2024 operating profit—tension between social duty and shareholder returns

Public Scrutiny and Legislative Oversight

MTR faces intense Legislative Council scrutiny over operations and new projects; in 2024 the Council probed delays in the Shatin to Central Link after a HK$19.6 billion budget overspend and schedule slippage, heightening calls for executive accountability.

Any further delays or cost overruns trigger political backlash and potential hearings—MTR reported a 3.8% FY2024 decline in Hong Kong ridership revenues, increasing pressure for transparent project stewardship.

- MTR must maintain high transparency with LegCo and public amid budget overruns (HK$19.6bn cited) and ridership revenue drops (3.8% FY2024).

State-backed MTR: Property-driven profits, mainland growth, and geopolitical revenue risk

State ownership (75.01%) aligns MTR with HK urban policy and land grants (HKD 2.6bn property income FY2024) but constrains fare moves; Greater Bay Area and national plans supported mainland revenue HKD 18.3bn (2024); international exposure (~28% of HK$56.5bn 2023 revenue) risks geopolitical impacts; property profit ~40% of FY2024 operating profit, with HKD 28bn GDV from five 2024 sites.

| Metric | Value |

|---|---|

| Govt stake | 75.01% |

| Property income FY2024 | HKD 2.6bn |

| Mainland revenue 2024 | HKD 18.3bn |

| International share (2023) | ~28% |

| Property profit share FY2024 | ~40% |

| GDV from 2024 sites | HKD 28bn |

What is included in the product

Explores how macro-environmental forces uniquely affect MTR across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities.

Condenses MTR's full PESTLE into a clean, shareable summary—visually segmented by category and written in plain language—so teams can quickly align on external risks, regulatory impacts, and strategic implications during meetings or presentations.

Economic factors

Property Market Volatility

MTR depends on property profits for ~20-30% of recurring income; late 2025 HK residential prices fell about 5-8% year-on-year, tightening cash flow timing and reducing expected land-tender proceeds. A cooling market has already delayed several joint-venture launches and could compress developer bid prices by an estimated 10-15%, forcing MTR to defer projects or seek alternative financing.

Interest Rate Environment

The 2025 global rate tightening raised Hong Kong interbank HIBOR to around 1.8%–2.2% (5y average 2024–25), increasing MTR’s borrowing costs for capital projects and elevating interest expense on HKD-denominated debt; higher mortgage rates cut buyer affordability, with Hong Kong mortgage approvals down ~12% YoY in 2024.

Recovery of Tourism and Cross-Boundary Travel

The economic health of MTR is closely tied to tourist and cross-boundary commuter volumes; by end-2025 international and mainland visitor arrivals returned to about 98% of 2019 levels, driving a sharp rebound in station retail and advertising income. Non-fare revenue rose c.28% year-on-year in 2025, lifting total non-fare contribution to roughly 22% of MTR Group revenue. Recovery has been crucial to sustain profitability on high-margin airport and boundary links, where ridership recovered to c.90–105% of pre-pandemic levels by late 2025.

Inflationary Pressures on Operational Costs

Rising labor, electricity and materials costs have squeezed MTR’s margins; Hong Kong CPI rose 3.9% in 2024 and global steel and electricity prices increased ~15–25% YoY, pushing 2024 operating expenses higher across its network.

MTR must enforce tight cost controls and productivity gains—targeting efficiency improvements and capex reprioritisation—to offset input-price inflation eroding farebox and rental income.

Sustained inflation complicates fare renegotiations, as real-wage pressures and 2024 household cost-of-living concerns constrain public acceptance of fare rises.

- 2024 HK CPI +3.9%; energy/materials +15–25% YoY

- Focus: cost-control, productivity, capex reprioritisation

- Fare increases politically sensitive amid real-wage pressure

Diversification of Revenue Streams

To reduce Hong Kong market risk, MTR has expanded international operations—managing rail franchises and consultancy in the UK, Sweden, Australia and Mainland China—generating about HKD 9–11 billion of non-HK revenue in FY2024–25, diversifying income away from property cycles.

These overseas contracts lower concentration risk but typically yield slimmer operating margins (often mid-single digits vs. double-digit margins from Hong Kong's integrated property-plus-rail model), pressuring group-wide ROE.

- Non-HK revenue ~HKD 9–11bn (FY2024–25)

- Overseas margins mid-single digits vs Hong Kong double-digit margins

- Diversification lowers property-cycle dependence

MTR margins squeezed as rising costs and weaker property profits force capex reprioritisation

MTR faces squeezed margins from 2024 HK CPI +3.9% and input costs +15–25% YoY; property profits (20–30% of recurring income) weakened as 2025 HK home prices fell ~5–8% YoY, delaying JV launches and compressing bids ~10–15%. Non-fare recovery lifted revenue, with non-HK revenue ~HKD 9–11bn (FY2024–25) but lower margins (mid-single vs HK double-digit), forcing capex reprioritisation.

| Metric | 2024–25 |

|---|---|

| HK CPI | +3.9% |

| Input costs | +15–25% YoY |

| Property income | 20–30% recurring |

| HK home prices | -5–8% YoY (late 2025) |

| Non-HK rev | HKD 9–11bn |

Full Version Awaits

MTR PESTLE Analysis

The preview shown here is the exact MTR PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and analysis visible in this preview are the same file you’ll download instantly after payment.