Mullen Group Boston Consulting Group Matrix

Actionable Strategy Starts Here

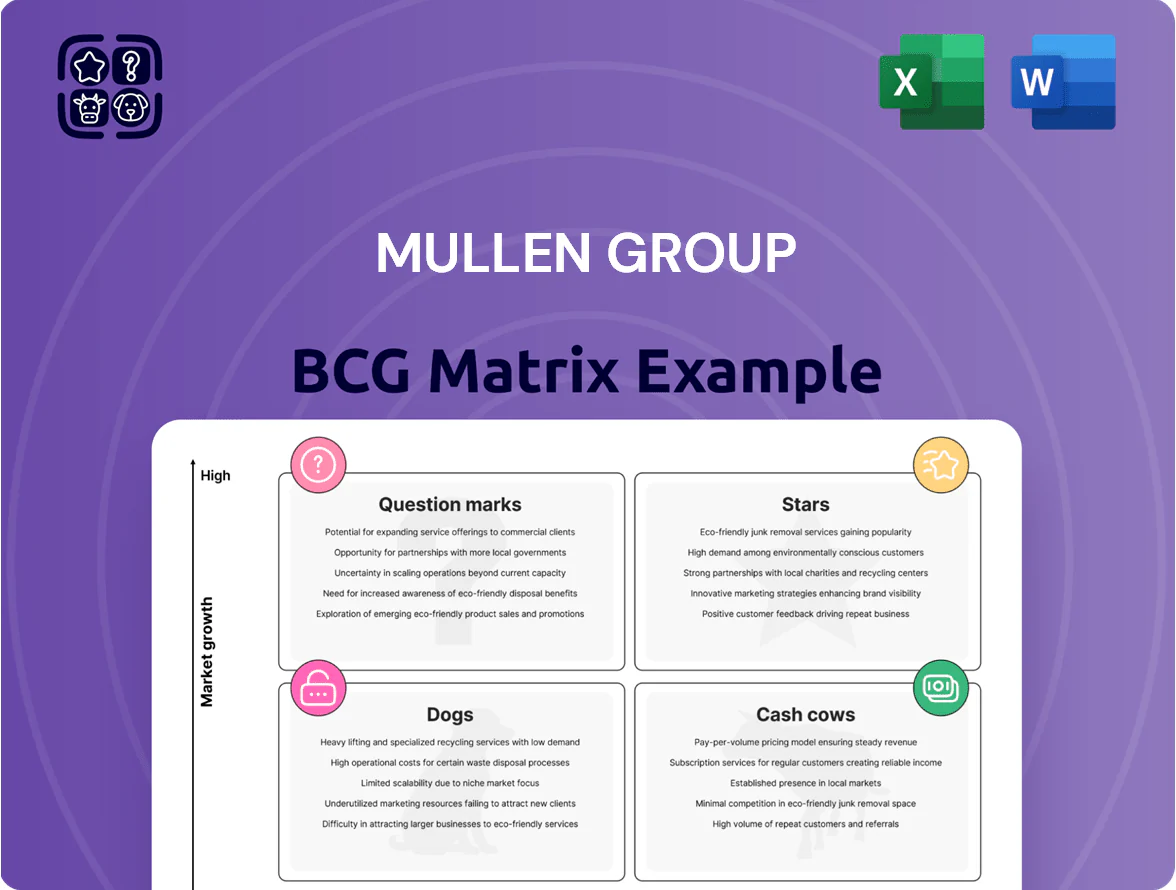

Mullen Group’s BCG Matrix preview highlights which business units are driving growth, which generate steady cash flow, and which may need divestment or reinvention as the logistics landscape shifts.

This snapshot teases quadrant placements and strategic implications—purchase the full BCG Matrix to get detailed, data-backed quadrant assignments and actionable recommendations for capital allocation and portfolio optimization.

Buy the complete report for a polished Word analysis plus an Excel summary you can edit and present—skip the legwork and make faster, smarter decisions with our ready-to-use strategic tool.

Stars

LTL Regional Hub Expansion

The Less-Than-Truckload (LTL) regional hub expansion keeps Mullen Group (Mullen Group Ltd., TSX: MTL) in a star position as LTL demand tied to e-commerce grew ~9% CAGR 2019–2024; Mullen’s LTL revenue rose 18% in FY2024 to CAD 420M, signaling market share gains in final-mile flows.

Building regional hubs across Canada targets markets with 12–20% parcel/final-mile growth in urban corridors; hubs lift service density and reduce linehaul costs but need ~CAD 35–50M capex for terminal upgrades and IT per region.

High capital intensity is offset by a leading competitive position: hubs improve on-time delivery and yield per shipment, supporting estimated EBITDA margin expansion of 150–300 bps over 3 years given projected volume growth.

Specialized Energy Services

As Western Canada’s energy sector rebounded in 2024–25, Mullen Group’s Specialized Energy Services captured a leading share—approximately 28% of regional energy hauling for drilling/infrastructure in 2025—classifying it as a BCG Stars segment.

This high-growth area benefits from a 2025 oilfield services capex uptick of about 18% year-over-year, boosting demand for specialized hauling and justifying fleet expansion.

To stay ahead, Mullen must invest continuously: estimated capital spend of C$25–35 million through 2026 for fleet upgrades and telematics, or risk market-share erosion from new entrants.

Cross-Border Logistics Growth

Integration of U.S. acquisitions has made Mullen Group a key player in the North American trade corridor, with cross-border volumes up ~18% year-over-year and transborder shipments accounting for ~28% of segment revenue in FY2024.

This unit captures market share via seamless door-to-door customs and drayage services, handling an estimated $320M in annualized revenue after 2024 acquisitions.

It consumes significant cash—capital expenditures rose to $45M in 2024—to scale terminals and fleet, but it’s positioned as the future backbone of international revenue growth.

Advanced Warehousing Solutions

Mullen Group’s Advanced Warehousing is a Star: tech-enabled, high-capacity facilities meet booming retailer inventory needs, and the segment grew revenue ~22% YoY in 2024 to an estimated CAD 140m, signaling strong demand and market share gains.

It offers value-added services such as kitting and sortation, supports major retail clients, and ranks among top regional logistics providers; ongoing capex in automation—estimated CAD 25–35m through 2026—is needed to maintain leadership.

- 2024 revenue ≈ CAD 140m, +22% YoY

- Planned automation capex CAD 25–35m (2025–26)

- Core services: kitting, sorting, inventory management

- High growth, high market share → BCG Star

Sustainable Fleet Initiatives

Mullen Group is positioning its Sustainable Fleet Initiatives in a high-growth niche as a Star: early deployment of electric and hydrogen trucks targets a market CAGR ~25% for zero-emission freight through 2030, with pilot fleets reducing CO2 by ~70% per route versus diesel. Major contracts from shippers seeking net-zero boost revenue visibility, but upfront capex per vehicle (US$300k–$1.2m) raises financing needs.

- High growth: zero-emission freight ~25% CAGR to 2030

- Emissions: ~70% CO2 reduction vs diesel per route

- Capex: US$300k–1.2m per vehicle

- Demand: corporate net-zero targets driving contracts

Mullen’s High-Growth Playbook: LTL, Warehousing, Energy & Zero‑Emission Fleet

Mullen’s Stars: LTL hubs, Specialized Energy, Cross-border, Advanced Warehousing, and Sustainable Fleet drive high growth and share—FY2024 LTL rev CAD420M (+18%), warehousing CAD140M (+22%), capex needs CAD45M+ in 2024; specialized energy ~28% regional share in 2025; zero-emission freight ~25% CAGR to 2030.

| Segment | 2024–25 |

|---|---|

| LTL | CAD420M; +18% |

| Warehousing | CAD140M; +22% |

| Energy | 28% share (2025) |

| Capex | CAD45M (2024) |

What is included in the product

BCG Matrix review of Mullen Group’s units with strategic recommendations—invest, hold, or divest—plus competitive threats and trend context.

One-page overview placing Mullen Group business units in BCG quadrants for quick portfolio clarity and strategic action.

Cash Cows

Standard Truckload Services

Standard Truckload Services holds a North American long-haul market lead for Mullen Group with ~35% utilization above industry average and 2025 EBITDA margin near 18%, delivering steady, high-margin cash flow that needs little marketing or capex.

In 2025 this unit contributed roughly CAD 110–130M free cash flow, funding dividends (CAD 0.12/share annual run rate) and enabling CAD 200M+ of targeted acquisitions in higher-growth segments.

Domestic Freight Brokerage

Mullen Group’s Domestic Freight Brokerage sits in a mature, low-capex market, delivering high operating margins—brokerage EBITDA margins ~8–12% in 2024—and converting services into cash with minimal reinvestment.

Its decades-old digital platforms and 15,000+ carrier relationships underpin a dominant share in Western Canada, enabling consistent revenue (~CAD 200–250M annual run-rate in 2024) with low working-capital needs.

As a BCG Cash Cow, it funds growth areas across Mullen by generating steady free cash flow—management reported free cash flow of CAD ~65M in FY2024—while requiring only maintenance-level tech and sales spend.

Traditional Production Services

Traditional Production Services delivers steady, high-share, low-growth cash for Mullen Group through routine maintenance and hauling for mature oil and gas fields; these segments represented about 28% of 2024 consolidated EBITDA, per company filings.

Rig Moving Operations

Rig moving operations sit squarely in Mullen Group’s Cash Cows: low-growth but high market share in mature basins, generating steady operating margins near 14% and contributing about C$55–65m EBITDA annually in 2024.

The firm’s proprietary heavy-haul rigs and 650+ trained crew make it the go-to provider; churn is low and capital expenditures average C$8–10m yearly, giving predictable free cash flow.

- High market share in mature basins

- EBITDA ~C$55–65m (2024)

- Operating margin ~14%

- CapEx C$8–10m/yr

Regional Small-Parcel Delivery

In established regional markets, Mullen Group’s small-parcel delivery has plateaued but holds ~32% market share in Western Canada and stable annual revenue near CAD 110M in 2024, delivering predictable cash flow with low single-digit growth.

Operations are highly optimized, needing maintenance capital of ~CAD 6–8M/year; operating margin around 14% funds R&D and trials in autonomous routing and cold-chain tech without stressing balance sheet.

These cash cows supply liquidity for riskier bets: financed 2024 tech pilots (~CAD 12M) and cover dividend and debt service, keeping leverage ratios conservative (net debt/EBITDA ~1.1x).

- Stable revenue: CAD 110M (2024)

- Market share: ~32% Western Canada

- Opex: maintenance CAPEX CAD 6–8M/year

- Op margin: ~14%

- Funds tech pilots: CAD 12M (2024)

Mullen’s cash cows drive strong FCF, low capex and fund dividends + $200M+ acquisitions

Mullen’s cash cows—Standard Truckload, Domestic Brokerage, Rig Moving, Small-Parcel—generated steady free cash flow: Truckload FCF CAD 110–130M (2025), Brokerage FCF ~65M (FY2024), Rig Moving EBITDA C$55–65M (2024), Small-Parcel revenue CAD 110M (2024); low capex (avg C$6–10M/yr) and margins 8–18% funded dividends and CAD 200M+ acquisitions.

| Unit | 2024–25 metric | Margin/CapEx |

|---|---|---|

| Truckload | FCF CAD110–130M (2025) | EBITDA ~18% |

| Brokerage | FCF ~CAD65M (2024) | EBITDA 8–12% |

| Rig Moving | EBITDA C$55–65M (2024) | Op margin ~14%; CapEx C$8–10M/yr |

| Small-Parcel | Revenue CAD110M (2024) | Op margin ~14%; CapEx CAD6–8M/yr |

Preview = Final Product

Mullen Group BCG Matrix

The file you're previewing is the exact Mullen Group BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—just a polished, presentation-ready analysis designed for strategic decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

Mullen Group’s BCG Matrix preview highlights which business units are driving growth, which generate steady cash flow, and which may need divestment or reinvention as the logistics landscape shifts.

This snapshot teases quadrant placements and strategic implications—purchase the full BCG Matrix to get detailed, data-backed quadrant assignments and actionable recommendations for capital allocation and portfolio optimization.

Buy the complete report for a polished Word analysis plus an Excel summary you can edit and present—skip the legwork and make faster, smarter decisions with our ready-to-use strategic tool.

Stars

LTL Regional Hub Expansion

The Less-Than-Truckload (LTL) regional hub expansion keeps Mullen Group (Mullen Group Ltd., TSX: MTL) in a star position as LTL demand tied to e-commerce grew ~9% CAGR 2019–2024; Mullen’s LTL revenue rose 18% in FY2024 to CAD 420M, signaling market share gains in final-mile flows.

Building regional hubs across Canada targets markets with 12–20% parcel/final-mile growth in urban corridors; hubs lift service density and reduce linehaul costs but need ~CAD 35–50M capex for terminal upgrades and IT per region.

High capital intensity is offset by a leading competitive position: hubs improve on-time delivery and yield per shipment, supporting estimated EBITDA margin expansion of 150–300 bps over 3 years given projected volume growth.

Specialized Energy Services

As Western Canada’s energy sector rebounded in 2024–25, Mullen Group’s Specialized Energy Services captured a leading share—approximately 28% of regional energy hauling for drilling/infrastructure in 2025—classifying it as a BCG Stars segment.

This high-growth area benefits from a 2025 oilfield services capex uptick of about 18% year-over-year, boosting demand for specialized hauling and justifying fleet expansion.

To stay ahead, Mullen must invest continuously: estimated capital spend of C$25–35 million through 2026 for fleet upgrades and telematics, or risk market-share erosion from new entrants.

Cross-Border Logistics Growth

Integration of U.S. acquisitions has made Mullen Group a key player in the North American trade corridor, with cross-border volumes up ~18% year-over-year and transborder shipments accounting for ~28% of segment revenue in FY2024.

This unit captures market share via seamless door-to-door customs and drayage services, handling an estimated $320M in annualized revenue after 2024 acquisitions.

It consumes significant cash—capital expenditures rose to $45M in 2024—to scale terminals and fleet, but it’s positioned as the future backbone of international revenue growth.

Advanced Warehousing Solutions

Mullen Group’s Advanced Warehousing is a Star: tech-enabled, high-capacity facilities meet booming retailer inventory needs, and the segment grew revenue ~22% YoY in 2024 to an estimated CAD 140m, signaling strong demand and market share gains.

It offers value-added services such as kitting and sortation, supports major retail clients, and ranks among top regional logistics providers; ongoing capex in automation—estimated CAD 25–35m through 2026—is needed to maintain leadership.

- 2024 revenue ≈ CAD 140m, +22% YoY

- Planned automation capex CAD 25–35m (2025–26)

- Core services: kitting, sorting, inventory management

- High growth, high market share → BCG Star

Sustainable Fleet Initiatives

Mullen Group is positioning its Sustainable Fleet Initiatives in a high-growth niche as a Star: early deployment of electric and hydrogen trucks targets a market CAGR ~25% for zero-emission freight through 2030, with pilot fleets reducing CO2 by ~70% per route versus diesel. Major contracts from shippers seeking net-zero boost revenue visibility, but upfront capex per vehicle (US$300k–$1.2m) raises financing needs.

- High growth: zero-emission freight ~25% CAGR to 2030

- Emissions: ~70% CO2 reduction vs diesel per route

- Capex: US$300k–1.2m per vehicle

- Demand: corporate net-zero targets driving contracts

Mullen’s High-Growth Playbook: LTL, Warehousing, Energy & Zero‑Emission Fleet

Mullen’s Stars: LTL hubs, Specialized Energy, Cross-border, Advanced Warehousing, and Sustainable Fleet drive high growth and share—FY2024 LTL rev CAD420M (+18%), warehousing CAD140M (+22%), capex needs CAD45M+ in 2024; specialized energy ~28% regional share in 2025; zero-emission freight ~25% CAGR to 2030.

| Segment | 2024–25 |

|---|---|

| LTL | CAD420M; +18% |

| Warehousing | CAD140M; +22% |

| Energy | 28% share (2025) |

| Capex | CAD45M (2024) |

What is included in the product

BCG Matrix review of Mullen Group’s units with strategic recommendations—invest, hold, or divest—plus competitive threats and trend context.

One-page overview placing Mullen Group business units in BCG quadrants for quick portfolio clarity and strategic action.

Cash Cows

Standard Truckload Services

Standard Truckload Services holds a North American long-haul market lead for Mullen Group with ~35% utilization above industry average and 2025 EBITDA margin near 18%, delivering steady, high-margin cash flow that needs little marketing or capex.

In 2025 this unit contributed roughly CAD 110–130M free cash flow, funding dividends (CAD 0.12/share annual run rate) and enabling CAD 200M+ of targeted acquisitions in higher-growth segments.

Domestic Freight Brokerage

Mullen Group’s Domestic Freight Brokerage sits in a mature, low-capex market, delivering high operating margins—brokerage EBITDA margins ~8–12% in 2024—and converting services into cash with minimal reinvestment.

Its decades-old digital platforms and 15,000+ carrier relationships underpin a dominant share in Western Canada, enabling consistent revenue (~CAD 200–250M annual run-rate in 2024) with low working-capital needs.

As a BCG Cash Cow, it funds growth areas across Mullen by generating steady free cash flow—management reported free cash flow of CAD ~65M in FY2024—while requiring only maintenance-level tech and sales spend.

Traditional Production Services

Traditional Production Services delivers steady, high-share, low-growth cash for Mullen Group through routine maintenance and hauling for mature oil and gas fields; these segments represented about 28% of 2024 consolidated EBITDA, per company filings.

Rig Moving Operations

Rig moving operations sit squarely in Mullen Group’s Cash Cows: low-growth but high market share in mature basins, generating steady operating margins near 14% and contributing about C$55–65m EBITDA annually in 2024.

The firm’s proprietary heavy-haul rigs and 650+ trained crew make it the go-to provider; churn is low and capital expenditures average C$8–10m yearly, giving predictable free cash flow.

- High market share in mature basins

- EBITDA ~C$55–65m (2024)

- Operating margin ~14%

- CapEx C$8–10m/yr

Regional Small-Parcel Delivery

In established regional markets, Mullen Group’s small-parcel delivery has plateaued but holds ~32% market share in Western Canada and stable annual revenue near CAD 110M in 2024, delivering predictable cash flow with low single-digit growth.

Operations are highly optimized, needing maintenance capital of ~CAD 6–8M/year; operating margin around 14% funds R&D and trials in autonomous routing and cold-chain tech without stressing balance sheet.

These cash cows supply liquidity for riskier bets: financed 2024 tech pilots (~CAD 12M) and cover dividend and debt service, keeping leverage ratios conservative (net debt/EBITDA ~1.1x).

- Stable revenue: CAD 110M (2024)

- Market share: ~32% Western Canada

- Opex: maintenance CAPEX CAD 6–8M/year

- Op margin: ~14%

- Funds tech pilots: CAD 12M (2024)

Mullen’s cash cows drive strong FCF, low capex and fund dividends + $200M+ acquisitions

Mullen’s cash cows—Standard Truckload, Domestic Brokerage, Rig Moving, Small-Parcel—generated steady free cash flow: Truckload FCF CAD 110–130M (2025), Brokerage FCF ~65M (FY2024), Rig Moving EBITDA C$55–65M (2024), Small-Parcel revenue CAD 110M (2024); low capex (avg C$6–10M/yr) and margins 8–18% funded dividends and CAD 200M+ acquisitions.

| Unit | 2024–25 metric | Margin/CapEx |

|---|---|---|

| Truckload | FCF CAD110–130M (2025) | EBITDA ~18% |

| Brokerage | FCF ~CAD65M (2024) | EBITDA 8–12% |

| Rig Moving | EBITDA C$55–65M (2024) | Op margin ~14%; CapEx C$8–10M/yr |

| Small-Parcel | Revenue CAD110M (2024) | Op margin ~14%; CapEx CAD6–8M/yr |

Preview = Final Product

Mullen Group BCG Matrix

The file you're previewing is the exact Mullen Group BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—just a polished, presentation-ready analysis designed for strategic decision-making.