Mullen Group Porter's Five Forces Analysis

Don't Miss the Bigger Picture

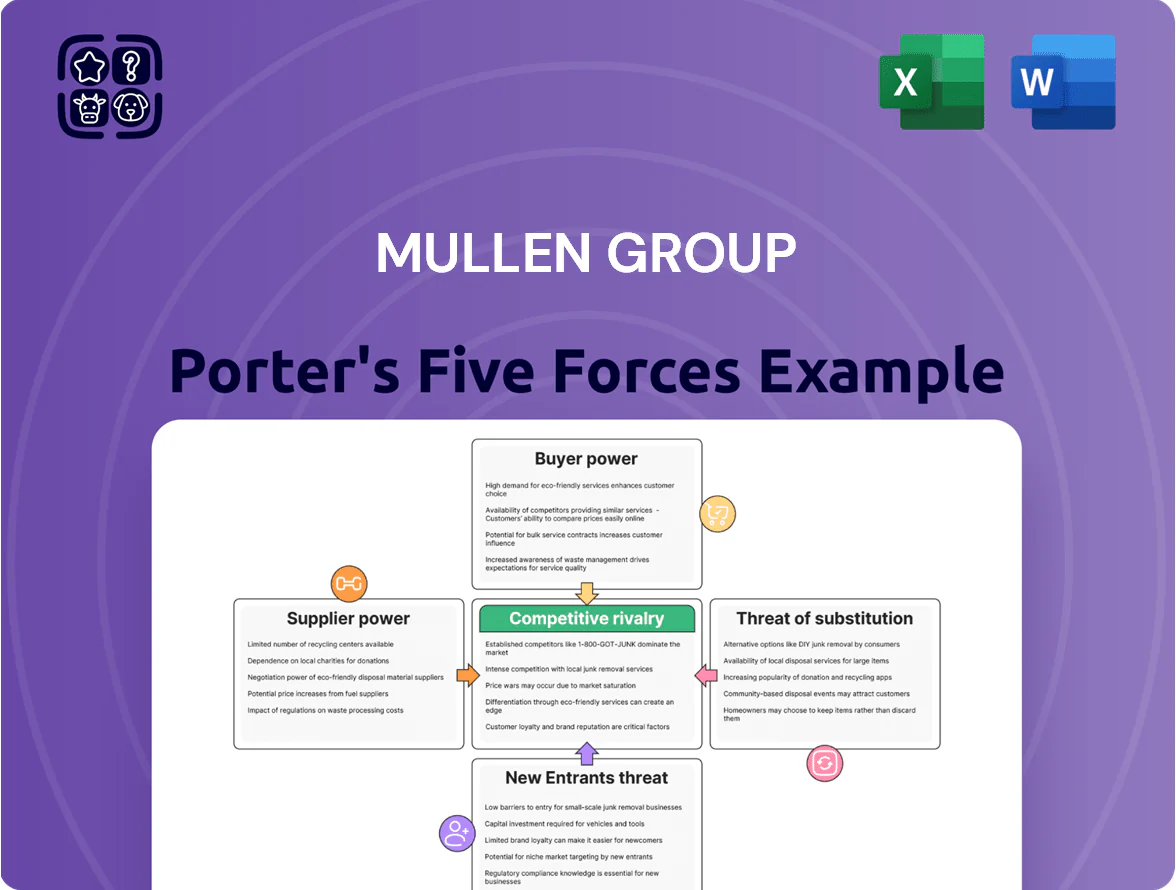

Mullen Group faces moderate competitive rivalry with asset-heavy barriers and regional specialization, while buyer bargaining and supplier influence vary by freight segment; regulatory and technological shifts heighten threat dynamics.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Mullen Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fuel Price Volatility and Dependency

Fuel is Mullen Group’s largest variable cost, with diesel accounting for roughly 20–25% of operating expenses; global Brent crude volatility (2024 range ~$70–$95/bbl) and refinery outages in 2024–25 directly raise per-mile costs.

Fuel surcharges recovered an estimated 60–80% of spot price moves in 2024, but sudden spikes—like the 15% jump after 2024 OPEC+ cuts—still compress margins.

Diesel and low-carbon fuel suppliers set prices via global benchmarks and credits; Mullen cannot control these mechanisms, leaving it exposed to tight supply windows and geopolitical-driven price shocks.

OEM and Equipment Availability

The procurement of heavy-duty trucks, trailers, and specialized equipment is concentrated among a few major OEMs (Paccar, Volvo, Daimler), giving suppliers high bargaining power; global truck OEM order backlogs peaked near 18 months in 2022 and remained elevated into 2024, letting OEMs set lead times and price premiums. Mullen Group’s fleet modernization hinges on supplier relationships and capex: Mullen spent about CA$120m on equipment in 2024, so delays or price rises materially affect replacement pace and operating costs.

Labor Market and Skilled Driver Shortage

The shortage of qualified long-haul and specialized drivers is a binding constraint for North American logistics; US/BLS showed 1.1 million trucker vacancies in 2024 and average turnover near 90% in long-haul fleets, boosting workers’ leverage. Competitive pay and benefits pushed median trucker wages up ~9% in 2023–24, forcing asset-based Mullen Group (TSX: MTL) to adjust diesel, lease, and labor costs and protect margins.

Specialized Technology and Software Providers

Mullen Group depends on third-party telematics, route-optimization, and ERP vendors as logistics shifts data-driven; in 2024 the global transportation management software market grew 11% to about US$12.3B, raising vendor leverage.

High integration and training make switching costly—estimates show enterprise migrations can exceed US$1M and 6–12 months—creating vendor lock-in and recurring SaaS fees.

To reduce dependency, Mullen must keep investing in proprietary systems and API-based modularity; without that, vendor pricing and upgrade cycles can squeeze margins.

- 2024 TMS market ~US$12.3B, +11%

- Switch cost ~US$1M and 6–12 months

- SaaS/vendor lock-in raises recurring Opex

- Proprietary/API investment cuts dependency

Maintenance and Infrastructure Costs

Suppliers of tires, parts, and third-party maintenance keep Mullen Group’s 2024 fleet (≈3,200 power units) running; maintenance accounted for an estimated 6–8% of operating expenses in 2024, pressuring margins if costs rise.

Regional concentration of heavy-equipment repair shops in Western Canada and parts shortages in remote routes reduce bargaining power and raise spot repair premiums by ~10–15% versus urban centers.

Consistent spend across North America—roughly CAD 45–60 million annually on outsourced maintenance—makes supplier relations critical to uptime and delivery reliability.

- Fleet size ~3,200 units (2024)

- Maintenance ≈6–8% of Opex (2024)

- Outsourced spend CAD 45–60M/year

- Repair premium in remote areas +10–15%

Suppliers Squeeze Margins: Fuel, OEM Backlogs, Labor & TMS Lock-In Drive Costs

Suppliers hold moderate-to-high power: fuel (20–25% of opex) and OEM equipment (CA$120m capex in 2024; OEM backlogs ~18 months) drive costs; labor shortages (1.1M US vacancies, ~90% turnover) and TMS/vendor lock-in (TMS market US$12.3B in 2024; switch cost ~US$1M, 6–12 months) add leverage, while maintenance (fleet ~3,200 units; 6–8% of opex; CAD45–60M/yr) tightens margins.

| Factor | 2024 Value |

|---|---|

| Fuel share of opex | 20–25% |

| Equipment capex | CA$120M |

| Fleet size | ~3,200 units |

| Maintenance % of opex | 6–8% |

| TMS market | US$12.3B (+11%) |

| OEM backlog | ~18 months |

| Driver vacancies (US) | 1.1M |

What is included in the product

Uncovers competitive drivers, buyer/supplier power, entry barriers, substitutes, and rivalry shaping Mullen Group’s freight and logistics position, highlighting emerging threats, pricing pressures, and strategic defenses to protect market share.

Concise Porter's Five Forces snapshot for Mullen Group—quickly assess competitive intensity and prioritize strategic moves to relieve margin and growth pressure.

Customers Bargaining Power

Concentration of Major Industrial Clients

Mullen Group serves large energy, mining and retail shippers who move millions of tonnes yearly; in 2024 its top 10 industrial clients accounted for roughly 32% of freight revenue, giving these customers strong price leverage and strict SLA demands.

High-volume contracts commonly secure discounts of 10–20% and prioritize capacity, so losing one major account can cut a specialized business unit’s revenue by 5–15% in a fiscal year.

Low Switching Costs for Standard Freight

For general truckload and LTL, switching costs are low: surveys show 68% of shippers changed carriers within 12 months (2024 study), so Mullen Group must compete on price and on-time performance to retain volume.

Demand for Integrated Logistics Solutions

Modern shippers want end-to-end visibility and integrated warehousing, not point-to-point hauling, and 62% of North American logistics buyers said they prefer bundled services in a 2024 Gartner survey, forcing Mullen Group to expand tech and warehousing to stay competitive.

That demand helps large customers extract lower rates—top-20 shippers account for ~35% of contract value at major carriers—so Mullen must innovate pricing and offer data-driven SLAs to avoid margin erosion.

Economic Sensitivity of End Markets

The bargaining power of customers for Mullen Group (Mullen Group Ltd., ticker MTL on TSX) rises when end markets like Canadian oil and gas weaken; crude-by-rail volumes fell ~22% in 2024 vs 2023, pushing shippers to demand lower rates.

Mullen’s mix of truckload, logistics, and specialized services reduced revenue cyclicality — 2024 diversified segment revenue split: ~45% freight, ~30% logistics, ~25% specialized, cutting customer renegotiation leverage.

Price Transparency through Digital Platforms

- DAT: +12% posted loads (2024)

- Dry van spot: $1.95/mile Q4 2024

- Smaller shippers gain real-time leverage

Top shippers wield pricing power as high churn and spot transparency boost customer leverage

Large industrial shippers (top 10 ≈32% freight revenue in 2024) hold strong price leverage; losing one can cut a unit’s revenue 5–15%. Low switching costs (68% changed carriers within 12 months, 2024) and rising spot transparency (DAT posted loads +12% 2024; dry-van spot $1.95/mile Q4 2024) increase customer bargaining power, though Mullen’s 2024 revenue mix (45/30/25) cushions some pressure.

| Metric | 2024 value |

|---|---|

| Top-10 client share | ≈32% |

| Customer churn (12m) | 68% |

| DAT posted loads change | +12% |

| Dry-van spot | $1.95/mile Q4 |

| Mullen revenue mix | 45/30/25 |

Same Document Delivered

Mullen Group Porter's Five Forces Analysis

This preview shows the exact Mullen Group Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples; it’s the full, professionally formatted document ready for download.

The report covers competitive rivalry, supplier and buyer power, threat of entrants and substitutes, plus implications for strategy and valuation, and is identical to the file delivered upon payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Mullen Group faces moderate competitive rivalry with asset-heavy barriers and regional specialization, while buyer bargaining and supplier influence vary by freight segment; regulatory and technological shifts heighten threat dynamics.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Mullen Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fuel Price Volatility and Dependency

Fuel is Mullen Group’s largest variable cost, with diesel accounting for roughly 20–25% of operating expenses; global Brent crude volatility (2024 range ~$70–$95/bbl) and refinery outages in 2024–25 directly raise per-mile costs.

Fuel surcharges recovered an estimated 60–80% of spot price moves in 2024, but sudden spikes—like the 15% jump after 2024 OPEC+ cuts—still compress margins.

Diesel and low-carbon fuel suppliers set prices via global benchmarks and credits; Mullen cannot control these mechanisms, leaving it exposed to tight supply windows and geopolitical-driven price shocks.

OEM and Equipment Availability

The procurement of heavy-duty trucks, trailers, and specialized equipment is concentrated among a few major OEMs (Paccar, Volvo, Daimler), giving suppliers high bargaining power; global truck OEM order backlogs peaked near 18 months in 2022 and remained elevated into 2024, letting OEMs set lead times and price premiums. Mullen Group’s fleet modernization hinges on supplier relationships and capex: Mullen spent about CA$120m on equipment in 2024, so delays or price rises materially affect replacement pace and operating costs.

Labor Market and Skilled Driver Shortage

The shortage of qualified long-haul and specialized drivers is a binding constraint for North American logistics; US/BLS showed 1.1 million trucker vacancies in 2024 and average turnover near 90% in long-haul fleets, boosting workers’ leverage. Competitive pay and benefits pushed median trucker wages up ~9% in 2023–24, forcing asset-based Mullen Group (TSX: MTL) to adjust diesel, lease, and labor costs and protect margins.

Specialized Technology and Software Providers

Mullen Group depends on third-party telematics, route-optimization, and ERP vendors as logistics shifts data-driven; in 2024 the global transportation management software market grew 11% to about US$12.3B, raising vendor leverage.

High integration and training make switching costly—estimates show enterprise migrations can exceed US$1M and 6–12 months—creating vendor lock-in and recurring SaaS fees.

To reduce dependency, Mullen must keep investing in proprietary systems and API-based modularity; without that, vendor pricing and upgrade cycles can squeeze margins.

- 2024 TMS market ~US$12.3B, +11%

- Switch cost ~US$1M and 6–12 months

- SaaS/vendor lock-in raises recurring Opex

- Proprietary/API investment cuts dependency

Maintenance and Infrastructure Costs

Suppliers of tires, parts, and third-party maintenance keep Mullen Group’s 2024 fleet (≈3,200 power units) running; maintenance accounted for an estimated 6–8% of operating expenses in 2024, pressuring margins if costs rise.

Regional concentration of heavy-equipment repair shops in Western Canada and parts shortages in remote routes reduce bargaining power and raise spot repair premiums by ~10–15% versus urban centers.

Consistent spend across North America—roughly CAD 45–60 million annually on outsourced maintenance—makes supplier relations critical to uptime and delivery reliability.

- Fleet size ~3,200 units (2024)

- Maintenance ≈6–8% of Opex (2024)

- Outsourced spend CAD 45–60M/year

- Repair premium in remote areas +10–15%

Suppliers Squeeze Margins: Fuel, OEM Backlogs, Labor & TMS Lock-In Drive Costs

Suppliers hold moderate-to-high power: fuel (20–25% of opex) and OEM equipment (CA$120m capex in 2024; OEM backlogs ~18 months) drive costs; labor shortages (1.1M US vacancies, ~90% turnover) and TMS/vendor lock-in (TMS market US$12.3B in 2024; switch cost ~US$1M, 6–12 months) add leverage, while maintenance (fleet ~3,200 units; 6–8% of opex; CAD45–60M/yr) tightens margins.

| Factor | 2024 Value |

|---|---|

| Fuel share of opex | 20–25% |

| Equipment capex | CA$120M |

| Fleet size | ~3,200 units |

| Maintenance % of opex | 6–8% |

| TMS market | US$12.3B (+11%) |

| OEM backlog | ~18 months |

| Driver vacancies (US) | 1.1M |

What is included in the product

Uncovers competitive drivers, buyer/supplier power, entry barriers, substitutes, and rivalry shaping Mullen Group’s freight and logistics position, highlighting emerging threats, pricing pressures, and strategic defenses to protect market share.

Concise Porter's Five Forces snapshot for Mullen Group—quickly assess competitive intensity and prioritize strategic moves to relieve margin and growth pressure.

Customers Bargaining Power

Concentration of Major Industrial Clients

Mullen Group serves large energy, mining and retail shippers who move millions of tonnes yearly; in 2024 its top 10 industrial clients accounted for roughly 32% of freight revenue, giving these customers strong price leverage and strict SLA demands.

High-volume contracts commonly secure discounts of 10–20% and prioritize capacity, so losing one major account can cut a specialized business unit’s revenue by 5–15% in a fiscal year.

Low Switching Costs for Standard Freight

For general truckload and LTL, switching costs are low: surveys show 68% of shippers changed carriers within 12 months (2024 study), so Mullen Group must compete on price and on-time performance to retain volume.

Demand for Integrated Logistics Solutions

Modern shippers want end-to-end visibility and integrated warehousing, not point-to-point hauling, and 62% of North American logistics buyers said they prefer bundled services in a 2024 Gartner survey, forcing Mullen Group to expand tech and warehousing to stay competitive.

That demand helps large customers extract lower rates—top-20 shippers account for ~35% of contract value at major carriers—so Mullen must innovate pricing and offer data-driven SLAs to avoid margin erosion.

Economic Sensitivity of End Markets

The bargaining power of customers for Mullen Group (Mullen Group Ltd., ticker MTL on TSX) rises when end markets like Canadian oil and gas weaken; crude-by-rail volumes fell ~22% in 2024 vs 2023, pushing shippers to demand lower rates.

Mullen’s mix of truckload, logistics, and specialized services reduced revenue cyclicality — 2024 diversified segment revenue split: ~45% freight, ~30% logistics, ~25% specialized, cutting customer renegotiation leverage.

Price Transparency through Digital Platforms

- DAT: +12% posted loads (2024)

- Dry van spot: $1.95/mile Q4 2024

- Smaller shippers gain real-time leverage

Top shippers wield pricing power as high churn and spot transparency boost customer leverage

Large industrial shippers (top 10 ≈32% freight revenue in 2024) hold strong price leverage; losing one can cut a unit’s revenue 5–15%. Low switching costs (68% changed carriers within 12 months, 2024) and rising spot transparency (DAT posted loads +12% 2024; dry-van spot $1.95/mile Q4 2024) increase customer bargaining power, though Mullen’s 2024 revenue mix (45/30/25) cushions some pressure.

| Metric | 2024 value |

|---|---|

| Top-10 client share | ≈32% |

| Customer churn (12m) | 68% |

| DAT posted loads change | +12% |

| Dry-van spot | $1.95/mile Q4 |

| Mullen revenue mix | 45/30/25 |

Same Document Delivered

Mullen Group Porter's Five Forces Analysis

This preview shows the exact Mullen Group Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples; it’s the full, professionally formatted document ready for download.

The report covers competitive rivalry, supplier and buyer power, threat of entrants and substitutes, plus implications for strategy and valuation, and is identical to the file delivered upon payment.