Mullen Group SWOT Analysis

Your Strategic Toolkit Starts Here

Mullen Group’s resilient logistics network and diversified services underpin steady revenue streams, while fleet modernization and regional market reach present clear growth levers; however, exposure to fuel costs, regulatory shifts, and cyclical freight demand create execution risks. Purchase the full SWOT analysis to access a professionally written, editable report and Excel matrix—perfect for investors, strategists, and advisors seeking actionable insights and financial context.

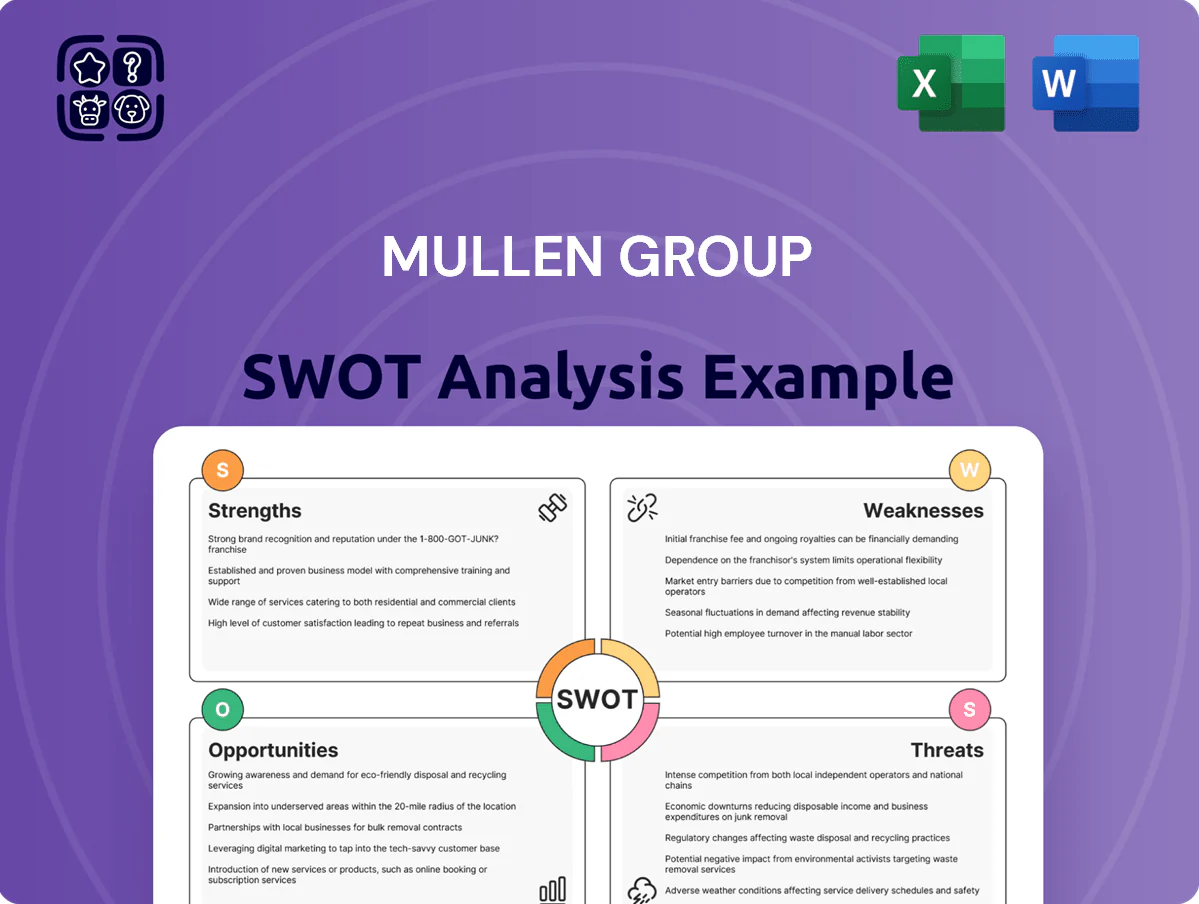

Strengths

Diversified Service Portfolio

Mullen Group operates across four segments—Less-Than-Truckload, Logistics and Warehousing, Specialized and Industrial Services, and US Logistics—generating CA$1.24 billion revenue in FY2024, which cushions swings in any single market. By serving retail, energy, agriculture and manufacturing, segment mix cut quarterly revenue volatility; FY2024 gross margin varied only 2.3 percentage points across segments. This diversification lowers exposure to regional downturns and supports steadier cash flow than pure-play carriers.

Decentralized Management Structure

Mullen Group uses a decentralized model where ~150 independent business units are run by local entrepreneurs, driving accountability and agility; units closed 2024 with combined revenue of CAD 1.15bn, helping average unit EBITDA margins stay near 14% versus industry ~9% in 2024. This structure speeds local decisions, keeps services aligned with customer needs, and still taps parent liquidity—$150m undrawn revolver at YE 2024—for scaling or downturns.

Robust Financial Position

Mullen Group (Mullen Trucking Inc., TSX: MTL) maintains a strong balance sheet: as of Q3 2025 cash and equivalents were C$142.3m and net debt-to-EBITDA was about 1.2x, reflecting manageable leverage. This liquidity and low gearing let Mullen pursue bolt-on acquisitions during 2024–25 market volatility. Their disciplined capital allocation funded C$28m in capex YTD 2025 and sustained a quarterly dividend of C$0.09 per share while supporting organic growth.

Strategic North American Footprint

Mullen Group operates over 200 terminals across Canada and, as of FY2024, expanded U.S. operations to 18 states, giving it a wide North American logistics footprint that supports national and cross-border contracts.

This network helped generate CAD 1.1 billion in 2024 revenue, enabling efficient freight flow and capacity to scale in corridors like Alberta–U.S. Pacific Northwest and Ontario–Midwest.

What this estimate hides: cross-border fuel and tariff volatility can affect margins.

- 200+ Canadian terminals

- 18 U.S. states (FY2024)

- CAD 1.1B revenue in 2024

- Key corridors: Alberta–PNW, Ontario–Midwest

Commitment to Technological Integration

Mullen Group has invested over CAD 45m in proprietary tech and logistics platforms through 2024, using data analytics and real-time tracking to cut empty miles and boost asset utilization across trucking, logistics, and oilfield services.

That tech improved route efficiency by ~12% and helped sustain adjusted EBITDA margin near 11.5% in fiscal 2024 in a capital-heavy industry, raising service reliability and customer retention.

- CAD 45m tech spend through 2024

- ~12% route efficiency gain

- Adjusted EBITDA margin ~11.5% (2024)

- Real-time tracking across business units

Mullen Group: CAD1.24B revenue, strong margins, C$142M cash & 1.2x leverage

Mullen Group’s diversified four-segment model and 200+ terminals drove CAD1.24B revenue in FY2024, lowering volatility and supporting steady cash flow; adjusted EBITDA margin ~11.5% (2024). Decentralized ~150 business units kept avg unit EBITDA ~14% vs industry ~9% in 2024, while C$142.3m cash (Q3 2025) and 1.2x net debt/EBITDA enabled bolt-on deals. Tech spend C$45m cut empty miles ~12%.

| Metric | Value |

|---|---|

| FY2024 Revenue | CAD 1.24B |

| Adj. EBITDA margin (2024) | ~11.5% |

| Avg unit EBITDA (2024) | ~14% |

| Cash (Q3 2025) | C$142.3M |

| Net debt/EBITDA | ~1.2x |

| Tech spend | C$45M (through 2024) |

What is included in the product

Provides a concise SWOT overview of Mullen Group, highlighting its operational strengths, internal weaknesses, external growth opportunities, and market threats shaping strategic decisions.

Provides a concise SWOT snapshot of Mullen Group for rapid strategic alignment and quick stakeholder briefings.

Weaknesses

Cyclical Energy Exposure

High Capital Expenditure Requirements

Maintaining a modern fleet forces Mullen Group to spend heavily: capital expenditures hit C$172.4M in FY2024, and new Class 8 truck prices rose ~12% from 2022–2024, squeezing cash available for ops. Rising maintenance on older assets raised operating maintenance costs by ~8% YoY in 2024, pressuring free cash flow during weak freight demand. This capital intensity forces tradeoffs between renewing fleet and preserving liquidity for acquisitions or tech investments.

Dependence on Labor Availability

The North American trucking sector faced a driver shortage of about 80,000 in 2024, and Mullen Group (Mullen Group Ltd., TSX: MTL) is exposed to this gap, raising recruitment and retention costs—Q3 2025 labour expense rose ~6% year-over-year.

Skilled technician shortages push maintenance lead times higher; any major disruption or understaffing would cap fleet utilization and could force Mullen to decline new contracts or miss SLAs, cutting revenue growth.

Geographic Concentration in Canada

Mullen Group’s assets and ~85% of 2024 revenue remained Canada-focused despite US expansion, leaving results sensitive to Canadian GDP swings, provincial regulation, and rail/road infrastructure bottlenecks.

A prolonged Canadian growth slowdown (GDP growth 0.9% in Q4 2024 annualized) could hit utilization and margins, amplifying cash-flow and leverage pressure on the company’s balance sheet.

- ~85% revenue in Canada (2024)

- Q4 2024 Canada GDP +0.9% annualized

- Exposure to provincial rules and infrastructure delays

Margin Pressure in Competitive Segments

The Less-Than-Truckload and general logistics markets are highly fragmented and intensely price-competitive, driving industry gross margins down; Mullen Group reported a 2024 consolidated gross margin near 14.8%, below some peers, highlighting vulnerability to pricing pressure.

Rivals with lower overhead or aggressive pricing can force margin compression; in 2024 LTL spot rates fell ~6% YoY, so Mullen must push continuous efficiency gains and service differentiation to protect profitability.

- 2024 gross margin ~14.8%

- LTL spot rates down ~6% YoY (2024)

- Requires ongoing cost cuts and tech investment

Canada-heavy oilfield exposure, rising costs and capex squeeze cash flow

| Metric | Value |

|---|---|

| FY2024 Capex | C$172.4M |

| Industrial rev change H1 2024 | -12% |

| Alberta oilfield activity 2024 | -18% YoY |

| 2024 Gross margin | ~14.8% |

| Canada revenue share 2024 | ~85% |

| Labor cost change Q3 2025 | +6% YoY |

| Maintenance cost change 2024 | +8% YoY |

What You See Is What You Get

Mullen Group SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is pulled straight from the final, editable file. You’re viewing a live preview of the real analysis; buy now to unlock the complete, detailed version.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Strategic Toolkit Starts Here

Mullen Group’s resilient logistics network and diversified services underpin steady revenue streams, while fleet modernization and regional market reach present clear growth levers; however, exposure to fuel costs, regulatory shifts, and cyclical freight demand create execution risks. Purchase the full SWOT analysis to access a professionally written, editable report and Excel matrix—perfect for investors, strategists, and advisors seeking actionable insights and financial context.

Strengths

Diversified Service Portfolio

Mullen Group operates across four segments—Less-Than-Truckload, Logistics and Warehousing, Specialized and Industrial Services, and US Logistics—generating CA$1.24 billion revenue in FY2024, which cushions swings in any single market. By serving retail, energy, agriculture and manufacturing, segment mix cut quarterly revenue volatility; FY2024 gross margin varied only 2.3 percentage points across segments. This diversification lowers exposure to regional downturns and supports steadier cash flow than pure-play carriers.

Decentralized Management Structure

Mullen Group uses a decentralized model where ~150 independent business units are run by local entrepreneurs, driving accountability and agility; units closed 2024 with combined revenue of CAD 1.15bn, helping average unit EBITDA margins stay near 14% versus industry ~9% in 2024. This structure speeds local decisions, keeps services aligned with customer needs, and still taps parent liquidity—$150m undrawn revolver at YE 2024—for scaling or downturns.

Robust Financial Position

Mullen Group (Mullen Trucking Inc., TSX: MTL) maintains a strong balance sheet: as of Q3 2025 cash and equivalents were C$142.3m and net debt-to-EBITDA was about 1.2x, reflecting manageable leverage. This liquidity and low gearing let Mullen pursue bolt-on acquisitions during 2024–25 market volatility. Their disciplined capital allocation funded C$28m in capex YTD 2025 and sustained a quarterly dividend of C$0.09 per share while supporting organic growth.

Strategic North American Footprint

Mullen Group operates over 200 terminals across Canada and, as of FY2024, expanded U.S. operations to 18 states, giving it a wide North American logistics footprint that supports national and cross-border contracts.

This network helped generate CAD 1.1 billion in 2024 revenue, enabling efficient freight flow and capacity to scale in corridors like Alberta–U.S. Pacific Northwest and Ontario–Midwest.

What this estimate hides: cross-border fuel and tariff volatility can affect margins.

- 200+ Canadian terminals

- 18 U.S. states (FY2024)

- CAD 1.1B revenue in 2024

- Key corridors: Alberta–PNW, Ontario–Midwest

Commitment to Technological Integration

Mullen Group has invested over CAD 45m in proprietary tech and logistics platforms through 2024, using data analytics and real-time tracking to cut empty miles and boost asset utilization across trucking, logistics, and oilfield services.

That tech improved route efficiency by ~12% and helped sustain adjusted EBITDA margin near 11.5% in fiscal 2024 in a capital-heavy industry, raising service reliability and customer retention.

- CAD 45m tech spend through 2024

- ~12% route efficiency gain

- Adjusted EBITDA margin ~11.5% (2024)

- Real-time tracking across business units

Mullen Group: CAD1.24B revenue, strong margins, C$142M cash & 1.2x leverage

Mullen Group’s diversified four-segment model and 200+ terminals drove CAD1.24B revenue in FY2024, lowering volatility and supporting steady cash flow; adjusted EBITDA margin ~11.5% (2024). Decentralized ~150 business units kept avg unit EBITDA ~14% vs industry ~9% in 2024, while C$142.3m cash (Q3 2025) and 1.2x net debt/EBITDA enabled bolt-on deals. Tech spend C$45m cut empty miles ~12%.

| Metric | Value |

|---|---|

| FY2024 Revenue | CAD 1.24B |

| Adj. EBITDA margin (2024) | ~11.5% |

| Avg unit EBITDA (2024) | ~14% |

| Cash (Q3 2025) | C$142.3M |

| Net debt/EBITDA | ~1.2x |

| Tech spend | C$45M (through 2024) |

What is included in the product

Provides a concise SWOT overview of Mullen Group, highlighting its operational strengths, internal weaknesses, external growth opportunities, and market threats shaping strategic decisions.

Provides a concise SWOT snapshot of Mullen Group for rapid strategic alignment and quick stakeholder briefings.

Weaknesses

Cyclical Energy Exposure

High Capital Expenditure Requirements

Maintaining a modern fleet forces Mullen Group to spend heavily: capital expenditures hit C$172.4M in FY2024, and new Class 8 truck prices rose ~12% from 2022–2024, squeezing cash available for ops. Rising maintenance on older assets raised operating maintenance costs by ~8% YoY in 2024, pressuring free cash flow during weak freight demand. This capital intensity forces tradeoffs between renewing fleet and preserving liquidity for acquisitions or tech investments.

Dependence on Labor Availability

The North American trucking sector faced a driver shortage of about 80,000 in 2024, and Mullen Group (Mullen Group Ltd., TSX: MTL) is exposed to this gap, raising recruitment and retention costs—Q3 2025 labour expense rose ~6% year-over-year.

Skilled technician shortages push maintenance lead times higher; any major disruption or understaffing would cap fleet utilization and could force Mullen to decline new contracts or miss SLAs, cutting revenue growth.

Geographic Concentration in Canada

Mullen Group’s assets and ~85% of 2024 revenue remained Canada-focused despite US expansion, leaving results sensitive to Canadian GDP swings, provincial regulation, and rail/road infrastructure bottlenecks.

A prolonged Canadian growth slowdown (GDP growth 0.9% in Q4 2024 annualized) could hit utilization and margins, amplifying cash-flow and leverage pressure on the company’s balance sheet.

- ~85% revenue in Canada (2024)

- Q4 2024 Canada GDP +0.9% annualized

- Exposure to provincial rules and infrastructure delays

Margin Pressure in Competitive Segments

The Less-Than-Truckload and general logistics markets are highly fragmented and intensely price-competitive, driving industry gross margins down; Mullen Group reported a 2024 consolidated gross margin near 14.8%, below some peers, highlighting vulnerability to pricing pressure.

Rivals with lower overhead or aggressive pricing can force margin compression; in 2024 LTL spot rates fell ~6% YoY, so Mullen must push continuous efficiency gains and service differentiation to protect profitability.

- 2024 gross margin ~14.8%

- LTL spot rates down ~6% YoY (2024)

- Requires ongoing cost cuts and tech investment

Canada-heavy oilfield exposure, rising costs and capex squeeze cash flow

| Metric | Value |

|---|---|

| FY2024 Capex | C$172.4M |

| Industrial rev change H1 2024 | -12% |

| Alberta oilfield activity 2024 | -18% YoY |

| 2024 Gross margin | ~14.8% |

| Canada revenue share 2024 | ~85% |

| Labor cost change Q3 2025 | +6% YoY |

| Maintenance cost change 2024 | +8% YoY |

What You See Is What You Get

Mullen Group SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is pulled straight from the final, editable file. You’re viewing a live preview of the real analysis; buy now to unlock the complete, detailed version.