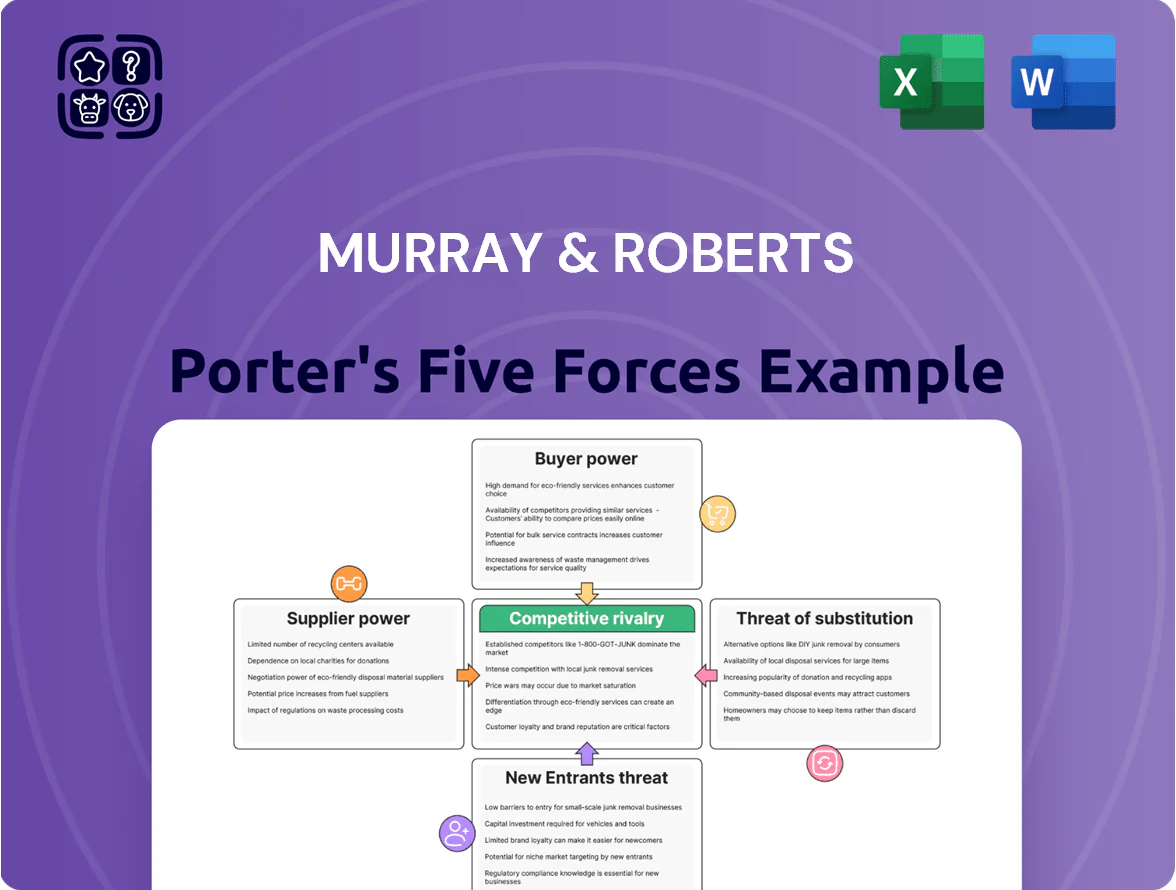

Murray & Roberts Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Murray & Roberts operates in a capital-intensive, project-driven sector where supplier leverage, client concentration, and project bidding dynamics shape profitability—this snapshot highlights core pressures and strategic levers.

The full Porter’s Five Forces Analysis uncovers force-by-force ratings, competitive intensity, and substitute risks, delivering visualizations and implications tailored to Murray & Roberts.

Ready to act? Unlock the complete report for a consultant-grade, data-driven breakdown to inform investment or strategic decisions.

Suppliers Bargaining Power

Specialized Equipment and Technology Providers

The procurement of advanced mining machinery and energy-infrastructure components depends on a handful of global OEMs, giving suppliers strong leverage over Murray & Roberts; 2024-25 data show the top 5 OEMs control roughly 60–70% of the relevant market for automated and EV-capable equipment. This concentration matters because specialized tech is required to meet safety and productivity KPIs, and price or lead-time shifts from suppliers can move project margins by 2–5 percentage points. The 2025 shift to automation and electric fleets further concentrates power among high-tech vendors with proprietary software and battery systems, where replacement lead times now average 6–12 months. For Murray & Roberts, diversified procurement and strategic vendor partnerships are essential to reduce single-supplier risk and cap potential cost increases.

Availability of Highly Skilled Engineering Talent

The bargaining power of highly skilled engineers and project managers is high due to a global shortfall—IEA and World Bank data show 15–20% skill gaps in mining and renewables by 2024—forcing Murray & Roberts to offer market-leading pay; median engineering salaries in South Africa rose ~12% in 2023 to ZAR 720,000, increasing project labor costs.

Volatility in Raw Material Pricing

Suppliers of steel, cement and alloys wield pricing power; global steel prices rose 12% in 2024, pushing input costs higher for construction firms like Murray & Roberts.

Long project timelines mean a 10% raw-material spike can cut margins sharply if contracts lack escalation clauses; many group EPC contracts in 2023–24 included partial escalation protections.

Maintaining ties with multiple distributors and sourcing hubs—South Africa, UAE, Europe—reduces disruption risk and hedges volatile spot markets.

Dependency on Niche Subcontractors

For large-scale infrastructure and energy projects, Murray & Roberts relies on local niche subcontractors for specialized site services and civil works; in some African and Australian remote sites, fewer than 10 qualified firms often bid, boosting those suppliers’ leverage.

Scarcity raises bargaining power, risks cost uplifts (observed subcontractor margins up to 15% in 2024 tenders) and schedule slippage, so M&R must tightly manage contracts, performance bonds, and contingency buffers.

- Dependency on <10 local specialists in remote sites

- Subcontractor margins up to 15% in 2024 tenders

- Requires performance bonds, tight SLAs, contingency buffers

Energy and Utility Costs

As a heavy industrial group, Murray & Roberts is highly sensitive to energy price swings and outages; South African industrial electricity tariffs rose ~54% from 2019–2024, raising operating costs materially for fabrication and mining services.

National utility Eskom’s near-monopoly gives suppliers pricing power and reliability risk, pushing Murray & Roberts to invest in on-site generation and renewables to protect margins.

Here’s the quick math: a 20% rise in energy cost can cut segment EBIT margins by ~3–5% if not mitigated.

- High exposure: heavy energy use in fabrication and construction

- Supplier power: Eskom monopoly → price + outage risk

- Mitigation: capex in self-generation and renewables

- Impact: 20% energy cost rise → ~3–5% EBIT margin hit

Supplier concentration & rising costs squeeze margins—2–5ppt hit, long lead times

Suppliers—few global OEMs for automated/EV equipment (top5: ~60–70% market share, 2024–25), scarce local niche subcontractors (<10 in remote bids), and Eskom’s near-monopoly—give high bargaining power, driving input-cost and lead-time risk (steel +12% in 2024; energy tariffs +54% 2019–24) that can shave 2–5ppt project margins or 3–5% EBIT on a 20% energy rise.

| Metric | Value |

|---|---|

| Top‑5 OEM share (2024–25) | 60–70% |

| Remote-site qualified subcontractors | <10 firms |

| Steel price change (2024) | +12% |

| SA industrial tariffs (2019–24) | +54% |

| Subcontractor margins (2024 tenders) | up to 15% |

| Lead times (battery/automation) | 6–12 months |

What is included in the product

Tailored exclusively for Murray & Roberts, this Porter's Five Forces overview uncovers competitive drivers, supplier and buyer influence, entry barriers, substitutes, and emerging threats shaping the firm’s profitability and strategic positioning.

A concise Porter's Five Forces snapshot for Murray & Roberts—turn complex competitive dynamics into actionable insights for faster strategic decisions.

Customers Bargaining Power

Concentration of Major Global Clients

The customer base for Murray & Roberts is dominated by a few large mining houses and energy conglomerates, with the top 5 clients historically accounting for roughly 35–45% of group revenue (2024 results). These blue-chip buyers wield strong leverage to demand extended credit terms and steep price cuts during tenders, squeezing margins. Losing a single major contract can cut annual revenue by mid-single-digit to low-double-digit percentages and damage market standing. This concentration raises client bargaining power and revenue volatility.

Rigorous Competitive Bidding Processes

Project procurement runs through transparent, highly competitive bidding cycles where price often decides winners; clients pushed average engineering margins down to ~6–8% in 2024 vs 9–11% in 2019, per industry reports. Customers exploit bidding to shift risk—contract-change liabilities and performance bonds rose 15% in median value in 2023. In 2025, digital procurement platforms let clients compare global bids in minutes, increasing quote volume by ~30% and further compressing prices.

High Standards for ESG and Safety Compliance

Modern clients require strict ESG and safety compliance as a contract must-have, with 72% of global procurement teams (2024 McKinsey survey) refusing bids that miss sustainability targets, so Murray & Roberts faces high customer scrutiny.

Buyers can disqualify firms lacking specific emissions reductions or safety KPIs, and 58% of EPC contracts in South Africa (2023 industry data) included penalty clauses tied to LTI rates and CO2 limits.

This gives customers leverage to dictate methods and force upfront capex for green tech—Murray & Roberts may need multimillion-rand investments to meet net-zero and ISO 45001 benchmarks or lose bids.

Low Switching Costs at the Tender Stage

Before contract award, buyers can switch among global engineering groups—tenders often see 4–6 bidders for large projects, letting clients secure price cuts of 5–12% during negotiation (example: 2024 South Africa infrastructure tenders averaged 5.8% bid compression).

During feasibility and design stages switching costs are low, so customers leverage competition to improve terms, but once construction starts costs and contractual penalties rise sharply, locking in suppliers and protecting Murray & Roberts’ margins.

- 4–6 bidders typical per large tender

- 5–12% average pre-award price compression (2024)

- High post-award switching costs and penalties

Demand for Fixed-Price and Turnkey Solutions

Clients increasingly demand fixed-price and turnkey contracts, shifting cost and schedule risk to contractors; globally, fixed-price project share rose to ~42% in large EPC tenders by 2024, pressuring margins.

Murray & Roberts must weigh bid-win pressure against risk: accepting lump-sum work can boost revenue but raises exposure to cost inflation, with COVID-era supply shocks pushing input volatility up ~18% (2021–24).

Careful contract modeling, tighter change-order clauses, and targeted risk premiums are needed to protect EBITDA; a 2–4% premium on bid price often reflects reasonable contingency for medium-risk projects.

- Fixed-price share ~42% in large EPC tenders (2024)

- Input price volatility +18% (2021–24)

- Suggested risk premium 2–4% of bid

- Prioritize change-order protection and capex hedges

Customers dictate terms: concentrated revenue, fierce bidding, ESG-driven pricing pressure

Customers hold high bargaining power: top 5 clients = 35–45% revenue (2024), 4–6 bidders per large tender, pre-award price compression 5–12% (2024), fixed-price share ~42% (2024), engineering margins ~6–8% (2024). Buyers push ESG/safety clauses (72% reject non-compliant bids) and shift risks via fixed-price/penalties, forcing Murray & Roberts to add 2–4% risk premiums.

| Metric | Value (Year) |

|---|---|

| Top-5 client revenue | 35–45% (2024) |

| Bidders per tender | 4–6 (2024) |

| Pre-award price compression | 5–12% (2024) |

| Fixed-price share | 42% (2024) |

| Engineering margins | 6–8% (2024) |

| ESG rejection rate | 72% (2024) |

| Suggested risk premium | 2–4% |

Full Version Awaits

Murray & Roberts Porter's Five Forces Analysis

This preview shows the exact Murray & Roberts Porter's Five Forces analysis you'll receive—fully written, formatted, and ready to download immediately after purchase with no placeholders or samples.

You're viewing the final deliverable: a concise, professional assessment of competitive rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications—available instantly once you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Murray & Roberts operates in a capital-intensive, project-driven sector where supplier leverage, client concentration, and project bidding dynamics shape profitability—this snapshot highlights core pressures and strategic levers.

The full Porter’s Five Forces Analysis uncovers force-by-force ratings, competitive intensity, and substitute risks, delivering visualizations and implications tailored to Murray & Roberts.

Ready to act? Unlock the complete report for a consultant-grade, data-driven breakdown to inform investment or strategic decisions.

Suppliers Bargaining Power

Specialized Equipment and Technology Providers

The procurement of advanced mining machinery and energy-infrastructure components depends on a handful of global OEMs, giving suppliers strong leverage over Murray & Roberts; 2024-25 data show the top 5 OEMs control roughly 60–70% of the relevant market for automated and EV-capable equipment. This concentration matters because specialized tech is required to meet safety and productivity KPIs, and price or lead-time shifts from suppliers can move project margins by 2–5 percentage points. The 2025 shift to automation and electric fleets further concentrates power among high-tech vendors with proprietary software and battery systems, where replacement lead times now average 6–12 months. For Murray & Roberts, diversified procurement and strategic vendor partnerships are essential to reduce single-supplier risk and cap potential cost increases.

Availability of Highly Skilled Engineering Talent

The bargaining power of highly skilled engineers and project managers is high due to a global shortfall—IEA and World Bank data show 15–20% skill gaps in mining and renewables by 2024—forcing Murray & Roberts to offer market-leading pay; median engineering salaries in South Africa rose ~12% in 2023 to ZAR 720,000, increasing project labor costs.

Volatility in Raw Material Pricing

Suppliers of steel, cement and alloys wield pricing power; global steel prices rose 12% in 2024, pushing input costs higher for construction firms like Murray & Roberts.

Long project timelines mean a 10% raw-material spike can cut margins sharply if contracts lack escalation clauses; many group EPC contracts in 2023–24 included partial escalation protections.

Maintaining ties with multiple distributors and sourcing hubs—South Africa, UAE, Europe—reduces disruption risk and hedges volatile spot markets.

Dependency on Niche Subcontractors

For large-scale infrastructure and energy projects, Murray & Roberts relies on local niche subcontractors for specialized site services and civil works; in some African and Australian remote sites, fewer than 10 qualified firms often bid, boosting those suppliers’ leverage.

Scarcity raises bargaining power, risks cost uplifts (observed subcontractor margins up to 15% in 2024 tenders) and schedule slippage, so M&R must tightly manage contracts, performance bonds, and contingency buffers.

- Dependency on <10 local specialists in remote sites

- Subcontractor margins up to 15% in 2024 tenders

- Requires performance bonds, tight SLAs, contingency buffers

Energy and Utility Costs

As a heavy industrial group, Murray & Roberts is highly sensitive to energy price swings and outages; South African industrial electricity tariffs rose ~54% from 2019–2024, raising operating costs materially for fabrication and mining services.

National utility Eskom’s near-monopoly gives suppliers pricing power and reliability risk, pushing Murray & Roberts to invest in on-site generation and renewables to protect margins.

Here’s the quick math: a 20% rise in energy cost can cut segment EBIT margins by ~3–5% if not mitigated.

- High exposure: heavy energy use in fabrication and construction

- Supplier power: Eskom monopoly → price + outage risk

- Mitigation: capex in self-generation and renewables

- Impact: 20% energy cost rise → ~3–5% EBIT margin hit

Supplier concentration & rising costs squeeze margins—2–5ppt hit, long lead times

Suppliers—few global OEMs for automated/EV equipment (top5: ~60–70% market share, 2024–25), scarce local niche subcontractors (<10 in remote bids), and Eskom’s near-monopoly—give high bargaining power, driving input-cost and lead-time risk (steel +12% in 2024; energy tariffs +54% 2019–24) that can shave 2–5ppt project margins or 3–5% EBIT on a 20% energy rise.

| Metric | Value |

|---|---|

| Top‑5 OEM share (2024–25) | 60–70% |

| Remote-site qualified subcontractors | <10 firms |

| Steel price change (2024) | +12% |

| SA industrial tariffs (2019–24) | +54% |

| Subcontractor margins (2024 tenders) | up to 15% |

| Lead times (battery/automation) | 6–12 months |

What is included in the product

Tailored exclusively for Murray & Roberts, this Porter's Five Forces overview uncovers competitive drivers, supplier and buyer influence, entry barriers, substitutes, and emerging threats shaping the firm’s profitability and strategic positioning.

A concise Porter's Five Forces snapshot for Murray & Roberts—turn complex competitive dynamics into actionable insights for faster strategic decisions.

Customers Bargaining Power

Concentration of Major Global Clients

The customer base for Murray & Roberts is dominated by a few large mining houses and energy conglomerates, with the top 5 clients historically accounting for roughly 35–45% of group revenue (2024 results). These blue-chip buyers wield strong leverage to demand extended credit terms and steep price cuts during tenders, squeezing margins. Losing a single major contract can cut annual revenue by mid-single-digit to low-double-digit percentages and damage market standing. This concentration raises client bargaining power and revenue volatility.

Rigorous Competitive Bidding Processes

Project procurement runs through transparent, highly competitive bidding cycles where price often decides winners; clients pushed average engineering margins down to ~6–8% in 2024 vs 9–11% in 2019, per industry reports. Customers exploit bidding to shift risk—contract-change liabilities and performance bonds rose 15% in median value in 2023. In 2025, digital procurement platforms let clients compare global bids in minutes, increasing quote volume by ~30% and further compressing prices.

High Standards for ESG and Safety Compliance

Modern clients require strict ESG and safety compliance as a contract must-have, with 72% of global procurement teams (2024 McKinsey survey) refusing bids that miss sustainability targets, so Murray & Roberts faces high customer scrutiny.

Buyers can disqualify firms lacking specific emissions reductions or safety KPIs, and 58% of EPC contracts in South Africa (2023 industry data) included penalty clauses tied to LTI rates and CO2 limits.

This gives customers leverage to dictate methods and force upfront capex for green tech—Murray & Roberts may need multimillion-rand investments to meet net-zero and ISO 45001 benchmarks or lose bids.

Low Switching Costs at the Tender Stage

Before contract award, buyers can switch among global engineering groups—tenders often see 4–6 bidders for large projects, letting clients secure price cuts of 5–12% during negotiation (example: 2024 South Africa infrastructure tenders averaged 5.8% bid compression).

During feasibility and design stages switching costs are low, so customers leverage competition to improve terms, but once construction starts costs and contractual penalties rise sharply, locking in suppliers and protecting Murray & Roberts’ margins.

- 4–6 bidders typical per large tender

- 5–12% average pre-award price compression (2024)

- High post-award switching costs and penalties

Demand for Fixed-Price and Turnkey Solutions

Clients increasingly demand fixed-price and turnkey contracts, shifting cost and schedule risk to contractors; globally, fixed-price project share rose to ~42% in large EPC tenders by 2024, pressuring margins.

Murray & Roberts must weigh bid-win pressure against risk: accepting lump-sum work can boost revenue but raises exposure to cost inflation, with COVID-era supply shocks pushing input volatility up ~18% (2021–24).

Careful contract modeling, tighter change-order clauses, and targeted risk premiums are needed to protect EBITDA; a 2–4% premium on bid price often reflects reasonable contingency for medium-risk projects.

- Fixed-price share ~42% in large EPC tenders (2024)

- Input price volatility +18% (2021–24)

- Suggested risk premium 2–4% of bid

- Prioritize change-order protection and capex hedges

Customers dictate terms: concentrated revenue, fierce bidding, ESG-driven pricing pressure

Customers hold high bargaining power: top 5 clients = 35–45% revenue (2024), 4–6 bidders per large tender, pre-award price compression 5–12% (2024), fixed-price share ~42% (2024), engineering margins ~6–8% (2024). Buyers push ESG/safety clauses (72% reject non-compliant bids) and shift risks via fixed-price/penalties, forcing Murray & Roberts to add 2–4% risk premiums.

| Metric | Value (Year) |

|---|---|

| Top-5 client revenue | 35–45% (2024) |

| Bidders per tender | 4–6 (2024) |

| Pre-award price compression | 5–12% (2024) |

| Fixed-price share | 42% (2024) |

| Engineering margins | 6–8% (2024) |

| ESG rejection rate | 72% (2024) |

| Suggested risk premium | 2–4% |

Full Version Awaits

Murray & Roberts Porter's Five Forces Analysis

This preview shows the exact Murray & Roberts Porter's Five Forces analysis you'll receive—fully written, formatted, and ready to download immediately after purchase with no placeholders or samples.

You're viewing the final deliverable: a concise, professional assessment of competitive rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications—available instantly once you buy.