Murray & Roberts SWOT Analysis

Your Strategic Toolkit Starts Here

Murray & Roberts faces a dynamic blend of engineering expertise and cyclical exposure—our concise SWOT highlights core strengths like project execution and geographic reach, while flagging risks from commodity cycles and contract concentration; for the full strategic picture, purchase the complete SWOT analysis to get a research-backed, editable report and Excel deliverable to support investment or planning decisions.

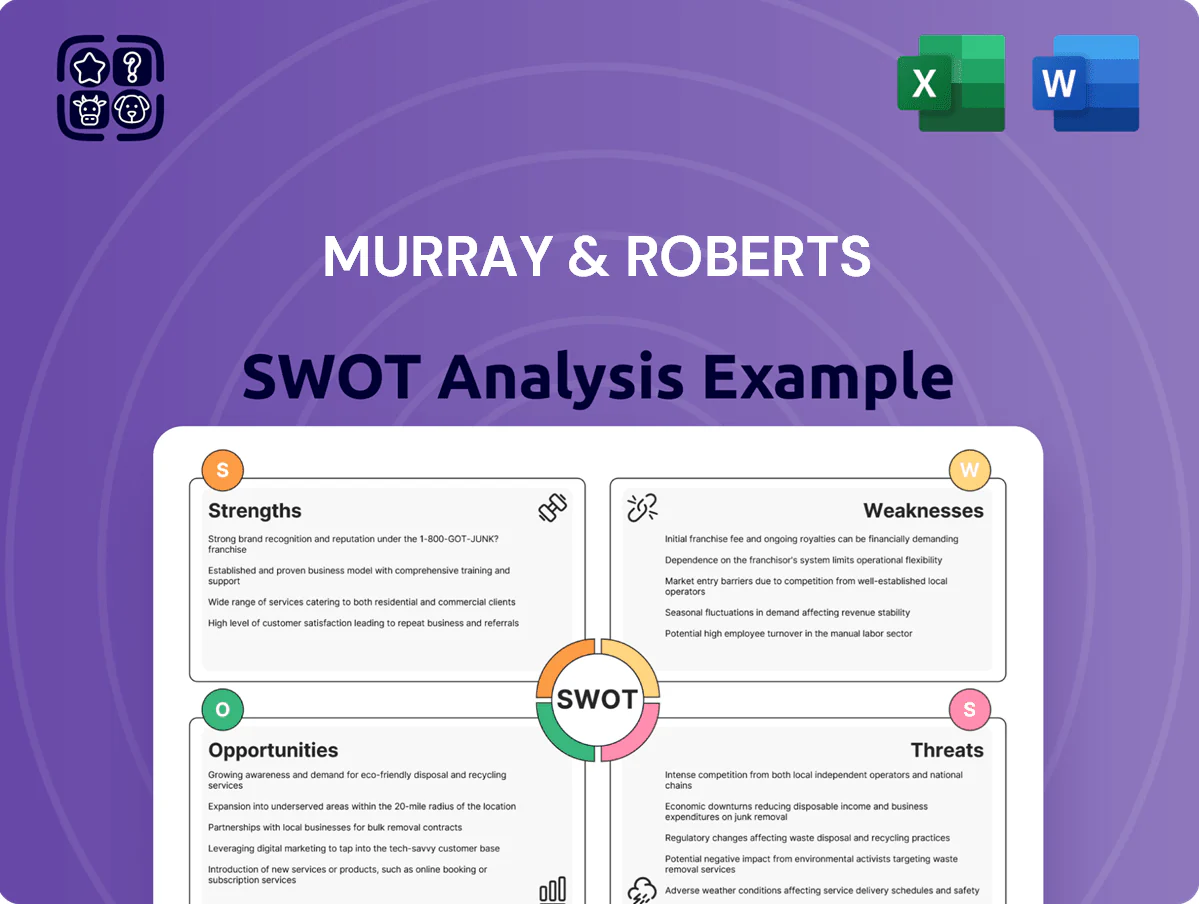

Strengths

Dominant Underground Mining Expertise

Geographically Diversified Revenue Streams

Murray & Roberts operates across Africa, the Americas and Australasia, reducing exposure to single-market shocks; regional revenue split—about 45% Africa, 30% Australasia, 25% Americas in FY2024—softens localized downturns.

The multinational footprint gives access to varied commodity cycles and infrastructure programs; FY2024 order book of ZAR 28.5bn diversified by region supports resilience.

Local teams navigate regulation while applying global best practices, enabling repeat wins on projects and improving margin recovery—group headcount ~8,400 in 2024 reflects regional capability.

Robust Multi-Year Order Book

The firm holds a multi-year order book worth about ZAR 45 billion as of FY2025, giving revenue visibility into the latter half of the decade and covering an estimated 60–70% of projected 2026–2028 revenue.

Contracts are with major mining and infrastructure clients—reducing short-term revenue gap risk—and average contract margins are higher after tighter project selection.

Management’s quality-over-quantity approach has cut project loss incidents by roughly 40% since 2021, improving the company’s forward earnings risk profile.

Specialized Engineering and Design Capabilities

- End-to-end capture: 27% revenue from integrated services (FY2025)

- Service backlog: R6.5bn, +18% YoY (Dec 2025)

- BIM impact: -22% rework, +14% on-time delivery

- Margin uplift: +260 bps EBITDA in engineered projects

Leaner Post-Restructuring Corporate Structure

- Overhead reduction ~18% vs 2022

- Mining & energy ~72% of revenue in 2025

- Won ~ZAR 4.1bn EPC contracts H1 2025

Murray & Roberts: Deep‑mine leader with R45bn order book, R1.2bn new wins

| Metric | Value |

|---|---|

| Deep-mine share | ~35% |

| New wins | R1.2bn (to Dec 2025) |

| Order book | R45bn (FY2025) |

| Underground rev | ~40% (FY2025) |

| Integrated services | 27% (FY2025) |

What is included in the product

Provides a concise SWOT assessment of Murray & Roberts, highlighting internal capabilities and weaknesses alongside external opportunities and threats shaping its competitive and strategic position.

Delivers a concise Murray & Roberts SWOT snapshot for rapid strategic alignment and decision-making across project and corporate portfolios.

Weaknesses

Historical Debt Burden and Financial Leverage

Exposure to Fixed-Price Contract Risks

Dependence on Cyclical Commodity Markets

A large majority of Murray & Roberts Group revenue comes from mining and energy clients, so it's highly exposed to commodity cycles; mining & materials made up about 60% of group revenue in FY2024 (annual report, 2024).

When copper, gold or oil prices fall, clients cut capex and tender volumes drop—BofA data shows mining capex fell ~12% year-on-year in 2024—reducing new contract awards to the group.

This cyclicality drives earnings and cashflow volatility; Murray & Roberts’ FY2024 EBIT swung by ±35% versus FY2023, and its share price volatility (beta ~1.4) reflects that sensitivity.

Geopolitical Risks in Emerging Markets

- 6% regional EBITDA margin impact (2024)

- R1.2 billion added working-capital (2022–24)

- Local-content law changes: Zambia 2023, Nigeria 2024

Limited Balance Sheet Scale for Mega-Projects

Compared with global EPC giants like Bechtel (2024 revenue US$12.1bn) Murray & Roberts (FY2024 revenue ZAR 24.6bn ≈ US$1.3bn) has limited balance-sheet capacity to provide the multi-hundred-million to multi-billion-dollar guarantees for mega-infrastructure projects, raising project financing constraints.

This often forces joint ventures to secure bids, which reduces control and dilutes profit share; in FY2024 JV revenue made up a material portion of large-project income, reflecting selective bidding to avoid overextension.

- FY2024 revenue ZAR 24.6bn (≈US$1.3bn)

- Bechtel 2024 revenue US$12.1bn (comparator)

- Relies on JVs for mega-project bids—dilutes control/profits

- Selective bidding needed to protect balance sheet and guarantees

High debt, thin EBITDA and mining exposure fuel volatility amid rising working capital

| Metric | Value |

|---|---|

| Net debt | ZAR 5.4bn |

| Interest/finance | ZAR 420m |

| Revenue FY2024 | ZAR 24.6bn |

| EBITDA margin | ~6% |

| Mining/energy revenue | 60% |

| Working-capital add | R1.2bn (2022–24) |

Same Document Delivered

Murray & Roberts SWOT Analysis

This is the actual Murray & Roberts SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth, editable version ready for immediate download.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Strategic Toolkit Starts Here

Murray & Roberts faces a dynamic blend of engineering expertise and cyclical exposure—our concise SWOT highlights core strengths like project execution and geographic reach, while flagging risks from commodity cycles and contract concentration; for the full strategic picture, purchase the complete SWOT analysis to get a research-backed, editable report and Excel deliverable to support investment or planning decisions.

Strengths

Dominant Underground Mining Expertise

Geographically Diversified Revenue Streams

Murray & Roberts operates across Africa, the Americas and Australasia, reducing exposure to single-market shocks; regional revenue split—about 45% Africa, 30% Australasia, 25% Americas in FY2024—softens localized downturns.

The multinational footprint gives access to varied commodity cycles and infrastructure programs; FY2024 order book of ZAR 28.5bn diversified by region supports resilience.

Local teams navigate regulation while applying global best practices, enabling repeat wins on projects and improving margin recovery—group headcount ~8,400 in 2024 reflects regional capability.

Robust Multi-Year Order Book

The firm holds a multi-year order book worth about ZAR 45 billion as of FY2025, giving revenue visibility into the latter half of the decade and covering an estimated 60–70% of projected 2026–2028 revenue.

Contracts are with major mining and infrastructure clients—reducing short-term revenue gap risk—and average contract margins are higher after tighter project selection.

Management’s quality-over-quantity approach has cut project loss incidents by roughly 40% since 2021, improving the company’s forward earnings risk profile.

Specialized Engineering and Design Capabilities

- End-to-end capture: 27% revenue from integrated services (FY2025)

- Service backlog: R6.5bn, +18% YoY (Dec 2025)

- BIM impact: -22% rework, +14% on-time delivery

- Margin uplift: +260 bps EBITDA in engineered projects

Leaner Post-Restructuring Corporate Structure

- Overhead reduction ~18% vs 2022

- Mining & energy ~72% of revenue in 2025

- Won ~ZAR 4.1bn EPC contracts H1 2025

Murray & Roberts: Deep‑mine leader with R45bn order book, R1.2bn new wins

| Metric | Value |

|---|---|

| Deep-mine share | ~35% |

| New wins | R1.2bn (to Dec 2025) |

| Order book | R45bn (FY2025) |

| Underground rev | ~40% (FY2025) |

| Integrated services | 27% (FY2025) |

What is included in the product

Provides a concise SWOT assessment of Murray & Roberts, highlighting internal capabilities and weaknesses alongside external opportunities and threats shaping its competitive and strategic position.

Delivers a concise Murray & Roberts SWOT snapshot for rapid strategic alignment and decision-making across project and corporate portfolios.

Weaknesses

Historical Debt Burden and Financial Leverage

Exposure to Fixed-Price Contract Risks

Dependence on Cyclical Commodity Markets

A large majority of Murray & Roberts Group revenue comes from mining and energy clients, so it's highly exposed to commodity cycles; mining & materials made up about 60% of group revenue in FY2024 (annual report, 2024).

When copper, gold or oil prices fall, clients cut capex and tender volumes drop—BofA data shows mining capex fell ~12% year-on-year in 2024—reducing new contract awards to the group.

This cyclicality drives earnings and cashflow volatility; Murray & Roberts’ FY2024 EBIT swung by ±35% versus FY2023, and its share price volatility (beta ~1.4) reflects that sensitivity.

Geopolitical Risks in Emerging Markets

- 6% regional EBITDA margin impact (2024)

- R1.2 billion added working-capital (2022–24)

- Local-content law changes: Zambia 2023, Nigeria 2024

Limited Balance Sheet Scale for Mega-Projects

Compared with global EPC giants like Bechtel (2024 revenue US$12.1bn) Murray & Roberts (FY2024 revenue ZAR 24.6bn ≈ US$1.3bn) has limited balance-sheet capacity to provide the multi-hundred-million to multi-billion-dollar guarantees for mega-infrastructure projects, raising project financing constraints.

This often forces joint ventures to secure bids, which reduces control and dilutes profit share; in FY2024 JV revenue made up a material portion of large-project income, reflecting selective bidding to avoid overextension.

- FY2024 revenue ZAR 24.6bn (≈US$1.3bn)

- Bechtel 2024 revenue US$12.1bn (comparator)

- Relies on JVs for mega-project bids—dilutes control/profits

- Selective bidding needed to protect balance sheet and guarantees

High debt, thin EBITDA and mining exposure fuel volatility amid rising working capital

| Metric | Value |

|---|---|

| Net debt | ZAR 5.4bn |

| Interest/finance | ZAR 420m |

| Revenue FY2024 | ZAR 24.6bn |

| EBITDA margin | ~6% |

| Mining/energy revenue | 60% |

| Working-capital add | R1.2bn (2022–24) |

Same Document Delivered

Murray & Roberts SWOT Analysis

This is the actual Murray & Roberts SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth, editable version ready for immediate download.