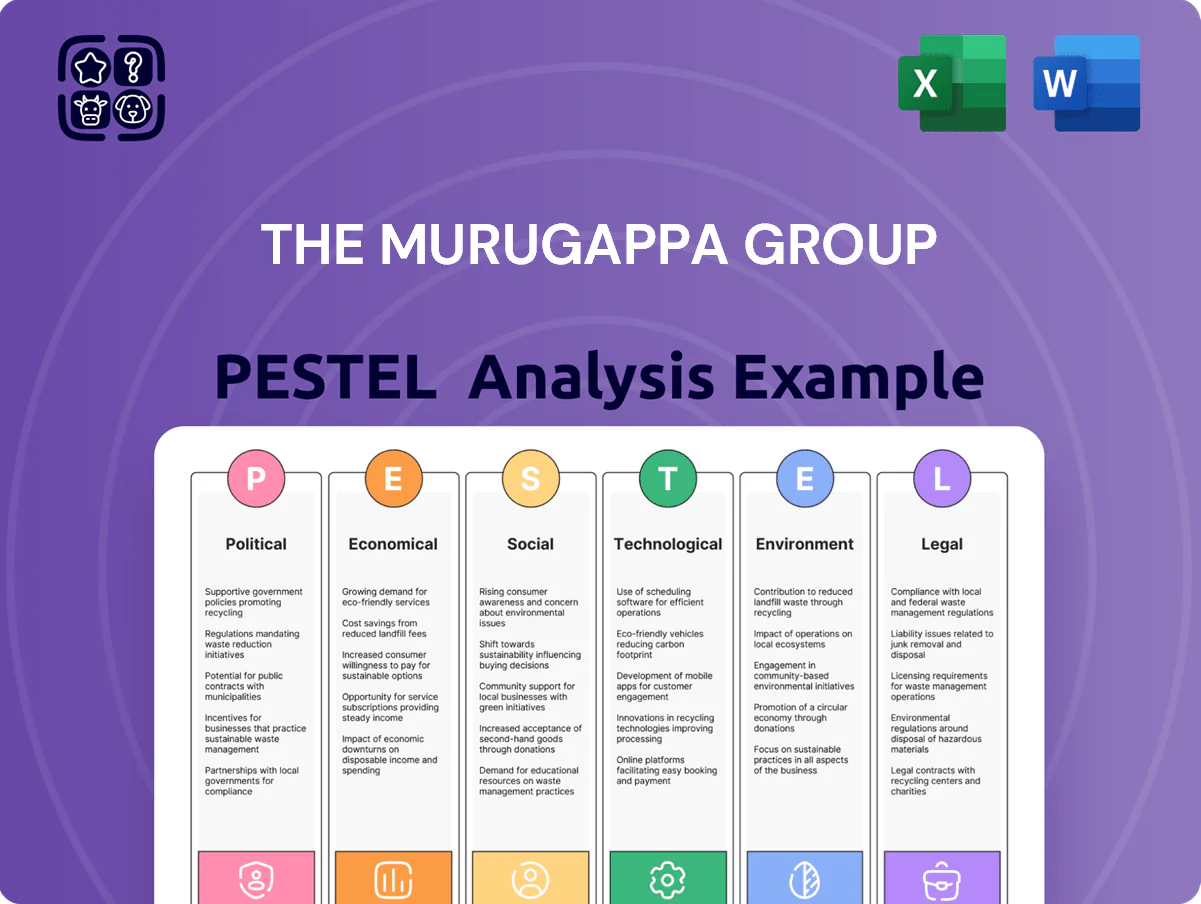

The Murugappa Group PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and technological innovation are reshaping The Murugappa Group’s strategic landscape—our PESTLE Analysis translates these external forces into actionable insights for investors and strategists; purchase the full report to access detailed risk assessments, growth opportunities, and ready-to-use slides and spreadsheets for immediate decision-making.

Political factors

Government Agriculture Policies

The Murugappa Group’s fertilizer and farm-input arms, led by Coromandel International, remain highly exposed to Indian government fertilizer subsidies (₹1.5 trillion FY2024 subsidy bill) and MSP-driven procurement; these policies accounted for c.40% of domestic fertilizer demand support in 2024. Changes in rural schemes or agricultural credit—RBI data shows farm credit growth 11% YoY as of FY2025—would directly affect product uptake. Policy stability through late 2025 has allowed multiyear procurement and capex planning for the primary sector.

Trade Relations and Export Incentives

Murugappa, with ~25% global share in bonded abrasives and substantial industrial ceramics exports, is sensitive to tariffs and FTAs; changes in EU/US tariff lines could shift margins on Rs ~6,500 crore FY24 engineering sales.

India’s RoDTEP, reimbursing duties up to 1.5–3% for eligible engineering exports, improves price competitiveness for Murugappa units like Tube Investments and Carborundum, impacting EBITDA on exported volumes.

Geopolitical tensions (e.g., 2023–24 supply disruptions) and formation of new trade blocs can reroute automotive component supply chains, affecting delivery times and market access in ASEAN and EU, where Murugappa exports ~18% of components.

Infrastructure Spending Mandates

The group’s engineering and metal units gain from India’s elevated infrastructure capex; Union Budget 2024/25 pegged capital expenditure at Rs 11.1 lakh crore, up 11% YoY, boosting demand for pipes, bearings and specialty steels.

Make in India incentives and import substitution policies support Tube Investments of India’s domestic manufacturing, aligning with higher localization and production-linked opportunities across 2024–25.

Future revenue growth hinges on timely execution of the National Infrastructure Pipeline (NIP) projects totaling Rs 111 lakh crore through 2026, which will drive order books and utilization across Murugappa’s engineering portfolio.

Regulatory Stability in Financial Services

Cholamandalam Investment and Finance faces regulatory stability risks as NBFC rules evolve; RBI reported NBFC sector assets at INR 57.1 trillion in FY2023, signalling close oversight that affects capital and provisioning norms.

Political pushes for financial inclusion and digital banking (Pradhan Mantri Jan Dhan accounts >450 million) require product alignment, while shifts on interest caps or loan waivers can widen NPA stress and credit risk.

- RBI NBFC assets INR 57.1T (FY2023)

- PMJDY accounts >450M—digital inclusion pressure

- Interest cap or waiver policy shifts increase NPA/credit risk

Regional Political Dynamics

The Murugappa Group, headquartered in Chennai, must manage state and central politics across India and operations in 20+ countries; in 2024 India manufacturing accounts for over 60% of group revenue (~INR 18,000 crore).

State labor laws and land acquisition rules in Tamil Nadu and Andhra Pradesh affect plant throughput—Tamil Nadu industrial disputes rose 8% in 2023, impacting uptime.

Maintaining strong ties with state administrations ensures steady power, water and faster industrial licensing; delays can add weeks and cost crores.

- Headquartered Chennai; 60%+ revenue from India (~INR 18,000 crore)

- Operations in 20+ countries

- Tamil Nadu industrial disputes +8% in 2023

- Regulatory delays can cost weeks and crores

India policy tailwinds—fertilizer subsidies, capex & NBFC shifts reshape Murugappa growth

Political factors: Murugappa depends on India’s ₹1.5T FY2024 fertilizer subsidies and MSP-linked demand; RBI shows farm credit +11% YoY (FY2025). Engineering exports benefit from RoDTEP (1.5–3%) but face tariff/FTA risks; infrastructure capex (Union Budget 2024/25 capex ₹11.1L crore) and Make in India aid localization; NBFC regulatory shifts (NBFC assets ₹57.1T FY2023) affect Cholamandalam funding.

| Item | Value |

|---|---|

| Fertilizer subsidy | ₹1.5T FY2024 |

| Farm credit growth | +11% FY2025 |

| Union capex | ₹11.1L crore 2024/25 |

| NBFC assets | ₹57.1T FY2023 |

What is included in the product

Explores how macro-environmental factors uniquely affect The Murugappa Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, backed by current trends and region-specific data to identify threats and opportunities for executives and investors.

Condensed PESTLE insights for The Murugappa Group, visually segmented for quick interpretation during meetings and easily dropped into presentations to align teams on external risks and strategic positioning.

Economic factors

Interest Rate Fluctuations

The Murugappa Group’s vehicle finance and home loan margins are highly sensitive to RBI repo rate shifts; a 250bps rise from 2022–24 pushed borrowing costs and compressed NIMs across its finance arm. High-rate periods have cut discretionary durable goods and bicycle demand—industry retail volumes fell ~6% YoY in 2024—while raising capital costs for CapEx in manufacturing. By end-2025, managing a cost-of-funds reduction of even 50–75bps will materially restore profitability in its financial services segment.

Rural Income and Monsoon Dependency

A significant portion of Murugappa Group revenue ties to rural India through fertilizers, pesticides and farm equipment, with Agri revenues estimated at ~18–22% of consolidated sales in FY2024; monsoon-driven cycles thus directly affect purchasing power of core customers. Good monsoons boost input demand—FY2023 rural GDP growth was 3.5% vs urban 2.1%—while weak rains compress farm cashflows and sales. Diversification into non-farm sectors (e.g., cycle and abrasives businesses generating ~45% of group EBITDA in FY2024) cushions volatility, but rural demand remains a primary economic pillar.

Inflation and Raw Material Costs

Fluctuations in global raw material prices—steel up ~18% in 2024 vs 2023, phosphoric acid rising 12–15% in 2023–24, and natural rubber volatile with a 20% swing in 2024—raise production costs for Murugappa’s engineering and fertilizer units.

The group’s ability to pass these costs to consumers without losing market share is critical; Murugappa reported gross margin pressure of ~120–160 bps in FY2024 in commodity-exposed segments.

Strategic sourcing, supplier contracts and backward integration—Cholamandalam’s feedstock initiatives and Carborundum Universal’s vertical moves—are essential to protect margins against ongoing inflationary commodity cycles.

Currency Exchange Rate Volatility

The Murugappa Group’s international operations and raw-material imports expose it to INR volatility against USD and EUR; INR moved ~4% stronger vs USD in 2024 but showed 6% intra-year swings in 2025, impacting costs.

Export-focused abrasives and ceramics gain from a weaker rupee—export revenue for Carborundum Universal rose ~12% in FY2024—while fertilizers face higher import bills for phosphate and potash.

Hedging and currency risk management—forward contracts and natural hedges—are vital to preserve margins; the group reported using forex derivatives covering ~40% of estimated 2025 net exposure.

- INR volatility: ~6% swing in 2025

- Abrasives exports: +12% revenue FY2024

- Derivatives cover: ~40% of 2025 exposure

- Fertilizer import costs: up with weaker rupee

GDP Growth and Industrial Production

GDP growth of 7.3% in FY2024 and IIP rising 4.6% YoY in Dec 2025 signal stronger demand for Murugappa’s engineering and automotive units, boosting orders for industrial consumables and precision tubes.

The group’s revenue and margin trajectory closely track India’s capex cycle, with industrial capex up 12% YoY in 2024 supporting higher utilization and pricing power.

- GDP FY2024: 7.3%

- IIP Dec 2025: +4.6% YoY

- Industrial capex 2024: +12% YoY

Murugappa: Rate, commodity and INR swings vs. rural demand shape volumes & margins

Economic drivers for Murugappa include RBI rate-driven NIM pressure (repo +250bps 2022–24), rural demand volatility (agri ~20% of sales FY2024), commodity cost swings (steel +18% 2024; phosphoric acid +12–15% 2023–24), INR swings (~6% 2025) and strong domestic capex/GDP (GDP 7.3% FY2024; IIP +4.6% Dec 2025) affecting volumes and margins.

| Metric | Value |

|---|---|

| Repo shift 2022–24 | +250bps |

| Agriculture share | ~18–22% sales FY2024 |

| Steel change 2024 | +18% |

| INR volatility 2025 | ~6% swing |

| GDP FY2024 | 7.3% |

Same Document Delivered

The Murugappa Group PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; it contains the complete PESTLE analysis for The Murugappa Group with all sections, insights, and formatting intact.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and technological innovation are reshaping The Murugappa Group’s strategic landscape—our PESTLE Analysis translates these external forces into actionable insights for investors and strategists; purchase the full report to access detailed risk assessments, growth opportunities, and ready-to-use slides and spreadsheets for immediate decision-making.

Political factors

Government Agriculture Policies

The Murugappa Group’s fertilizer and farm-input arms, led by Coromandel International, remain highly exposed to Indian government fertilizer subsidies (₹1.5 trillion FY2024 subsidy bill) and MSP-driven procurement; these policies accounted for c.40% of domestic fertilizer demand support in 2024. Changes in rural schemes or agricultural credit—RBI data shows farm credit growth 11% YoY as of FY2025—would directly affect product uptake. Policy stability through late 2025 has allowed multiyear procurement and capex planning for the primary sector.

Trade Relations and Export Incentives

Murugappa, with ~25% global share in bonded abrasives and substantial industrial ceramics exports, is sensitive to tariffs and FTAs; changes in EU/US tariff lines could shift margins on Rs ~6,500 crore FY24 engineering sales.

India’s RoDTEP, reimbursing duties up to 1.5–3% for eligible engineering exports, improves price competitiveness for Murugappa units like Tube Investments and Carborundum, impacting EBITDA on exported volumes.

Geopolitical tensions (e.g., 2023–24 supply disruptions) and formation of new trade blocs can reroute automotive component supply chains, affecting delivery times and market access in ASEAN and EU, where Murugappa exports ~18% of components.

Infrastructure Spending Mandates

The group’s engineering and metal units gain from India’s elevated infrastructure capex; Union Budget 2024/25 pegged capital expenditure at Rs 11.1 lakh crore, up 11% YoY, boosting demand for pipes, bearings and specialty steels.

Make in India incentives and import substitution policies support Tube Investments of India’s domestic manufacturing, aligning with higher localization and production-linked opportunities across 2024–25.

Future revenue growth hinges on timely execution of the National Infrastructure Pipeline (NIP) projects totaling Rs 111 lakh crore through 2026, which will drive order books and utilization across Murugappa’s engineering portfolio.

Regulatory Stability in Financial Services

Cholamandalam Investment and Finance faces regulatory stability risks as NBFC rules evolve; RBI reported NBFC sector assets at INR 57.1 trillion in FY2023, signalling close oversight that affects capital and provisioning norms.

Political pushes for financial inclusion and digital banking (Pradhan Mantri Jan Dhan accounts >450 million) require product alignment, while shifts on interest caps or loan waivers can widen NPA stress and credit risk.

- RBI NBFC assets INR 57.1T (FY2023)

- PMJDY accounts >450M—digital inclusion pressure

- Interest cap or waiver policy shifts increase NPA/credit risk

Regional Political Dynamics

The Murugappa Group, headquartered in Chennai, must manage state and central politics across India and operations in 20+ countries; in 2024 India manufacturing accounts for over 60% of group revenue (~INR 18,000 crore).

State labor laws and land acquisition rules in Tamil Nadu and Andhra Pradesh affect plant throughput—Tamil Nadu industrial disputes rose 8% in 2023, impacting uptime.

Maintaining strong ties with state administrations ensures steady power, water and faster industrial licensing; delays can add weeks and cost crores.

- Headquartered Chennai; 60%+ revenue from India (~INR 18,000 crore)

- Operations in 20+ countries

- Tamil Nadu industrial disputes +8% in 2023

- Regulatory delays can cost weeks and crores

India policy tailwinds—fertilizer subsidies, capex & NBFC shifts reshape Murugappa growth

Political factors: Murugappa depends on India’s ₹1.5T FY2024 fertilizer subsidies and MSP-linked demand; RBI shows farm credit +11% YoY (FY2025). Engineering exports benefit from RoDTEP (1.5–3%) but face tariff/FTA risks; infrastructure capex (Union Budget 2024/25 capex ₹11.1L crore) and Make in India aid localization; NBFC regulatory shifts (NBFC assets ₹57.1T FY2023) affect Cholamandalam funding.

| Item | Value |

|---|---|

| Fertilizer subsidy | ₹1.5T FY2024 |

| Farm credit growth | +11% FY2025 |

| Union capex | ₹11.1L crore 2024/25 |

| NBFC assets | ₹57.1T FY2023 |

What is included in the product

Explores how macro-environmental factors uniquely affect The Murugappa Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, backed by current trends and region-specific data to identify threats and opportunities for executives and investors.

Condensed PESTLE insights for The Murugappa Group, visually segmented for quick interpretation during meetings and easily dropped into presentations to align teams on external risks and strategic positioning.

Economic factors

Interest Rate Fluctuations

The Murugappa Group’s vehicle finance and home loan margins are highly sensitive to RBI repo rate shifts; a 250bps rise from 2022–24 pushed borrowing costs and compressed NIMs across its finance arm. High-rate periods have cut discretionary durable goods and bicycle demand—industry retail volumes fell ~6% YoY in 2024—while raising capital costs for CapEx in manufacturing. By end-2025, managing a cost-of-funds reduction of even 50–75bps will materially restore profitability in its financial services segment.

Rural Income and Monsoon Dependency

A significant portion of Murugappa Group revenue ties to rural India through fertilizers, pesticides and farm equipment, with Agri revenues estimated at ~18–22% of consolidated sales in FY2024; monsoon-driven cycles thus directly affect purchasing power of core customers. Good monsoons boost input demand—FY2023 rural GDP growth was 3.5% vs urban 2.1%—while weak rains compress farm cashflows and sales. Diversification into non-farm sectors (e.g., cycle and abrasives businesses generating ~45% of group EBITDA in FY2024) cushions volatility, but rural demand remains a primary economic pillar.

Inflation and Raw Material Costs

Fluctuations in global raw material prices—steel up ~18% in 2024 vs 2023, phosphoric acid rising 12–15% in 2023–24, and natural rubber volatile with a 20% swing in 2024—raise production costs for Murugappa’s engineering and fertilizer units.

The group’s ability to pass these costs to consumers without losing market share is critical; Murugappa reported gross margin pressure of ~120–160 bps in FY2024 in commodity-exposed segments.

Strategic sourcing, supplier contracts and backward integration—Cholamandalam’s feedstock initiatives and Carborundum Universal’s vertical moves—are essential to protect margins against ongoing inflationary commodity cycles.

Currency Exchange Rate Volatility

The Murugappa Group’s international operations and raw-material imports expose it to INR volatility against USD and EUR; INR moved ~4% stronger vs USD in 2024 but showed 6% intra-year swings in 2025, impacting costs.

Export-focused abrasives and ceramics gain from a weaker rupee—export revenue for Carborundum Universal rose ~12% in FY2024—while fertilizers face higher import bills for phosphate and potash.

Hedging and currency risk management—forward contracts and natural hedges—are vital to preserve margins; the group reported using forex derivatives covering ~40% of estimated 2025 net exposure.

- INR volatility: ~6% swing in 2025

- Abrasives exports: +12% revenue FY2024

- Derivatives cover: ~40% of 2025 exposure

- Fertilizer import costs: up with weaker rupee

GDP Growth and Industrial Production

GDP growth of 7.3% in FY2024 and IIP rising 4.6% YoY in Dec 2025 signal stronger demand for Murugappa’s engineering and automotive units, boosting orders for industrial consumables and precision tubes.

The group’s revenue and margin trajectory closely track India’s capex cycle, with industrial capex up 12% YoY in 2024 supporting higher utilization and pricing power.

- GDP FY2024: 7.3%

- IIP Dec 2025: +4.6% YoY

- Industrial capex 2024: +12% YoY

Murugappa: Rate, commodity and INR swings vs. rural demand shape volumes & margins

Economic drivers for Murugappa include RBI rate-driven NIM pressure (repo +250bps 2022–24), rural demand volatility (agri ~20% of sales FY2024), commodity cost swings (steel +18% 2024; phosphoric acid +12–15% 2023–24), INR swings (~6% 2025) and strong domestic capex/GDP (GDP 7.3% FY2024; IIP +4.6% Dec 2025) affecting volumes and margins.

| Metric | Value |

|---|---|

| Repo shift 2022–24 | +250bps |

| Agriculture share | ~18–22% sales FY2024 |

| Steel change 2024 | +18% |

| INR volatility 2025 | ~6% swing |

| GDP FY2024 | 7.3% |

Same Document Delivered

The Murugappa Group PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; it contains the complete PESTLE analysis for The Murugappa Group with all sections, insights, and formatting intact.