Muyuan Foodstuff Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

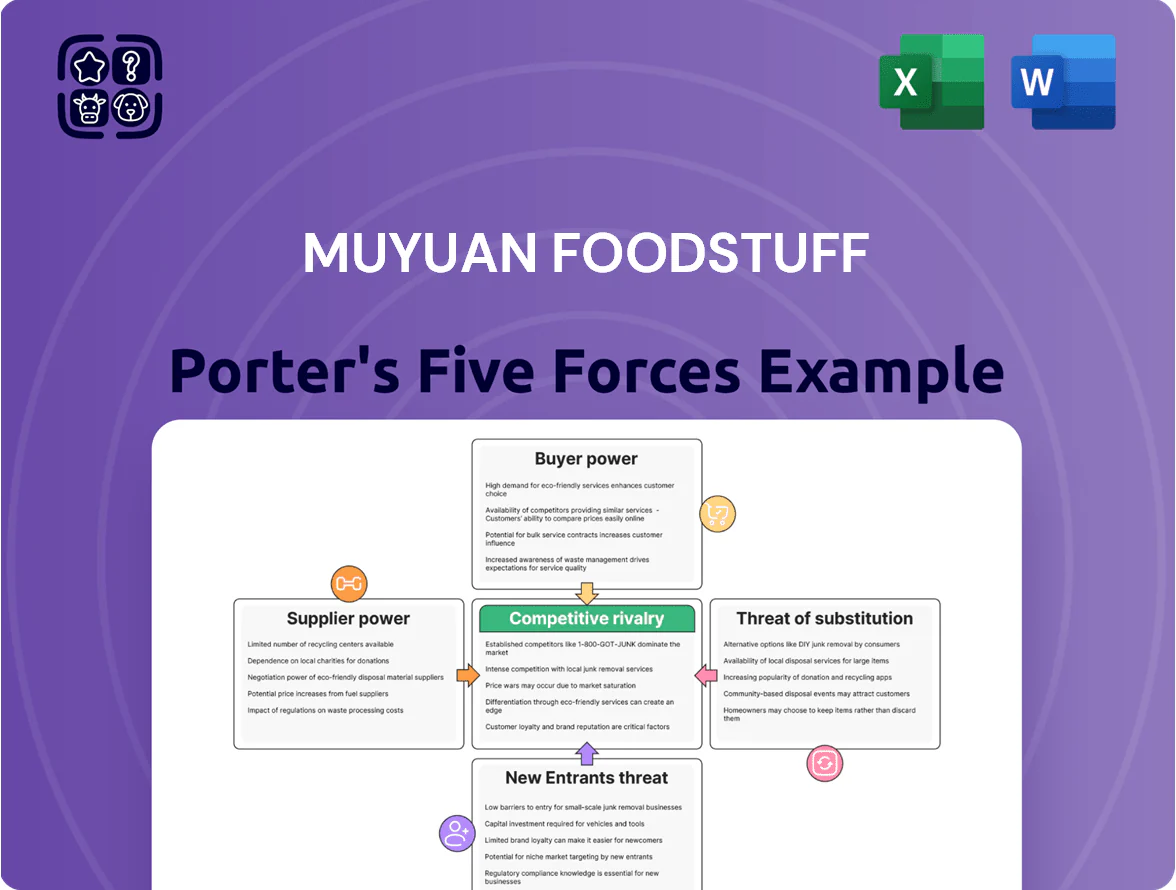

Muyuan Foodstuff faces intense competitive rivalry and significant buyer power amid price-sensitive markets, while supplier influence and substitute threats remain moderate due to scale advantages and product differentiation.

Suppliers Bargaining Power

Volatility of Feed Ingredient Markets

Muyuan’s primary inputs—corn and soybean meal—track global commodity swings; CBOT corn futures rose 18% in 2024 and soymeal 12%, forcing raw-material cost pressure.

Despite large volumes, Muyuan is a price taker in international grain markets; China imported 30% of soybeans in 2024, limiting negotiating power.

By end-2025, stability hinges on US, Brazil harvests and trade policy; a 5% yield shock could raise feed costs ~3–4% and cut margins.

Sophisticated hedging—futures, options, forward contracts—will be needed to protect margins; Muyuan reported limited disclosed hedge ratios in 2024.

Specialized Breeding Technology and Genetics

Muyuan depends on elite genetic stock and specialized equipment to sustain >25% herd productivity gains reported in 2024, giving suppliers of breeding tech and automated feeders moderate bargaining power due to strict specs for large-scale farms.

Advanced veterinary med suppliers also hold moderate leverage, but Muyuan’s R&D—21% of capex in 2023–24 on breeding/genetics—cuts long-term reliance on external breeders.

That vertical integration boosts Muyuan’s negotiating strength versus smaller rivals, lowering input cost volatility and supplier switching risk.

Energy and Utility Requirements

Large-scale hog farming needs steady power for climate control, waste treatment, and automation; Muyuan used ~0.9 kWh per piglet production cycle in 2024, so energy is material to margins.

China’s utilities are often state-owned or regional monopolies, limiting price negotiation; industrial electricity prices rose ~6% YoY in 2024 in Henan province.

By late 2025, greener-energy mandates and grid fees add regulatory cost pressure; on-site biogas and solar—Muyuan reported 120 MWth biogas capacity projects in 2023—are key to cut exposure.

Logistics and Cold Chain Infrastructure

The shift to chilled-meat distribution raises reliance on specialized cold-chain logistics; Muyuan’s own fleet covers routine routes, but end-2025 production of ~9.2 million hogs equivalent requires third-party refrigerated capacity for urban delivery.

Third-party cold-chain suppliers hold moderate bargaining power due to strong industry-wide demand; capacity tightness and disruptions (e.g., 2024 national cold-chain utilization ~78%) can directly delay deliveries and increase spoilage risk.

- End-2025 output ~9.2M hogs eq.

- Own fleet covers routine routes, not peak capacity.

- Cold-chain utilization ~78% (2024).

- Supplier power: moderate — disruption raises spoilage/delivery risk.

Land Availability and Government Leasing

Access to land for Muyuan’s large-scale hog hotels and integrated facilities is effectively controlled by local and provincial governments, making the state the primary supplier of the key expansion resource.

Competitive bidding, strict environmental zoning and waste-disposal permits give land authorities strong leverage over project timelines and capex; delays raise costs and push up required returns.

By 2025, suitable land within 200 km of major consumption hubs fell below demand, increasing regional authorities’ bargaining power and raising site acquisition premiums by an estimated 15–25% in key provinces.

- State controls land supply

- Competitive bids raise capex

- Environmental zoning delays projects

- 2025: site premium +15–25% near hubs

Moderate supplier power: feed prices up, Muyuan's vertical integration cushions risk

Suppliers hold moderate bargaining power: commodity feed (corn/soymeal) is price-taking and lifted input costs (CBOT corn +18% in 2024; soymeal +12%), while proprietary genetics, vet meds, cold‑chain and land (state-controlled) add pockets of leverage; Muyuan’s vertical integration, 21% capex to breeding (2023–24), 120 MWth biogas (2023) and own fleet cut some supplier risk.

| Item | 2024–25 |

|---|---|

| CBOT corn | +18% |

| Soymeal | +12% |

| Hog output | 9.2M eq (end‑2025) |

| Breeding capex | 21% of capex |

What is included in the product

Tailored Porter's Five Forces analysis for Muyuan Foodstuff that uncovers competitive drivers, supplier and buyer power, entry barriers, substitute threats, and strategic implications to inform investor materials, strategy decks, and academic projects.

One-sheet Porter’s Five Forces for Muyuan Foodstuff—instantly highlights supplier, buyer, rivalry, entrant, and substitute pressures for faster, board-ready decisions.

Customers Bargaining Power

Concentration of Large Retail and E-commerce Platforms

Major supermarket chains and platforms like Meituan and JD.com buy huge volumes from Muyuan and push for price cuts; in 2024 Meituan Grocery and JD Retail together accounted for over 45% of online fresh-food sales, concentrating buyer power. These channels link directly to China’s urban middle class, so Muyuan accepts tighter margins to secure scale while protecting branded SKUs. By 2025, digitized grocery shopping grew to ~62% penetration in tier‑1/2 cities, further consolidating distributor leverage.

Low Switching Costs for Wholesale Buyers

Wholesale buyers face low switching costs and routinely shift suppliers for price/availability; pork trades as a commodity so B2B brand loyalty is weak. Muyuan (Muyuan Foodstuff, listed 2014) stresses biosecurity and steady quality—its 2024 pig slaughter capacity ~11.5 million head/year—to retain contracts. Still, 2024–25 China pork surplus pushed spot prices down ~28% year-over-year, letting buyers squeeze margins sharply.

Price Sensitivity of Individual Consumers

Pork is still the main protein for Chinese households, so price moves hit demand hard; a 2024 NBS survey showed pork accounted for ~41% of per-capita meat consumption, making spikes politically and socially sensitive.

Consumers shift fast to chicken or plant proteins when pork rises; retail elasticity estimates ~-0.6 to -0.9 imply meaningful volume loss on price hikes, capping Muyuan’s pass-through of higher feed or disease costs.

By late 2025, price-comparison apps reached ~320 million users, raising price transparency and shortening reaction time, further constraining Muyuan’s pricing power.

Impact of Government Reserve Management

The Chinese government functions as a major 'customer' via its strategic pork reserve, which in 2024 released about 1.05 million tonnes of pork to the market and in 2025 continued active management to cap retail prices near targets set by the National Food and Strategic Reserves Administration.

These interventions set de facto price ceilings and floors, forcing Muyuan to accept narrower spreads and reducing its bargaining power, especially during 2024–2025 inflation spikes when reserve purchases limited upside pricing.

Muyuan must align sales and inventory timing with national food security goals, often prioritizing supply stability over margin maximization, which constrains its customer-side leverage.

Demand for Traceability and Food Safety

Modern consumers and high-end restaurants demand full transparency on meat origin and safety, shifting power toward buyers but also creating leverage for Muyuan, whose integrated model offers stronger traceability than fragmented small farms.

Customers pay a slight premium—industry reports show 3–7% higher prices for certified disease-free/antibiotic-free pork—and Muyuan’s digital tracking investments by 2025 support maintaining those premium tiers.

Digital traceability has cut recall-related losses by an estimated 15% and is used as a negotiation tool in supply contracts.

- Integrated model = better traceability vs small farms

- Premium paid: 3–7% for certified pork

- 2025 digital tracking key to pricing

- Recall loss reduction ~15%

Platform power squeezes pork margins as digitized grocery and reserves cap upside

Buyers hold strong leverage: Meituan+JD accounted for >45% of online fresh-food sales in 2024 and digitized grocery reached ~62% penetration in tier‑1/2 cities by 2025, enabling rapid price pressure; wholesale switching costs are low and pork is a commodity, so Muyuan accepts tighter margins despite 2024 slaughter capacity ~11.5M head. Government reserve releases (~1.05M tonnes in 2024) cap upside, while traceability and certified SKUs earn 3–7% premiums and reduce recall losses ~15%.

| Metric | Value |

|---|---|

| Meituan+JD share (2024) | >45% |

| Digitized grocery (tier‑1/2, 2025) | ~62% |

| Muyuan slaughter capacity (2024) | ~11.5M head/yr |

| Govt reserve release (2024) | ~1.05M tonnes |

| Certified pork premium | 3–7% |

| Recall loss reduction | ~15% |

Same Document Delivered

Muyuan Foodstuff Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Muyuan Foodstuff you'll receive immediately after purchase—no placeholders or mockups.

The document displayed is the professionally formatted, ready-to-use file that becomes available for instant download once you complete your purchase.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Muyuan Foodstuff faces intense competitive rivalry and significant buyer power amid price-sensitive markets, while supplier influence and substitute threats remain moderate due to scale advantages and product differentiation.

Suppliers Bargaining Power

Volatility of Feed Ingredient Markets

Muyuan’s primary inputs—corn and soybean meal—track global commodity swings; CBOT corn futures rose 18% in 2024 and soymeal 12%, forcing raw-material cost pressure.

Despite large volumes, Muyuan is a price taker in international grain markets; China imported 30% of soybeans in 2024, limiting negotiating power.

By end-2025, stability hinges on US, Brazil harvests and trade policy; a 5% yield shock could raise feed costs ~3–4% and cut margins.

Sophisticated hedging—futures, options, forward contracts—will be needed to protect margins; Muyuan reported limited disclosed hedge ratios in 2024.

Specialized Breeding Technology and Genetics

Muyuan depends on elite genetic stock and specialized equipment to sustain >25% herd productivity gains reported in 2024, giving suppliers of breeding tech and automated feeders moderate bargaining power due to strict specs for large-scale farms.

Advanced veterinary med suppliers also hold moderate leverage, but Muyuan’s R&D—21% of capex in 2023–24 on breeding/genetics—cuts long-term reliance on external breeders.

That vertical integration boosts Muyuan’s negotiating strength versus smaller rivals, lowering input cost volatility and supplier switching risk.

Energy and Utility Requirements

Large-scale hog farming needs steady power for climate control, waste treatment, and automation; Muyuan used ~0.9 kWh per piglet production cycle in 2024, so energy is material to margins.

China’s utilities are often state-owned or regional monopolies, limiting price negotiation; industrial electricity prices rose ~6% YoY in 2024 in Henan province.

By late 2025, greener-energy mandates and grid fees add regulatory cost pressure; on-site biogas and solar—Muyuan reported 120 MWth biogas capacity projects in 2023—are key to cut exposure.

Logistics and Cold Chain Infrastructure

The shift to chilled-meat distribution raises reliance on specialized cold-chain logistics; Muyuan’s own fleet covers routine routes, but end-2025 production of ~9.2 million hogs equivalent requires third-party refrigerated capacity for urban delivery.

Third-party cold-chain suppliers hold moderate bargaining power due to strong industry-wide demand; capacity tightness and disruptions (e.g., 2024 national cold-chain utilization ~78%) can directly delay deliveries and increase spoilage risk.

- End-2025 output ~9.2M hogs eq.

- Own fleet covers routine routes, not peak capacity.

- Cold-chain utilization ~78% (2024).

- Supplier power: moderate — disruption raises spoilage/delivery risk.

Land Availability and Government Leasing

Access to land for Muyuan’s large-scale hog hotels and integrated facilities is effectively controlled by local and provincial governments, making the state the primary supplier of the key expansion resource.

Competitive bidding, strict environmental zoning and waste-disposal permits give land authorities strong leverage over project timelines and capex; delays raise costs and push up required returns.

By 2025, suitable land within 200 km of major consumption hubs fell below demand, increasing regional authorities’ bargaining power and raising site acquisition premiums by an estimated 15–25% in key provinces.

- State controls land supply

- Competitive bids raise capex

- Environmental zoning delays projects

- 2025: site premium +15–25% near hubs

Moderate supplier power: feed prices up, Muyuan's vertical integration cushions risk

Suppliers hold moderate bargaining power: commodity feed (corn/soymeal) is price-taking and lifted input costs (CBOT corn +18% in 2024; soymeal +12%), while proprietary genetics, vet meds, cold‑chain and land (state-controlled) add pockets of leverage; Muyuan’s vertical integration, 21% capex to breeding (2023–24), 120 MWth biogas (2023) and own fleet cut some supplier risk.

| Item | 2024–25 |

|---|---|

| CBOT corn | +18% |

| Soymeal | +12% |

| Hog output | 9.2M eq (end‑2025) |

| Breeding capex | 21% of capex |

What is included in the product

Tailored Porter's Five Forces analysis for Muyuan Foodstuff that uncovers competitive drivers, supplier and buyer power, entry barriers, substitute threats, and strategic implications to inform investor materials, strategy decks, and academic projects.

One-sheet Porter’s Five Forces for Muyuan Foodstuff—instantly highlights supplier, buyer, rivalry, entrant, and substitute pressures for faster, board-ready decisions.

Customers Bargaining Power

Concentration of Large Retail and E-commerce Platforms

Major supermarket chains and platforms like Meituan and JD.com buy huge volumes from Muyuan and push for price cuts; in 2024 Meituan Grocery and JD Retail together accounted for over 45% of online fresh-food sales, concentrating buyer power. These channels link directly to China’s urban middle class, so Muyuan accepts tighter margins to secure scale while protecting branded SKUs. By 2025, digitized grocery shopping grew to ~62% penetration in tier‑1/2 cities, further consolidating distributor leverage.

Low Switching Costs for Wholesale Buyers

Wholesale buyers face low switching costs and routinely shift suppliers for price/availability; pork trades as a commodity so B2B brand loyalty is weak. Muyuan (Muyuan Foodstuff, listed 2014) stresses biosecurity and steady quality—its 2024 pig slaughter capacity ~11.5 million head/year—to retain contracts. Still, 2024–25 China pork surplus pushed spot prices down ~28% year-over-year, letting buyers squeeze margins sharply.

Price Sensitivity of Individual Consumers

Pork is still the main protein for Chinese households, so price moves hit demand hard; a 2024 NBS survey showed pork accounted for ~41% of per-capita meat consumption, making spikes politically and socially sensitive.

Consumers shift fast to chicken or plant proteins when pork rises; retail elasticity estimates ~-0.6 to -0.9 imply meaningful volume loss on price hikes, capping Muyuan’s pass-through of higher feed or disease costs.

By late 2025, price-comparison apps reached ~320 million users, raising price transparency and shortening reaction time, further constraining Muyuan’s pricing power.

Impact of Government Reserve Management

The Chinese government functions as a major 'customer' via its strategic pork reserve, which in 2024 released about 1.05 million tonnes of pork to the market and in 2025 continued active management to cap retail prices near targets set by the National Food and Strategic Reserves Administration.

These interventions set de facto price ceilings and floors, forcing Muyuan to accept narrower spreads and reducing its bargaining power, especially during 2024–2025 inflation spikes when reserve purchases limited upside pricing.

Muyuan must align sales and inventory timing with national food security goals, often prioritizing supply stability over margin maximization, which constrains its customer-side leverage.

Demand for Traceability and Food Safety

Modern consumers and high-end restaurants demand full transparency on meat origin and safety, shifting power toward buyers but also creating leverage for Muyuan, whose integrated model offers stronger traceability than fragmented small farms.

Customers pay a slight premium—industry reports show 3–7% higher prices for certified disease-free/antibiotic-free pork—and Muyuan’s digital tracking investments by 2025 support maintaining those premium tiers.

Digital traceability has cut recall-related losses by an estimated 15% and is used as a negotiation tool in supply contracts.

- Integrated model = better traceability vs small farms

- Premium paid: 3–7% for certified pork

- 2025 digital tracking key to pricing

- Recall loss reduction ~15%

Platform power squeezes pork margins as digitized grocery and reserves cap upside

Buyers hold strong leverage: Meituan+JD accounted for >45% of online fresh-food sales in 2024 and digitized grocery reached ~62% penetration in tier‑1/2 cities by 2025, enabling rapid price pressure; wholesale switching costs are low and pork is a commodity, so Muyuan accepts tighter margins despite 2024 slaughter capacity ~11.5M head. Government reserve releases (~1.05M tonnes in 2024) cap upside, while traceability and certified SKUs earn 3–7% premiums and reduce recall losses ~15%.

| Metric | Value |

|---|---|

| Meituan+JD share (2024) | >45% |

| Digitized grocery (tier‑1/2, 2025) | ~62% |

| Muyuan slaughter capacity (2024) | ~11.5M head/yr |

| Govt reserve release (2024) | ~1.05M tonnes |

| Certified pork premium | 3–7% |

| Recall loss reduction | ~15% |

Same Document Delivered

Muyuan Foodstuff Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Muyuan Foodstuff you'll receive immediately after purchase—no placeholders or mockups.

The document displayed is the professionally formatted, ready-to-use file that becomes available for instant download once you complete your purchase.