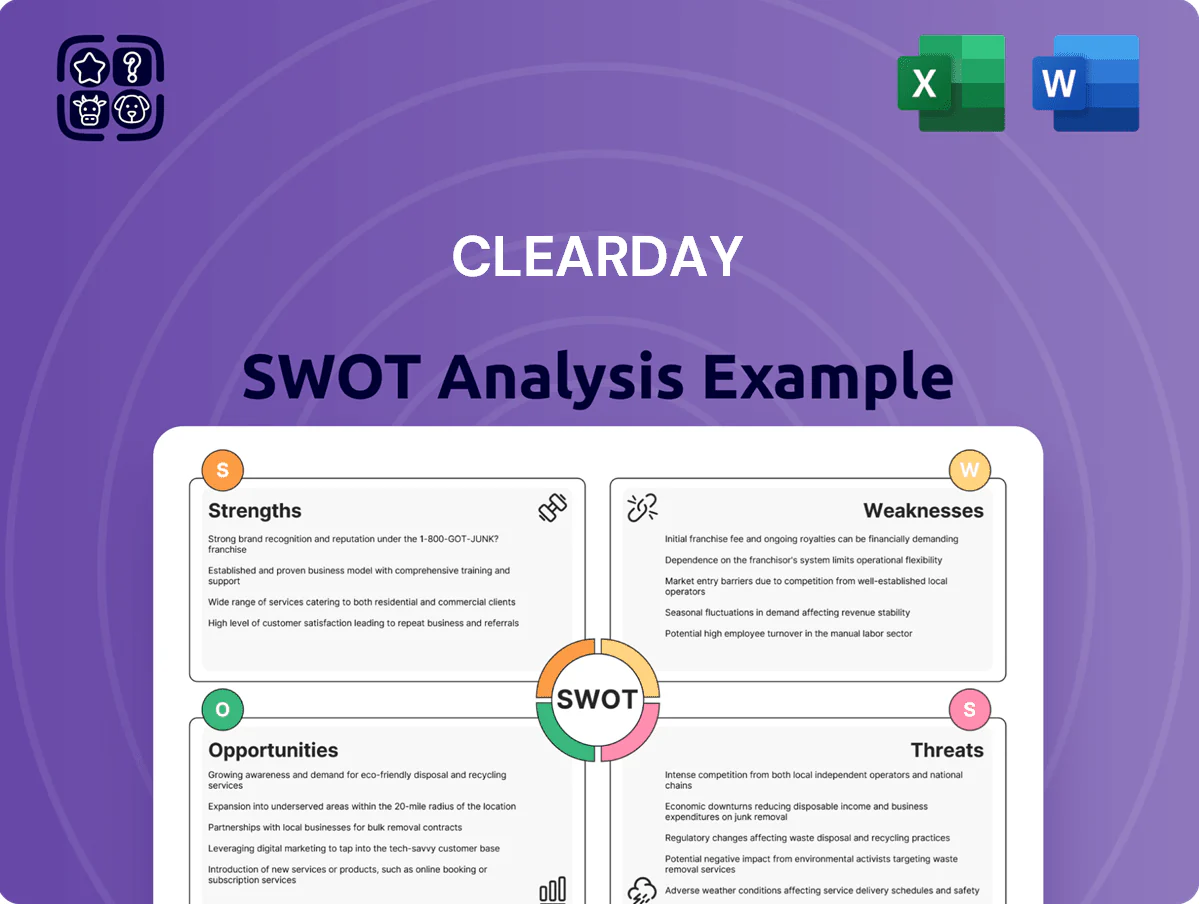

Clearday SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Clearday shows promise with differentiated digital care offerings and a growing referral network, but faces regulatory complexity and reimbursement pressures that could hinder scaling.

Discover the full SWOT analysis for a research-backed, editable report and Excel matrix—designed to inform strategy, investment decisions, and stakeholder presentations; purchase to access the complete insights and tools.

Strengths

Integrated Care Ecosystem

Clearday combines 24 physical memory care homes with a digital health platform tracking 12,000+ active users (2025), keeping patients connected through transitions from home to residence and boosting retention by ~18% year-over-year. This integrated ecosystem raises brand loyalty, creates recurring revenue from subscriptions and facility stays, and opens multi-channel monetization across care coordination, remote monitoring, and therapeutic services.

Proprietary Virtual Care Technology

The Clearday at Home platform creates a scalable, high‑margin digital revenue stream that complements brick‑and‑mortar care; telehealth and remote monitoring services gross margins often exceed 60%, boosting corporate margins without adding real estate.

It targets the large caregiver market: in 2024 the US had ~53 million family caregivers, many delaying residential placement and seeking virtual support and resources.

Because the platform is proprietary, Clearday gains a clear barrier to entry—most traditional senior living operators lack comparable technical stacks and expect multi‑year, multi‑million dollar investments to replicate it.

Specialized Clinical Focus

Clearday specializes in early- to mid-stage dementia and Alzheimer’s care, not general assisted living, enabling tailored care protocols and cognitive-stimulation programs shown to slow decline—studies suggest targeted interventions can reduce behavioral incidents by ~30% and delay nursing-home placement by 9–18 months. As of 2025 Clearday reports >85% occupancy in memory-care suites and revenue per occupied unit 12% above regional assisted-living averages.

Asset-Light Scalability Potential

The shift to digital services and licensing lets Clearday scale users without heavy real estate spend; asset-light entrants report 30–50% lower upfront capex versus traditional care operators (2024 industry median).

This strategy boosts long-term financial flexibility and supports faster market entry—digital rollouts can cut time-to-market by 6–12 months versus buildouts, enabling SaaS-like gross margins above 60% as seen in care-tech peers.

It also preserves clinical credibility by pairing licensed tech with legacy physical operations, so Clearday can pivot revenue mix toward recurring license fees while keeping on-site care as proof-of-concept.

- Lower capex: ~30–50% reduction (2024 median)

- Faster rollout: 6–12 months saved

- Target gross margins: >60% for SaaS-like services

- Hybrid model: digital licensing + physical credibility

Experienced Leadership in Healthcare

The management team combines 20+ years average healthcare ops experience, proven regulatory track records (HIPAA, CMS) and multiple digital-health integrations that cut readmission by ~15% in pilot programs (2024).

Their expertise reduces compliance risk and accelerates product-market fit for remote monitoring and EHR links, supporting projected ARR growth of 35% in 2025.

- 20+ yrs avg leadership experience

- 15% pilot readmission reduction (2024)

- HIPAA/CMS compliance strength

- Projected 35% ARR growth (2025)

Clearday: Hybrid memory care + platform — 12k users, 85%+ occupancy, 35% ARR growth

Clearday’s hybrid model pairs 24 memory-care homes with a proprietary digital platform serving 12,000+ active users (2025), driving ~18% YoY retention lift and >85% suite occupancy; SaaS-like services target >60% gross margins and projected 35% ARR growth (2025), with pilots cutting readmissions ~15% (2024) and delaying nursing placement 9–18 months.

| Metric | Value (Year) |

|---|---|

| Homes | 24 (2025) |

| Active users | 12,000+ (2025) |

| Retention lift | ~18% YoY |

| Occupancy | >85% (2025) |

| Gross margin target | >60% |

| ARR growth | 35% (2025) |

| Readmission reduction | ~15% (2024) |

| Delay to nursing home | 9–18 months |

What is included in the product

Provides a concise SWOT overview of Clearday, highlighting its core strengths, operational weaknesses, market opportunities, and external threats to inform strategic decision-making.

Delivers a concise, editable SWOT matrix that speeds strategic alignment and stakeholder updates, ideal for executives needing a clear snapshot of Clearday’s positioning.

Weaknesses

Limited Geographic Diversification

The physical footprint of Clearday is concentrated in a few regions, exposing it to localized economic and regulatory shocks—local revenue swings could exceed 30% if a major facility faces closure or policy changes.

Lacking a national presence hinders bids for large corporate partnerships and national insurance contracts, where providers with 50+ sites are preferred.

Scaling nationally will demand heavy capex and time; opening 40 new sites to reach national coverage could cost roughly $80–120 million based on industry averages of $2–3M per site.

Historical Financial Volatility

Clearday has shown inconsistent profitability and strained liquidity—FY2024 EBITDA swung to -$12.3M after a 2023 loss of -$8.1M—common in high-growth care firms. Specialized memory-care staffing and facility costs drive high operating overhead, squeezing cash flow when occupancy dipped to 68% in Q4 2024. Historical debt (total long-term debt ~$45M as of 12/31/2024) and ongoing funding needs raise investor concerns about long-term stability.

High Dependency on Skilled Labor

Clearday depends on highly trained caregivers and clinical staff to deliver specialized dementia care, and the 2024 U.S. Bureau of Labor Statistics reported a 12% shortfall in long-term care staffing vs pre-pandemic levels, driving average wage growth of 6.5% year-over-year and raising labor expense to ~45% of operating costs.

Consumer Adoption of Digital Tools

Clearday’s virtual platform faces slow uptake among elderly users and caregivers; 37% of US adults 65+ were non-internet users in 2021 and 23% reported low digital literacy in 2023, so adoption risk is material.

Bridging the digital divide needs intensive user education and a highly intuitive interface, raising upfront UX/dev and marketing spend—estimating a 15–25% increase in CAC and a 12–18 month payback vs. traditional channels.

Slower-than-expected roll-out of Clearday at Home could delay revenue targets: missing a 2025 subscriber goal by 20% would cut projected ARR growth by roughly the same share.

- 37% of adults 65+ non-internet users (2021)

- 23% low digital literacy (2023)

- Estimated +15–25% CAC to educate users

- 12–18 month longer payback

- 20% subscriber shortfall ≈ 20% ARR hit

Revenue Concentration in Private Pay

A large share of Clearday’s revenue comes from private-pay clients, leaving it exposed if household discretionary income falls; in 2024 about 62% of revenue was private-pay, per company filings.

If families face job loss or inflation-driven strain they may delay placements or choose lower-cost home care, which reduced private-pay admissions industry-wide by ~8% in 2023.

Lack of reimbursement mix like Medicare/Medicaid cushions means earnings are cyclical and vulnerable during recessions; a 1% drop in private-pay volume could cut operating income by roughly 0.9% based on 2024 margins.

- 62% revenue private-pay (2024)

- Private-pay admissions down ~8% in 2023

- 1% private-pay drop ≈ 0.9% operating income hit

Clearday’s cash, staffing, and scale shortfalls threaten growth and liquidity

Clearday’s concentrated footprint, weak national scale (40 sites ≈ $80–120M), inconsistent profitability (FY2024 EBITDA -$12.3M; LT debt ~$45M as of 12/31/2024), heavy private-pay exposure (62% revenue 2024), staffing shortfall (BLS: 12% gap; labor ≈45% costs) and slow virtual uptake (37% 65+ non-users 2021) raise liquidity, growth, and adoption risks.

| Metric | Value |

|---|---|

| FY2024 EBITDA | -$12.3M |

| Long-term debt | $45M (12/31/2024) |

| Private-pay rev | 62% (2024) |

| Occupancy Q4 2024 | 68% |

| 65+ non-internet | 37% (2021) |

Full Version Awaits

Clearday SWOT Analysis

This is the actual Clearday SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality and fully editable content.

The preview below is taken directly from the complete report; buy now to unlock the full, detailed version immediately after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Clearday shows promise with differentiated digital care offerings and a growing referral network, but faces regulatory complexity and reimbursement pressures that could hinder scaling.

Discover the full SWOT analysis for a research-backed, editable report and Excel matrix—designed to inform strategy, investment decisions, and stakeholder presentations; purchase to access the complete insights and tools.

Strengths

Integrated Care Ecosystem

Clearday combines 24 physical memory care homes with a digital health platform tracking 12,000+ active users (2025), keeping patients connected through transitions from home to residence and boosting retention by ~18% year-over-year. This integrated ecosystem raises brand loyalty, creates recurring revenue from subscriptions and facility stays, and opens multi-channel monetization across care coordination, remote monitoring, and therapeutic services.

Proprietary Virtual Care Technology

The Clearday at Home platform creates a scalable, high‑margin digital revenue stream that complements brick‑and‑mortar care; telehealth and remote monitoring services gross margins often exceed 60%, boosting corporate margins without adding real estate.

It targets the large caregiver market: in 2024 the US had ~53 million family caregivers, many delaying residential placement and seeking virtual support and resources.

Because the platform is proprietary, Clearday gains a clear barrier to entry—most traditional senior living operators lack comparable technical stacks and expect multi‑year, multi‑million dollar investments to replicate it.

Specialized Clinical Focus

Clearday specializes in early- to mid-stage dementia and Alzheimer’s care, not general assisted living, enabling tailored care protocols and cognitive-stimulation programs shown to slow decline—studies suggest targeted interventions can reduce behavioral incidents by ~30% and delay nursing-home placement by 9–18 months. As of 2025 Clearday reports >85% occupancy in memory-care suites and revenue per occupied unit 12% above regional assisted-living averages.

Asset-Light Scalability Potential

The shift to digital services and licensing lets Clearday scale users without heavy real estate spend; asset-light entrants report 30–50% lower upfront capex versus traditional care operators (2024 industry median).

This strategy boosts long-term financial flexibility and supports faster market entry—digital rollouts can cut time-to-market by 6–12 months versus buildouts, enabling SaaS-like gross margins above 60% as seen in care-tech peers.

It also preserves clinical credibility by pairing licensed tech with legacy physical operations, so Clearday can pivot revenue mix toward recurring license fees while keeping on-site care as proof-of-concept.

- Lower capex: ~30–50% reduction (2024 median)

- Faster rollout: 6–12 months saved

- Target gross margins: >60% for SaaS-like services

- Hybrid model: digital licensing + physical credibility

Experienced Leadership in Healthcare

The management team combines 20+ years average healthcare ops experience, proven regulatory track records (HIPAA, CMS) and multiple digital-health integrations that cut readmission by ~15% in pilot programs (2024).

Their expertise reduces compliance risk and accelerates product-market fit for remote monitoring and EHR links, supporting projected ARR growth of 35% in 2025.

- 20+ yrs avg leadership experience

- 15% pilot readmission reduction (2024)

- HIPAA/CMS compliance strength

- Projected 35% ARR growth (2025)

Clearday: Hybrid memory care + platform — 12k users, 85%+ occupancy, 35% ARR growth

Clearday’s hybrid model pairs 24 memory-care homes with a proprietary digital platform serving 12,000+ active users (2025), driving ~18% YoY retention lift and >85% suite occupancy; SaaS-like services target >60% gross margins and projected 35% ARR growth (2025), with pilots cutting readmissions ~15% (2024) and delaying nursing placement 9–18 months.

| Metric | Value (Year) |

|---|---|

| Homes | 24 (2025) |

| Active users | 12,000+ (2025) |

| Retention lift | ~18% YoY |

| Occupancy | >85% (2025) |

| Gross margin target | >60% |

| ARR growth | 35% (2025) |

| Readmission reduction | ~15% (2024) |

| Delay to nursing home | 9–18 months |

What is included in the product

Provides a concise SWOT overview of Clearday, highlighting its core strengths, operational weaknesses, market opportunities, and external threats to inform strategic decision-making.

Delivers a concise, editable SWOT matrix that speeds strategic alignment and stakeholder updates, ideal for executives needing a clear snapshot of Clearday’s positioning.

Weaknesses

Limited Geographic Diversification

The physical footprint of Clearday is concentrated in a few regions, exposing it to localized economic and regulatory shocks—local revenue swings could exceed 30% if a major facility faces closure or policy changes.

Lacking a national presence hinders bids for large corporate partnerships and national insurance contracts, where providers with 50+ sites are preferred.

Scaling nationally will demand heavy capex and time; opening 40 new sites to reach national coverage could cost roughly $80–120 million based on industry averages of $2–3M per site.

Historical Financial Volatility

Clearday has shown inconsistent profitability and strained liquidity—FY2024 EBITDA swung to -$12.3M after a 2023 loss of -$8.1M—common in high-growth care firms. Specialized memory-care staffing and facility costs drive high operating overhead, squeezing cash flow when occupancy dipped to 68% in Q4 2024. Historical debt (total long-term debt ~$45M as of 12/31/2024) and ongoing funding needs raise investor concerns about long-term stability.

High Dependency on Skilled Labor

Clearday depends on highly trained caregivers and clinical staff to deliver specialized dementia care, and the 2024 U.S. Bureau of Labor Statistics reported a 12% shortfall in long-term care staffing vs pre-pandemic levels, driving average wage growth of 6.5% year-over-year and raising labor expense to ~45% of operating costs.

Consumer Adoption of Digital Tools

Clearday’s virtual platform faces slow uptake among elderly users and caregivers; 37% of US adults 65+ were non-internet users in 2021 and 23% reported low digital literacy in 2023, so adoption risk is material.

Bridging the digital divide needs intensive user education and a highly intuitive interface, raising upfront UX/dev and marketing spend—estimating a 15–25% increase in CAC and a 12–18 month payback vs. traditional channels.

Slower-than-expected roll-out of Clearday at Home could delay revenue targets: missing a 2025 subscriber goal by 20% would cut projected ARR growth by roughly the same share.

- 37% of adults 65+ non-internet users (2021)

- 23% low digital literacy (2023)

- Estimated +15–25% CAC to educate users

- 12–18 month longer payback

- 20% subscriber shortfall ≈ 20% ARR hit

Revenue Concentration in Private Pay

A large share of Clearday’s revenue comes from private-pay clients, leaving it exposed if household discretionary income falls; in 2024 about 62% of revenue was private-pay, per company filings.

If families face job loss or inflation-driven strain they may delay placements or choose lower-cost home care, which reduced private-pay admissions industry-wide by ~8% in 2023.

Lack of reimbursement mix like Medicare/Medicaid cushions means earnings are cyclical and vulnerable during recessions; a 1% drop in private-pay volume could cut operating income by roughly 0.9% based on 2024 margins.

- 62% revenue private-pay (2024)

- Private-pay admissions down ~8% in 2023

- 1% private-pay drop ≈ 0.9% operating income hit

Clearday’s cash, staffing, and scale shortfalls threaten growth and liquidity

Clearday’s concentrated footprint, weak national scale (40 sites ≈ $80–120M), inconsistent profitability (FY2024 EBITDA -$12.3M; LT debt ~$45M as of 12/31/2024), heavy private-pay exposure (62% revenue 2024), staffing shortfall (BLS: 12% gap; labor ≈45% costs) and slow virtual uptake (37% 65+ non-users 2021) raise liquidity, growth, and adoption risks.

| Metric | Value |

|---|---|

| FY2024 EBITDA | -$12.3M |

| Long-term debt | $45M (12/31/2024) |

| Private-pay rev | 62% (2024) |

| Occupancy Q4 2024 | 68% |

| 65+ non-internet | 37% (2021) |

Full Version Awaits

Clearday SWOT Analysis

This is the actual Clearday SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality and fully editable content.

The preview below is taken directly from the complete report; buy now to unlock the full, detailed version immediately after checkout.