Mycronic Porter's Five Forces Analysis

From Overview to Strategy Blueprint

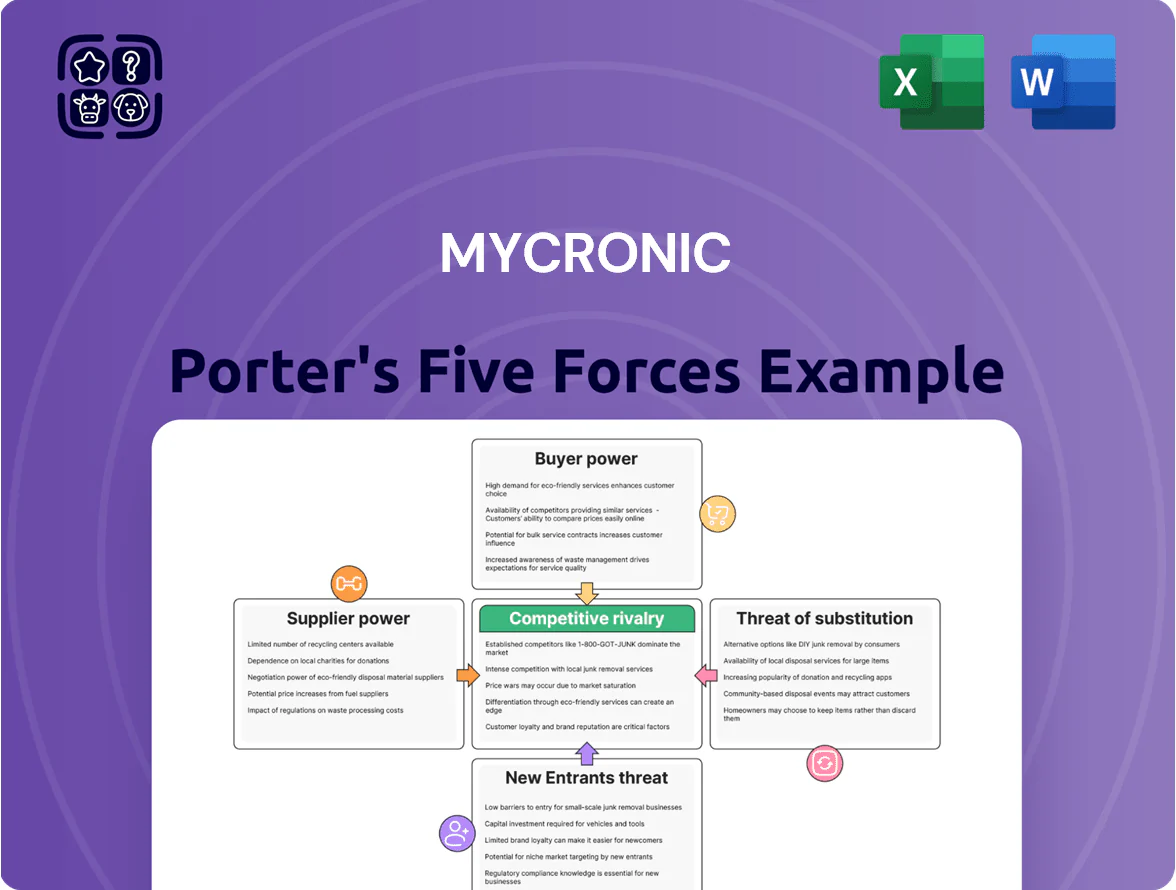

Mycronic operates in a capital-intensive, tech-driven niche where supplier specialization and customer concentration shape bargaining power, while high R&D and equipment costs raise barriers to entry and limit substitutes.

Competitive rivalry is intense among precision-equipment players, but Mycronic’s IP and service model provide defensive advantages—yet demand cyclicality and geopolitical risk remain material threats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Mycronic’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Optical and Laser Systems

Mycronic depends on a few high-end suppliers for precision optics and laser sources used in its mask writer division; these vendors supply components meeting specs at sub-micron accuracy and account for supply concentration—top 3 suppliers likely cover >70% of market for such parts as of 2025. Those vendors hold pricing and delivery leverage because only a handful of firms meet the tolerance and reliability standards. Switching would need 9–18 months of requalification and capital redesign, plus multimillion-dollar tooling and validation costs, raising supplier bargaining power significantly.

Advanced Semiconductor Components

Advanced semiconductor components and sensors for Mycronic’s jet printing systems face tight global supply: the semiconductor industry saw a 15% capacity shortfall in 2024, pushing spot prices up ~12% year-on-year, and Mycronic often competes with larger electronics OEMs for the same parts.

This dependency forces Mycronic to hold higher safety stock—company filings show inventory days rose to ~110 in 2024—and to pursue multi-year contracts with suppliers to reduce shortage and price-risk exposure.

Precision Mechanical Engineering

Precision mechanical parts from specialist firms are critical to Mycronic’s machines, and about 40–50% of unit cost variability ties to these components per industry estimates; suppliers’ proprietary techniques raise switching costs and limit alternative sourcing.

Software and Control Interface Licensing

Software and control interface licensing gives suppliers strong leverage over Mycronic because modern machines depend on proprietary control algorithms; third-party software partners can charge recurring licensing and support fees—industry reports show embedded software can account for 8–12% of OEM lifecycle costs and update contracts add ~15% annual service revenue.

Switching costs are high: migrating to new architectures can take 12–24 months and cost tens of millions for R&D and revalidation, so Mycronic faces supplier-driven price and timing risk.

- Proprietary software = recurring fees

- Updates critical for uptime, performance

- Embedded SW ~8–12% OEM lifecycle cost

- Migration 12–24 months, multi‑million cost

Raw Material Volatility

The manufacturing of Mycronic’s high-precision equipment relies on specialized alloys and rare-earths vulnerable to geopolitical risk; rare-earth prices rose ~45% from 2020–2024, amplifying input-cost swings. Suppliers can push prices when electronics-capacity expansions raise demand, squeezing Mycronic’s 2024 gross margin of ~33% unless costs are passed through or efficiency improves.

- Rare-earth price rise ~45% (2020–2024)

- Mycronic gross margin ~33% in 2024

- Supplier-driven spikes during electronics demand surges

- Need to pass costs or boost efficiency to protect margins

High supplier power: top‑3 >70%, long switch costs, +45% rare‑earths, safety stock needed

Supplier power is high: top 3 precision optics/laser suppliers likely >70% share (2025), switching costs 9–24 months and multi‑million requalification, inventory days ~110 (2024), rare‑earth prices +45% (2020–2024), Mycronic gross margin ~33% (2024), embedded software 8–12% of lifecycle costs; multiyear contracts and safety stock needed to mitigate price and delivery risk.

| Metric | Value |

|---|---|

| Top‑3 supplier share | >70% (2025) |

| Switch time/cost | 9–24 months; multi‑$m |

| Inventory days | ~110 (2024) |

| Rare‑earth change | +45% (2020–2024) |

| Gross margin | ~33% (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Mycronic that uncovers competitive drivers, buyer and supplier power, threat of new entrants and substitutes, and identifies disruptive risks and protective market dynamics to inform strategic and investment decisions.

A concise Porter's Five Forces one-sheet for Mycronic—quickly highlights supplier/buyer power, competitive rivalry, threat of substitutes and entrants to speed strategic decisions.

Customers Bargaining Power

Concentration of Global Electronics Giants

High Capital Expenditure Sensitivity

The equipment Mycronic sells is a major capex item, so order rates track global GDP and electronics demand; in 2024 Mycronic reported a 22% year‑over‑year order volatility linked to consumer electronics cycles.

Customers routinely delay or renegotiate during downturns—EMS capital spending fell ~18% in 2023—so buyers push for concessions and timing flexibility.

To win deals, Mycronic offers tailored financing and service bundles; flexible payment terms helped secure several multi‑year contracts worth >SEK 1bn in 2024.

Stringent Performance and Quality Standards

Customers in semiconductor and display sectors demand near-zero error rates, giving them power to require extreme precision and reliability; Mycronic’s 2024 service revenue of SEK 1.9bn shows this after-sales focus.

Failing throughput or quality benchmarks lets buyers demand costly fixes or penalties—industry fabs push for >99.9% uptime and sub-ppm defect rates, raising risk for vendors.

So Mycronic must fund continuous support and optimization; R&D and service spend were ~22% of 2024 sales, key to retaining premium clients.

Low Switching Costs in Assembly Segments

Customers in surface-mount tech and dispensing face low switching costs because the assembly segment is fragmented and price-sensitive; in 2024 Mycronic’s assembly rival base grew over 8% as budget OEMs expanded, making swaps easier.

High-end mask writers stay concentrated, but assembly buyers readily shift to rivals offering better price-to-AOI (automated optical inspection) performance, impacting Mycronic’s bargaining power and pressuring ASPs.

- Fragmented assembly market → more competitors, lower stickiness

- 2024: >8% growth in low-cost assembly OEMs

- Customers prioritize price + AOI capability

- Low switching costs weaken Mycronic’s leverage

Demands for Integrated Industry 4.0 Solutions

Customers now demand factory-wide Industry 4.0 solutions that talk across machines and IT, giving buyers leverage to require Mycronic to support diverse software and third-party hardware; in 2024, 62% of manufacturers prioritized open integration when buying equipment (Capgemini report).

If Mycronic fails on interoperability, buyers can switch to rivals—companies offering open platforms saw 8–12% higher equipment win rates in 2023.

Mycronic under margin pressure: concentrated buyers, order volatility, open‑platform risk

| Metric | 2023–2024 |

|---|---|

| Revenue concentration from Tier‑1 | 40–50% |

| Order volatility (YoY) | ±22% |

| EMS capex decline (2023) | −18% |

| Service revenue | SEK 1.9bn (2024) |

| R&D+service spend | ~22% of sales (2024) |

| Low‑cost OEM growth | >8% (2024) |

| Manufacturers preferring open integration | 62% (2024) |

Preview Before You Purchase

Mycronic Porter's Five Forces Analysis

This preview shows the exact Mycronic Porter’s Five Forces analysis you’ll receive—fully formatted, professionally written, and ready for immediate download after purchase with no placeholders or mockups.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Mycronic operates in a capital-intensive, tech-driven niche where supplier specialization and customer concentration shape bargaining power, while high R&D and equipment costs raise barriers to entry and limit substitutes.

Competitive rivalry is intense among precision-equipment players, but Mycronic’s IP and service model provide defensive advantages—yet demand cyclicality and geopolitical risk remain material threats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Mycronic’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Optical and Laser Systems

Mycronic depends on a few high-end suppliers for precision optics and laser sources used in its mask writer division; these vendors supply components meeting specs at sub-micron accuracy and account for supply concentration—top 3 suppliers likely cover >70% of market for such parts as of 2025. Those vendors hold pricing and delivery leverage because only a handful of firms meet the tolerance and reliability standards. Switching would need 9–18 months of requalification and capital redesign, plus multimillion-dollar tooling and validation costs, raising supplier bargaining power significantly.

Advanced Semiconductor Components

Advanced semiconductor components and sensors for Mycronic’s jet printing systems face tight global supply: the semiconductor industry saw a 15% capacity shortfall in 2024, pushing spot prices up ~12% year-on-year, and Mycronic often competes with larger electronics OEMs for the same parts.

This dependency forces Mycronic to hold higher safety stock—company filings show inventory days rose to ~110 in 2024—and to pursue multi-year contracts with suppliers to reduce shortage and price-risk exposure.

Precision Mechanical Engineering

Precision mechanical parts from specialist firms are critical to Mycronic’s machines, and about 40–50% of unit cost variability ties to these components per industry estimates; suppliers’ proprietary techniques raise switching costs and limit alternative sourcing.

Software and Control Interface Licensing

Software and control interface licensing gives suppliers strong leverage over Mycronic because modern machines depend on proprietary control algorithms; third-party software partners can charge recurring licensing and support fees—industry reports show embedded software can account for 8–12% of OEM lifecycle costs and update contracts add ~15% annual service revenue.

Switching costs are high: migrating to new architectures can take 12–24 months and cost tens of millions for R&D and revalidation, so Mycronic faces supplier-driven price and timing risk.

- Proprietary software = recurring fees

- Updates critical for uptime, performance

- Embedded SW ~8–12% OEM lifecycle cost

- Migration 12–24 months, multi‑million cost

Raw Material Volatility

The manufacturing of Mycronic’s high-precision equipment relies on specialized alloys and rare-earths vulnerable to geopolitical risk; rare-earth prices rose ~45% from 2020–2024, amplifying input-cost swings. Suppliers can push prices when electronics-capacity expansions raise demand, squeezing Mycronic’s 2024 gross margin of ~33% unless costs are passed through or efficiency improves.

- Rare-earth price rise ~45% (2020–2024)

- Mycronic gross margin ~33% in 2024

- Supplier-driven spikes during electronics demand surges

- Need to pass costs or boost efficiency to protect margins

High supplier power: top‑3 >70%, long switch costs, +45% rare‑earths, safety stock needed

Supplier power is high: top 3 precision optics/laser suppliers likely >70% share (2025), switching costs 9–24 months and multi‑million requalification, inventory days ~110 (2024), rare‑earth prices +45% (2020–2024), Mycronic gross margin ~33% (2024), embedded software 8–12% of lifecycle costs; multiyear contracts and safety stock needed to mitigate price and delivery risk.

| Metric | Value |

|---|---|

| Top‑3 supplier share | >70% (2025) |

| Switch time/cost | 9–24 months; multi‑$m |

| Inventory days | ~110 (2024) |

| Rare‑earth change | +45% (2020–2024) |

| Gross margin | ~33% (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Mycronic that uncovers competitive drivers, buyer and supplier power, threat of new entrants and substitutes, and identifies disruptive risks and protective market dynamics to inform strategic and investment decisions.

A concise Porter's Five Forces one-sheet for Mycronic—quickly highlights supplier/buyer power, competitive rivalry, threat of substitutes and entrants to speed strategic decisions.

Customers Bargaining Power

Concentration of Global Electronics Giants

High Capital Expenditure Sensitivity

The equipment Mycronic sells is a major capex item, so order rates track global GDP and electronics demand; in 2024 Mycronic reported a 22% year‑over‑year order volatility linked to consumer electronics cycles.

Customers routinely delay or renegotiate during downturns—EMS capital spending fell ~18% in 2023—so buyers push for concessions and timing flexibility.

To win deals, Mycronic offers tailored financing and service bundles; flexible payment terms helped secure several multi‑year contracts worth >SEK 1bn in 2024.

Stringent Performance and Quality Standards

Customers in semiconductor and display sectors demand near-zero error rates, giving them power to require extreme precision and reliability; Mycronic’s 2024 service revenue of SEK 1.9bn shows this after-sales focus.

Failing throughput or quality benchmarks lets buyers demand costly fixes or penalties—industry fabs push for >99.9% uptime and sub-ppm defect rates, raising risk for vendors.

So Mycronic must fund continuous support and optimization; R&D and service spend were ~22% of 2024 sales, key to retaining premium clients.

Low Switching Costs in Assembly Segments

Customers in surface-mount tech and dispensing face low switching costs because the assembly segment is fragmented and price-sensitive; in 2024 Mycronic’s assembly rival base grew over 8% as budget OEMs expanded, making swaps easier.

High-end mask writers stay concentrated, but assembly buyers readily shift to rivals offering better price-to-AOI (automated optical inspection) performance, impacting Mycronic’s bargaining power and pressuring ASPs.

- Fragmented assembly market → more competitors, lower stickiness

- 2024: >8% growth in low-cost assembly OEMs

- Customers prioritize price + AOI capability

- Low switching costs weaken Mycronic’s leverage

Demands for Integrated Industry 4.0 Solutions

Customers now demand factory-wide Industry 4.0 solutions that talk across machines and IT, giving buyers leverage to require Mycronic to support diverse software and third-party hardware; in 2024, 62% of manufacturers prioritized open integration when buying equipment (Capgemini report).

If Mycronic fails on interoperability, buyers can switch to rivals—companies offering open platforms saw 8–12% higher equipment win rates in 2023.

Mycronic under margin pressure: concentrated buyers, order volatility, open‑platform risk

| Metric | 2023–2024 |

|---|---|

| Revenue concentration from Tier‑1 | 40–50% |

| Order volatility (YoY) | ±22% |

| EMS capex decline (2023) | −18% |

| Service revenue | SEK 1.9bn (2024) |

| R&D+service spend | ~22% of sales (2024) |

| Low‑cost OEM growth | >8% (2024) |

| Manufacturers preferring open integration | 62% (2024) |

Preview Before You Purchase

Mycronic Porter's Five Forces Analysis

This preview shows the exact Mycronic Porter’s Five Forces analysis you’ll receive—fully formatted, professionally written, and ready for immediate download after purchase with no placeholders or mockups.