Myer Porter's Five Forces Analysis

Don't Miss the Bigger Picture

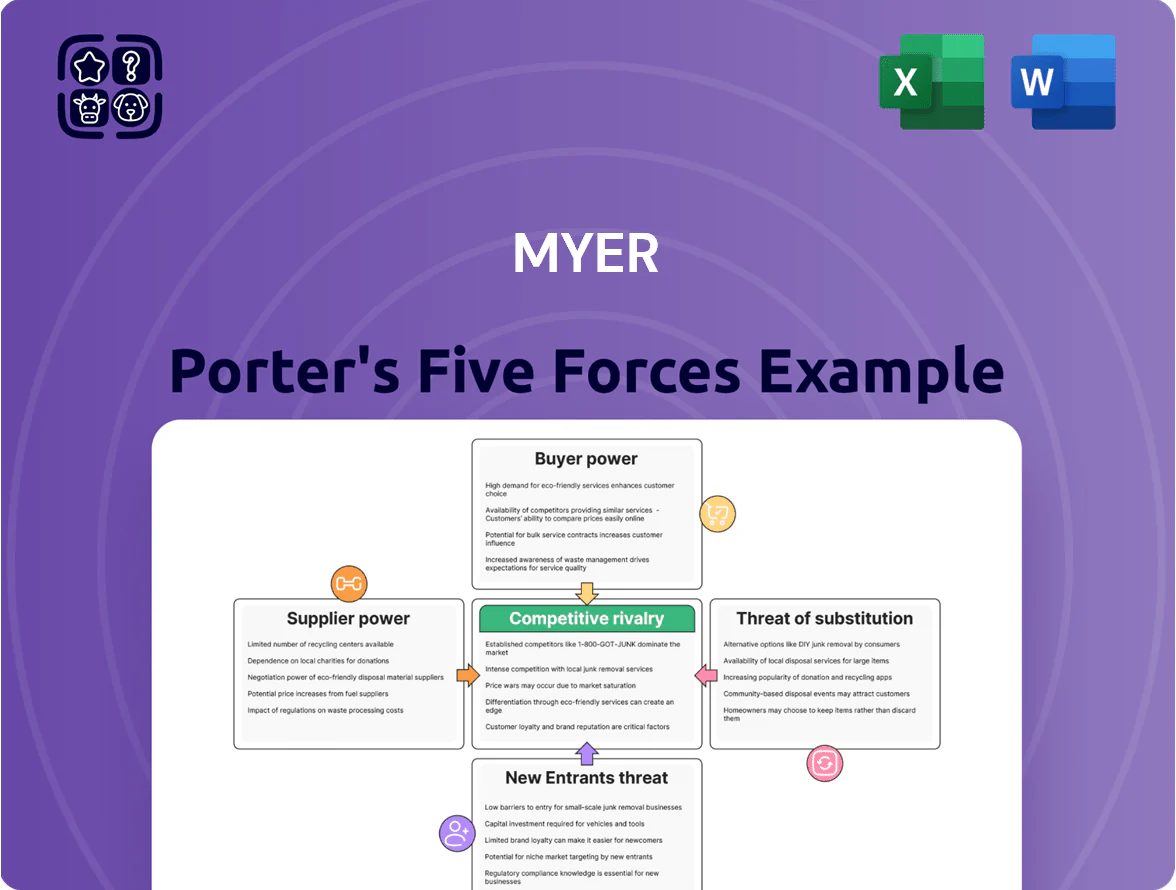

Myer faces intense competitive rivalry, moderate supplier power, and high buyer bargaining driven by value-conscious consumers and omni-channel choices; barriers to entry are mixed while substitute threats from fast-fashion and online marketplaces loom.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Myer’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Prestige Brands

The bargaining power of suppliers is high for prestige and international brands Myer uses to drive foot traffic; in 2024 luxury and beauty tenants contributed roughly 35% of Myer’s full-price sales, so losing a marquee cosmetics or fashion house would cut high-spender appeal sharply.

These brands often set floor-space, fixture and pricing terms—estimates show anchor brand leases can yield 20–30% higher rent-free fit-out allowances—giving suppliers leverage over merchandising and margins.

If a major prestige brand withdraws, Myer risks a measurable drop in basket size: similar department-store exits in Australia have led to 8–12% declines in high-value customer visits within 12 months.

Expansion of Private Label Brands

By end-2025 Myer grew private-label sales to about 28% of apparel revenue, cutting reliance on external vendors and lifting gross margins by ~220 basis points versus 2022.

Designing and sourcing its own labels gave Myer tighter supply-chain control, shortened lead times by ~15%, and reduced wholesalers’ bargaining power over pricing and product mix.

Global Supply Chain Dynamics

Suppliers of electronics and homewares sell globally and retain strong leverage due to scale and essential product status; top 10 manufacturers control ~60% of consumer electronics shipments in 2024, keeping pricing and allocation power.

By 2025 supply-chain stability rose—global lead-time volatility fell from ±22% in 2021 to ±9% in 2024—yet large manufacturers still dictate volume discounts and priority during peaks.

Myer must keep preferred terms with these giants; securing even a 5% higher allocation for peak months can raise seasonal sales by an estimated AUD 12–18m based on FY24 turnover patterns.

Switching Costs for Specialty Goods

Switching basic apparel suppliers is low-cost, but replacing premium vendors for Myer incurs high switching costs and brand risk; onboarding a new luxury brand can take 6–12 months and marketing spends often exceed A$1–3m to re-educate customers.

To avoid stock gaps and preserve customer loyalty, Myer frequently accepts narrower margins or stricter payment terms from specialty suppliers, with premium category fill-rate targets above 95% driving concessions.

- Onboarding time: 6–12 months

- Marketing re-education: A$1–3m

- Premium fill-rate target: >95%

- Leads to narrower margins, looser payment terms

Impact of Logistics and Input Costs

Suppliers are passing sustainable packaging and carbon-neutral shipping costs to retailers; by late 2025 this added ~2–4% to wholesale prices for apparel and homewares, squeezing Myer’s gross margins.

Higher raw-material prices (cotton up ~18% YoY in 2024–25) and manufacturing labor shortages in Vietnam and Bangladesh force suppliers to seek price hikes; Myer must absorb costs or lose key lines to rivals paying higher wholesale rates.

- 2–4% extra wholesale cost late 2025

- Cotton +18% YoY 2024–25

- Vietnam/Bangladesh labor shortages raise lead times 10–20%

- Choice: margin hit or lost SKUs to competitors

Suppliers Squeeze Margins: Private Label Lift Offsets Rising Costs and Onboarding Pain

Suppliers hold high bargaining power for prestige brands and electronics—luxury/beauty made ~35% of full-price sales in 2024; anchor brand fit-outs raise costs 20–30%. Myer boosted private-label to ~28% of apparel by end-2025, cutting reliance and improving gross margin ~220 bps. Rising input costs (cotton +18% 2024–25) and sustainability fees (+2–4%) squeeze margins; replacing premium suppliers costs 6–12 months and A$1–3m.

| Metric | Value |

|---|---|

| Luxury/beauty share (2024) | ~35% |

| Private-label apparel (end-2025) | ~28% |

| Gross margin lift vs 2022 | ~220 bps |

| Cotton price change (2024–25) | +18% YoY |

| Sustainability cost to wholesale | +2–4% |

| Onboarding premium brand | 6–12 months; A$1–3m |

What is included in the product

Tailored Porter's Five Forces analysis for Myer that uncovers competitive pressures, buyer and supplier power, entry barriers, and substitute threats, highlighting strategic risks and opportunities in the department-store sector.

Instantly map competitive threats with a concise Five Forces overview—ideal for rapid strategy sessions or investor decks.

Customers Bargaining Power

Low Switching Costs in Retail

The bargaining power of customers is very high for Myer because shoppers face no financial penalty switching to rivals; Australian retail survey data show 62% of consumers compare prices in-store using phones (Roy Morgan, 2024). Shoppers can view competing offers across apps and websites instantly, pressuring Myer to match prices and promotions. This low switching cost forces Myer to innovate services and loyalty programs—Myer One reported 1.4 million members in FY2024—to retain customers.

Price Sensitivity and Economic Pressure

By end-2025 Australian shoppers stayed price-sensitive after rate volatility; ABS retail trade showed household retail volumes fell 1.2% year-to-date to Q3 2025, reflecting cautious spend. Consumers increasingly wait for Black Friday and Click Frenzy—Adobe data: Black Friday 2024 drove a 28% uplift in online traffic vs. monthly avg—so buyers now dictate timing and depth of Myer’s discount cycles.

Influence of Online Transparency

Digital platforms give Australian shoppers clear global price benchmarks; 2024 data from Deloitte Australia shows 59% compare international prices before buying, raising expectations that Myer match or beat prices from sites like Amazon or local discounters such as Kmart.

That transparency shifts bargaining power to tech-savvy customers, pressuring Myer’s margins—retail CPI rose 3.1% in 2024—forcing more promotions, price-matching, or value-added services to retain sales.

Loyalty Program Maturity

The MYER one loyalty program reduces customer bargaining power by driving repeat visits with tiered, personalized rewards; as of FY2024 Myer reported ~3.2 million members and loyalty sales contributing ~28% of total revenue.

By 2025 customers expect advanced personalization and clear value for data; surveys show 68% will switch brands if rewards feel insufficient, so weak perks quickly shift loyalty to rivals like David Jones or Amazon.

- 3.2M members; 28% revenue (FY2024)

- 68% switch if rewards insufficient (2025 survey)

- Personalization now required to retain repeat spend

Demand for Omnichannel Flexibility

Customers now demand a seamless experience between Myer’s stores and digital channels, with click-and-collect and easy returns becoming baseline expectations; 2024 Omnichannel shoppers spent ~45% more per visit than single-channel shoppers, raising the stakes for Myer.

Myer’s 2023–24 investment in its online platform and fulfilment (A$60m+ reported capex) responds to this power, since clunky interfaces drive churn—60% of Australians would switch brands after one bad digital experience.

The customer’s freedom to choose shopping mode forces continuous upgrades to Myer’s inventory, logistics and POS systems, increasing operating costs and compressing margins.

- Omnichannel shoppers +45% spend

- Myer capex A$60m+ (2023–24)

- 60% would switch after bad digital UX

Myer faces strong customer leverage—loyalty helps but 68% will switch if rewards fail

Customers hold high bargaining power over Myer: low switching costs, digital price transparency, and event-driven buying force frequent promotions; MYERone (3.2M members, 28% revenue FY2024) and A$60m+ capex (2023–24) mitigate but don’t eliminate pressure—68% switch if rewards weak; omnichannel shoppers spend ~45% more; retail CPI +3.1% (2024) squeezes margins.

| Metric | Value |

|---|---|

| MYERone members | 3.2M (FY2024) |

| Revenue from loyalty | 28% (FY2024) |

| Capex | A$60m+ (2023–24) |

| Switch if rewards weak | 68% (2025 survey) |

| Omnichannel uplift | +45% |

Same Document Delivered

Myer Porter's Five Forces Analysis

This preview shows the exact Myer Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples; the full, professionally formatted document is ready for instant download and use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Myer faces intense competitive rivalry, moderate supplier power, and high buyer bargaining driven by value-conscious consumers and omni-channel choices; barriers to entry are mixed while substitute threats from fast-fashion and online marketplaces loom.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Myer’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Prestige Brands

The bargaining power of suppliers is high for prestige and international brands Myer uses to drive foot traffic; in 2024 luxury and beauty tenants contributed roughly 35% of Myer’s full-price sales, so losing a marquee cosmetics or fashion house would cut high-spender appeal sharply.

These brands often set floor-space, fixture and pricing terms—estimates show anchor brand leases can yield 20–30% higher rent-free fit-out allowances—giving suppliers leverage over merchandising and margins.

If a major prestige brand withdraws, Myer risks a measurable drop in basket size: similar department-store exits in Australia have led to 8–12% declines in high-value customer visits within 12 months.

Expansion of Private Label Brands

By end-2025 Myer grew private-label sales to about 28% of apparel revenue, cutting reliance on external vendors and lifting gross margins by ~220 basis points versus 2022.

Designing and sourcing its own labels gave Myer tighter supply-chain control, shortened lead times by ~15%, and reduced wholesalers’ bargaining power over pricing and product mix.

Global Supply Chain Dynamics

Suppliers of electronics and homewares sell globally and retain strong leverage due to scale and essential product status; top 10 manufacturers control ~60% of consumer electronics shipments in 2024, keeping pricing and allocation power.

By 2025 supply-chain stability rose—global lead-time volatility fell from ±22% in 2021 to ±9% in 2024—yet large manufacturers still dictate volume discounts and priority during peaks.

Myer must keep preferred terms with these giants; securing even a 5% higher allocation for peak months can raise seasonal sales by an estimated AUD 12–18m based on FY24 turnover patterns.

Switching Costs for Specialty Goods

Switching basic apparel suppliers is low-cost, but replacing premium vendors for Myer incurs high switching costs and brand risk; onboarding a new luxury brand can take 6–12 months and marketing spends often exceed A$1–3m to re-educate customers.

To avoid stock gaps and preserve customer loyalty, Myer frequently accepts narrower margins or stricter payment terms from specialty suppliers, with premium category fill-rate targets above 95% driving concessions.

- Onboarding time: 6–12 months

- Marketing re-education: A$1–3m

- Premium fill-rate target: >95%

- Leads to narrower margins, looser payment terms

Impact of Logistics and Input Costs

Suppliers are passing sustainable packaging and carbon-neutral shipping costs to retailers; by late 2025 this added ~2–4% to wholesale prices for apparel and homewares, squeezing Myer’s gross margins.

Higher raw-material prices (cotton up ~18% YoY in 2024–25) and manufacturing labor shortages in Vietnam and Bangladesh force suppliers to seek price hikes; Myer must absorb costs or lose key lines to rivals paying higher wholesale rates.

- 2–4% extra wholesale cost late 2025

- Cotton +18% YoY 2024–25

- Vietnam/Bangladesh labor shortages raise lead times 10–20%

- Choice: margin hit or lost SKUs to competitors

Suppliers Squeeze Margins: Private Label Lift Offsets Rising Costs and Onboarding Pain

Suppliers hold high bargaining power for prestige brands and electronics—luxury/beauty made ~35% of full-price sales in 2024; anchor brand fit-outs raise costs 20–30%. Myer boosted private-label to ~28% of apparel by end-2025, cutting reliance and improving gross margin ~220 bps. Rising input costs (cotton +18% 2024–25) and sustainability fees (+2–4%) squeeze margins; replacing premium suppliers costs 6–12 months and A$1–3m.

| Metric | Value |

|---|---|

| Luxury/beauty share (2024) | ~35% |

| Private-label apparel (end-2025) | ~28% |

| Gross margin lift vs 2022 | ~220 bps |

| Cotton price change (2024–25) | +18% YoY |

| Sustainability cost to wholesale | +2–4% |

| Onboarding premium brand | 6–12 months; A$1–3m |

What is included in the product

Tailored Porter's Five Forces analysis for Myer that uncovers competitive pressures, buyer and supplier power, entry barriers, and substitute threats, highlighting strategic risks and opportunities in the department-store sector.

Instantly map competitive threats with a concise Five Forces overview—ideal for rapid strategy sessions or investor decks.

Customers Bargaining Power

Low Switching Costs in Retail

The bargaining power of customers is very high for Myer because shoppers face no financial penalty switching to rivals; Australian retail survey data show 62% of consumers compare prices in-store using phones (Roy Morgan, 2024). Shoppers can view competing offers across apps and websites instantly, pressuring Myer to match prices and promotions. This low switching cost forces Myer to innovate services and loyalty programs—Myer One reported 1.4 million members in FY2024—to retain customers.

Price Sensitivity and Economic Pressure

By end-2025 Australian shoppers stayed price-sensitive after rate volatility; ABS retail trade showed household retail volumes fell 1.2% year-to-date to Q3 2025, reflecting cautious spend. Consumers increasingly wait for Black Friday and Click Frenzy—Adobe data: Black Friday 2024 drove a 28% uplift in online traffic vs. monthly avg—so buyers now dictate timing and depth of Myer’s discount cycles.

Influence of Online Transparency

Digital platforms give Australian shoppers clear global price benchmarks; 2024 data from Deloitte Australia shows 59% compare international prices before buying, raising expectations that Myer match or beat prices from sites like Amazon or local discounters such as Kmart.

That transparency shifts bargaining power to tech-savvy customers, pressuring Myer’s margins—retail CPI rose 3.1% in 2024—forcing more promotions, price-matching, or value-added services to retain sales.

Loyalty Program Maturity

The MYER one loyalty program reduces customer bargaining power by driving repeat visits with tiered, personalized rewards; as of FY2024 Myer reported ~3.2 million members and loyalty sales contributing ~28% of total revenue.

By 2025 customers expect advanced personalization and clear value for data; surveys show 68% will switch brands if rewards feel insufficient, so weak perks quickly shift loyalty to rivals like David Jones or Amazon.

- 3.2M members; 28% revenue (FY2024)

- 68% switch if rewards insufficient (2025 survey)

- Personalization now required to retain repeat spend

Demand for Omnichannel Flexibility

Customers now demand a seamless experience between Myer’s stores and digital channels, with click-and-collect and easy returns becoming baseline expectations; 2024 Omnichannel shoppers spent ~45% more per visit than single-channel shoppers, raising the stakes for Myer.

Myer’s 2023–24 investment in its online platform and fulfilment (A$60m+ reported capex) responds to this power, since clunky interfaces drive churn—60% of Australians would switch brands after one bad digital experience.

The customer’s freedom to choose shopping mode forces continuous upgrades to Myer’s inventory, logistics and POS systems, increasing operating costs and compressing margins.

- Omnichannel shoppers +45% spend

- Myer capex A$60m+ (2023–24)

- 60% would switch after bad digital UX

Myer faces strong customer leverage—loyalty helps but 68% will switch if rewards fail

Customers hold high bargaining power over Myer: low switching costs, digital price transparency, and event-driven buying force frequent promotions; MYERone (3.2M members, 28% revenue FY2024) and A$60m+ capex (2023–24) mitigate but don’t eliminate pressure—68% switch if rewards weak; omnichannel shoppers spend ~45% more; retail CPI +3.1% (2024) squeezes margins.

| Metric | Value |

|---|---|

| MYERone members | 3.2M (FY2024) |

| Revenue from loyalty | 28% (FY2024) |

| Capex | A$60m+ (2023–24) |

| Switch if rewards weak | 68% (2025 survey) |

| Omnichannel uplift | +45% |

Same Document Delivered

Myer Porter's Five Forces Analysis

This preview shows the exact Myer Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples; the full, professionally formatted document is ready for instant download and use.