Fawry PESTLE Analysis

Your Competitive Advantage Starts with This Report

Explore how political shifts, economic trends, and rapid tech adoption are reshaping Fawry’s growth trajectory—our concise PESTLE highlights key risks and opportunities for investors and strategists; buy the full analysis for a detailed, actionable roadmap to strengthen your market position and inform smarter decisions.

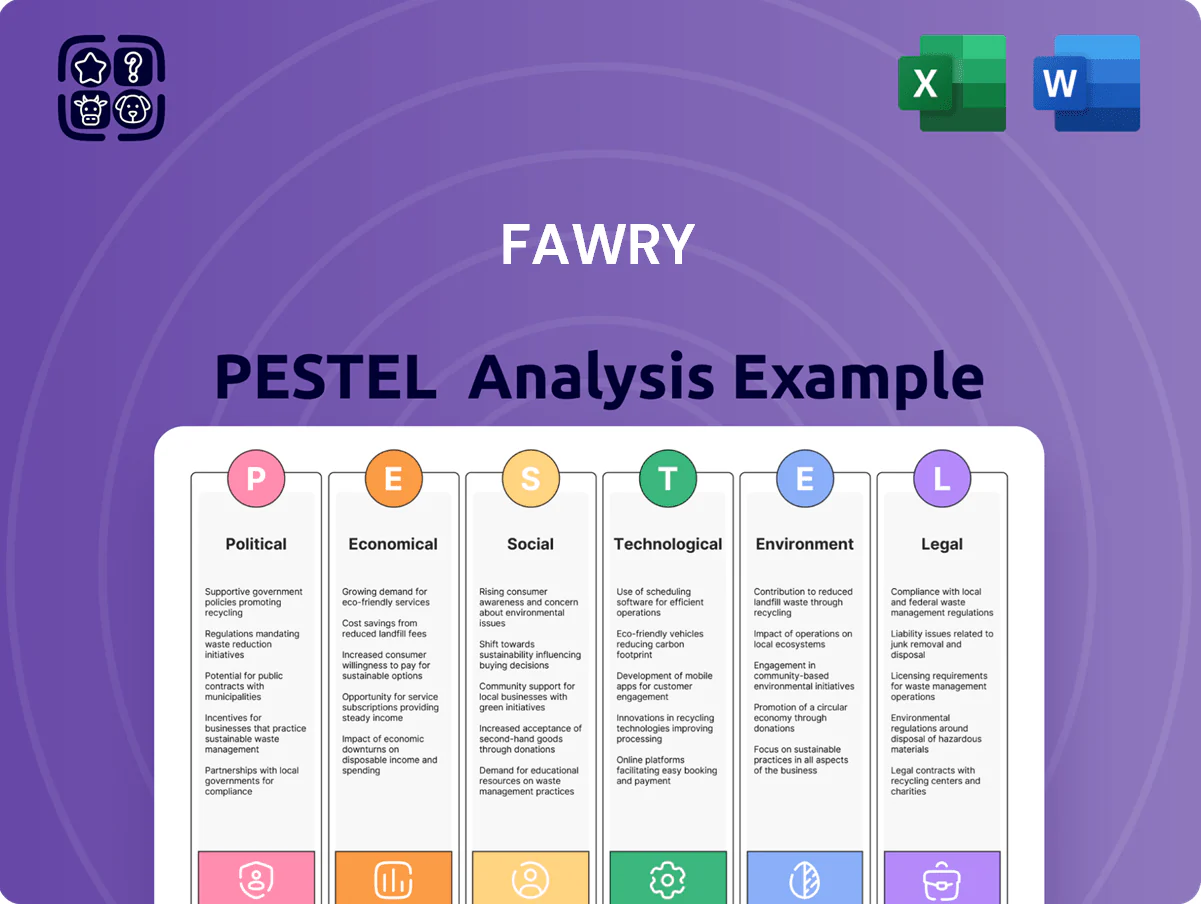

Political factors

Government Support for Digital Transformation

The Egyptian government continued prioritizing the Digital Egypt initiative into late 2025, allocating over EGP 15 billion to digital infrastructure and services, bolstering fintech adoption nationwide.

Fawry benefits as state-led cashless policies raised electronic transactions 28% YoY in 2024–25, reducing cash reliance and expanding addressable transaction volumes.

Political backing yields strategic partnerships with ministries and public entities, supporting Fawry’s revenue diversification and risk mitigation in a stable regulatory environment.

Geopolitical Stability in the MENA Region

Regional political dynamics heavily affect investor sentiment and FDI into Egyptian fintechs; Fawry saw foreign investor holdings fluctuate, with GCC-backed funds accounting for ~18% of announced fintech deals in Egypt in 2024 and $320m in regional tech investments across North Africa that year.

Regulatory Influence of the Central Bank

The Central Bank of Egypt (CBE) tightly regulates digital payments to safeguard monetary policy and inclusion; in 2024 it capped individual e-wallet limits at EGP 50,000 and issued 12 new fintech licenses, shaping market access.

Strategic Alliances with State Entities

Fawry's deep integration with government payment systems processes over 60% of Egypt's e-government transactions, handling more than EGP 120 billion in public-sector flows in 2024, creating high barriers to entry and embedding the company into national administrative infrastructure.

These political ties secure a steady stream of public-sector transactions—roughly 25–30% of Fawry's revenue in 2024—buffering revenue against private-market volatility and deterring competitors.

- Processes >60% of e-government transactions

- Handled ~EGP 120bn public-sector flows in 2024

- Public transactions ≈25–30% of 2024 revenue

- High entry barriers for competitors

Taxation Policies on Digital Services

New levies on electronic transactions and digital advertising as Egypt broadens its tax base could compress Fawry’s margins; Egypt collected EGP 1.2 trillion in tax revenues in FY2023/24, signaling tightening fiscal measures.

Changes to VAT rates or removal of tech-sector tax incentives would directly reduce free cash flow and reinvestment capacity for Fawry, which reported 2024 revenue of EGP 3.8 billion.

Proactive monitoring of fiscal policy is essential for pricing adjustments to protect competitiveness and maintain EBITDA margins (29% in 2024).

- New digital levies risk margin pressure

- VAT/corporate incentives affect reinvestment

- 2024 revenue EGP 3.8bn; EBITDA 29%

- Close policy monitoring required

Fawry dominates Egypt e-gov payments (>60%) as public flows ~EGP120bn; margin risks from new levies

Political support for Digital Egypt (EGP 15bn+ to 2025) and CBE regulation (EGP50k wallet cap; 12 fintech licenses in 2024) anchored Fawry’s government payment dominance—>60% e-gov transactions; ~EGP120bn public flows; public revenue 25–30% of 2024 revenue (EGP3.8bn; EBITDA 29%) while new digital levies and VAT shifts risk margin pressure.

| Metric | Value (2024–25) |

|---|---|

| Govt digital spend | EGP 15bn+ |

| Public flows | EGP 120bn |

| Share of e-gov txns | >60% |

| Revenue | EGP 3.8bn |

| EBITDA margin | 29% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Fawry across Political, Economic, Social, Technological, Environmental, and Legal dimensions, each backed by current data and regional industry trends to reveal actionable threats and opportunities for executives and investors.

A concise PESTLE snapshot tailored for Fawry that highlights key political, economic, social, technological, legal, and environmental risks and opportunities, enabling rapid alignment in meetings and clear, shareable insights for strategists and consultants.

Economic factors

Currency Volatility and Exchange Rate Management

The volatility of the Egyptian Pound directly affects Fawry’s asset valuations and hardware import costs; after the 2022-2024 depreciation and float adjustments that saw the EGP weaken roughly 40% vs USD, Fawry revised capital expenditure plans to reflect higher import costs. Following further adjustments into 2025, the company updated financial forecasts to buffer inflationary pressures—Egypt’s CPI ran near 32% in 2024—while hedging and FX clauses were strengthened. Effective foreign currency exposure management remains essential to preserve margins, reassure international shareholders, and support sustainable growth.

Impact of High Inflationary Pressures

Persistent inflation in Egypt (annual CPI ~26% in 2024) erodes household purchasing power, reducing the volume of discretionary e-commerce transactions routed via Fawry even as nominal bill values rise.

Higher prices lift average transaction amounts—supporting nominal fee revenues—but may depress transaction counts as consumers cut nonessential spending.

Fawry must fine-tune fee structures and promote low-cost payment options to protect margins while maintaining affordability for ~64 million mobile/internet users in Egypt (2024).

Interest Rate Fluctuations

The Central Bank of Egypt's policy rate, raised to 30.25% in March 2023 and held around 30% through 2024–25, directly affects Fawry's borrowing costs for expansion and its microfinance arm, increasing capital expenses while potentially widening lending margins. Higher rates elevate funding costs but can boost yields on Fawry's consumer credit and bill-payment financing, supporting net interest income. Fawry monitors CBE rate moves to adjust pricing, manage debt maturities, and calibrate consumer-credit product terms to protect profitability and liquidity.

Growth of the Informal Economy Transition

Egypt's informal economy remains large—estimated at about 40-50% of GDP pre-2024—and government drives to formalize present a major addressable market for Fawry, enabling onboarding of micro-enterprises and informal workers.

By 2025 Fawry reports growth in merchant count and active users, aided by outreach to unbanked segments (about 28% unbanked in 2023), increasing transaction frequency and ARPU on digital payment rails.

- Informal economy ~40–50% of GDP

- Unbanked ~28% (2023)

- Rising merchant/user adds driving transaction growth by 2025

Expansion into Microfinance and Credit Services

Fawry's move into microfinance and BNPL now contributes materially, with payment and lending revenues growing; in 2024 Fawry reported group transaction value surpassing EGP 200 billion and lending-related fees rising double digits year-on-year.

These services meet strong demand from SME owners and consumers facing tight liquidity; Egypt's consumer credit grew ~18% in 2023–2024, driving uptake of BNPL.

Performance hinges on robust credit scoring and Egyptian credit market conditions—non-performing loan ratios and bureau coverage will determine credit losses and margin sustainability.

- 2024 group TV > EGP 200bn

- Consumer credit growth ~18% (2023–24)

- Lending fees up double digits YoY

- Dependency: credit scoring quality and NPL trends

Egypt: Soaring costs, high rates and huge informal market fuel lending and digital growth

EGP depreciation (~40% vs USD since 2022) and 2024 CPI ~32% raised import and operating costs; CBE policy rate ~30% increased funding costs while supporting lending yields. Informal economy ~40–50% of GDP and ~28% unbanked (2023) create expansion opportunities; 2024 group transaction value >EGP 200bn, consumer credit growth ~18% (2023–24), lending fees up double digits YoY.

| Metric | Value |

|---|---|

| EGP weakening | ~40% vs USD (2022–24) |

| CPI 2024 | ~32% |

| CBE policy rate | ~30% |

| Informal economy | 40–50% GDP |

| Unbanked | ~28% (2023) |

| Group TV 2024 | >EGP 200bn |

| Consumer credit growth | ~18% (2023–24) |

Preview Before You Purchase

Fawry PESTLE Analysis

The preview shown here is the exact Fawry PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Explore how political shifts, economic trends, and rapid tech adoption are reshaping Fawry’s growth trajectory—our concise PESTLE highlights key risks and opportunities for investors and strategists; buy the full analysis for a detailed, actionable roadmap to strengthen your market position and inform smarter decisions.

Political factors

Government Support for Digital Transformation

The Egyptian government continued prioritizing the Digital Egypt initiative into late 2025, allocating over EGP 15 billion to digital infrastructure and services, bolstering fintech adoption nationwide.

Fawry benefits as state-led cashless policies raised electronic transactions 28% YoY in 2024–25, reducing cash reliance and expanding addressable transaction volumes.

Political backing yields strategic partnerships with ministries and public entities, supporting Fawry’s revenue diversification and risk mitigation in a stable regulatory environment.

Geopolitical Stability in the MENA Region

Regional political dynamics heavily affect investor sentiment and FDI into Egyptian fintechs; Fawry saw foreign investor holdings fluctuate, with GCC-backed funds accounting for ~18% of announced fintech deals in Egypt in 2024 and $320m in regional tech investments across North Africa that year.

Regulatory Influence of the Central Bank

The Central Bank of Egypt (CBE) tightly regulates digital payments to safeguard monetary policy and inclusion; in 2024 it capped individual e-wallet limits at EGP 50,000 and issued 12 new fintech licenses, shaping market access.

Strategic Alliances with State Entities

Fawry's deep integration with government payment systems processes over 60% of Egypt's e-government transactions, handling more than EGP 120 billion in public-sector flows in 2024, creating high barriers to entry and embedding the company into national administrative infrastructure.

These political ties secure a steady stream of public-sector transactions—roughly 25–30% of Fawry's revenue in 2024—buffering revenue against private-market volatility and deterring competitors.

- Processes >60% of e-government transactions

- Handled ~EGP 120bn public-sector flows in 2024

- Public transactions ≈25–30% of 2024 revenue

- High entry barriers for competitors

Taxation Policies on Digital Services

New levies on electronic transactions and digital advertising as Egypt broadens its tax base could compress Fawry’s margins; Egypt collected EGP 1.2 trillion in tax revenues in FY2023/24, signaling tightening fiscal measures.

Changes to VAT rates or removal of tech-sector tax incentives would directly reduce free cash flow and reinvestment capacity for Fawry, which reported 2024 revenue of EGP 3.8 billion.

Proactive monitoring of fiscal policy is essential for pricing adjustments to protect competitiveness and maintain EBITDA margins (29% in 2024).

- New digital levies risk margin pressure

- VAT/corporate incentives affect reinvestment

- 2024 revenue EGP 3.8bn; EBITDA 29%

- Close policy monitoring required

Fawry dominates Egypt e-gov payments (>60%) as public flows ~EGP120bn; margin risks from new levies

Political support for Digital Egypt (EGP 15bn+ to 2025) and CBE regulation (EGP50k wallet cap; 12 fintech licenses in 2024) anchored Fawry’s government payment dominance—>60% e-gov transactions; ~EGP120bn public flows; public revenue 25–30% of 2024 revenue (EGP3.8bn; EBITDA 29%) while new digital levies and VAT shifts risk margin pressure.

| Metric | Value (2024–25) |

|---|---|

| Govt digital spend | EGP 15bn+ |

| Public flows | EGP 120bn |

| Share of e-gov txns | >60% |

| Revenue | EGP 3.8bn |

| EBITDA margin | 29% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Fawry across Political, Economic, Social, Technological, Environmental, and Legal dimensions, each backed by current data and regional industry trends to reveal actionable threats and opportunities for executives and investors.

A concise PESTLE snapshot tailored for Fawry that highlights key political, economic, social, technological, legal, and environmental risks and opportunities, enabling rapid alignment in meetings and clear, shareable insights for strategists and consultants.

Economic factors

Currency Volatility and Exchange Rate Management

The volatility of the Egyptian Pound directly affects Fawry’s asset valuations and hardware import costs; after the 2022-2024 depreciation and float adjustments that saw the EGP weaken roughly 40% vs USD, Fawry revised capital expenditure plans to reflect higher import costs. Following further adjustments into 2025, the company updated financial forecasts to buffer inflationary pressures—Egypt’s CPI ran near 32% in 2024—while hedging and FX clauses were strengthened. Effective foreign currency exposure management remains essential to preserve margins, reassure international shareholders, and support sustainable growth.

Impact of High Inflationary Pressures

Persistent inflation in Egypt (annual CPI ~26% in 2024) erodes household purchasing power, reducing the volume of discretionary e-commerce transactions routed via Fawry even as nominal bill values rise.

Higher prices lift average transaction amounts—supporting nominal fee revenues—but may depress transaction counts as consumers cut nonessential spending.

Fawry must fine-tune fee structures and promote low-cost payment options to protect margins while maintaining affordability for ~64 million mobile/internet users in Egypt (2024).

Interest Rate Fluctuations

The Central Bank of Egypt's policy rate, raised to 30.25% in March 2023 and held around 30% through 2024–25, directly affects Fawry's borrowing costs for expansion and its microfinance arm, increasing capital expenses while potentially widening lending margins. Higher rates elevate funding costs but can boost yields on Fawry's consumer credit and bill-payment financing, supporting net interest income. Fawry monitors CBE rate moves to adjust pricing, manage debt maturities, and calibrate consumer-credit product terms to protect profitability and liquidity.

Growth of the Informal Economy Transition

Egypt's informal economy remains large—estimated at about 40-50% of GDP pre-2024—and government drives to formalize present a major addressable market for Fawry, enabling onboarding of micro-enterprises and informal workers.

By 2025 Fawry reports growth in merchant count and active users, aided by outreach to unbanked segments (about 28% unbanked in 2023), increasing transaction frequency and ARPU on digital payment rails.

- Informal economy ~40–50% of GDP

- Unbanked ~28% (2023)

- Rising merchant/user adds driving transaction growth by 2025

Expansion into Microfinance and Credit Services

Fawry's move into microfinance and BNPL now contributes materially, with payment and lending revenues growing; in 2024 Fawry reported group transaction value surpassing EGP 200 billion and lending-related fees rising double digits year-on-year.

These services meet strong demand from SME owners and consumers facing tight liquidity; Egypt's consumer credit grew ~18% in 2023–2024, driving uptake of BNPL.

Performance hinges on robust credit scoring and Egyptian credit market conditions—non-performing loan ratios and bureau coverage will determine credit losses and margin sustainability.

- 2024 group TV > EGP 200bn

- Consumer credit growth ~18% (2023–24)

- Lending fees up double digits YoY

- Dependency: credit scoring quality and NPL trends

Egypt: Soaring costs, high rates and huge informal market fuel lending and digital growth

EGP depreciation (~40% vs USD since 2022) and 2024 CPI ~32% raised import and operating costs; CBE policy rate ~30% increased funding costs while supporting lending yields. Informal economy ~40–50% of GDP and ~28% unbanked (2023) create expansion opportunities; 2024 group transaction value >EGP 200bn, consumer credit growth ~18% (2023–24), lending fees up double digits YoY.

| Metric | Value |

|---|---|

| EGP weakening | ~40% vs USD (2022–24) |

| CPI 2024 | ~32% |

| CBE policy rate | ~30% |

| Informal economy | 40–50% GDP |

| Unbanked | ~28% (2023) |

| Group TV 2024 | >EGP 200bn |

| Consumer credit growth | ~18% (2023–24) |

Preview Before You Purchase

Fawry PESTLE Analysis

The preview shown here is the exact Fawry PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.