Myriad Group AG Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

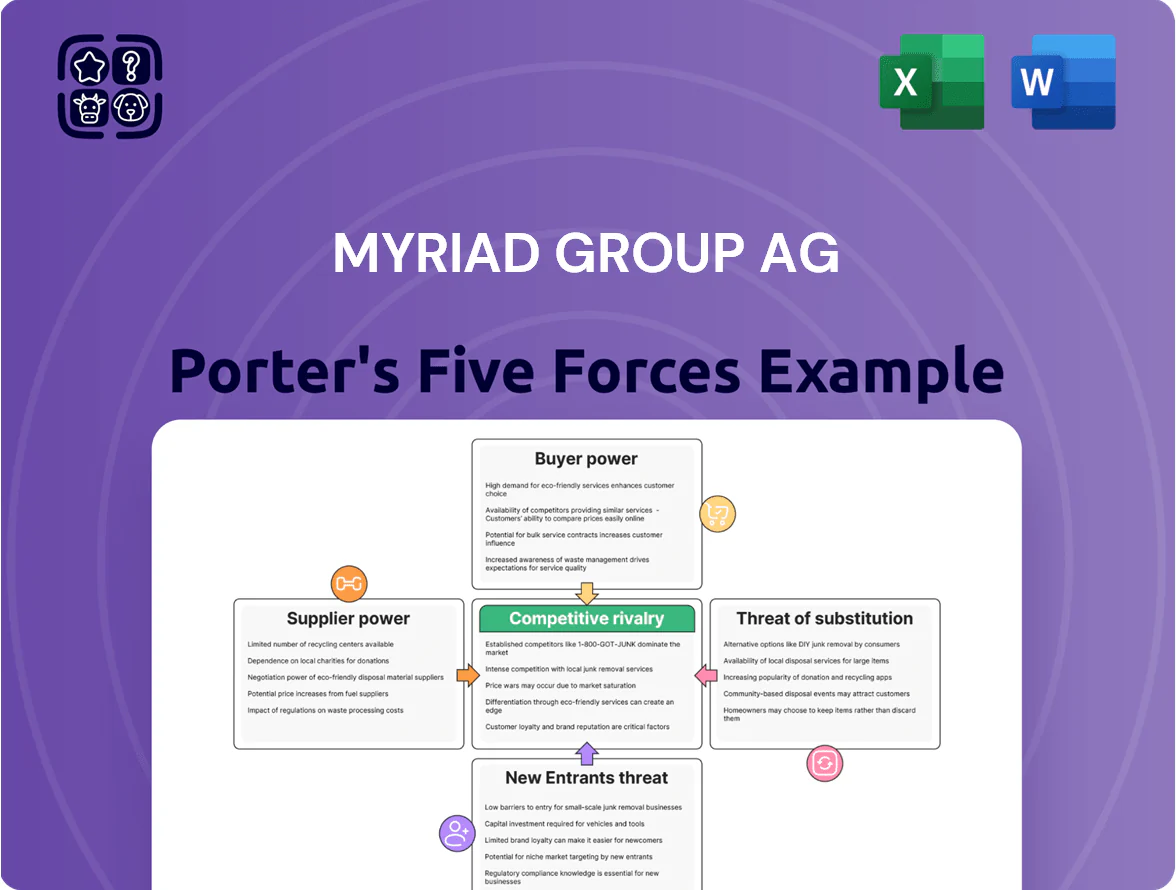

Myriad Group AG faces moderate competitive intensity driven by specialized product demand, concentrated suppliers for key components, and evolving regulatory pressures that shape margins and innovation incentives; buyer power is mixed due to niche clients but digital substitutes and new entrants pose growing threats. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Myriad Group AG’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Cloud Infrastructure Providers

Myriad depends on AWS and Azure for messaging and sync services, creating vendor concentration that raises supplier power; switching costs and technical debt are high—migrations often exceed $2–5m and 6–12 months for comparable stacks.

By late 2025, the top three cloud providers held ~65–70% market share, limiting Myriad’s bargaining leverage and keeping infrastructure unit costs sticky despite company growth.

Scarcity of Specialized Software Engineering Talent

At end-2025 demand for embedded systems and IoT protocol engineers outstrips supply; global vacancy rate for software engineering roles hit 4.1% in tech hubs and specialized IoT roles show 15% year-on-year hiring growth.

That narrow talent pool acts as powerful human-capital suppliers, pushing median embedded engineer pay up 22% in 2025 versus 2022.

Myriad must match market offers—cash, equity, training—to avoid losing staff to Big Tech and conserve product timelines and IP.

Licensing of Third-Party Intellectual Property

Many embedded software solutions need licenses for protocols or codecs owned by third parties; these suppliers can raise royalties or impose restrictive terms, squeezing Myriad Group AG’s gross margins—Myriad reported 2024 gross margin 46.2%, so a 1–3 p.p. royalty hike would cut absolute gross profit by €1.5–4.5m on €150m revenue. Maintaining compatibility forces continuous negotiations and legal costs, raising supplier dependency risk.

Dependence on Operating System Gatekeepers

Myriad Group AG depends on Google Android and Apple iOS as OS gatekeepers; in 2025 Android+iOS held ~99% global mobile OS share, so policy or API changes from these suppliers can halt features and revenue streams within weeks.

App-store fees and developer-program costs—Apple's 15–30% App Store cut and Google's similar fees—plus 2024–25 shifts to in-app payment rules materially raise unit economics and compliance costs for Myriad.

- ~99% market share: Android+iOS (2025)

- 15–30% typical app-store fee

- Policy changes can disrupt releases in weeks

- API access limits raise dev costs and reduce feature parity

Influence of Open Source Communities

Myriad relies on open-source components as indirect suppliers, with 40%+ of its 2024 codebase using OSS libraries, so community decisions materially affect product roadmaps.

Although OSS is free, shifts in major projects (Linux kernel, OpenSSL, React) force engineering pivots and cost Myriad estimated €1.2–1.8M annually in compatibility work in 2024.

Through 2025 Myriad must track upstream roadmaps and allocate ~12% of R&D to maintain standards compatibility and security backports.

- 40%+ OSS in codebase (2024)

- €1.2–1.8M yearly compatibility cost

- ~12% R&D budget for upkeep through 2025

High supplier power: cloud/OS concentration, rising talent & royalty costs

Supplier power is high: cloud vendor concentration (AWS/Azure ~65–70% top-3 share, 2025) and OS gatekeepers (Android+iOS ~99%) raise switching costs (~€2–5m, 6–12 months). Talent scarcity (embedded engineer pay +22% vs 2022) and licensing royalties (1–3 p.p. margin hit = €1.5–4.5m on €150m) plus 40%+ OSS dependence drive recurring compliance and compatibility costs.

| Metric | 2024–25 |

|---|---|

| Cloud top-3 share | 65–70% |

| Mobile OS share | ~99% |

| Switch cost | €2–5m, 6–12m |

| Embedded pay rise | +22% |

| OSS in codebase | 40%+ |

| Royalty impact | €1.5–4.5m |

What is included in the product

Tailored exclusively for Myriad Group AG, this Porter's Five Forces analysis uncovers competitive drivers, buyer and supplier influence, entry barriers, substitutes, and emerging threats to the company’s market share and profitability.

Concise Porter's Five Forces snapshot for Myriad Group AG—instantly highlights competitive pressures and strategic risks for quick boardroom decisions.

Customers Bargaining Power

Consolidation of Mobile Network Operators

Low Switching Costs for Device Manufacturers

Original equipment manufacturers (OEMs) choose among multiple browser and messaging vendors during design, so Myriad Group AG faces low switching costs: embedded tools can be replaced at contract renewal with relatively little friction. In 2024, global handset OEMs awarded ~15–25% of new device contracts to alternative UI vendors, forcing Myriad to invest R&D—its 2024 R&D spend rose to €6.8m, up 12%—to stay on new models.

Demand for Integrated IoT Ecosystems

Enterprise buyers increasingly prefer end-to-end IoT ecosystems, pushing demand away from standalone modules; IDC reported in 2024 that 62% of enterprises prioritize integrated platforms for IoT deployments.

These customers can push down prices for single software components unless vendors bundle services like device management, analytics, and SLAs—services that raise contract value by 18–25% on average per McKinsey 2023 estimates.

Myriad Group AG must justify its per-module pricing versus comprehensive suites from Amazon Web Services, Microsoft, and Google, which captured 48% of cloud-native IoT spend in 2024, squeezing margin on standalone offers.

Availability of Alternative Messaging Solutions

End-users and operators choose among many messaging platforms—WhatsApp (2+ billion users in 2024), RCS rollouts (GSMA: 100+ operators live by 2024) and niche apps—so customers can drop Myriad’s legacy tools if features lag.

That dynamic forces Myriad Group AG to spend heavily on R&D; global messaging platform R&D trends show vendors allocating ~10–15% of revenue to product development to stay competitive.

- Wide choice: 2B+ WhatsApp users, 100+ RCS operators by 2024

- Churn risk if features lag: high

- R&D need: ~10–15% revenue benchmark

Price Sensitivity in Emerging Markets

Myriad sells software for feature phones and low-cost devices in developing regions where over 60% of consumers cite price as the top purchase factor, capping licensing fees and squeezing margins.

To stay competitive, Myriad must optimize code for low-spec hardware and target sub-$50 devices, keeping per-unit software cost well below industry average royalties (around 2–4% of device price).

Consolidation, cloud power and low switching costs squeeze IoT margins—Myriad ups R&D

| Metric | 2024–25 |

|---|---|

| Top MNO revenue share | 60–70% |

| MNO consolidation | 4 major mergers by 2025 |

| OEM reassignments | 15–25% |

| Cloud IoT share (AWS/MS/Google) | 48% |

| Enterprise pref. integrated IoT | 62% |

| Myriad R&D | €6.8m (2024) |

Preview Before You Purchase

Myriad Group AG Porter's Five Forces Analysis

This preview shows the exact Myriad Group AG Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples; it covers supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry with actionable insights and concise valuation implications.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Myriad Group AG faces moderate competitive intensity driven by specialized product demand, concentrated suppliers for key components, and evolving regulatory pressures that shape margins and innovation incentives; buyer power is mixed due to niche clients but digital substitutes and new entrants pose growing threats. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Myriad Group AG’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Cloud Infrastructure Providers

Myriad depends on AWS and Azure for messaging and sync services, creating vendor concentration that raises supplier power; switching costs and technical debt are high—migrations often exceed $2–5m and 6–12 months for comparable stacks.

By late 2025, the top three cloud providers held ~65–70% market share, limiting Myriad’s bargaining leverage and keeping infrastructure unit costs sticky despite company growth.

Scarcity of Specialized Software Engineering Talent

At end-2025 demand for embedded systems and IoT protocol engineers outstrips supply; global vacancy rate for software engineering roles hit 4.1% in tech hubs and specialized IoT roles show 15% year-on-year hiring growth.

That narrow talent pool acts as powerful human-capital suppliers, pushing median embedded engineer pay up 22% in 2025 versus 2022.

Myriad must match market offers—cash, equity, training—to avoid losing staff to Big Tech and conserve product timelines and IP.

Licensing of Third-Party Intellectual Property

Many embedded software solutions need licenses for protocols or codecs owned by third parties; these suppliers can raise royalties or impose restrictive terms, squeezing Myriad Group AG’s gross margins—Myriad reported 2024 gross margin 46.2%, so a 1–3 p.p. royalty hike would cut absolute gross profit by €1.5–4.5m on €150m revenue. Maintaining compatibility forces continuous negotiations and legal costs, raising supplier dependency risk.

Dependence on Operating System Gatekeepers

Myriad Group AG depends on Google Android and Apple iOS as OS gatekeepers; in 2025 Android+iOS held ~99% global mobile OS share, so policy or API changes from these suppliers can halt features and revenue streams within weeks.

App-store fees and developer-program costs—Apple's 15–30% App Store cut and Google's similar fees—plus 2024–25 shifts to in-app payment rules materially raise unit economics and compliance costs for Myriad.

- ~99% market share: Android+iOS (2025)

- 15–30% typical app-store fee

- Policy changes can disrupt releases in weeks

- API access limits raise dev costs and reduce feature parity

Influence of Open Source Communities

Myriad relies on open-source components as indirect suppliers, with 40%+ of its 2024 codebase using OSS libraries, so community decisions materially affect product roadmaps.

Although OSS is free, shifts in major projects (Linux kernel, OpenSSL, React) force engineering pivots and cost Myriad estimated €1.2–1.8M annually in compatibility work in 2024.

Through 2025 Myriad must track upstream roadmaps and allocate ~12% of R&D to maintain standards compatibility and security backports.

- 40%+ OSS in codebase (2024)

- €1.2–1.8M yearly compatibility cost

- ~12% R&D budget for upkeep through 2025

High supplier power: cloud/OS concentration, rising talent & royalty costs

Supplier power is high: cloud vendor concentration (AWS/Azure ~65–70% top-3 share, 2025) and OS gatekeepers (Android+iOS ~99%) raise switching costs (~€2–5m, 6–12 months). Talent scarcity (embedded engineer pay +22% vs 2022) and licensing royalties (1–3 p.p. margin hit = €1.5–4.5m on €150m) plus 40%+ OSS dependence drive recurring compliance and compatibility costs.

| Metric | 2024–25 |

|---|---|

| Cloud top-3 share | 65–70% |

| Mobile OS share | ~99% |

| Switch cost | €2–5m, 6–12m |

| Embedded pay rise | +22% |

| OSS in codebase | 40%+ |

| Royalty impact | €1.5–4.5m |

What is included in the product

Tailored exclusively for Myriad Group AG, this Porter's Five Forces analysis uncovers competitive drivers, buyer and supplier influence, entry barriers, substitutes, and emerging threats to the company’s market share and profitability.

Concise Porter's Five Forces snapshot for Myriad Group AG—instantly highlights competitive pressures and strategic risks for quick boardroom decisions.

Customers Bargaining Power

Consolidation of Mobile Network Operators

Low Switching Costs for Device Manufacturers

Original equipment manufacturers (OEMs) choose among multiple browser and messaging vendors during design, so Myriad Group AG faces low switching costs: embedded tools can be replaced at contract renewal with relatively little friction. In 2024, global handset OEMs awarded ~15–25% of new device contracts to alternative UI vendors, forcing Myriad to invest R&D—its 2024 R&D spend rose to €6.8m, up 12%—to stay on new models.

Demand for Integrated IoT Ecosystems

Enterprise buyers increasingly prefer end-to-end IoT ecosystems, pushing demand away from standalone modules; IDC reported in 2024 that 62% of enterprises prioritize integrated platforms for IoT deployments.

These customers can push down prices for single software components unless vendors bundle services like device management, analytics, and SLAs—services that raise contract value by 18–25% on average per McKinsey 2023 estimates.

Myriad Group AG must justify its per-module pricing versus comprehensive suites from Amazon Web Services, Microsoft, and Google, which captured 48% of cloud-native IoT spend in 2024, squeezing margin on standalone offers.

Availability of Alternative Messaging Solutions

End-users and operators choose among many messaging platforms—WhatsApp (2+ billion users in 2024), RCS rollouts (GSMA: 100+ operators live by 2024) and niche apps—so customers can drop Myriad’s legacy tools if features lag.

That dynamic forces Myriad Group AG to spend heavily on R&D; global messaging platform R&D trends show vendors allocating ~10–15% of revenue to product development to stay competitive.

- Wide choice: 2B+ WhatsApp users, 100+ RCS operators by 2024

- Churn risk if features lag: high

- R&D need: ~10–15% revenue benchmark

Price Sensitivity in Emerging Markets

Myriad sells software for feature phones and low-cost devices in developing regions where over 60% of consumers cite price as the top purchase factor, capping licensing fees and squeezing margins.

To stay competitive, Myriad must optimize code for low-spec hardware and target sub-$50 devices, keeping per-unit software cost well below industry average royalties (around 2–4% of device price).

Consolidation, cloud power and low switching costs squeeze IoT margins—Myriad ups R&D

| Metric | 2024–25 |

|---|---|

| Top MNO revenue share | 60–70% |

| MNO consolidation | 4 major mergers by 2025 |

| OEM reassignments | 15–25% |

| Cloud IoT share (AWS/MS/Google) | 48% |

| Enterprise pref. integrated IoT | 62% |

| Myriad R&D | €6.8m (2024) |

Preview Before You Purchase

Myriad Group AG Porter's Five Forces Analysis

This preview shows the exact Myriad Group AG Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples; it covers supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry with actionable insights and concise valuation implications.